Reports

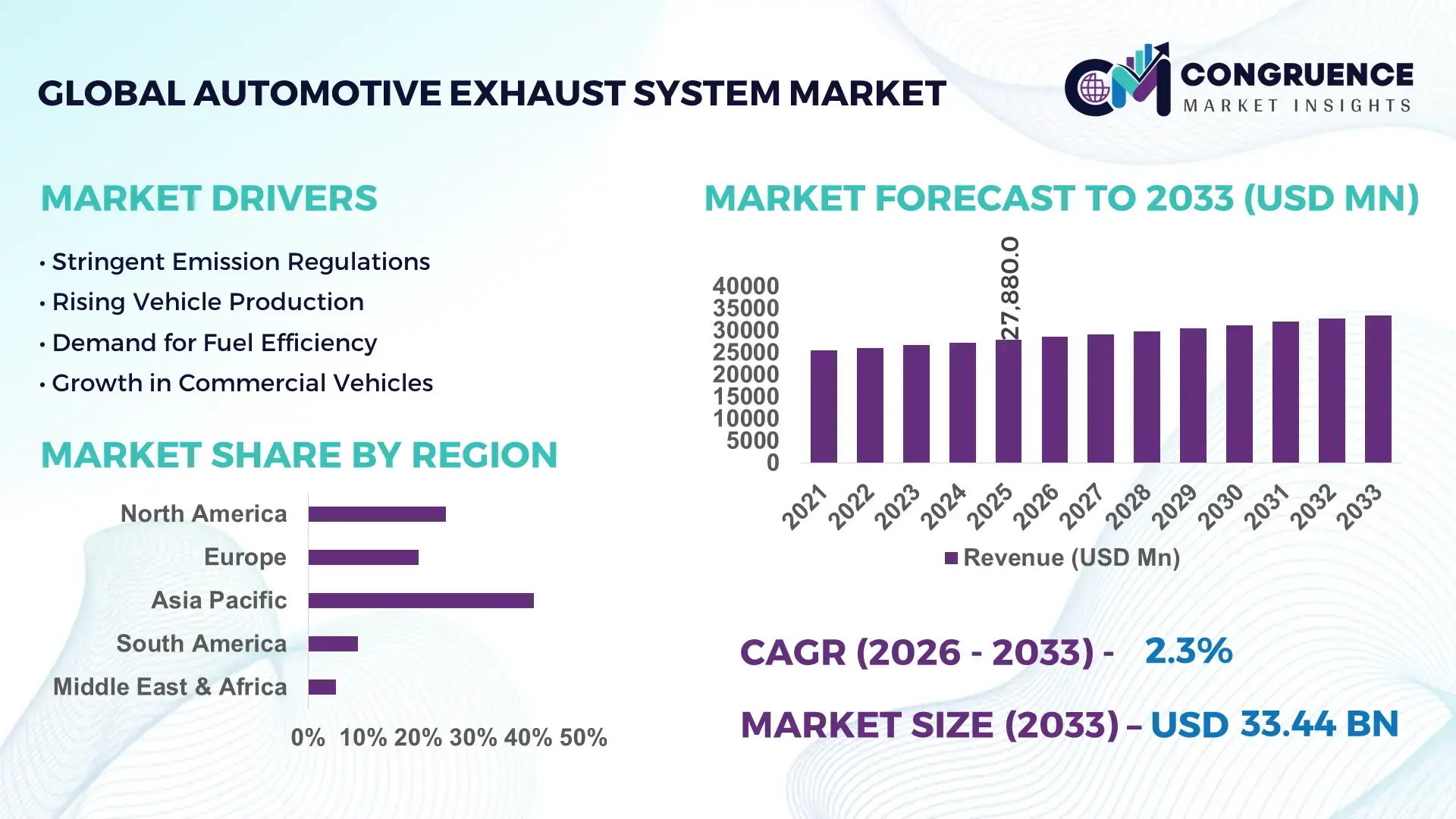

The Global Automotive Exhaust System Market was valued at USD 27880 Million in 2025 and is anticipated to reach a value of USD 33442.43 Million by 2033 expanding at a CAGR of 2.3% between 2026 and 2033. Stricter Euro 7 emission implementation, rising hybrid vehicle production, and accelerated replacement demand for lightweight stainless-steel exhaust architectures are driving advanced automotive exhaust system adoption across passenger and commercial vehicle platforms.

China dominates the global automotive exhaust system market with nearly 34% manufacturing share supported by annual vehicle production exceeding 31 million units, while integrated investments in low-emission mobility infrastructure and advanced catalytic converter capacity expansion continue reshaping regional supply chains. Chinese Tier-1 suppliers increased automated exhaust module deployment by 18% during 2025–2026 to support hybrid and export-oriented vehicle programs. Germany maintains stronger penetration of premium emission-control technologies with over 72% adoption of advanced particulate filtration systems across new diesel and hybrid commercial fleets, driven by post-energy-crisis industrial efficiency mandates and stricter European carbon compliance frameworks. Compared with North American facilities, Asian manufacturing hubs currently operate nearly 22% lower exhaust component processing costs due to localized stainless-steel sourcing and vertically integrated fabrication ecosystems.

Manufacturers prioritizing lightweight modular exhaust platforms, regionalized sourcing strategies, and next-generation emission integration capabilities are positioned to secure long-term OEM contracts amid tightening global compliance standards and evolving hybrid vehicle production cycles.

Market Size & Growth: Market expands from USD 27880 million in 2025 to USD 33442.43 million by 2033 at 2.3% growth, supported by hybrid vehicle integration and stricter emission-control manufacturing standards.

Top Growth Drivers: Lightweight exhaust materials improve fuel efficiency by 7%, particulate filtration adoption rises 19%, and hybrid vehicle exhaust customization demand increases 14% globally.

Short-Term Forecast: By 2027, automated exhaust welding systems reduce production defects by 16% while assembly throughput efficiency improves nearly 11% across high-volume manufacturing plants.

Emerging Technologies: AI-enabled emission diagnostics, laser-welded stainless assemblies, and sensor-integrated exhaust monitoring systems increase predictive maintenance accuracy by 21% in advanced OEM facilities.

Regional Leaders: Asia Pacific surpasses USD 14 billion driven by EV-hybrid coexistence, Europe exceeds USD 8 billion through Euro 7 adoption, and North America crosses USD 6 billion via commercial fleet upgrades.

Consumer/End-User Trends: Nearly 48% of fleet operators prioritize corrosion-resistant exhaust systems to reduce maintenance cycles and improve long-distance vehicle operational reliability.

Pilot/Case Example: In 2026, a Japanese OEM reduced exhaust component weight by 13% using high-strength alloys, improving hybrid vehicle thermal efficiency and compliance performance.

Competitive Landscape: Top manufacturers control approximately 42% market share, with Faurecia, Tenneco, Eberspächer, Benteler, and Yutaka Giken expanding localized production amid supply chain diversification.

Regulatory & ESG Impact: Advanced emission-control integration lowers particulate emissions by 28% in regulated markets as Europe and China tighten commercial vehicle compliance standards.

Investment & Funding: Global investments exceeded USD 3.1 billion during 2025–2026, primarily targeting automated fabrication lines, thermal management innovation, and regional manufacturing expansion.

Innovation & Future Outlook: Smart exhaust monitoring modules, modular aftertreatment systems, and lightweight alloy integration are accelerating next-generation hybrid vehicle platform optimization strategies.

Fleet operators increasingly prefer regionally sourced aftermarket exhaust assemblies over imported premium systems to minimize downtime and inventory delays. Commercial vehicle maintenance contracts now prioritize standardized modular exhaust components compatible across multiple fleet platforms, reducing warehouse complexity by nearly 17% while improving replacement turnaround efficiency in logistics-intensive transportation networks.

The automotive exhaust system market is becoming strategically critical as global automakers balance internal combustion optimization with hybrid platform expansion under tightening emission mandates. Supply-chain restructuring across China, Mexico, and Eastern Europe is accelerating localized exhaust module production to reduce logistics exposure and improve compliance responsiveness. Advanced exhaust architectures integrating thermal management sensors and lightweight alloys are now influencing OEM sourcing decisions, particularly in commercial fleets and hybrid passenger vehicles where durability and fuel efficiency directly affect lifecycle operating costs.

Electronically monitored exhaust systems currently improve emission-control efficiency by nearly 18% compared with legacy mechanically tuned configurations while reducing maintenance intervals by approximately 12% in heavy-duty vehicle operations. Germany and Japan lead premium exhaust innovation through automated stainless-steel fabrication and particulate filtration deployment, whereas India and Thailand are scaling cost-efficient manufacturing capacity for export-oriented vehicle assembly. Over the next two to three years, hybrid-compatible exhaust integration across mid-range vehicle platforms is expected to expand significantly as automakers standardize modular emission-control components.

Commercial fleet operators are increasingly deploying corrosion-resistant modular exhaust units to simplify maintenance scheduling and reduce downtime across logistics networks. In response, suppliers are expanding regional fabrication partnerships, investing in robotic welding systems, and prioritizing vertically integrated sourcing models to secure long-term OEM positioning and operational resilience.

Stricter emission-control mandates across China, Germany, and India are accelerating adoption of advanced automotive exhaust technologies integrated with particulate filtration and thermal monitoring systems. Nearly 64% of newly launched hybrid commercial vehicles now incorporate lightweight stainless-steel exhaust modules to improve fuel optimization and regulatory compliance simultaneously. Automated exhaust fabrication lines have reduced component defect rates by 15%, enabling suppliers to scale precision manufacturing for high-volume OEM programs. Europe’s Euro 7 implementation and India’s tightening BS-VI phase expansion are forcing manufacturers to redesign exhaust architectures for lower nitrogen oxide output and improved thermal efficiency. In response, companies are expanding localized catalyst coating facilities, forming material supply partnerships, and investing in robotic welding systems to strengthen compliance readiness while reducing long-term manufacturing inefficiencies.

Volatile stainless steel, palladium, and rhodium pricing continues pressuring automotive exhaust system profitability, particularly for suppliers dependent on imported catalytic converter materials. During 2025–2026, catalyst material procurement costs fluctuated by more than 21%, disrupting production planning and contract pricing stability across North American and European manufacturing hubs. Smaller Tier-2 suppliers are experiencing margin compression as OEMs resist aggressive component price revisions despite increasing compliance complexity. China’s tighter export monitoring on processed industrial metals and shipping disruptions through Red Sea trade routes have further extended lead times for emission-control assemblies by nearly 13%. To reduce operational exposure, manufacturers are increasing localized sourcing agreements, diversifying alloy procurement networks, and redesigning exhaust systems with lower precious-metal dependency while maintaining regulatory performance standards.

Hybrid vehicle expansion is creating specialized demand for compact, heat-efficient automotive exhaust systems capable of supporting intermittent engine operation and lower-temperature emission cycles. Japan and South Korea are accelerating deployment of sensor-integrated exhaust modules, with smart diagnostic integration improving predictive maintenance accuracy by nearly 20% across hybrid fleet operations. Advanced hydroforming technologies reduce exhaust assembly weight by approximately 11%, improving vehicle efficiency without compromising durability. India’s growing hybrid passenger vehicle production and Southeast Asia’s export-focused assembly expansion are opening cost-competitive manufacturing opportunities for regional suppliers. Companies are increasing R&D investments in modular exhaust platforms, forming semiconductor integration partnerships, and developing digitally monitored aftertreatment systems to capture long-term contracts tied to next-generation hybrid mobility ecosystems and evolving emission-control software architectures.

Automotive exhaust system manufacturers face increasing execution pressure from complex multi-material integration, precision welding requirements, and advanced sensor calibration demands. More than 41% of suppliers report skilled labor shortages in automated fabrication and emission-control assembly operations, particularly across Germany, Mexico, and Eastern Europe. Integration of thermal sensors, lightweight alloys, and electronically controlled filtration systems has increased production cycle complexity by nearly 17%, limiting scalability for smaller manufacturers transitioning from conventional exhaust platforms. Tightening durability validation standards are also extending product testing timelines for OEM approvals. To maintain competitiveness, companies must accelerate workforce automation training, expand AI-assisted quality inspection systems, and strengthen engineering partnerships capable of supporting high-precision manufacturing consistency across geographically distributed production networks.

Smart Exhaust Monitoring Expansion AI-enabled exhaust diagnostics and sensor-integrated aftertreatment systems are expanding rapidly across hybrid and commercial fleets, with predictive fault detection accuracy improving by 22% and maintenance downtime declining nearly 14%. Japan-based OEMs are integrating cloud-linked emission analytics into fleet operations following stricter compliance audits. Suppliers are scaling embedded sensor partnerships and upgrading electronic calibration workflows to improve operational visibility and reduce warranty-related servicing costs.

Localized Manufacturing Network Shifts Exhaust component manufacturers are restructuring supply chains toward Mexico, India, and Thailand to reduce shipping volatility and lower sourcing dependency on single-country metal processing hubs. Regionalized fabrication lowered average delivery lead times by 17% during 2025–2026, while localized stainless-steel procurement reduced logistics costs by 11%. Companies are increasing robotic welding capacity and establishing multi-country catalyst sourcing agreements to stabilize production continuity amid Red Sea freight disruptions and industrial trade realignment.

Lightweight Alloy Integration Surge High-strength stainless steel and hydroformed alloy exhaust assemblies are replacing conventional welded systems across passenger and commercial vehicle platforms. Advanced lightweight exhaust integration reduces component mass by nearly 13% while improving thermal retention efficiency by 9% in hybrid drivetrains. German and South Korean manufacturers are expanding automated hydroforming lines and material-engineering partnerships to support next-generation vehicle platforms requiring compact exhaust routing and enhanced fuel optimization capabilities.

Modular Fleet Retrofit Adoption Commercial fleet operators are increasingly deploying modular retrofit exhaust kits to extend vehicle lifecycle performance under tightening urban emission-control rules. Retrofit-compatible particulate filtration installations increased 19% across logistics fleets in India and Poland, while standardized exhaust assemblies reduced maintenance inventory complexity by approximately 15%. Manufacturers are responding through aftermarket expansion programs, quick-installation exhaust configurations, and fleet-service collaborations focused on reducing vehicle downtime and accelerating regulatory compliance upgrades.

Catalytic converters remain the leading segment within the automotive exhaust system market due to mandatory emission-control integration across passenger and commercial vehicle production lines. Nearly 46% of newly manufactured vehicles now utilize advanced multi-layer catalyst systems optimized for hybrid and low-temperature operating conditions. Diesel particulate filters represent the fastest-growing type as heavy-duty transport operators adopt stricter particulate management technologies under expanding commercial emission regulations in Germany, China, and India. Mufflers continue maintaining stable aftermarket demand driven by replacement cycles and noise-control compliance, while exhaust manifolds are increasingly engineered using lightweight heat-resistant alloys to improve thermal efficiency. Exhaust pipes are witnessing gradual material innovation through corrosion-resistant stainless-steel integration. In response, manufacturers are increasing investments in modular aftertreatment systems, automated catalyst coating facilities, and hydroformed component production to strengthen OEM supply agreements and reduce long-term material dependency risks.

Emission control remains the dominant application segment as governments intensify nitrogen oxide and particulate reduction standards across commercial and passenger vehicle categories. More than 62% of newly deployed exhaust systems now prioritize integrated emission-management functionality over conventional noise-focused configurations. Performance enhancement applications are emerging as the fastest-growing area, particularly within hybrid passenger vehicles where optimized exhaust flow and thermal retention improve fuel efficiency by nearly 10%. Passenger vehicles continue driving large-scale exhaust deployment volumes, while commercial vehicles are accelerating adoption of sensor-enabled aftertreatment systems to meet logistics-sector compliance targets. Noise reduction applications maintain importance in urban fleet operations, especially in Japan and Germany where municipal transport regulations are tightening. Manufacturers are responding through AI-assisted calibration integration, modular exhaust architecture development, and automated fabrication expansion to support multi-application compatibility and faster deployment across evolving vehicle platforms.

Automotive manufacturers remain the dominant end-user group due to large-scale OEM integration requirements tied to hybrid expansion, compliance redesign, and platform standardization initiatives. Nearly 68% of advanced exhaust assemblies are currently deployed through direct OEM production contracts, particularly across China, Germany, and Japan. Commercial fleet operators represent the fastest-growing end-user segment as logistics providers modernize diesel and hybrid vehicle fleets to reduce maintenance downtime and comply with tightening urban emission mandates. Aftermarket service providers continue benefiting from replacement demand cycles, especially for corrosion-resistant mufflers and retrofit particulate filtration systems. The construction equipment and mining industries are increasing purchases of heavy-duty thermal-resistant exhaust solutions for off-highway machinery operating under extended load conditions, while the agricultural sector is gradually adopting modular low-maintenance exhaust configurations. Companies are strengthening segment-specific strategies through long-term supply partnerships, customized fleet-service agreements, and regionally localized manufacturing expansion.

Asia-Pacific accounted for the largest market share at 41% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 3.4% between 2026 and 2033.

Fleet Modernization and Regionalized Manufacturing Expansion

North America maintains strong automotive exhaust system deployment through commercial fleet modernization, localized component sourcing, and hybrid vehicle production expansion. The region contributes nearly 24% of global exhaust system integration activity, supported by advanced manufacturing clusters across the United States and Mexico. Automated robotic welding adoption increased by 16% during 2025–2026 as suppliers optimized precision fabrication and shortened OEM delivery timelines. Rising demand for corrosion-resistant exhaust assemblies in logistics and pickup truck platforms is accelerating aftermarket replacement cycles. Companies are strengthening regional resilience through cross-border catalyst sourcing partnerships, modular exhaust production facilities, and vertically integrated fabrication strategies designed to reduce dependency on imported stainless-steel processing.

United States Market Outlook: The United States leads North American automotive exhaust system deployment through large-scale commercial vehicle production, advanced aftermarket infrastructure, and strong hybrid pickup demand. More than 58% of regional heavy-duty fleet modernization projects now integrate upgraded particulate filtration and sensor-monitored exhaust systems. Domestic manufacturers are expanding AI-assisted fabrication lines and heat-resistant alloy processing capacity to support tightening emission compliance requirements and improve operational durability across long-haul transportation fleets.

Regulatory Engineering Reshaping Exhaust Innovation

Europe remains a high-value automotive exhaust system market driven by stringent emission-control frameworks, advanced engineering standards, and rapid deployment of hybrid-compatible aftertreatment systems. The region accounts for approximately 28% of global advanced exhaust technology integration, particularly across Germany, France, and Italy. Euro 7 compliance preparation accelerated deployment of low-temperature catalytic systems by nearly 19% during 2025–2026. Automotive suppliers are increasingly investing in lightweight hydroformed exhaust structures and digitally monitored emission-control modules to improve regulatory adaptability and reduce manufacturing inefficiencies. Cross-border industrial partnerships between material suppliers and OEMs are strengthening localized catalyst processing and automated filtration system development.

Germany Market Outlook: Germany dominates European exhaust technology advancement through precision manufacturing capabilities, premium vehicle engineering, and high adoption of automated particulate filtration systems. Nearly 74% of newly engineered commercial diesel platforms now utilize advanced thermal-resistant exhaust integration for compliance optimization and fuel-efficiency balancing. German suppliers continue expanding robotic fabrication centers and stainless-steel hydroforming operations to maintain competitive leadership in high-performance exhaust architecture development.

High-Volume Manufacturing and Export Leadership

Asia-Pacific leads the automotive exhaust system market through large-scale vehicle manufacturing capacity, vertically integrated supply chains, and export-oriented component production. The region contributes more than 41% of global exhaust assembly output, with China, Japan, South Korea, and India serving as major fabrication and deployment hubs. Automated exhaust module production across Asia-Pacific increased by approximately 21% during 2025–2026 as manufacturers accelerated localized sourcing and robotic assembly adoption. Hybrid vehicle expansion and tightening emission standards are driving integration of lightweight catalytic systems and modular particulate filtration technologies. Companies are scaling hydroforming operations, expanding regional fabrication networks, and increasing strategic alloy procurement partnerships to support export stability and production continuity.

China Market Outlook: China remains the largest operational hub for automotive exhaust system manufacturing due to its extensive OEM ecosystem, stainless-steel processing infrastructure, and hybrid vehicle production scale. More than 31 million vehicles produced annually continue supporting strong demand for catalytic converters, mufflers, and integrated filtration systems. Domestic suppliers are increasing investment in automated coating technologies and sensor-enabled exhaust assemblies to strengthen export competitiveness and align with evolving low-emission transportation policies.

Commercial Vehicle Demand Supporting Industrial Activity

South America is witnessing stable automotive exhaust system demand driven by commercial transportation upgrades, agricultural equipment deployment, and expanding regional assembly operations. Brazil and Argentina account for the majority of regional exhaust integration activity, particularly in diesel-powered fleet and utility vehicle applications. Heavy-duty aftermarket exhaust replacement demand increased by nearly 14% during 2025–2026 as logistics operators extended vehicle service life under cost-sensitive operating conditions. Infrastructure limitations and import dependency on advanced catalyst materials continue affecting manufacturing scalability, yet suppliers are improving regional responsiveness through localized assembly expansion and strategic distribution partnerships focused on reducing replacement lead times.

Brazil Market Outlook: Brazil leads South American automotive exhaust system activity through its commercial vehicle manufacturing base, agricultural machinery deployment, and extensive aftermarket service network. More than 46% of regional heavy-duty exhaust replacement demand originates from long-haul transportation and industrial fleet operations within the country. Manufacturers are prioritizing localized muffler and exhaust pipe production while expanding partnerships with fleet maintenance providers to improve replacement efficiency and operational continuity.

Industrial Diversification and Fleet Infrastructure Expansion

Middle East & Africa is emerging as a strategically expanding automotive exhaust system market supported by logistics infrastructure investment, industrial diversification initiatives, and growing commercial fleet modernization. The region contributes a smaller deployment share but is experiencing increasing adoption of modular exhaust assemblies and retrofit-compatible particulate filtration systems. Commercial transport and mining operations increased demand for heavy-duty exhaust replacement components by approximately 18% during 2025–2026. Gulf countries are investing in localized automotive component assembly zones while African logistics operators prioritize durable corrosion-resistant exhaust configurations for high-temperature operating conditions. Suppliers are expanding regional distribution agreements and maintenance partnerships to strengthen aftermarket penetration and improve deployment responsiveness.

Saudi Arabia Market Outlook: Saudi Arabia is strengthening its position within the regional automotive exhaust system market through industrial diversification policies, commercial fleet expansion, and growing investment in localized vehicle component manufacturing. Logistics corridor development and mining-sector vehicle utilization continue driving demand for thermal-resistant exhaust systems across heavy-duty transport applications. The country is also expanding industrial partnerships supporting regional assembly operations and improving aftermarket servicing infrastructure for commercial vehicle fleets operating in high-temperature environments.

Global leaders including Faurecia, Tenneco, Eberspächer, Benteler, and Yutaka Giken compete directly against regional low-cost manufacturers and specialized aftermarket suppliers across OEM and fleet-focused contracts. The top five players collectively control nearly 42% of market activity through integrated manufacturing, catalyst technology expertise, and long-term automaker partnerships. Competition centers on production efficiency, lightweight material engineering, delivery speed, and emission-control performance. Automated fabrication systems improved manufacturing throughput by 15%, while modular exhaust integration reduced installation complexity by approximately 12% for commercial fleet operators. Japanese and German manufacturers are prioritizing robotic hydroforming and sensor-enabled exhaust systems, whereas Chinese suppliers compete aggressively through vertically integrated stainless-steel sourcing and lower processing costs. Strategic acquisitions, regional assembly expansion, and alloy supply partnerships are reshaping competitive positioning. High compliance costs, precision manufacturing requirements, and catalyst material dependency remain major entry barriers. Winning requires scalable manufacturing, localized supply resilience, advanced emission integration, and strong OEM alignment.

Faurecia

Tenneco

Eberspächer

Benteler International

Yutaka Giken

Bosal International

Futaba Industrial Co., Ltd.

Sejong Industrial Co., Ltd.

Sango Co., Ltd.

Friedrich Boysen GmbH

Harbin Airui Automotive Exhaust Systems Co., Ltd.

Dinex Group

Katcon Global

Walker Exhaust Systems

Advanced automotive exhaust systems are increasingly integrating lightweight stainless-steel alloys, hydroforming processes, and electronically controlled emission modules to improve thermal efficiency and compliance performance. Sensor-enabled particulate filtration systems now reduce diagnostic detection time by nearly 18% compared with legacy mechanically monitored systems, while automated robotic welding improves production precision by approximately 15%. More than 62% of newly engineered hybrid commercial vehicle platforms incorporate modular exhaust architectures designed for lower-temperature emission cycles and compact underbody integration.

Emerging technologies between 2026 and 2028 include AI-assisted exhaust diagnostics, smart thermal monitoring sensors, and digitally calibrated aftertreatment systems capable of improving predictive maintenance accuracy by nearly 21%. Electronically controlled exhaust flow systems deliver approximately 11% better thermal retention efficiency than conventional fixed-flow exhaust assemblies. Japanese and German OEM suppliers are aggressively scaling smart exhaust integration partnerships to strengthen premium vehicle differentiation, while Chinese manufacturers focus on cost-efficient automated fabrication and vertically integrated catalyst processing.

Disruptive innovation is shifting toward hybrid-compatible aftertreatment platforms, heat-energy recovery systems, and low-precious-metal catalytic technologies. Advanced catalyst coating methods reduce precious-metal dependency by nearly 13%, helping manufacturers manage material volatility and compliance costs simultaneously. Companies adopting modular exhaust ecosystems, AI-driven quality inspection, and automated hydroforming capabilities are securing stronger OEM positioning through faster deployment cycles, lower operational waste, and improved emission-control consistency across multi-platform vehicle production programs.

June 2025 – Tenneco released its 2024 sustainability report highlighting a 23% reduction in energy consumption and 78% operational waste recycling across manufacturing sites, strengthening low-emission exhaust production efficiency and OEM sustainability alignment. Source: automotiveworld.com

February 2024 – Tenneco introduced Monroe RideRefine SDD valve technology improving damping tunability and reducing vibration during short piston strokes, enhancing premium vehicle ride comfort and supporting advanced exhaust-acoustic integration strategies for OEM platforms.

November 2025 – Tenneco Clean Air India confirmed development of hybrid exhaust aftertreatment architectures and BS7-ready systems at Chakan and Chennai facilities, strengthening future emission-control readiness and accelerating localized advanced exhaust integration capabilities. Source: tennecoindia.com

2024 – Faurecia Service expanded Easy2Fit exhaust kits and remanufactured diesel particulate filter offerings, improving installation efficiency and aftermarket logistics optimization while supporting sustainable replacement demand across commercial and passenger vehicle servicing networks. Source: faurecia-service.com

The automotive exhaust system market report provides comprehensive analysis across exhaust manifolds, mufflers, catalytic converters, diesel particulate filters, and exhaust pipes, covering operational trends across passenger vehicles, commercial vehicles, off-highway applications, emission control, noise reduction, and performance enhancement segments. The study evaluates demand patterns among automotive manufacturers, aftermarket service providers, commercial fleet operators, construction equipment companies, mining enterprises, and agricultural equipment users. More than 40% of current deployment activity remains concentrated within hybrid-compatible and emission-optimized exhaust architectures integrated across Asia-Pacific, Europe, and North America manufacturing hubs.

The report delivers detailed regional intelligence covering production ecosystems, supply-chain restructuring, regulatory transitions, automation deployment, and material innovation trends between 2026 and 2033. It highlights strategic shifts including modular exhaust adoption, AI-assisted diagnostics, lightweight alloy integration, and localized manufacturing expansion. Business insights support investment prioritization, competitive benchmarking, procurement strategy development, aftermarket positioning, and long-term OEM partnership planning while identifying operational gaps, technology adoption signals, and evolving infrastructure requirements shaping future market competitiveness.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 27880 Million |

|

Market Revenue in 2033 |

USD 33442.43 Million |

|

CAGR (2026 - 2033) |

2.3% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Faurecia, Tenneco, Eberspächer, Benteler International, Yutaka Giken, Bosal International, Futaba Industrial Co., Ltd., Sejong Industrial Co., Ltd., Sango Co., Ltd., Friedrich Boysen GmbH, Harbin Airui Automotive Exhaust Systems Co., Ltd., Dinex Group, Katcon Global, Walker Exhaust Systems |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |