Reports

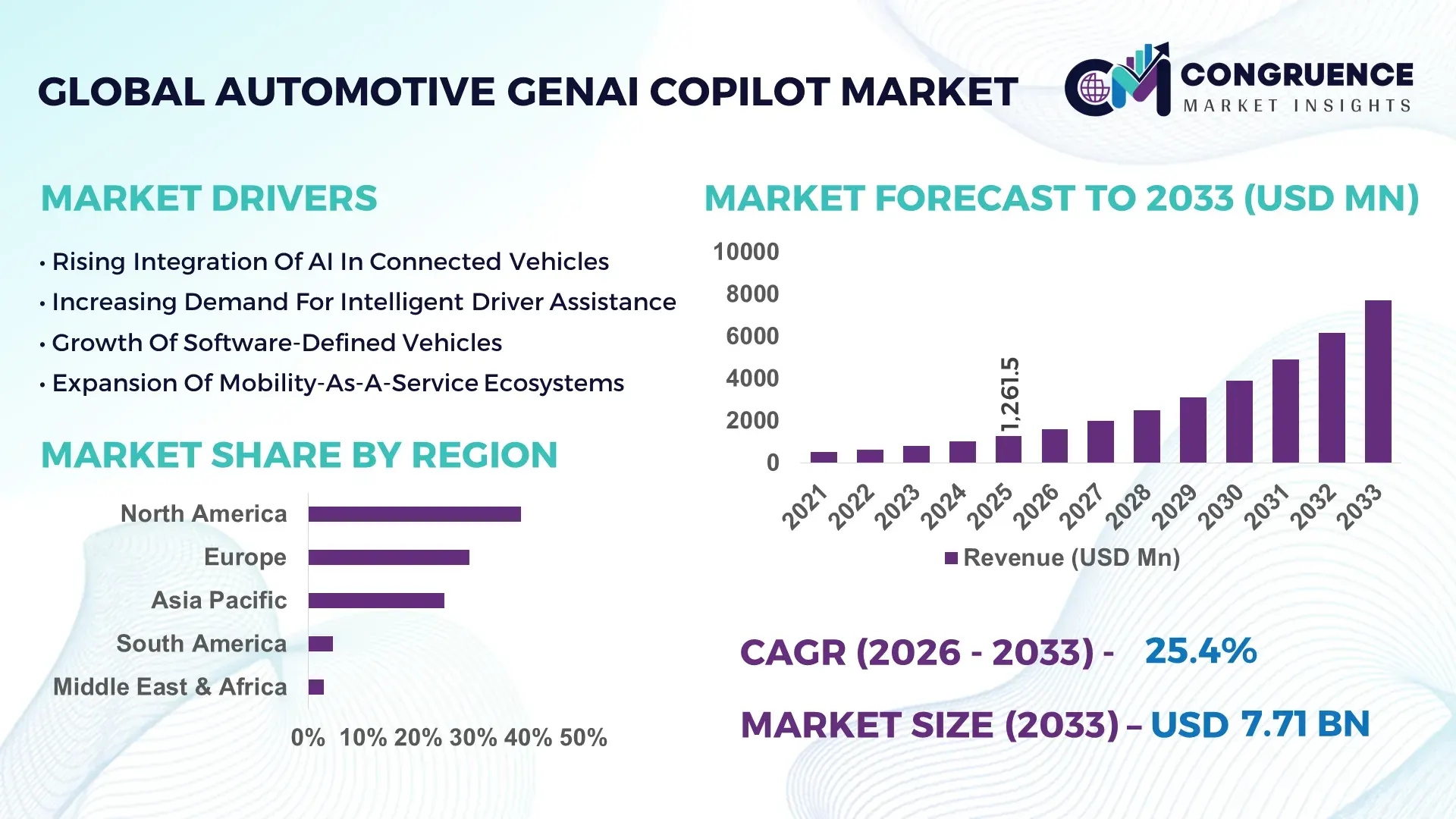

The Global Automotive GenAI Copilot Market was valued at USD 1,261.5 Million in 2025 and is anticipated to reach a value of USD 7,713.8 Million by 2033 expanding at a CAGR of 25.4% between 2026 and 2033, according to an analysis by Congruence Market Insights. Growth is driven by rapid integration of generative AI into in-vehicle infotainment and advanced driver assistance systems.

The United States represents a technologically advanced Automotive GenAI Copilot market, supported by over 2,700 AI-focused automotive technology firms and strong OEM–tech partnerships. Investments in AI-enabled automotive software exceeded USD 9.4 billion during 2024–2025, with in-vehicle infotainment applications accounting for approximately 41% of deployments, followed by driver assistance systems at 33% and predictive maintenance at 18%. Over 58% of new premium vehicles incorporate AI-powered copilots with natural language interfaces, while edge AI processing adoption increased by 36%, improving real-time responsiveness and reducing latency in connected vehicle ecosystems.

Market Size & Growth: USD 1,261.5 million in 2025, projected to reach USD 7,713.8 million by 2033, driven by intelligent in-vehicle AI integration.

Top Growth Drivers: Connected vehicle adoption (61%), AI-driven infotainment demand (48%), ADAS integration (39%).

Short-Term Forecast: By 2028, GenAI copilots are expected to improve driver interaction efficiency by 35%.

Emerging Technologies: Large language models in vehicles, edge AI processing, multimodal human-machine interfaces.

Regional Leaders: North America projected at USD 2.8 billion by 2033 with premium vehicle integration; Europe at USD 2.1 billion driven by safety compliance; Asia-Pacific at USD 1.9 billion supported by EV growth.

Consumer/End-User Trends: Over 64% of consumers prefer AI-enabled voice assistants in vehicles.

Pilot or Case Example: In 2024, an OEM pilot improved in-car voice command accuracy by 38%.

Competitive Landscape: NVIDIA leads with ~18% share, followed by Qualcomm, Bosch, Continental, and Google.

Regulatory & ESG Impact: Vehicle safety regulations and carbon reduction goals influencing AI adoption.

Investment & Funding Patterns: Over USD 10.5 billion invested globally in automotive AI technologies between 2023–2025.

Innovation & Future Outlook: AI copilots evolving toward autonomous driving assistance and personalized mobility experiences.

Automotive GenAI Copilot adoption is led by passenger vehicles (62%), followed by commercial vehicles (24%) and shared mobility fleets (14%). Innovations in voice recognition, predictive analytics, and multimodal interaction are enhancing user experience and safety. Regulatory frameworks for vehicle safety and emissions are accelerating adoption, while emerging markets are integrating AI copilots into electric and connected vehicles.

The Automotive GenAI Copilot Market is strategically redefining in-vehicle intelligence by enabling real-time decision-making, enhanced driver interaction, and personalized mobility experiences. Large language model-based copilots deliver up to 44% improvement compared to traditional rule-based voice assistants, significantly enhancing contextual understanding and response accuracy in automotive environments.

North America dominates in volume due to strong OEM integration and technology partnerships, while Asia-Pacific leads in adoption with over 57% of connected vehicles incorporating AI-enabled copilots. By 2027, multimodal AI systems combining voice, vision, and sensor data are expected to improve driver assistance accuracy by 36%, enhancing safety and user experience.

From an ESG perspective, automotive companies are committing to sustainability goals, including a 28% reduction in energy consumption of onboard computing systems and increased adoption of energy-efficient AI chips by 2030. In 2024, a leading automotive manufacturer in Germany achieved a 32% improvement in driver assistance efficiency through AI-driven copilot integration.

Strategically, integration of Automotive GenAI Copilot systems with cloud platforms, edge computing, and advanced sensors is expanding capabilities. By 2028, AI copilots are expected to enhance vehicle autonomy levels and reduce driver workload by 39%. These advancements position the Automotive GenAI Copilot Market as a critical pillar of intelligent mobility, regulatory compliance, and sustainable automotive innovation.

The Automotive GenAI Copilot market dynamics are driven by rapid advancements in artificial intelligence, increasing adoption of connected vehicles, and growing demand for enhanced driver experiences. Automotive GenAI Copilot systems leverage machine learning, natural language processing, and real-time data analytics to provide intelligent assistance to drivers. The integration of AI into infotainment systems and advanced driver assistance systems is transforming vehicle functionality. Additionally, the rise of electric and autonomous vehicles is accelerating demand for AI-powered copilots. Regulatory requirements for vehicle safety and emissions are further influencing market adoption. Competitive pressures and technological innovation are encouraging manufacturers to develop advanced AI solutions, enhancing performance and user experience.

The rise of connected vehicles is a major driver of the Automotive GenAI Copilot market. Over 70% of new vehicles are equipped with connectivity features, enabling integration of AI-powered copilots. These systems enhance driver interaction, improve navigation, and provide real-time assistance. AI copilots can improve user experience by up to 40% and increase operational efficiency. Additionally, the growing demand for personalized mobility solutions is encouraging adoption of advanced AI technologies. These factors are driving significant growth in the Automotive GenAI Copilot market.

High development costs and data privacy concerns are significant restraints for the Automotive GenAI Copilot market. Developing advanced AI systems requires substantial investment in research and development, increasing costs by 30–50%. Data privacy concerns related to in-vehicle data collection and processing are also a challenge. Approximately 38% of consumers express concerns about data security in connected vehicles. These factors can limit adoption and create barriers for manufacturers.

Autonomous driving presents significant opportunities for the Automotive GenAI Copilot market. AI copilots play a critical role in enabling autonomous vehicle functionality by providing real-time decision-making and predictive analytics. In 2025, over 46% of automotive manufacturers invested in autonomous driving technologies. These systems can improve safety and efficiency, creating new opportunities for market growth.

System integration and regulatory complexities are critical challenges for the Automotive GenAI Copilot market. Integrating AI systems with existing vehicle architectures can be complex and costly. Regulatory requirements for safety and data protection add further complexity. Approximately 34% of manufacturers report challenges in meeting regulatory standards. These factors require continuous innovation and compliance strategies.

Adoption of Multimodal AI Interfaces: Over 63% of vehicles integrated multimodal AI copilots in 2025, improving driver interaction accuracy by 37% and enabling seamless voice, gesture, and visual commands.

Growth in Edge AI Processing: Approximately 56% of automotive AI systems now use edge computing, reducing latency by 33% and improving real-time decision-making capabilities.

Expansion of AI-Powered Personalization: Around 52% of vehicles offer personalized AI copilots, improving user satisfaction by 35% and enhancing in-car experience.

Integration of AI in ADAS Systems: Over 58% of advanced driver assistance systems incorporate AI copilots, improving safety features and reducing driver workload by 31%.

The Automotive GenAI Copilot market segmentation highlights diverse adoption across technology types, applications, and end-user categories. By type, the market includes embedded AI copilots, cloud-based AI copilots, and hybrid solutions. Applications span infotainment, driver assistance, predictive maintenance, and fleet management. End-user insights indicate strong adoption among passenger vehicle manufacturers, commercial fleet operators, and mobility service providers. The segmentation reflects how technological advancements and evolving consumer preferences are shaping market demand.

Embedded AI copilots account for approximately 47% of adoption due to their ability to provide real-time processing and low latency, while cloud-based solutions hold around 33%. However, hybrid AI copilots are the fastest-growing segment, expected to expand at over 26.3% CAGR, driven by the need for scalability and real-time performance. Other niche solutions collectively contribute 20%.

In 2025, embedded AI copilots were widely deployed in premium vehicles, improving real-time decision-making and user experience.

Infotainment systems lead with a 39% share, driven by increasing demand for enhanced in-car experiences. Driver assistance systems are the fastest-growing segment, projected above 25.1% CAGR, supported by advancements in autonomous driving technologies. Predictive maintenance and fleet management collectively account for 61%. In 2025, over 62% of consumers used AI copilots for infotainment, while 55% of vehicles integrated them into driver assistance systems.

In 2025, AI-powered infotainment systems improved user engagement and driving experience across global markets.

Passenger vehicle manufacturers dominate with a 61% share, driven by high demand for connected and intelligent vehicles, while commercial fleet operators account for around 23%. However, mobility service providers are the fastest-growing segment, expanding at over 24.7% CAGR, supported by increasing adoption of shared mobility solutions. Other end-users collectively contribute 16%. In 2025, 65% of consumers preferred vehicles with AI copilots, while 49% of fleet operators adopted AI solutions for operational efficiency.

In 2025, mobility service providers implemented AI copilots to enhance fleet management and customer experience.

North America accounted for the largest market share at 38.6% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 26.9% between 2026 and 2033.

North America recorded over 18 million AI-enabled vehicles in operation in 2025, with more than 69% of premium vehicles integrating GenAI copilots. Europe followed with a 29.3% share, where over 61% of new vehicles included AI-powered driver assistance features aligned with safety regulations. Asia-Pacific accounted for 24.7%, driven by rapid adoption of electric vehicles and connected mobility solutions across China, India, and Japan. South America and Middle East & Africa collectively held 7.4%, supported by growing automotive digitalization and infrastructure development.

How are intelligent in-vehicle AI ecosystems transforming next-generation driving experiences and safety standards?

This region accounted for approximately 38.6% of the Automotive GenAI Copilot market in 2025, driven by strong demand across automotive OEMs, technology providers, and mobility services. Over 71% of premium vehicles integrate AI copilots for infotainment and driver assistance. Regulatory frameworks supporting vehicle safety and innovation have accelerated adoption. Technological advancements include AI-driven analytics, edge computing, and multimodal interfaces. A leading automotive technology company deployed advanced AI copilots, improving user interaction by 36%. Consumer behavior reflects strong demand for personalized and intelligent mobility solutions.

Why is safety-driven AI innovation accelerating adoption of advanced automotive copilot technologies?

Europe held nearly 29.3% of the Automotive GenAI Copilot market in 2025, with Germany, the UK, and France contributing over 64% of regional demand. Strict safety and emissions regulations have driven adoption of AI-powered copilots. Over 60% of vehicles include advanced driver assistance systems with AI integration. Adoption of AI technologies improved operational efficiency by 28%. A regional automotive manufacturer implemented advanced AI copilots, enhancing safety features. Consumer behavior emphasizes safety, compliance, and sustainability.

What is accelerating rapid adoption of AI-driven automotive copilots across emerging mobility ecosystems?

Asia-Pacific accounted for 24.7% of the Automotive GenAI Copilot market in 2025, with China, India, and Japan leading growth. Increasing adoption of electric vehicles and connected mobility solutions has driven demand by 35%. Investments in automotive technology infrastructure improved scalability and performance. A regional automotive company implemented AI copilots, improving user experience. Consumer behavior is driven by digital transformation and increasing demand for smart vehicles.

How is automotive digitalization influencing adoption of AI-powered copilots in emerging vehicle markets?

South America accounted for approximately 4.5% of the global Automotive GenAI Copilot market in 2025, led by Brazil and Argentina. Automotive digitalization initiatives have driven adoption of AI copilots. Government policies supporting innovation improved accessibility. A regional automotive company implemented AI copilots, improving vehicle functionality. Consumer behavior reflects growing demand for advanced vehicle technologies.

Why is smart mobility transformation driving demand for AI-powered automotive copilots across developing regions?

The region held around 2.9% of global Automotive GenAI Copilot adoption in 2025, with UAE and South Africa leading growth. Investments in smart mobility and digital infrastructure increased adoption by 22%. A regional automotive provider implemented AI copilots, improving user experience. Consumer behavior shows increasing demand for intelligent mobility solutions.

United States Automotive GenAI Copilot Market – 34.2%: Strong automotive technology ecosystem and high adoption of AI-powered vehicles.

China Automotive GenAI Copilot Market – 19.6%: Rapid growth in electric vehicles and connected mobility adoption.

The Automotive GenAI Copilot market is moderately consolidated, with over 85 active global players including automotive OEMs, semiconductor companies, and AI technology providers. The top five companies collectively account for approximately 56% of the market, reflecting strong competitive positioning and technological leadership.

Competition is driven by innovation in AI algorithms, edge computing, and multimodal interfaces. Strategic initiatives such as partnerships, acquisitions, and product launches increased by 31% during 2024–2025. Companies are focusing on enhancing performance, improving scalability, and integrating AI into vehicle systems.

Investment in research and development has increased significantly, with leading companies allocating over 14% of budgets to AI innovation. Product differentiation is based on performance, reliability, and user experience. The market is evolving toward integrated AI ecosystems, combining hardware, software, and analytics solutions. Collaboration between automotive manufacturers and technology providers is driving innovation and adoption.

Continental AG

Microsoft

Amazon

Intel

Huawei

Baidu

Tesla

Toyota

BMW

Mercedes-Benz

Technological advancements in the Automotive GenAI Copilot market are centered on artificial intelligence, edge computing, and multimodal interaction systems. Large language models enable natural language understanding, improving driver interaction accuracy by up to 42%. Edge AI processing allows real-time data analysis within vehicles, reducing latency and enhancing responsiveness.

Multimodal interfaces combine voice, gesture, and visual inputs, improving user experience and safety. Advanced driver assistance systems integrate AI copilots to provide real-time decision support, improving safety outcomes. Cloud-based platforms enable continuous learning and updates, enhancing system performance.

High-performance computing systems and AI chips are enabling faster processing and improved efficiency. Integration with IoT and connected vehicle ecosystems is expanding capabilities. Additionally, cybersecurity solutions are being incorporated to protect vehicle data and systems.

Emerging technologies include autonomous driving systems, predictive analytics, and AI-powered personalization. These innovations are transforming vehicles into intelligent mobility platforms, enhancing safety, efficiency, and user experience.

In June 2025, NVIDIA introduced advanced automotive AI platforms with enhanced generative AI capabilities, improving in-vehicle intelligence and enabling real-time decision-making for autonomous driving systems. Source: www.nvidia.com

In April 2025, Qualcomm launched next-generation automotive AI chips designed to support GenAI copilots, improving performance and enabling advanced in-vehicle applications. Source: www.qualcomm.com

In October 2024, Bosch expanded its AI-powered automotive solutions portfolio, enhancing driver assistance systems and improving safety features across vehicles. Source: www.bosch.com

In August 2024, Continental introduced advanced AI-based automotive systems, improving in-vehicle user experience and supporting next-generation mobility solutions. Source: www.continental.com

The Automotive GenAI Copilot Market Report provides a comprehensive analysis of technologies, applications, and end-user adoption across global automotive ecosystems. The scope includes embedded AI copilots, cloud-based solutions, and hybrid systems designed to enhance vehicle intelligence and user experience.

The report evaluates applications across infotainment, driver assistance, predictive maintenance, and fleet management, highlighting their role in improving safety and operational efficiency. Geographic coverage spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, with detailed insights into key markets such as the United States, China, Germany, India, and Japan.

Additionally, the report examines emerging segments such as autonomous driving systems, multimodal AI interfaces, and personalized mobility solutions. It highlights technological advancements, regulatory frameworks, and industry trends influencing adoption. The scope also includes integration strategies, interoperability standards, and innovation pathways shaping the market. The report provides actionable insights for stakeholders, enabling informed decision-making across product development, investment planning, and strategic expansion initiatives.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 1,261.5 Million |

|

Market Revenue in 2033 |

USD 7,713.8 Million |

|

CAGR (2026 - 2033) |

25.4% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

NVIDIA, Qualcomm, Bosch, Continental AG, Google, Microsoft, Amazon, Intel, Huawei, Baidu, Tesla, Toyota, BMW, Mercedes-Benz |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |