Reports

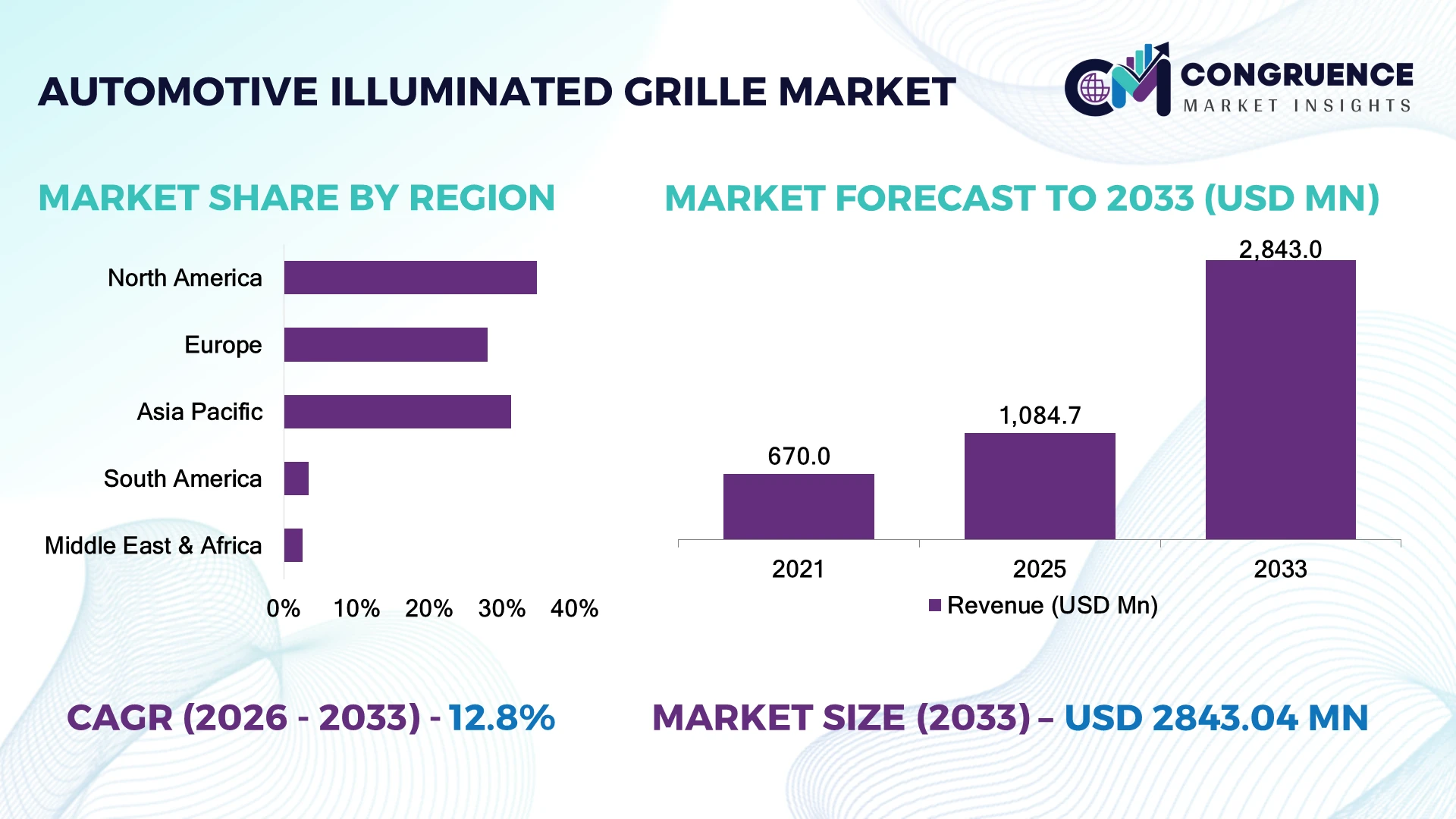

The Global Automotive Illuminated Grille Market was valued at USD 1,084.7 Million in 2025 and is anticipated to reach a value of USD 2,843.0 Million by 2033 expanding at a CAGR of 12.8% between 2026 and 2033. Growth is being driven by rising integration of illuminated brand signatures in electric and premium vehicles, stricter vehicle differentiation strategies, and advances in energy-efficient LED lighting modules integrated with smart front-end architectures.

China leads the global Automotive Illuminated Grille Market with approximately 36% production share, supported by large-scale EV manufacturing, intelligent lighting component ecosystems, and continued automotive investments exceeding USD 40 billion across advanced manufacturing initiatives. Compared with Germany, China delivers significantly higher production volumes, while Germany maintains leadership in premium automotive lighting engineering. Ongoing global supply-chain diversification following geopolitical trade realignments continues accelerating localized component sourcing.

Strategic investment in intelligent lighting platforms and regional manufacturing partnerships is becoming essential for securing long-term competitive positioning.

Market Size & Growth: Valued at USD 1,084.7 Million in 2025 and projected to reach USD 2,843.0 Million by 2033 at a CAGR of 12.8%, driven by expanding EV production and advanced vehicle styling integration.

Top Growth Drivers: EV adoption (+31%), premium vehicle demand (+18%), and intelligent exterior lighting penetration (+22%) continue accelerating market expansion.

Short-Term Forecast: By 2028, LED module manufacturing efficiency improves by 16%, while assembly costs decline by approximately 11% through production automation.

Emerging Technologies: AI-enabled lighting control, adaptive LED systems, and lightweight composite grille structures improve energy efficiency by nearly 14%.

Regional Leaders: Asia-Pacific approaches USD 1.28 Billion, Europe exceeds USD 760 Million, and North America surpasses USD 540 Million, supported by premium vehicle electrification and regional manufacturing expansion.

Consumer/End-User Trends: Nearly 47% of premium vehicle buyers prefer illuminated front-end styling, strengthening OEM differentiation strategies.

Pilot/Case Example: A 2026 intelligent lighting deployment program reduced assembly complexity by 13% through modular front-end integration.

Competitive Landscape: The top five companies collectively control around 54% market share, with Valeo, Marelli, FORVIA HELLA, Magna International, and OPmobility leading innovation.

Regulatory & ESG Impact: Vehicle lighting regulations and ESG-focused manufacturing initiatives reduce lighting power consumption by approximately 18% across next-generation platforms.

Investment & Funding: Industry investments exceed USD 2.6 Billion, driven by supplier partnerships, regional manufacturing expansion, and resilient supply-chain localization.

Innovation & Future Outlook: Software-defined lighting, customizable illuminated logos, and connected vehicle interfaces are reshaping competitive product strategies across the global automotive industry.

Automotive illuminated grilles are becoming a defining feature across electric, luxury, and connected vehicles as manufacturers strengthen exterior brand identity through programmable lighting systems. Advanced micro-LED technologies and integrated sensor-compatible grille designs now account for nearly 28% of new premium platform developments. Regional component localization and evolving vehicle lighting regulations continue influencing design, procurement, and production strategies, setting the stage for broader strategic transformation.

The Automotive Illuminated Grille Market has become strategically important as vehicle manufacturers increasingly compete through distinctive exterior design, intelligent lighting integration, and premium customer experience. Electrification has eliminated conventional radiator requirements in many vehicle platforms, creating new opportunities for illuminated front-end designs that reinforce brand identity. At the same time, regional supply-chain restructuring is encouraging manufacturers to localize LED modules, electronic controllers, and optical components to improve production resilience and shorten lead times.

Advanced programmable LED grille systems consume approximately 20% less energy than conventional lighting assemblies while providing higher brightness uniformity, longer service life, and software-controlled lighting functions. Asia-Pacific leads large-scale manufacturing and supplier integration, whereas Europe continues emphasizing premium innovation, regulatory compliance, and advanced automotive design. Over the next two to three years, intelligent lighting integration across premium and upper mid-range vehicles is expected to expand steadily as digital vehicle architectures become standard.

Automotive manufacturers are increasingly deploying modular illuminated grille platforms that simplify assembly, reduce component variation, and accelerate vehicle customization. Companies are strengthening partnerships with lighting specialists, electronics suppliers, and software developers while expanding regional production capabilities to support localized manufacturing. This combination of operational flexibility, design differentiation, and intelligent lighting capability positions illuminated grilles as a long-term competitive asset within next-generation vehicle development strategies.

Automotive manufacturers are accelerating illuminated grille integration as exterior lighting becomes a key vehicle differentiation strategy, particularly across electric and premium models. Nearly 52% of newly introduced EV platforms incorporate illuminated front-end identity elements, while programmable lighting features improve brand recognition by approximately 30% during low-visibility conditions. China continues expanding intelligent vehicle manufacturing through advanced lighting supply clusters, supported by increasing localization of LED electronics and optical modules. This shift enables faster product development cycles and lower sourcing risks. In response, component suppliers are investing in smart lighting software, modular grille architectures, and OEM partnerships to deliver scalable, customizable solutions. The resulting transition from decorative styling to software-enabled exterior communication is strengthening competitive positioning and increasing value across next-generation vehicle platforms.

High dependence on advanced LEDs, optical light guides, electronic control units, and precision molding continues limiting cost competitiveness, particularly in mid-range vehicle segments. Premium illuminated grille systems typically increase front-end component costs by 18–24%, while semiconductor-related electronics still account for nearly 35% of total module value. Periodic supply disruptions affecting specialized lighting chips and optical materials have extended procurement timelines for several global manufacturers. These structural pressures reduce deployment flexibility and compress supplier margins during vehicle launch programs. Companies are mitigating risks by localizing electronics production, establishing multi-source procurement contracts, and redesigning lighting modules with standardized components that improve manufacturing efficiency while reducing exposure to single-country supply dependencies.

The emergence of software-defined vehicles is creating new opportunities for intelligent illuminated grille systems capable of delivering dynamic lighting signatures, welcome animations, and vehicle-to-user communication. More than 40% of premium vehicle development programs now prioritize programmable exterior lighting, while over 26% of new lighting platforms are designed for over-the-air software updates. Germany is advancing automotive digitalization through integrated vehicle electronics and functional lighting innovation, encouraging greater software-lighting convergence. Suppliers are expanding R&D investments, collaborating with semiconductor developers, and building scalable lighting control ecosystems. A significant strategic opportunity lies in transforming illuminated grilles from fixed styling components into upgradeable digital features that generate long-term product differentiation without extensive hardware redesign.

Integrating illuminated grille systems with vehicle electronics, ADAS sensors, thermal management, and cybersecurity architectures presents a growing engineering challenge for automotive manufacturers. Around 32% of product development time is now dedicated to system validation and electronic compatibility testing, while software verification activities have increased by nearly 22% across connected vehicle programs. Japan's automotive industry is emphasizing functional safety and electronic reliability, requiring increasingly rigorous validation processes before commercialization. These technical demands extend development schedules and increase engineering complexity across multi-platform vehicle programs. Companies must strengthen cross-functional software expertise, digital simulation capabilities, and supplier collaboration to ensure consistent performance while maintaining scalability across diverse vehicle architectures.

Programmable Brand Identity Expansion: Vehicle manufacturers are replacing static front-end styling with programmable illuminated grilles, with nearly 44% of premium launches now supporting customizable lighting sequences and approximately 27% faster software-based personalization. Digital vehicle platforms enable feature updates without hardware replacement, reducing engineering changes during production. Manufacturers are scaling software partnerships and centralized lighting controllers to simplify deployment across multiple vehicle platforms.

Localized Lighting Supply Networks: Supply-chain diversification is reshaping component sourcing as China and Mexico expand production of LED modules, optical guides, and electronic controllers. Localized procurement has reduced logistics lead times by around 19%, while inventory availability has improved by 16% for several automotive programs. Companies are restructuring supplier networks and increasing regional manufacturing capacity to strengthen operational resilience against geopolitical trade disruptions.

Sensor-Compatible Front-End Designs: Illuminated grille assemblies are increasingly engineered to accommodate radar and camera integration without compromising lighting performance. Advanced optical materials improve signal transmission efficiency by approximately 12%, while modular front-end assemblies reduce installation complexity by nearly 15%. OEMs are collaborating with sensor and lighting specialists to standardize multifunctional grille architectures that support autonomous driving technologies and simplify vehicle assembly workflows.

Energy-Efficient Lighting Architectures: Manufacturers are transitioning toward high-efficiency micro-LEDs, intelligent power management, and lightweight composite structures that reduce lighting energy consumption by approximately 18% and component weight by 11%. Tightening vehicle efficiency requirements are accelerating this transition, particularly in electric vehicle programs. Companies are expanding automated production lines and advanced material partnerships to improve manufacturing consistency while lowering lifecycle operating costs.

LED Illuminated Grilles account for approximately 68% of the Automotive Illuminated Grille Market, making them the leading segment due to superior energy efficiency, long operating life, compact packaging, and seamless integration with vehicle electronics. OEMs increasingly standardize LED-based grille systems across premium electric and luxury vehicles because they support programmable lighting signatures and lower maintenance requirements. Dynamic Illuminated Grilles represent the fastest-growing segment, driven by software-defined vehicle architectures and demand for customizable lighting animations. Static Illuminated Grilles continue serving mainstream vehicle platforms where cost optimization remains a priority, while laser-based and advanced optical solutions are gaining selective adoption in flagship models requiring premium visual differentiation. Companies are expanding intelligent lighting portfolios, strengthening semiconductor partnerships, and investing in modular electronic architectures to improve scalability and accelerate platform integration.

As vehicle lighting evolves into a digital interface, investment priorities are shifting from standalone illumination hardware toward software-controlled lighting ecosystems capable of supporting future vehicle communication features. Manufacturers in Germany and China are increasingly aligning product development with intelligent exterior lighting platforms that simplify cross-platform deployment while improving design flexibility.

According to the 2025 International Automotive Lighting and Light Signalling Expert Symposium (ISAL), intelligent exterior lighting is increasingly being integrated into vehicle communication strategies, with programmable LED technologies becoming a primary focus for next-generation automotive front-end design.

OEM applications represent approximately 81% of total demand as illuminated grilles are increasingly integrated during vehicle design rather than installed after production. Vehicle manufacturers prioritize factory-installed lighting systems to ensure seamless electronic integration, functional safety compliance, and consistent brand identity across model portfolios. The Aftermarket segment is expanding at the fastest pace as consumers seek premium vehicle customization through retrofit illuminated grille kits, particularly across pickup trucks, SUVs, and luxury passenger vehicles. Nearly 34% of premium customization projects now include illuminated exterior components, reflecting stronger personalization trends. Companies are responding by expanding OEM development programs while simultaneously launching modular aftermarket solutions that simplify installation and compatibility across multiple vehicle platforms.

Demand is becoming increasingly concentrated within factory-installed intelligent lighting systems as software integration, warranty coverage, and electronic reliability remain major purchasing priorities. At the same time, aftermarket suppliers are improving digital configuration tools and expanding distribution partnerships to capture customization-driven demand in mature automotive markets.

Findings presented by the 2026 Society of Automotive Engineers (SAE International) indicate that integrated exterior lighting systems are becoming a standard design priority within next-generation vehicle development programs as electronic architecture complexity continues increasing.

Passenger Vehicle OEMs account for approximately 74% of Automotive Illuminated Grille deployments due to high production volumes, premium model expansion, and increasing adoption of brand-specific lighting signatures. Electric passenger vehicle manufacturers represent the fastest-growing end-user group as illuminated front-end designs replace conventional radiator grilles and enhance vehicle identity. Luxury automotive manufacturers continue investing in advanced programmable lighting, while commercial vehicle manufacturers selectively adopt illuminated grilles for premium fleet and specialty applications. Aftermarket customization businesses maintain growing relevance, supported by nearly 21% higher demand for vehicle personalization products across developed automotive markets. Companies are addressing these customer groups through differentiated pricing strategies, platform-specific product customization, and long-term OEM development partnerships.

Competitive positioning increasingly depends on offering scalable lighting platforms tailored to multiple customer groups rather than single-vehicle programs. Suppliers are expanding engineering collaboration with passenger vehicle manufacturers while strengthening aftermarket distribution networks to diversify revenue opportunities and improve lifecycle product support.

According to the 2025 OICA (International Organization of Motor Vehicle Manufacturers), passenger vehicles continue to represent the overwhelming majority of global vehicle production, reinforcing OEM investment priorities in advanced exterior lighting technologies and vehicle differentiation features.

North America accounted for the largest market share at 34.8%in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 14.2% between 2026 and 2033.

Premium Vehicle Innovation and Intelligent Lighting Leadership

North America maintains the largest share of the Automotive Illuminated Grille Market through strong premium vehicle production, rapid electric vehicle deployment, and advanced automotive electronics integration. The region represents nearly 35% of global demand, supported by high adoption of software-defined vehicle platforms and premium exterior lighting technologies. OEMs increasingly deploy illuminated grille systems to strengthen vehicle branding and improve digital user interaction. More than 46% of newly launched premium EV models in the region feature illuminated front-end lighting elements. Automotive suppliers continue expanding local electronics production while strengthening partnerships with lighting technology specialists to reduce supply-chain risks and accelerate product development across multiple vehicle platforms.

United States Market Outlook: The United States leads regional demand through its strong premium vehicle manufacturing base, advanced automotive software ecosystem, and expanding electric vehicle production. Nearly 48% of North America's premium vehicle assembly is concentrated in the country, encouraging greater deployment of intelligent lighting systems. Leading OEMs are integrating programmable illuminated grilles into next-generation electric SUVs and luxury vehicles while suppliers continue investing in localized electronics manufacturing and advanced lighting validation facilities to support long-term product innovation.

Premium Automotive Engineering Accelerates Intelligent Exterior Design

Europe remains a technology-driven market supported by luxury vehicle manufacturing, stringent vehicle safety standards, and advanced automotive lighting engineering. The region accounts for approximately 28% of global demand, with Germany, France, and Italy driving premium vehicle production. Intelligent exterior lighting has become an important product differentiation strategy as software-controlled lighting systems gain wider deployment. Several automotive suppliers have expanded intelligent lighting engineering centers to improve system integration and accelerate development of multifunctional front-end architectures supporting connected and electric vehicles.

Germany Market Outlook: Germany remains Europe's strategic hub for premium automotive manufacturing and intelligent lighting innovation. Major luxury vehicle manufacturers continue integrating illuminated grille systems across flagship electric models while strengthening collaboration with electronics and lighting suppliers. Around 40% of the region's premium vehicle development activities are concentrated in Germany, supporting continuous innovation in programmable lighting technologies, digital vehicle architecture, and advanced manufacturing processes.

Manufacturing Scale and EV Expansion Drive Adoption

Asia-Pacific represents the fastest-expanding Automotive Illuminated Grille Market due to its extensive automotive manufacturing capacity, strong electric vehicle production, and rapidly evolving supplier ecosystem. The region contributes nearly 41% of global vehicle production, creating significant opportunities for intelligent lighting integration across passenger vehicles. China, Japan, and South Korea continue strengthening localized semiconductor, LED, and automotive electronics manufacturing. Several lighting component manufacturers have expanded production facilities to support growing OEM demand while reducing dependence on imported electronic components and shortening production lead times.

China Market Outlook: China leads the regional market through unmatched electric vehicle production, integrated automotive supply chains, and large-scale electronics manufacturing. More than 55% of regional EV production is concentrated in China, accelerating deployment of illuminated grille technologies across domestic and international vehicle brands. Local suppliers continue investing in intelligent lighting controllers, advanced LED packaging, and automated manufacturing systems to improve production efficiency and strengthen export competitiveness.

Premium Vehicle Customization Supports Market Development

South America is experiencing gradual adoption of illuminated grille technologies as premium passenger vehicle sales and vehicle customization activities continue expanding. Brazil and Argentina account for the majority of automotive manufacturing within the region, supporting selective deployment of advanced exterior lighting systems. Approximately 18% of premium vehicle customization programs now include illuminated front-end components. While supply-chain limitations and dependence on imported electronics remain operational challenges, distributors and automotive suppliers are expanding regional partnerships and localized assembly capabilities to improve product availability and reduce procurement delays.

Brazil Market Outlook: Brazil serves as the region's primary automotive manufacturing center, supported by established assembly facilities and a growing premium vehicle market. Domestic distributors are expanding partnerships with international lighting component suppliers while increasing local assembly activities for vehicle accessories. Continued investment in automotive manufacturing modernization and rising consumer preference for premium vehicle styling are strengthening long-term demand for intelligent exterior lighting technologies.

Luxury Vehicle Investment Strengthens Intelligent Lighting Demand

The Middle East & Africa market is supported by expanding luxury vehicle imports, automotive retail modernization, and increasing investment in premium mobility solutions. Gulf countries continue driving demand for advanced exterior lighting features, while South Africa remains an important automotive manufacturing base. Premium vehicle registrations have increased by approximately 15% across key Gulf markets, encouraging wider deployment of illuminated grille systems. Automotive distributors are strengthening supplier partnerships while expanding specialized installation and service capabilities to support technologically advanced vehicle platforms.

United Arab Emirates Market Outlook: The United Arab Emirates leads regional demand through its strong luxury automotive market, premium consumer base, and advanced vehicle retail ecosystem. High adoption of premium electric and luxury vehicles continues supporting intelligent exterior lighting deployment. Automotive dealers and customization specialists are expanding partnerships with global lighting technology providers while investing in advanced installation capabilities to meet growing demand for digitally integrated vehicle styling solutions.

The Automotive Illuminated Grille Market is led by global lighting specialists including Valeo, FORVIA HELLA, Magna International, OPmobility, and Marelli, which compete directly on intelligent lighting integration, while regional suppliers primarily compete through manufacturing cost and localization. The top five players collectively account for approximately 54% of market share, reflecting moderate industry consolidation. Competition centers on software-enabled lighting, optical performance, and integrated sensor compatibility rather than component pricing alone. Companies delivering modular lighting platforms reduce vehicle integration time by nearly 18%, while localized supply chains shorten lead times by approximately 15% and automated production lowers manufacturing costs by around 12%. Leading suppliers are expanding engineering centers, forming semiconductor partnerships, and vertically integrating electronics capabilities to strengthen OEM relationships. The competitive landscape is shifting toward software-defined exterior lighting and multifunctional front-end modules. High validation requirements, intellectual property, and OEM qualification cycles remain major entry barriers. Winning requires scalable technology, manufacturing resilience, and deep vehicle platform integration.

Valeo

FORVIA HELLA

Magna International Inc.

Marelli Holdings Co., Ltd.

OPmobility

SL Corporation

Koito Manufacturing Co., Ltd.

Stanley Electric Co., Ltd.

Varroc Engineering Limited

ZKW Group GmbH

Xingyu Automotive Lighting Systems Co., Ltd.

Hyundai Mobis Co., Ltd.

Automotive illuminated grille technology is evolving from decorative lighting toward intelligent front-end communication systems. Advanced micro-LEDs, adaptive light guides, and programmable lighting controllers now enable dynamic welcome animations, charging indicators, and brand-specific signatures. Nearly 46% of premium vehicle platforms incorporate software-controlled exterior lighting, while micro-LED architectures improve luminous efficiency by approximately 18% compared with conventional LED modules. Manufacturers benefit from greater design flexibility and lower power consumption without increasing system complexity.

The strongest technology transition is the integration of lighting, sensing, and electronics into unified front-end modules. Compared with conventional standalone grille lighting, integrated smart modules reduce component count by around 20% while shortening vehicle assembly time by nearly 15%. Premium OEMs and advanced lighting suppliers gain the greatest competitive advantage through simplified vehicle architecture, enhanced sensor compatibility, and faster platform standardization. AI-enabled lighting controllers, radar-transparent materials, and over-the-air configurable lighting functions are becoming standard development priorities.

Between 2026 and 2028, programmable lighting ecosystems, digital vehicle architectures, and multifunctional front-end modules will reshape competitive positioning. Adoption of software-defined lighting is expected to exceed 55% across newly launched premium electric vehicle platforms. Companies investing in semiconductor partnerships, intelligent lighting software, and modular electronics will improve product scalability, accelerate vehicle development, and strengthen long-term differentiation as exterior lighting becomes an active communication interface rather than a passive styling element.

September 2025 – Valeo partnered with Ennostar to introduce a Mini LED High Definition automotive exterior display at IAA Mobility, enhancing digital vehicle communication through advanced Mini LED technology with improved brightness and energy efficiency. Source: Valeo

August 2025 – Mercedes-Benz unveiled its next-generation Iconic Grille for the electric GLC with EQ Technology, integrating 942 illuminated pixels into the front fascia to strengthen digital brand identity and exterior vehicle communication. Source: Mercedes-Benz Group

March 2026 – FORVIA HELLA entered series production of the world's first Front Phygital Shield for the BMW iX3, integrating illuminated grille elements, LED headlamps, and radar sensors into a single module, reducing front-end component complexity through multifunctional integration. Source: FORVIA HELLA

March 2026 – BMW expanded deployment of illuminated kidney grille technology within its Neue Klasse platform, replacing conventional chrome-focused front-end design with digitally integrated lighting architecture supporting next-generation electric vehicle identity. Source: Autoblog.

This report provides comprehensive analysis of the Automotive Illuminated Grille Market across product types, applications, end-users, and major geographic regions. It evaluates LED-enabled, dynamic, static, and advanced lighting technologies while assessing OEM and aftermarket deployment trends together with passenger and commercial vehicle demand. The study examines adoption patterns, manufacturing concentration, intelligent lighting integration, software-defined vehicle platforms, and competitive participation across more than 12 leading industry companies.

The report delivers strategic insights supporting investment planning, product development, geographic expansion, and competitive positioning between 2026 and 2033. It assesses regional manufacturing dynamics, supply-chain evolution, technology adoption, and emerging opportunities in intelligent exterior lighting. Coverage extends to digital lighting architectures, sensor-integrated front-end modules, vehicle customization trends, and next-generation communication-enabled lighting systems, enabling decision-makers to identify high-potential segments, operational priorities, and long-term competitive strategies across the global automotive ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 1,084.7 Million |

|

Market Revenue in 2033 |

USD 2,843.0 Million |

|

CAGR (2026 - 2033) |

12.8% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Valeo, FORVIA HELLA, Magna International Inc., Marelli Holdings Co., Ltd., OPmobility, SL Corporation, Koito Manufacturing Co., Ltd., Stanley Electric Co., Ltd., Varroc Engineering Limited, ZKW Group GmbH, Xingyu Automotive Lighting Systems Co., Ltd., Hyundai Mobis Co., Ltd. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |