Reports

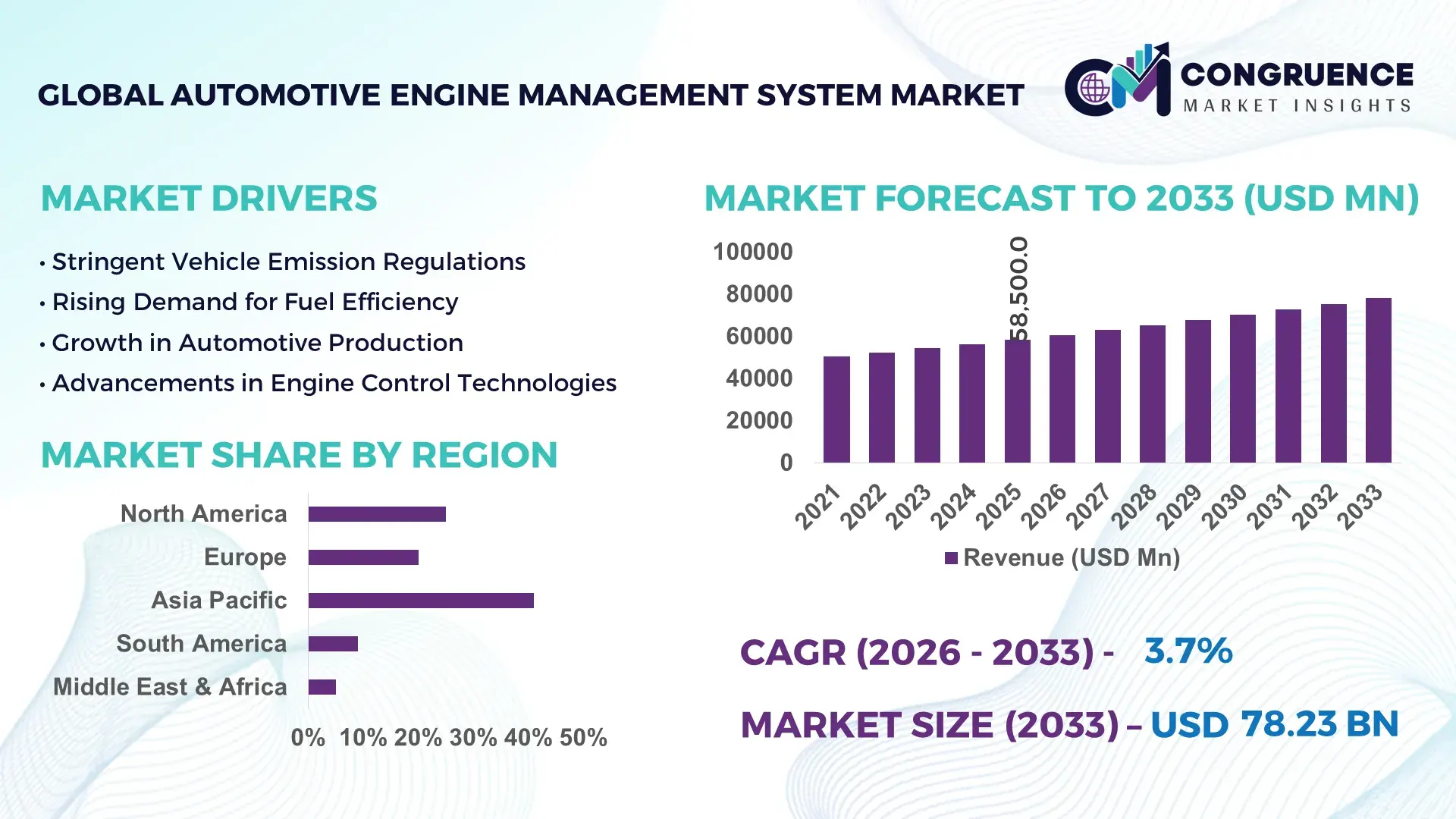

The Global Automotive Engine Management System Market was valued at USD 58500 Million in 2025 and is anticipated to reach a value of USD 78232.26 Million by 2033 expanding at a CAGR of 3.7% between 2026 and 2033. Growth is primarily driven by increasing demand for fuel-efficient and low-emission vehicles supported by advanced electronic control technologies.

The United States leads the Automotive Engine Management System market with robust production capacity exceeding 10 million vehicles annually, supported by high integration of electronic control units (ECUs) across passenger and commercial vehicles. Over 85% of newly manufactured vehicles in the country are equipped with advanced engine management systems incorporating real-time diagnostics and adaptive fuel injection technologies. Investments in automotive R&D exceeded USD 120 billion in recent years, with a significant share directed toward powertrain optimization and emission control systems. Key industry applications include hybrid powertrain management, turbocharged engine optimization, and onboard diagnostics. Additionally, adoption of AI-driven calibration tools has improved fuel efficiency by up to 12%, reinforcing technological leadership in the region.

Market Size & Growth: USD 58500 Million in 2025, projected to reach USD 78232.26 Million by 2033 at 3.7% CAGR, driven by stringent emission regulations and efficiency optimization.

Top Growth Drivers: Emission reduction compliance (65%), fuel efficiency improvement (58%), ECU integration in vehicles (72%).

Short-Term Forecast: By 2028, advanced engine control systems are expected to improve fuel efficiency by 10% and reduce emissions by 15%.

Emerging Technologies: AI-based engine calibration, predictive diagnostics systems, and cloud-connected ECU architectures.

Regional Leaders: North America (USD 24 billion by 2033) with advanced diagnostics adoption; Europe (USD 20 billion) driven by emission norms; Asia-Pacific (USD 28 billion) with high production volume.

Consumer Trends: Increasing preference for fuel-efficient vehicles, hybrid engines, and digitally integrated automotive systems.

Pilot Example: In 2024, a European OEM improved engine efficiency by 11% using AI-driven fuel mapping systems.

Competitive Landscape: Leading player holds approximately 22% share, followed by major global automotive component manufacturers.

Regulatory & ESG Impact: Adoption driven by emission standards targeting up to 30% reduction in CO₂ emissions by 2030.

Investment Patterns: Over USD 40 billion invested globally in powertrain electronics and smart engine systems development.

Innovation Outlook: Growth of software-defined vehicles and real-time engine analytics shaping future advancements.

The Automotive Engine Management System market continues to evolve with strong contributions from passenger vehicles accounting for nearly 60% of total system installations, followed by commercial vehicles and off-highway equipment. Technological innovations such as adaptive ignition timing, electronic throttle control, and integrated sensor networks have significantly enhanced engine efficiency and emission control. Regulatory frameworks focused on carbon neutrality and stricter emission limits are accelerating the deployment of advanced engine control units. Asia-Pacific shows rapid consumption growth due to high vehicle production volumes, while Europe emphasizes compliance-driven innovation. Emerging trends include electrified powertrain integration, hybrid engine optimization, and increased reliance on software-driven engine control platforms, positioning the market for sustained technological advancement.

The Automotive Engine Management System market holds strong strategic relevance as global automotive manufacturers shift toward efficiency optimization, emission reduction, and digital vehicle architecture. Engine management systems are central to modern powertrain performance, controlling fuel injection, ignition timing, and air-fuel ratios with high precision. Advanced AI-driven engine control technologies deliver up to 18% improvement compared to conventional mechanical control systems, enabling superior fuel economy and reduced emissions. North America dominates in volume production due to large-scale vehicle manufacturing, while Europe leads in adoption with over 70% of vehicles integrating advanced emission control technologies aligned with regulatory mandates.

By 2028, AI-enabled predictive engine management is expected to improve diagnostic accuracy by 25% and reduce maintenance costs by 20%, enhancing operational efficiency for fleet operators and consumers. Firms are committing to ESG metrics such as a 30% reduction in vehicle emissions by 2030 through the adoption of advanced engine management solutions and hybrid integration strategies. In 2024, a leading automotive manufacturer in Germany achieved a 14% reduction in fuel consumption through AI-based engine optimization and adaptive combustion control systems, demonstrating measurable efficiency gains.

The integration of cloud computing, edge analytics, and software-defined vehicle architectures is shaping future pathways for the Automotive Engine Management System market. Increasing electrification, coupled with hybrid engine systems, is further expanding the role of engine control technologies. As regulatory pressures intensify and sustainability targets become more stringent, the Automotive Engine Management System market is positioned as a critical pillar supporting resilience, compliance, and long-term sustainable growth across the global automotive ecosystem.

Stringent emission regulations across major automotive markets are significantly driving the demand for advanced Automotive Engine Management Systems. Governments in regions such as Europe and North America have implemented strict emission standards requiring reductions of up to 30% in nitrogen oxides and carbon emissions. These regulations necessitate precise control of combustion processes, fuel injection timing, and exhaust gas recirculation, all of which are managed by sophisticated engine control systems. Over 90% of modern vehicles now incorporate electronic engine management solutions to comply with these standards. Additionally, increasing adoption of hybrid and turbocharged engines requires advanced control mechanisms to maintain efficiency and performance. As regulatory frameworks continue to tighten, manufacturers are investing heavily in next-generation engine management technologies to ensure compliance and enhance vehicle efficiency.

The growing adoption of electric vehicles presents a significant restraint for the Automotive Engine Management System market. Fully electric vehicles eliminate the need for traditional internal combustion engine management systems, reducing overall demand for such technologies. Global electric vehicle adoption has surpassed 18% of total vehicle sales, indicating a steady transition toward electrification. Additionally, government incentives and policies supporting zero-emission vehicles are accelerating this shift. As automakers invest heavily in battery technologies and electric drivetrains, resources allocated to conventional engine management systems are gradually declining. This structural transition poses challenges for traditional component manufacturers, requiring them to adapt by diversifying into hybrid and electric powertrain control systems to remain competitive in the evolving automotive landscape.

The rapid expansion of hybrid vehicles presents substantial opportunities for the Automotive Engine Management System market. Hybrid powertrains require sophisticated coordination between internal combustion engines and electric motors, increasing the complexity and demand for advanced engine control systems. Hybrid vehicle production has grown by over 25% in recent years, with manufacturers focusing on optimizing fuel efficiency and reducing emissions. Engine management systems in hybrids enable seamless switching between power sources, improved regenerative braking efficiency, and enhanced energy utilization. Additionally, advancements in sensor technologies and real-time data analytics are enabling more precise engine control, further enhancing performance. As governments promote hybrid vehicles as a transitional solution toward full electrification, demand for integrated engine management systems is expected to rise significantly.

Increasing system complexity and integration costs present a major challenge for the Automotive Engine Management System market. Modern engine management systems require integration of multiple sensors, control units, and software platforms, significantly increasing development and manufacturing costs. Advanced systems may include over 50 sensors and multiple ECUs, leading to higher production complexity and testing requirements. Additionally, the need for cybersecurity measures and software updates further adds to system costs. Automakers must also ensure compatibility with evolving vehicle architectures, including hybrid and connected systems, which complicates design and deployment processes. These challenges can lead to longer development cycles and increased expenses, particularly for smaller manufacturers, limiting widespread adoption and creating barriers to entry in the market.

• Integration of AI-Driven Engine Control Systems:

Artificial intelligence integration is transforming engine management systems, with over 68% of newly developed vehicles incorporating AI-based calibration and predictive analytics modules. These systems improve combustion efficiency by up to 15% and reduce fuel consumption by approximately 10%. Automotive manufacturers are increasingly deploying machine learning algorithms for real-time optimization of ignition timing and fuel injection, particularly in high-performance and hybrid vehicles. In North America and Europe, nearly 60% of premium vehicles now feature AI-assisted diagnostics, enabling predictive maintenance and reducing unplanned downtime by 20%.

• Expansion of Sensor Networks and Real-Time Data Processing:

Modern automotive engine management systems are witnessing a surge in sensor integration, with advanced vehicles utilizing more than 70 sensors per engine system. These sensors monitor parameters such as temperature, pressure, and air-fuel ratios in real time, enhancing engine efficiency by up to 12%. Over 75% of commercial vehicles now rely on multi-sensor configurations to ensure compliance with emission standards. The increasing use of edge computing technologies enables faster data processing, reducing response times by nearly 30%, thereby improving overall vehicle performance and reliability.

• Growth of Hybrid Powertrain Management Systems:

Hybrid vehicle adoption is driving demand for sophisticated engine management solutions, with hybrid models accounting for over 28% of global vehicle production. Engine management systems in hybrid vehicles facilitate seamless coordination between internal combustion engines and electric motors, improving energy efficiency by up to 18%. Approximately 65% of hybrid vehicles now use integrated control units capable of managing dual power sources simultaneously. This trend is particularly strong in Asia-Pacific, where hybrid vehicle production has increased by more than 22% in recent years.

• Transition Toward Software-Defined Vehicle Architectures:

The shift toward software-defined vehicles is reshaping the Automotive Engine Management System market, with over 55% of new vehicles incorporating centralized electronic architectures. Software-based control systems allow over-the-air updates, reducing maintenance costs by up to 25% and enabling continuous performance improvements. Nearly 50% of automotive OEMs are investing in cloud-connected engine management platforms, supporting real-time data analytics and remote diagnostics. This trend is accelerating innovation cycles and enhancing system adaptability across different vehicle platforms.

The Automotive Engine Management System market segmentation reflects a diverse and technologically evolving landscape across types, applications, and end-users. By type, electronic control units and integrated engine management modules dominate due to their critical role in optimizing engine performance and emission control. By application, passenger vehicles account for the largest share, driven by high production volumes and increasing demand for fuel-efficient systems, while commercial vehicles are rapidly adopting advanced solutions for fleet efficiency and compliance. End-user segmentation highlights automotive OEMs as primary adopters, accounting for a significant portion of system integration, followed by aftermarket service providers supporting maintenance and upgrades. Hybrid and connected vehicle segments are emerging as key growth areas, supported by regulatory pressures and consumer demand for enhanced vehicle performance and sustainability.

The Automotive Engine Management System market includes key product types such as Electronic Control Units (ECUs), Engine Control Modules (ECMs), Powertrain Control Modules (PCMs), and integrated engine management systems. ECUs lead the segment with approximately 46% share due to their essential role in controlling engine parameters, enabling real-time adjustments in fuel injection, ignition timing, and emission control. In comparison, ECMs hold around 28% adoption, while PCMs account for nearly 16%. However, integrated engine management systems are emerging as the fastest-growing segment, expanding at an estimated CAGR of 6.1% due to their ability to consolidate multiple control functions into a single platform, reducing system complexity and improving efficiency.

Other niche types, including standalone ignition controllers and fuel management modules, collectively contribute about 10% of the market, primarily used in specialized and performance-oriented vehicles. Increasing demand for compact and high-performance systems is driving innovation across all product categories.

Passenger vehicles dominate the Automotive Engine Management System market, accounting for approximately 62% of total adoption due to high production volumes and increasing consumer demand for fuel-efficient and low-emission vehicles. Commercial vehicles represent around 25% of the market, driven by fleet operators focusing on fuel optimization and regulatory compliance. In comparison, off-highway vehicles, including construction and agricultural machinery, hold a smaller share of about 13%.

Hybrid vehicle applications are the fastest-growing segment, with an estimated CAGR of 7.2%, supported by rising environmental concerns and government incentives promoting cleaner mobility solutions. Engine management systems in hybrid applications enable efficient coordination between electric motors and combustion engines, significantly enhancing overall performance. Other applications, including performance vehicles and specialty automotive segments, contribute to the remaining share, driven by demand for high-performance tuning and precision engine control.

Automotive OEMs represent the leading end-user segment in the Automotive Engine Management System market, accounting for approximately 70% of total demand due to direct integration of systems during vehicle manufacturing. Aftermarket service providers hold around 20% share, driven by maintenance, repair, and system upgrades across existing vehicle fleets. Fleet operators and logistics companies contribute nearly 10%, leveraging advanced engine management solutions to optimize operational efficiency.

Fleet operators are the fastest-growing end-user segment, expanding at an estimated CAGR of 6.8%, supported by increasing adoption of predictive maintenance and real-time diagnostics. These systems help reduce fuel consumption by up to 12% and lower operational downtime by approximately 18%, making them critical for large-scale fleet management. Other end-users, including performance tuning companies and specialized vehicle manufacturers, contribute to the remaining share, focusing on customized engine optimization solutions.

Region Asia-Pacific accounted for the largest market share at 41% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 4.2% between 2026 and 2033.

Asia-Pacific’s dominance is supported by vehicle production exceeding 45 million units annually, with China contributing over 30 million units alone. India and Japan collectively add more than 12 million vehicles, strengthening regional demand for advanced Automotive Engine Management Systems. Europe holds approximately 28% share, driven by stringent emission regulations across Germany, France, and the UK, where over 85% of vehicles are equipped with advanced ECUs. North America accounts for nearly 22% of the market, supported by high adoption of AI-enabled engine control systems in over 65% of premium vehicles. South America and the Middle East & Africa collectively contribute around 9%, with growing automotive production and infrastructure investments. Increasing hybrid vehicle penetration, which surpassed 25% in key markets, and rising integration of software-defined vehicle architectures are shaping regional consumption patterns globally.

How are advanced emission standards and digital powertrain technologies accelerating system adoption?

North America accounts for approximately 22% of the Automotive Engine Management System market, driven by strong automotive manufacturing output exceeding 14 million vehicles annually. Key industries include passenger vehicles, commercial fleets, and high-performance automotive segments. Regulatory frameworks such as stringent emission standards targeting up to 30% reduction in greenhouse gas emissions are accelerating the adoption of advanced engine management technologies. Over 70% of vehicles in this region are equipped with multi-sensor engine control systems, supporting real-time diagnostics and fuel optimization. Technological advancements include widespread adoption of AI-driven engine calibration and cloud-connected ECUs, improving fuel efficiency by nearly 12%. A leading regional automotive component manufacturer recently implemented predictive engine diagnostics across its product portfolio, reducing maintenance downtime by 18%. Consumer behavior reflects a strong preference for fuel-efficient and performance-optimized vehicles, with over 60% of buyers prioritizing advanced engine technologies and digital integration features.

What role do strict emission mandates and sustainable mobility initiatives play in system innovation?

Europe holds approximately 28% of the Automotive Engine Management System market, with Germany, the UK, and France serving as key automotive hubs. The region’s market is strongly influenced by regulatory bodies enforcing emission reductions of up to 35%, prompting widespread adoption of advanced engine control systems. More than 80% of newly manufactured vehicles integrate high-precision ECUs designed for emission compliance and fuel efficiency optimization. The adoption of emerging technologies such as hybrid powertrain management and real-time emission monitoring systems is significantly increasing. A prominent European automotive supplier has introduced advanced engine control modules capable of reducing fuel consumption by 10% through adaptive combustion control. Consumer behavior is shaped by regulatory pressure, leading to higher demand for environmentally compliant and technologically advanced automotive solutions. Over 65% of consumers prefer vehicles equipped with intelligent engine management systems aligned with sustainability goals.

How is large-scale vehicle production and rapid industrialization shaping demand dynamics?

Asia-Pacific dominates the Automotive Engine Management System market in terms of volume, accounting for over 41% of global demand. China, India, and Japan are the leading consuming countries, collectively producing more than 45 million vehicles annually. Rapid industrialization and expanding automotive manufacturing infrastructure are key growth drivers. Over 75% of vehicles produced in the region now incorporate electronic engine management systems to meet evolving emission standards. The region is also a hub for technological innovation, with increasing adoption of hybrid engine management and AI-based control systems. A major automotive manufacturer in Japan has deployed advanced engine management solutions that improved fuel efficiency by 13% across its hybrid vehicle lineup. Consumer behavior in this region is influenced by affordability and efficiency, with more than 55% of buyers prioritizing fuel economy and low maintenance costs, driving widespread adoption of advanced engine technologies.

How are industrial expansion and trade policies influencing automotive system demand?

South America represents approximately 5% of the Automotive Engine Management System market, with Brazil and Argentina being the primary contributors. The region’s automotive production exceeds 3 million vehicles annually, supporting demand for engine management systems in both passenger and commercial segments. Infrastructure development and expansion of the automotive manufacturing sector are key growth drivers. Government incentives promoting domestic vehicle production and trade agreements supporting automotive exports are influencing market expansion. A regional automotive supplier has recently introduced cost-effective engine management modules, improving fuel efficiency by 9% in mid-range vehicles. Consumer behavior is characterized by price sensitivity, with over 60% of buyers prioritizing cost-effective solutions that deliver fuel efficiency and reliability, contributing to steady market growth.

What factors are driving modernization and adoption of advanced engine technologies?

The Middle East & Africa account for around 4% of the Automotive Engine Management System market, with key growth countries including the UAE and South Africa. Demand is largely driven by sectors such as oil & gas transportation, construction, and commercial vehicle operations. Vehicle imports exceed 2 million units annually, creating opportunities for advanced engine management system integration. Technological modernization is evident through increasing adoption of electronic control systems in over 50% of imported vehicles. Trade partnerships and regulatory initiatives aimed at improving fuel efficiency are supporting market growth. A regional distributor has implemented advanced diagnostic engine systems that reduced fuel consumption by 8% in commercial fleets. Consumer behavior varies, with strong demand for durable and performance-oriented vehicles, particularly in harsh environmental conditions, driving adoption of reliable engine management technologies.

United States Automotive Engine Management System Market – 21% share: High vehicle production capacity and widespread adoption of advanced ECU technologies across passenger and commercial vehicles.

China Automotive Engine Management System Market – 29% share: Strong automotive manufacturing output exceeding 30 million vehicles annually and rapid integration of hybrid engine management systems.

The Automotive Engine Management System market is moderately consolidated, with the top five companies accounting for approximately 54% of the total market share. Over 35 active global competitors operate across different segments, including ECU manufacturing, software development, and integrated powertrain solutions. Leading companies are focusing on strategic partnerships, product innovation, and digital transformation to strengthen their market position.

Recent trends indicate that more than 60% of key players are investing in AI-driven engine control technologies and predictive diagnostics to enhance product offerings. Mergers and acquisitions have increased by nearly 18% in the past two years, reflecting efforts to expand technological capabilities and geographic presence. Additionally, over 45% of companies have introduced new engine management solutions designed for hybrid and electric powertrains, aligning with the industry’s transition toward electrification.

Innovation remains a critical competitive factor, with companies allocating up to 12% of their annual budgets to research and development. The integration of cloud-based platforms and software-defined vehicle architectures is further intensifying competition. Market participants are also focusing on sustainability initiatives, with over 50% committing to emission reduction technologies and energy-efficient product designs, shaping the evolving competitive landscape.

Robert Bosch GmbH

Continental AG

Denso Corporation

Delphi Technologies

Hitachi Astemo Ltd.

ZF Friedrichshafen AG

Magneti Marelli S.p.A.

Sensata Technologies

Infineon Technologies AG

NXP Semiconductors N.V.

The Automotive Engine Management System market is undergoing rapid technological transformation driven by advancements in electronics, software integration, and real-time data processing. Modern engine management systems increasingly rely on high-performance microcontrollers capable of executing over 200 million instructions per second, enabling precise control of fuel injection, ignition timing, and emission regulation. Advanced Electronic Control Units (ECUs) now integrate more than 50–70 sensors per vehicle, capturing parameters such as air intake pressure, exhaust composition, and engine temperature to optimize performance dynamically.

Artificial intelligence and machine learning are becoming integral to next-generation systems, with over 60% of premium vehicles incorporating AI-based predictive diagnostics. These technologies enhance fault detection accuracy by up to 25% and reduce maintenance intervals by approximately 20%. Additionally, edge computing capabilities are being embedded within engine control modules, reducing data processing latency by nearly 30% and enabling faster response times under varying driving conditions. The shift toward software-defined vehicle architectures is another critical development, with over 55% of new vehicle platforms adopting centralized computing systems. This enables over-the-air updates for engine control software, reducing service costs by up to 25% and improving system adaptability. Hybrid powertrain integration is also driving innovation, requiring advanced coordination between internal combustion engines and electric motors, improving overall energy efficiency by up to 18%.

Furthermore, advancements in semiconductor technologies, including 7nm and 10nm chipsets, are enhancing computational efficiency while reducing power consumption by nearly 15%. The integration of cybersecurity frameworks within engine management systems is also gaining traction, with over 40% of manufacturers implementing secure communication protocols to protect vehicle data. These technological advancements are positioning engine management systems as critical components in achieving performance optimization, emission compliance, and digital transformation in the automotive industry.

• In March 2025, Robert Bosch GmbH expanded its next-generation engine control unit portfolio with enhanced AI-enabled combustion optimization technology, improving fuel efficiency by up to 12% and reducing nitrogen oxide emissions. The system integrates advanced sensor fusion and real-time analytics for improved engine performance. Source: www.bosch.com

• In September 2024, Continental AG launched an advanced powertrain control module designed for hybrid vehicles, enabling seamless coordination between electric motors and combustion engines. The solution demonstrated a 15% improvement in energy efficiency and enhanced emission compliance for next-generation vehicle platforms. Source: www.continental.com

• In May 2025, Denso Corporation introduced a high-speed ECU platform supporting over-the-air software updates and real-time diagnostics, reducing system latency by 30%. The platform is designed to support software-defined vehicle architectures and improve engine performance optimization capabilities. Source: www.denso.com

• In November 2024, ZF Friedrichshafen AG developed an integrated engine management solution for commercial vehicles, incorporating predictive maintenance features that reduced downtime by 18% and improved fuel efficiency through adaptive engine control technologies. Source: www.zf.com

The Automotive Engine Management System Market Report provides a comprehensive analysis of the industry by covering a wide range of technological, operational, and regional dimensions. The scope includes detailed segmentation across product types such as Electronic Control Units (ECUs), Engine Control Modules (ECMs), Powertrain Control Modules (PCMs), and integrated engine management systems, which collectively account for over 90% of system installations in modern vehicles. The report also evaluates applications across passenger vehicles, commercial vehicles, and off-highway machinery, with passenger vehicles representing more than 60% of system deployments globally.

Geographically, the report encompasses key regions including Asia-Pacific, North America, Europe, South America, and the Middle East & Africa, collectively representing 100% of global automotive production. Asia-Pacific alone contributes over 40% of total vehicle output, making it a focal point for market expansion and manufacturing investments. The scope further includes analysis of emerging markets where vehicle production is increasing by over 8% annually, driving demand for advanced engine management solutions.

The report also examines technological advancements such as AI-driven engine control, cloud-connected ECUs, and hybrid powertrain integration, which are being adopted in more than 55% of newly manufactured vehicles. It highlights industry focus areas including emission reduction technologies, predictive diagnostics, and software-defined vehicle architectures. Additionally, the scope extends to niche segments such as performance tuning systems and aftermarket upgrades, which together contribute nearly 15% of overall system demand. This structured coverage ensures a detailed understanding of market dynamics, technological evolution, and strategic opportunities for stakeholders.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

3.7% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Robert Bosch GmbH, Continental AG, Denso Corporation, Delphi Technologies, Hitachi Astemo Ltd., ZF Friedrichshafen AG, Magneti Marelli S.p.A., Sensata Technologies, Infineon Technologies AG, NXP Semiconductors N.V. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |