Reports

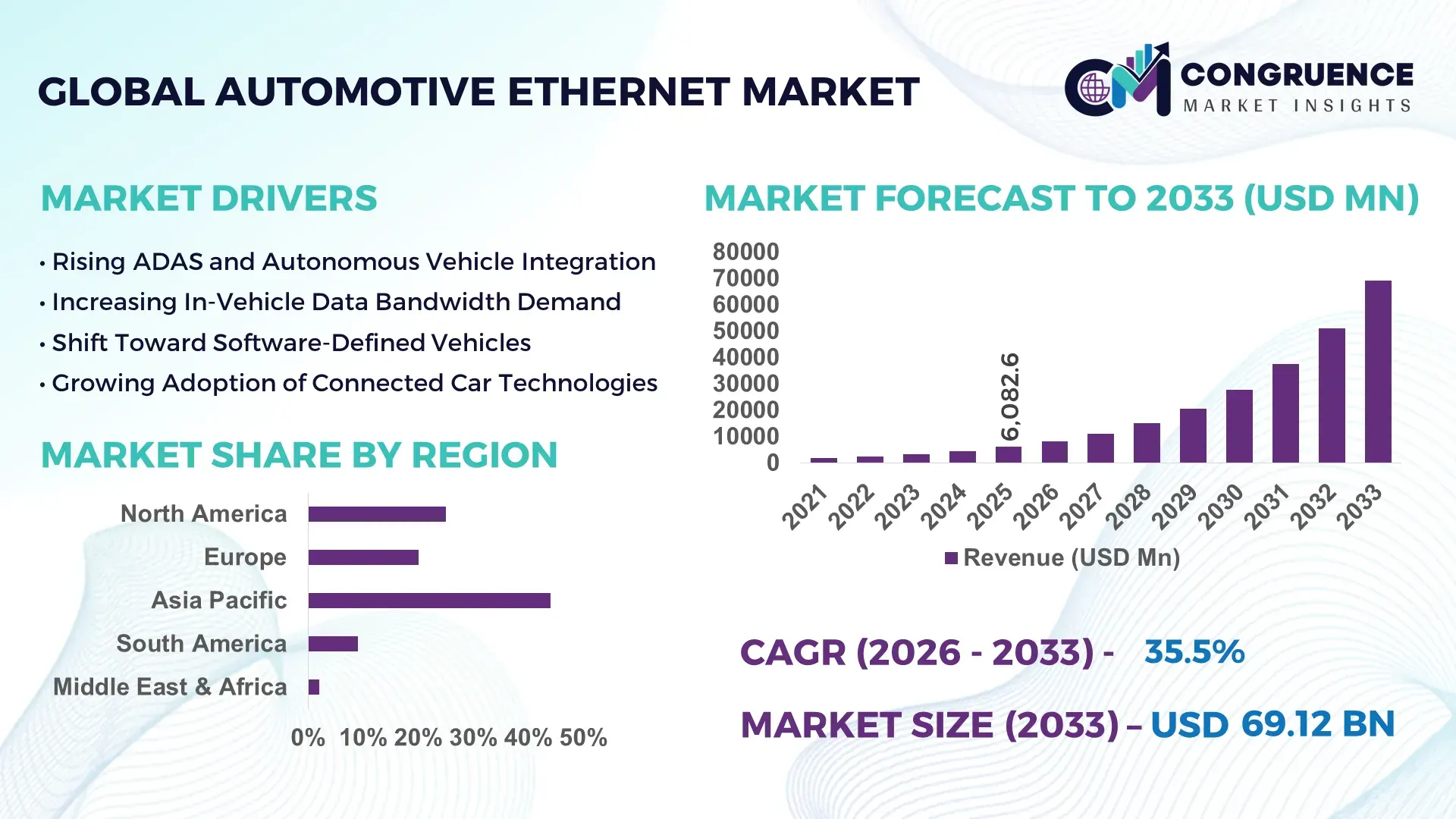

The Global Automotive Ethernet Market was valued at USD 6082.59 Million in 2025 and is anticipated to reach a value of USD 69119.92 Million by 2033 expanding at a CAGR of 35.5% between 2026 and 2033. This expansion is supported by the rapid integration of high-speed in-vehicle networking to manage data-intensive applications such as ADAS, infotainment, and centralized vehicle computing.

Germany represents the dominant country within the Automotive Ethernet market, underpinned by its advanced automotive manufacturing ecosystem and strong engineering base. In 2024, Germany produced over 4.1 million passenger vehicles, with more than 65% integrating Ethernet-based architectures for infotainment and driver-assistance systems. Annual automotive R&D investment exceeded USD 55 billion, a substantial portion directed toward software-defined vehicles and zonal E/E architectures. Automotive Ethernet deployment in Germany is concentrated across premium passenger vehicles, autonomous test fleets, and electric vehicle platforms, with in-vehicle data transmission speeds commonly exceeding 1 Gbps. Consumer adoption is strongest in luxury and upper mid-segment vehicles, where Ethernet penetration surpassed 70% of newly registered models in 2025.

Market Size & Growth: Valued at USD 6082.59 Million in 2025 and projected to reach USD 69119.92 Million by 2033, growing at a CAGR of 35.5%, driven by rising data bandwidth requirements in software-defined and autonomous vehicles.

Top Growth Drivers: ADAS adoption growth at 42%, in-vehicle data traffic increase of 55%, wiring weight reduction efficiency of 30%.

Short-Term Forecast: By 2028, OEMs are expected to achieve up to 25% reduction in vehicle network complexity through Ethernet-based zonal architectures.

Emerging Technologies: 10BASE-T1S multi-drop Ethernet, Time-Sensitive Networking (TSN), and integration with centralized vehicle compute platforms.

Regional Leaders: Asia Pacific projected to reach USD 31200 Million by 2033 with EV-led adoption; Europe USD 19800 Million driven by premium vehicles; North America USD 15200 Million supported by autonomous testing programs.

Consumer/End-User Trends: Passenger vehicles account for over 72% of deployments, with strong uptake in connected infotainment and Level 2+ ADAS-equipped models.

Pilot or Case Example: A 2025 OEM pilot integrating Ethernet backbones reported 28% reduction in wiring harness weight and 22% improvement in data latency.

Competitive Landscape: Broadcom leads with approximately 28% share, followed by NXP Semiconductors, Marvell Technology, Infineon Technologies, and Texas Instruments.

Regulatory & ESG Impact: Vehicle safety regulations supporting ADAS deployment and emission norms encouraging lightweight network architectures are accelerating adoption.

Investment & Funding Patterns: Over USD 9.5 billion invested globally between 2023–2025 in automotive networking ICs, platforms, and software-defined vehicle programs.

Innovation & Future Outlook: Continued shift toward zonal architectures, Ethernet-to-sensor integration, and multi-gigabit networks for Level 3–4 autonomy.

The Automotive Ethernet market is shaped by strong demand from passenger vehicles, commercial fleets, and autonomous test platforms, with passenger cars contributing approximately 70% of overall consumption. Recent innovations include multi-gigabit Ethernet PHYs, TSN-enabled controllers, and simplified single-pair cabling systems that reduce weight and cost. Regulatory emphasis on vehicle safety, cybersecurity compliance, and emission reduction supports Ethernet adoption by enabling centralized control and efficient data handling. Asia Pacific leads consumption growth due to high vehicle production volumes and EV penetration, while Europe focuses on premium and autonomous applications. Future outlook points toward full Ethernet backbones replacing legacy CAN and LIN networks, enabling scalable, software-driven vehicle architectures through 2033.

The strategic relevance of the Automotive Ethernet Market is closely linked to the automotive industry’s transition toward software-defined, connected, and autonomous vehicles. Automotive Ethernet has become a foundational technology enabling high-bandwidth, low-latency data transmission required for ADAS, centralized computing, over-the-air updates, and immersive infotainment. From a comparative benchmark perspective, 1000BASE-T1 Automotive Ethernet delivers up to 90% higher data throughput compared to legacy CAN and FlexRay standards, while reducing cabling complexity and signal interference. This performance advantage directly supports vehicle architectures handling more than 4 TB of data per day in advanced driver-assistance configurations.

Regionally, Asia Pacific dominates in volume due to high vehicle production output, while Europe leads in adoption, with over 68% of premium vehicle platforms integrating Ethernet-based zonal architectures by 2025. Strategic investments are increasingly aligned with AI-driven perception systems and centralized ECUs. By 2028, AI-enabled network management and Time-Sensitive Networking (TSN) are expected to improve in-vehicle data latency performance by approximately 30%, enhancing real-time safety functions.

From a compliance and ESG perspective, firms are committing to sustainability improvements such as 25% wiring weight reduction and increased recyclability of copper components by 2030, supporting emission reduction targets. In 2025, Germany achieved a 22% reduction in vehicle wiring weight through Ethernet-based zonal architecture initiatives across electric vehicle platforms. Looking ahead, the Automotive Ethernet Market is positioned as a critical pillar of resilience, regulatory compliance, and sustainable growth, supporting scalable vehicle innovation across global mobility ecosystems.

The increasing integration of advanced driver-assistance systems is a primary driver for the Automotive Ethernet Market. Modern vehicles equipped with Level 2 and Level 2+ ADAS can generate data streams exceeding 20 Gbps from cameras, radar, and lidar sensors combined. Automotive Ethernet enables this data to be transmitted reliably with deterministic timing, supporting real-time decision-making. By 2025, over 60% of newly developed passenger vehicle platforms incorporated multiple high-resolution cameras, significantly increasing internal network bandwidth requirements. Automotive Ethernet supports sensor fusion and centralized processing by reducing latency by up to 40% compared to traditional bus systems. This capability directly improves object detection accuracy, lane-keeping performance, and collision avoidance response times, making Ethernet a preferred networking solution for safety-focused vehicle architectures.

Despite its advantages, integration complexity remains a restraint within the Automotive Ethernet Market. Transitioning from legacy protocols to Ethernet-based architectures requires significant redesign of vehicle E/E systems, including new PHY components, connectors, and diagnostic tools. OEMs report development cycles extending by 12–18 months when shifting to fully Ethernet-based backbones due to validation, interoperability testing, and cybersecurity compliance requirements. Additionally, the need for skilled engineers with expertise in Ethernet, TSN, and automotive software stacks creates workforce constraints. Compatibility issues between mixed network environments, where CAN, LIN, and Ethernet coexist, further increase system integration costs and testing complexity, slowing adoption in cost-sensitive vehicle segments.

The emergence of software-defined vehicles presents significant opportunities for the Automotive Ethernet Market. Software-defined platforms rely on centralized compute architectures and continuous software updates, requiring robust, high-speed in-vehicle networks. Automotive Ethernet enables over-the-air updates that can transfer gigabyte-scale software packages efficiently, reducing update time by more than 50% compared to legacy systems. By 2027, over 45% of new vehicle platforms are expected to support centralized domain or zonal computing, creating demand for multi-gigabit Ethernet links. This shift opens opportunities for advanced network management software, Ethernet-enabled sensors, and scalable architectures that support feature upgrades throughout the vehicle lifecycle.

Cybersecurity and functional safety requirements present ongoing challenges for the Automotive Ethernet Market. As Ethernet increases vehicle connectivity, it expands the potential attack surface for cyber threats. Automotive systems must comply with ISO 21434 cybersecurity standards and ISO 26262 functional safety requirements, increasing development and certification complexity. Implementing secure Ethernet communication, including encryption, authentication, and intrusion detection, can increase network processing overhead by up to 15%. Additionally, ensuring deterministic behavior under fault conditions requires extensive validation and redundancy planning. These technical and regulatory demands raise development costs and extend testing timelines, posing challenges for rapid deployment across diverse vehicle platforms.

Expansion of Zonal E/E Architectures in New Vehicle Platforms

Automotive Ethernet adoption is accelerating as OEMs transition from domain-based to zonal electrical and electronic architectures. By 2025, over 48% of newly developed vehicle platforms incorporated zonal designs, reducing wiring length by up to 30% and overall harness weight by nearly 25%. Ethernet-enabled zonal gateways now support data aggregation rates above 10 Gbps, improving signal reliability and simplifying vehicle assembly processes.

Rising Integration of Multi-Gigabit Ethernet for ADAS and Autonomous Functions

The shift toward higher automation levels is driving demand for multi-gigabit Automotive Ethernet. Vehicles equipped with Level 2+ ADAS increasingly deploy 2.5GBASE-T1 and 5GBASE-T1 links, supporting camera and radar data flows exceeding 20 Gbps per vehicle. In 2024–2025, approximately 40% of ADAS-enabled models integrated at least one multi-gigabit Ethernet link, enhancing real-time sensor fusion accuracy by nearly 35%.

Increased Adoption of Time-Sensitive Networking for Deterministic Communication

Time-Sensitive Networking is emerging as a critical trend within the Automotive Ethernet market, enabling deterministic, low-latency data transfer for safety-critical applications. OEM validation programs indicate that TSN-enabled Ethernet can reduce network jitter by up to 70% and improve end-to-end latency consistency by around 45%. By 2026, nearly 50% of Ethernet-based in-vehicle networks are expected to support TSN profiles for braking, steering, and advanced driver monitoring systems.

Growing Use of Automotive Ethernet in Software-Defined and OTA-Centric Vehicles

Software-defined vehicles are reshaping Automotive Ethernet deployment strategies, with Ethernet serving as the backbone for over-the-air updates and centralized compute. By 2025, more than 60% of connected vehicles supported Ethernet-based OTA architectures, enabling software update times to fall by approximately 55%. Centralized Ethernet networks also improved diagnostic data throughput by nearly 40%, supporting predictive maintenance and continuous feature enhancement across the vehicle lifecycle.

The Automotive Ethernet market segmentation reflects the structural evolution of in-vehicle networking as data volumes, functional complexity, and software integration intensify. Segmentation by type highlights clear differentiation between bandwidth tiers and protocol capabilities aligned with safety, infotainment, and autonomous driving needs. Application-based segmentation shows uneven demand distribution, with data-heavy use cases accounting for the majority of deployments. End-user insights further distinguish adoption patterns between passenger vehicles, commercial vehicles, and emerging mobility platforms. Across all segments, adoption is influenced by factors such as sensor density, compute centralization, regulatory safety requirements, and lifecycle software update strategies. The market demonstrates a strong shift toward higher-speed, deterministic Ethernet variants, while legacy-compatible solutions retain relevance in transitional architectures. This layered segmentation provides decision-makers with clarity on where near-term deployment volumes are concentrated and where future expansion is structurally embedded.

The Automotive Ethernet market by type is primarily segmented into 100BASE-T1, 1000BASE-T1, multi-gigabit Ethernet (2.5G/5G/10GBASE-T1), and other specialized Ethernet variants. 1000BASE-T1 currently represents the leading type, accounting for approximately 46% of total adoption, driven by its balance between bandwidth capacity and cost efficiency. It is widely deployed in ADAS controllers, infotainment head units, and centralized gateways, where data rates around 1 Gbps sufficiently support camera and sensor fusion workloads.

Multi-gigabit Automotive Ethernet is the fastest-growing type, expanding at an estimated CAGR of 38%, propelled by rising deployment of high-resolution cameras, surround-view systems, and automated driving stacks requiring aggregated data flows exceeding 20 Gbps per vehicle. This growth is particularly visible in premium passenger vehicles and autonomous test fleets. In comparison, 100BASE-T1 continues to serve body electronics and control applications with lower bandwidth needs, while other niche Ethernet variants collectively account for about 19% of deployments, supporting diagnostics, redundancy, and backward compatibility.

By application, the Automotive Ethernet market is segmented into ADAS and safety systems, infotainment and connectivity, body and comfort electronics, powertrain and chassis systems, and diagnostics and updates. ADAS and safety systems represent the leading application, contributing approximately 41% of overall adoption, as these systems demand low-latency, high-reliability communication between cameras, radar, lidar, and centralized processors. In comparison, infotainment and connectivity applications account for around 27%, supporting high-definition displays, streaming, and connected services.

ADAS applications also represent the fastest-growing segment, expanding at an estimated CAGR of 36%, supported by regulatory mandates for advanced safety features and increased deployment of Level 2+ driver assistance. Other applications, including body electronics, powertrain control, and diagnostics, collectively contribute about 32%, maintaining relevance through gradual migration from legacy networks.

End-user segmentation of the Automotive Ethernet market includes passenger vehicles, commercial vehicles, autonomous mobility platforms, and specialty vehicles. Passenger vehicles dominate adoption, accounting for approximately 72% of total deployments, reflecting high production volumes and strong integration of infotainment and ADAS features. Within this segment, Ethernet penetration in mid- to high-end passenger vehicles exceeded 65% in newly developed platforms by 2025.

Autonomous and next-generation mobility platforms represent the fastest-growing end-user group, with an estimated CAGR of 40%, driven by dense sensor configurations, centralized computing, and continuous software updates. Commercial vehicles contribute steadily, accounting for around 18%, particularly in fleet telematics, driver monitoring, and predictive maintenance applications. The remaining end-users, including off-highway and specialty vehicles, collectively represent about 10%, serving niche but technically advanced use cases.

Asia Pacific accounted for the largest market share at 44% in 2025 however, Europe is expected to register the fastest growth, expanding at a CAGR of 38% between 2026 and 2033.

Asia Pacific benefits from high vehicle production volumes exceeding 50 million units annually, with Automotive Ethernet penetration rising above 60% in new electric and connected vehicle platforms. Europe’s accelerated growth is driven by premium vehicle manufacturing, where over 70% of newly developed models integrate Ethernet-based zonal architectures. North America held approximately 26% share in 2025, supported by autonomous vehicle testing programs and software-defined vehicle initiatives. South America and the Middle East & Africa together accounted for nearly 10%, reflecting gradual adoption aligned with localized manufacturing, fleet modernization, and infrastructure development. Regional differences in regulatory frameworks, digital readiness, and consumer demand for connected mobility significantly shape Automotive Ethernet deployment intensity and technology mix.

North America accounted for nearly 26% of the Automotive Ethernet market in 2025, supported by strong adoption in passenger vehicles, autonomous fleets, and commercial mobility solutions. Demand is driven by industries such as automotive manufacturing, logistics fleets, and mobility service providers integrating ADAS and centralized computing. Regulatory initiatives promoting vehicle safety, cybersecurity compliance, and connected vehicle pilots have accelerated Ethernet deployment. Technological trends include large-scale validation of 2.5G and 5G Ethernet links and increased use of over-the-air update frameworks. A leading semiconductor supplier in the region expanded Automotive Ethernet PHY production capacity by over 20% in 2024 to support OEM demand. Consumer behavior shows higher adoption of connected and autonomous features, with over 65% of new vehicle buyers prioritizing advanced infotainment and driver-assistance capabilities.

Europe represented approximately 22% of the Automotive Ethernet market in 2025, with Germany, France, and the UK collectively accounting for over 60% of regional adoption. Strong regulatory oversight related to vehicle safety, emissions, and cybersecurity is driving Ethernet integration into standardized vehicle platforms. Sustainability initiatives targeting wiring weight reduction of 20–25% further support Ethernet-based zonal architectures. Emerging technologies such as Time-Sensitive Networking and multi-gigabit Ethernet are increasingly adopted in premium and electric vehicles. A major European automotive supplier deployed Ethernet-enabled centralized gateways across multiple EV platforms, reducing system complexity by 30%. Consumer behavior reflects high demand for compliant, explainable, and secure vehicle systems driven by regulatory and environmental expectations.

Asia-Pacific led global adoption with a 44% market share in 2025, ranking first by volume. China, Japan, and South Korea together produced over 35 million vehicles annually, with Automotive Ethernet penetration exceeding 55% in newly developed models. Manufacturing trends emphasize cost-optimized Ethernet PHYs and large-scale integration in electric and connected vehicles. Regional innovation hubs focus on sensor fusion, AI-driven driving systems, and centralized vehicle computing. A leading Japanese OEM standardized Ethernet backbones across its EV lineup, enabling software update deployment time reductions of 50%. Consumer behavior in the region is driven by high acceptance of connected mobility features and rapid uptake of digital vehicle services.

South America accounted for approximately 6% of the Automotive Ethernet market in 2025, led by Brazil and Argentina. Vehicle production in Brazil exceeded 2.3 million units, with Ethernet adoption increasing in locally assembled passenger and light commercial vehicles. Infrastructure modernization and trade incentives supporting automotive localization are improving access to advanced networking technologies. Government policies encouraging safer and more connected vehicles are influencing OEM platform upgrades. A regional vehicle manufacturer integrated Ethernet-based infotainment networks to support connected services in over 40% of its new models. Consumer behavior shows growing preference for digital dashboards and localized infotainment content.

The Middle East & Africa region held around 4% of the Automotive Ethernet market in 2025, with growth concentrated in the UAE, Saudi Arabia, and South Africa. Demand is driven by premium vehicle imports, fleet modernization, and smart mobility initiatives. Technological modernization programs emphasize connected fleet management and safety systems. Trade partnerships and regulatory alignment with international automotive standards are facilitating Ethernet adoption. In the UAE, smart mobility programs integrated Ethernet-enabled vehicle diagnostics across public and commercial fleets, improving maintenance efficiency by 25%. Consumer behavior reflects higher demand for premium connectivity features and reliability in extreme operating environments.

China – 24% market share: Dominates the Automotive Ethernet market due to massive vehicle production capacity and high integration of Ethernet in electric and connected vehicles.

Germany – 18% market share: Leads through advanced automotive engineering, premium vehicle platforms, and strong deployment of Ethernet-based zonal architectures.

The Automotive Ethernet market exhibits a moderately consolidated competitive structure, characterized by a mix of global semiconductor leaders, automotive networking specialists, and system-level solution providers. More than 30 active competitors operate across PHYs, switches, controllers, and software stacks, with the top five companies collectively accounting for approximately 62% of total deployments. These leading players maintain strong positioning through early standard adoption, multi-gigabit Ethernet portfolios, and long-term supply agreements with global OEMs and Tier-1 suppliers.

Competition is increasingly shaped by innovation in 2.5G, 5G, and 10G Automotive Ethernet, Time-Sensitive Networking integration, and support for zonal vehicle architectures. Strategic initiatives include cross-industry partnerships between semiconductor firms and OEMs, joint validation programs, and accelerated product launches aligned with software-defined vehicle roadmaps. Between 2024 and 2025, over 45 new Automotive Ethernet PHY and switch variants were introduced globally, reflecting intense R&D activity.

Mergers and technology collaborations remain selective rather than widespread, as companies focus on interoperability and standard compliance rather than consolidation. Smaller players compete by targeting niche applications such as diagnostics, redundancy, or cybersecurity-enabled Ethernet stacks, representing nearly 18% of total solution offerings. Overall, competitive intensity is driven by performance differentiation, scalability, and compliance readiness rather than price alone.

Broadcom Inc.

NXP Semiconductors

Marvell Technology

Infineon Technologies

Texas Instruments

Analog Devices

Microchip Technology

Renesas Electronics

Realtek Semiconductor

Toshiba Electronic Devices & Storage

STMicroelectronics

ON Semiconductor

Technology development within the Automotive Ethernet market is centered on enabling higher bandwidth, deterministic communication, and scalable network architectures to support next-generation vehicles. Current deployments are dominated by 1000BASE-T1 solutions, which deliver 1 Gbps data rates over single twisted-pair cables and are widely used for ADAS controllers, infotainment head units, and centralized gateways. This technology supports reliable transmission over distances of up to 15 meters inside vehicles while reducing cabling weight by approximately 20–25% compared to legacy multi-wire networks. Emerging technologies are rapidly expanding bandwidth capacity. 2.5GBASE-T1 and 5GBASE-T1 implementations are increasingly adopted in premium and autonomous vehicle platforms, enabling aggregated sensor data flows exceeding 20 Gbps per vehicle. 10GBASE-T1 is under active validation for high-level automated driving systems, where vehicles may deploy more than 120 sensors, each generating high-resolution data streams.

Time-Sensitive Networking (TSN) is another critical advancement, providing deterministic communication for safety-critical functions. TSN-enabled Automotive Ethernet reduces network jitter by up to 70% and ensures bounded latency below 1 millisecond, supporting braking, steering, and drive-by-wire applications. Additionally, Ethernet-based zonal architectures are reshaping vehicle design by consolidating up to 40% of electronic control units into centralized compute domains, simplifying software updates and diagnostics. Integrated cybersecurity features such as hardware-based encryption and intrusion detection are also being embedded at the PHY and switch levels, increasing secure data handling efficiency by nearly 30%. Collectively, these technologies position Automotive Ethernet as the foundational in-vehicle networking solution for connected, autonomous, and software-defined mobility.

• In January 2025, NXP Semiconductors completed a $625 million acquisition of TTTech Auto, integrating automotive-grade safety middleware and embedded systems expertise to enhance functional safety and networking solutions tailored for Ethernet-based zonal architectures in next-generation vehicles.

• In April 2025, Infineon Technologies successfully launched a new automotive Ethernet PHY platform supporting 2.5 Gbps links with enhanced Time-Sensitive Networking (TSN) and low-power operation, aimed at central gateway applications and high-speed in-vehicle networking.

• In March 2025, Texas Instruments announced a significant product launch of its new 1000BASE-T1 automotive Ethernet PHY family, featuring improved electromagnetic interference (EMI) performance, reduced power consumption, and integrated MAC/PHY capabilities to simplify ECU designs for ADAS and EV networks.

• In March 2024, Analog Devices and the BMW Group collaborated to adopt ADI’s 10BASE-T1S Ethernet-to-Edge (E²B) solution in BMW vehicle platforms, enabling zonal architecture simplification and enhanced in-vehicle connectivity for ambient lighting and software-defined experiences. (investor.analog.com)

The Automotive Ethernet Market Report provides a comprehensive examination of the structural, technological, and regional facets shaping Automotive Ethernet adoption across global automotive ecosystems. It encapsulates segmentation based on technology types—ranging from 100BASE-T1 and 1000BASE-T1 to 2.5/5/10 Gbps and emerging higher-speed PHY variants—highlighting their relevance to vehicle applications such as ADAS and autonomous systems, infotainment and connectivity modules, diagnostics and telematics, powertrain control, and body electronics networks. The report also surveys how Automotive Ethernet integrates with overarching vehicle architectures, including traditional distributed, domain, and emerging zonal and centralized compute topologies.

Geographically, the scope spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, detailing regional infrastructure trends, manufacturing footprints, regulatory landscapes, and consumer adoption variations that influence deployment intensity. It captures infrastructure enablers like test and validation ecosystems, compliance frameworks, and ecosystem bodies supporting interoperability and standardization.

Technological dimensions include Time-Sensitive Networking (TSN), cybersecurity enhancements, Ethernet-to-Edge innovations, and in-vehicle gateway solutions, which collectively underpin functional safety and high-bandwidth data flows. The report also profiles strategic initiatives, partnerships, product ecosystem evolution, and niche segments such as optical Automotive Ethernet, low-power edge Ethernet, and multi-gigabit PHYs, providing business professionals and decision-makers with actionable insights into competitive dynamics, technology differentiation, and future-oriented network architectures in connected, software-defined mobility.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

35.5% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Broadcom Inc., NXP Semiconductors, Marvell Technology, Infineon Technologies, Texas Instruments, Analog Devices, Microchip Technology, Renesas Electronics, Realtek Semiconductor, Toshiba Electronic Devices & Storage, STMicroelectronics, ON Semiconductor |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |