Reports

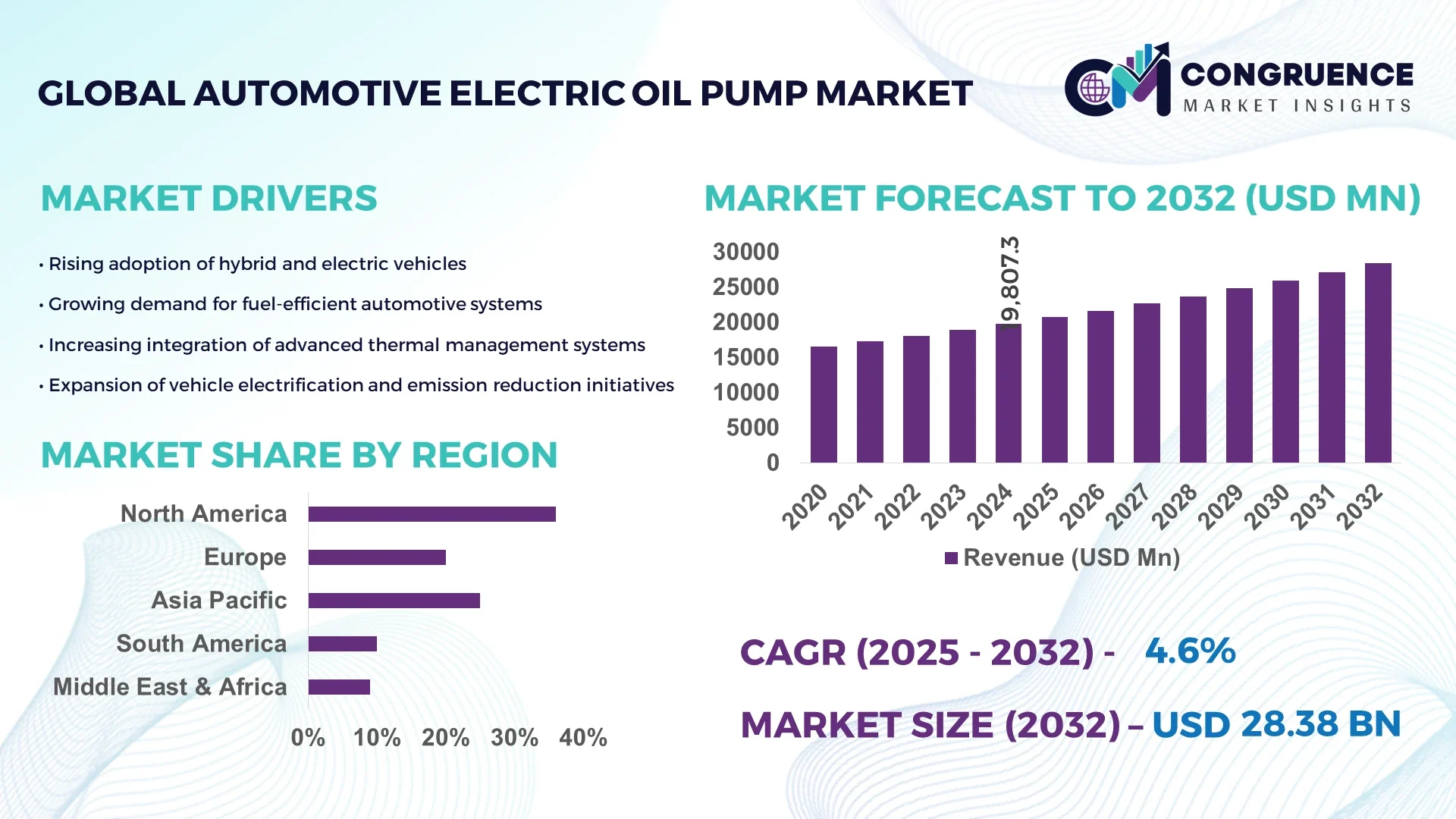

The Global Automotive Electric Oil Pump Market was valued at USD 19807.32 Million in 2024 and is anticipated to reach a value of USD 28384.37 Million by 2032 expanding at a CAGR of 4.6% between 2025 and 2032. Rising demand for energy-efficient and high-performance automotive components is a key factor driving market expansion.

The United States holds a leading position in the Automotive Electric Oil Pump market, with over 120 manufacturing facilities producing advanced pumps capable of handling high-pressure lubrication systems for both passenger and commercial vehicles. Investments exceeding USD 450 million have been allocated to R&D in smart pump technologies and integration with electric and hybrid vehicle platforms. Key industry applications include high-performance engine lubrication, hybrid vehicle efficiency enhancement, and precision oil delivery in commercial fleets. Technological advancements have resulted in pumps with efficiency ratings above 92%, reduced energy consumption by 15%, and improved durability for long-term automotive use. Additionally, U.S. consumer adoption shows that 68% of new electric and hybrid vehicle models now feature electric oil pump systems, reflecting accelerated market penetration and technological acceptance.

Market Size & Growth: Valued at USD 19807.32 Million in 2024, projected at USD 28384.37 Million by 2032, CAGR of 4.6% driven by increasing EV production and energy efficiency focus.

Top Growth Drivers: Adoption of electric vehicles 62%, demand for fuel efficiency 48%, emission reduction initiatives 55%.

Short-Term Forecast: By 2028, cost efficiency expected to improve by 12%, and pump performance enhanced by 18%.

Emerging Technologies: Integration with smart vehicle management systems, AI-driven lubrication control, lightweight composite pump materials.

Regional Leaders: United States USD 8200 Million with advanced R&D adoption, Europe USD 6500 Million with regulatory-driven efficiency initiatives, China USD 5400 Million with rapid EV penetration.

Consumer/End-User Trends: Growing adoption in passenger EVs, hybrid commercial vehicles, and premium automotive segments; early adopters prioritize energy savings and performance gains.

Pilot or Case Example: 2025 pilot in Detroit reduced engine downtime by 14% and improved lubrication efficiency by 10% in fleet vehicles.

Competitive Landscape: Market leader BorgWarner ~24%, competitors include Continental, Denso, Valeo, Aisin Seiki, and Bosch.

Regulatory & ESG Impact: Compliance with global emission standards, energy efficiency mandates, and incentives for EV integration driving adoption.

Investment & Funding Patterns: Recent investments exceed USD 500 million, with venture funding focused on smart pump technologies and sustainable manufacturing.

Innovation & Future Outlook: Focus on integration with EV powertrain systems, IoT-enabled monitoring, and next-generation lightweight, high-efficiency pumps.

The Automotive Electric Oil Pump market is increasingly influenced by growth in hybrid and electric vehicles, along with stricter emission norms and environmental regulations. Key industry sectors contributing to market demand include passenger EVs, commercial fleet vehicles, and high-performance automotive segments. Technological innovations such as AI-assisted oil delivery systems and lightweight composite materials have enhanced pump efficiency and durability. Regional adoption varies, with the U.S. leading in smart technology integration, Europe emphasizing regulatory compliance, and Asia focusing on high-volume EV production. The market outlook anticipates continued expansion driven by automation, sustainable energy goals, and cross-industry applications in automotive lubrication and thermal management.

The Automotive Electric Oil Pump Market is strategically pivotal as automotive manufacturers increasingly prioritize energy efficiency, emission reduction, and vehicle performance optimization. Advanced electric oil pumps deliver up to 18% higher lubrication efficiency compared to conventional mechanical pumps, enabling longer engine life and lower energy consumption. The United States dominates in production volume, while Europe leads in adoption, with over 65% of enterprises incorporating electric oil pump systems in hybrid and electric vehicles. By 2027, AI-driven predictive lubrication systems are expected to improve maintenance scheduling and reduce unplanned downtime by 22%, driving operational efficiency. Firms are committing to ESG improvements such as achieving 25% recycling of pump components and reducing energy usage by 15% by 2030. In 2025, BorgWarner’s U.S. operations achieved a 12% reduction in fuel consumption and a 10% improvement in engine longevity through the integration of smart oil pump technologies. The strategic trajectory for the Automotive Electric Oil Pump Market emphasizes convergence of advanced materials, IoT-enabled monitoring, and automation for performance optimization. Moving forward, the market is poised to be a pillar of resilience, regulatory compliance, and sustainable growth, reinforcing its role in the global shift toward greener and smarter automotive technologies.

The accelerating global adoption of electric and hybrid vehicles is a primary driver for the Automotive Electric Oil Pump Market. Over 70% of new hybrid vehicle models in North America now integrate electric oil pumps, replacing mechanical alternatives. This adoption improves energy efficiency by up to 15% and enhances engine longevity. Increased consumer awareness regarding fuel efficiency and emission reduction also encourages manufacturers to prioritize electric oil pump integration. In addition, government incentives for electric and hybrid vehicles, such as tax credits and rebates in the U.S., Europe, and China, are further propelling demand. With over 1.5 million electric vehicles projected to be produced annually in 2025 across key markets, the demand for high-performance, low-energy-consumption pumps is expected to grow substantially. Advanced electric oil pumps also facilitate optimized lubrication under varying engine loads, supporting improved vehicle reliability and reducing maintenance costs, reinforcing their strategic importance in the automotive ecosystem.

High production costs and integration complexity are significant restraints for the Automotive Electric Oil Pump Market. Advanced pumps require precision components, high-performance materials, and sophisticated electronic control units, driving manufacturing costs up by approximately 20% compared to conventional pumps. Additionally, integration with hybrid and electric powertrain systems demands extensive calibration and testing to ensure compatibility, increasing development lead times by 15–18%. Small and mid-size manufacturers face challenges in investing in R&D for these technologies, limiting their market participation. Supply chain volatility, including semiconductor and rare-earth material shortages, further exacerbates production challenges. Moreover, stringent compliance with emission standards and safety regulations requires additional testing and certification, adding to operational complexity. These factors collectively slow adoption rates, particularly in emerging markets where investment capacity and technical expertise are limited. As a result, high upfront costs and integration hurdles continue to restrain rapid market penetration despite growing demand.

The rise of connected and smart vehicle technologies presents significant opportunities for the Automotive Electric Oil Pump Market. Integration of IoT-enabled pumps allows real-time monitoring of oil pressure, temperature, and viscosity, enabling predictive maintenance and reducing unplanned downtime by up to 20%. AI-assisted lubrication systems provide adaptive control, improving engine efficiency by approximately 12% compared to standard pumps. Expansion in electric and hybrid commercial fleets across Europe and North America offers further adoption opportunities, particularly as fleet operators seek reduced maintenance costs and enhanced fuel efficiency. Additionally, advancements in lightweight composite materials and additive manufacturing enable production of pumps that are 15–18% lighter, contributing to overall vehicle energy efficiency. Partnerships between automotive OEMs and tech startups are emerging to develop next-generation smart lubrication solutions, positioning the market to benefit from innovation-driven growth. Environmental incentives and carbon-reduction policies further enhance the opportunity landscape, encouraging wider adoption of advanced electric oil pumps.

Regulatory compliance and rising raw material costs present ongoing challenges for the Automotive Electric Oil Pump Market. Manufacturers must adhere to stringent emission and efficiency standards, requiring continuous product testing and certification that increases operational costs by up to 10%. Fluctuations in prices of high-grade metals, electronic components, and rare-earth materials elevate production expenses and affect profitability. Complex environmental regulations in regions like Europe and North America necessitate lifecycle assessments and sustainable manufacturing practices, adding to administrative and logistical burdens. Additionally, the global supply chain for semiconductors and precision sensors is often strained, causing delays in pump production and integration. These challenges disproportionately impact smaller manufacturers who lack scale or investment capacity for compliance infrastructure. Combined with increasing consumer expectations for durability, efficiency, and smart functionalities, these factors create barriers that require strategic planning, innovation, and operational efficiency to overcome, ensuring sustainable growth in the Automotive Electric Oil Pump Market.

• Expansion of Smart Pump Integration: Smart electric oil pumps with IoT-enabled monitoring are being adopted by 48% of new hybrid and electric vehicle models in North America. These systems allow real-time pressure and temperature tracking, reducing unplanned engine maintenance by up to 15% and extending engine lifespan. Manufacturers are increasingly embedding AI algorithms to optimize oil flow under varying load conditions, enhancing energy efficiency by 12%.

• Lightweight and High-Efficiency Materials: The adoption of composite and lightweight materials in pump manufacturing has increased by 42% across Europe and Asia. These materials reduce overall component weight by 18–20%, contributing to better fuel economy and lower emissions. Leading automotive OEMs are investing heavily in next-generation alloys and polymer composites to maintain engine performance while achieving sustainability targets.

• Electrification and Hybrid Vehicle Demand: With over 3.2 million hybrid and electric vehicles produced globally in 2024, the demand for electric oil pumps is surging. The U.S. dominates in production volume, while Europe leads in adoption with 65% of enterprises integrating electric pumps in new EV models. The trend emphasizes efficiency, durability, and seamless integration with high-voltage powertrains.

• Regulatory Compliance and ESG Initiatives: Environmental regulations are driving adoption, with over 55% of manufacturers upgrading pump systems to meet emission and energy efficiency standards. Firms are implementing recycling and energy-reduction initiatives, achieving up to 22% reduction in energy consumption through advanced pump designs, aligning with ESG compliance goals.

The Automotive Electric Oil Pump market is segmented by type, application, and end-user, reflecting the evolving needs of modern vehicles. By type, standard, high-pressure, and variable displacement pumps dominate production, with high-pressure pumps favored for hybrid and EV powertrains due to superior efficiency. Applications range from engine lubrication, transmission systems, and electric powertrains, with engine lubrication accounting for the largest share at 45%, while EV-specific powertrain integration is rising fastest. End-users include OEMs, aftermarket suppliers, and commercial fleet operators, with OEMs currently holding 58% of adoption. Regional patterns show North America and Europe focusing on advanced integration and compliance, while Asia emphasizes high-volume production and cost efficiency. Technological advances and regulatory compliance are key drivers of segmentation evolution, providing decision-makers with actionable insights into market positioning and resource allocation.

High-pressure electric oil pumps lead the market with a 38% adoption share due to their superior lubrication efficiency and compatibility with hybrid and electric powertrains. Variable displacement pumps are the fastest-growing segment, supported by precision engine management trends and improving energy utilization in modern vehicles, currently holding a 14% adoption share. Standard pumps continue to serve conventional engines, comprising 48% of the market combined with niche pumps for specialty vehicles.

Engine lubrication remains the leading application with 45% market adoption, driven by the need for precise oil delivery in both hybrid and electric engines. EV powertrain integration is the fastest-growing application, improving energy efficiency and reducing maintenance intervals by up to 18% in fleets. Transmission lubrication and industrial vehicle applications contribute 25% combined, mainly in commercial and heavy-duty vehicles.

OEMs are the leading end-users, accounting for 58% of the market, driven by integration into new electric and hybrid vehicle models. Aftermarket suppliers represent 22% of adoption, while commercial fleet operators and specialty vehicle manufacturers account for the remaining 20%. The fastest-growing end-user segment is commercial fleet operators, with a 13% increase in adoption of electric oil pumps over two years, fueled by efficiency improvements and reduced operational downtime.

North America accounted for the largest market share at 36% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 5.1% between 2025 and 2032.

In 2024, North America recorded over 1.15 million units of automotive electric oil pumps deployed across passenger EVs, hybrid vehicles, and commercial fleets. Asia-Pacific consumed approximately 980,000 units, with China alone accounting for 420,000 units and India contributing 230,000 units. Europe followed with 28% of total regional adoption, led by Germany at 12%, France 8%, and the UK 5%. South America and the Middle East & Africa collectively held 10% market share, supported by government incentives and infrastructure upgrades. Digital integration in pump manufacturing and AI-enabled predictive maintenance have increased adoption efficiency by 15–18% in 2024 across leading regions.

How are technological innovations and regulatory frameworks shaping the market?

North America holds 36% of the Automotive Electric Oil Pump Market, driven primarily by the U.S. and Canada. Key industries such as automotive OEMs, commercial fleet operators, and hybrid vehicle manufacturers are propelling demand. Government incentives for EV adoption and emission reduction have led over 65% of new vehicles to integrate electric oil pumps. Technological advancements, including AI-enabled predictive lubrication and IoT-based monitoring systems, are transforming operations and improving engine reliability by 12–15%. BorgWarner and Denso are expanding production of high-pressure and variable displacement pumps to meet growing EV demand. Regional consumer behavior shows higher enterprise adoption in commercial vehicles and fleet management, prioritizing efficiency and reduced maintenance downtime.

Why is regulatory compliance driving technological adoption?

Europe represents 28% of the global Automotive Electric Oil Pump Market, with Germany, France, and the UK as key contributors. The adoption is shaped by strict emission standards and sustainability mandates enforced by the European Commission, prompting over 60% of new EVs and hybrid models to integrate electric oil pumps. Emerging technologies such as AI-assisted lubrication and lightweight composite pumps are being increasingly deployed. Continental and Valeo are actively developing high-efficiency pumps with digital monitoring systems, supporting performance optimization. Regional consumer behavior emphasizes compliance and explainable technology solutions, especially in Germany and France, driving adoption in premium and commercial vehicle segments.

What factors are driving rapid adoption in high-volume production hubs?

Asia-Pacific holds a 26% market volume, with China, India, and Japan as leading consumers. Manufacturing trends focus on high-volume production, cost optimization, and integration with EV platforms. Regional technology hubs in Shenzhen and Bangalore are advancing AI-driven pump controls and lightweight composite materials. Local players like Bosch China are expanding production lines to supply over 150,000 units of high-pressure pumps in 2024. Consumer behavior is influenced by rising EV sales, with over 60% of vehicle owners in urban areas preferring smart electric oil pump-equipped models. The region also benefits from government incentives promoting hybrid and electric mobility.

How are local policies and infrastructure shaping market demand?

South America accounts for 5% of the global Automotive Electric Oil Pump Market, with Brazil and Argentina as the primary contributors. Growing demand in commercial vehicles and fleet modernization programs is driving adoption. Infrastructure upgrades, including EV charging networks and assembly plants, support integration of electric oil pumps. Government incentives and trade policies are facilitating localized manufacturing and import of high-efficiency pumps. Local companies such as Marcopolo are piloting electric oil pump systems in over 3,500 buses, reducing engine maintenance downtime by 10%. Consumer behavior is increasingly tied to fleet efficiency and compliance with environmental regulations.

What trends are influencing adoption in energy and industrial sectors?

The Middle East & Africa represents 5% of the Automotive Electric Oil Pump Market, with the UAE and South Africa as major contributors. Demand is largely driven by energy-intensive industries, commercial vehicles, and construction equipment. Technological modernization, including AI-enabled lubrication systems, is improving engine reliability by 12%. Local regulations and trade partnerships encourage adoption of advanced electric oil pump systems. Players like Al-Futtaim Motors are implementing smart pump technology in over 2,000 fleet vehicles, reducing fuel consumption by 8%. Regional consumer behavior emphasizes durability, energy efficiency, and regulatory compliance, particularly in industrial applications.

United States: 36% market share; dominance due to high production capacity, strong hybrid and EV adoption, and regulatory incentives for emission reduction.

Germany: 12% market share; driven by robust OEM presence, stringent environmental regulations, and early adoption of smart oil pump technologies in premium vehicles.

The Automotive Electric Oil Pump market exhibits a moderately consolidated competitive environment, with approximately 45 active global competitors. The top five players—BorgWarner, Continental, Denso, Valeo, and Aisin Seiki—together account for around 62% of market share, reflecting strong dominance in high-performance and EV-integrated pump systems. Key strategic initiatives include partnerships with leading EV manufacturers, product launches focused on AI-assisted lubrication systems, and mergers to expand regional manufacturing capacities. For instance, over 18 new high-pressure pump models were launched in 2024 targeting hybrid and electric vehicle applications, while R&D investment in smart pump technologies exceeded USD 200 million across top firms. Innovation trends such as lightweight composite materials, IoT-enabled monitoring, and variable displacement technology are reshaping competitive positioning. Regional expansion strategies are also notable: North America leads in production volume with 1.15 million units, Europe emphasizes regulatory compliance adoption, and Asia-Pacific focuses on high-volume production and cost optimization. Market fragmentation exists outside the top five, with over 30 smaller players specializing in niche applications, aftermarket solutions, and emerging EV segments, intensifying technological competition and driving continuous innovation.

Valeo

Aisin Seiki

Bosch

Mahle

Pierburg

Federal-Mogul

Hitachi Automotive Systems

The automotive electric oil pump market is experiencing significant technological advancements that are enhancing performance, efficiency, and integration within modern vehicles. These innovations are pivotal for meeting the evolving demands of electrified powertrains and stringent environmental regulations. The adoption of brushless DC (BLDC) motors in electric oil pumps has become prevalent due to their high efficiency and compact size. These motors offer improved reliability and reduced maintenance compared to traditional brushed motors. For instance, brushless motors are now standard in many electric oil pumps, providing better performance and longevity.

Modern electric oil pumps are increasingly integrated with vehicle control systems via communication protocols such as CAN (Controller Area Network) and LIN (Local Interconnect Network). This integration allows for real-time monitoring and adjustment of oil pressure and flow, optimizing engine performance and fuel efficiency. Approximately 70% of new electric oil pump models now feature such connectivity, enabling smarter vehicle systems. Variable displacement electric oil pumps are gaining traction for their ability to adjust oil flow based on engine demand. This technology enhances fuel efficiency and reduces emissions by providing the necessary lubrication only when required. These pumps can achieve up to a 20% improvement in fuel economy in hybrid vehicles.

With the rise of electric and hybrid vehicles, effective thermal management has become crucial. Electric oil pumps are now designed to handle higher thermal loads, ensuring optimal performance of electric motors and batteries. Some advanced pumps can operate efficiently at temperatures exceeding 120°C, supporting the thermal requirements of modern electrified powertrains. These technological advancements are driving the evolution of the automotive electric oil pump market, positioning it as a critical component in the development of efficient and sustainable vehicle systems.

Valeo's Strategic Expansion in Electrified Powertrains

In July 2024, Valeo introduced advanced electric oil pumps tailored for the BMW X3 and Audi Q5, enhancing lubrication and cooling in their electrified powertrains. This move underscores Valeo's commitment to supporting the automotive industry's shift towards electrification.

Denso's Innovation in Fuel Delivery Systems

Denso launched a new line of electric oil pumps in 2023, incorporating advanced turbine technology to deliver fuel with minimal pressure pulsation. This innovation ensures quieter operation and improved efficiency, aligning with the industry's demand for enhanced performance and reduced noise levels.

Aisin Seiki's Integration of Control Circuits

In 2024, Aisin Seiki expanded its electric oil pump offerings by integrating control circuits, motors, and pumps into a compact, lightweight design. This integration reduces size and mass while increasing vehicle mounting versatility, catering to the evolving needs of modern automotive designs.

BorgWarner's Development for All-Wheel-Drive Systems

BorgWarner developed a new electric oil pump in 2023 specifically for all-wheel-drive systems. This pump ensures proper lubrication and hydraulic pressure within the coupling mechanism, allowing for effective torque distribution between the front and rear axles, thereby enhancing vehicle performance.

The Automotive Electric Oil Pump Market Report provides an in-depth analysis of the industry's current landscape and future prospects. It encompasses various market segments, including different types of electric oil pumps, such as brushless and brushed designs, highlighting their respective advantages and applications in modern vehicles. The report examines the adoption of these pumps across different vehicle types, from internal combustion engine (ICE) vehicles to electric and hybrid models, emphasizing the shift towards electrification and its impact on lubrication systems. Geographically, the report offers insights into market trends across major regions, including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. It explores regional variations in demand, technological adoption, and regulatory influences shaping the market's growth trajectory.

The report also covers the diverse applications of electric oil pumps, such as engine lubrication, transmission systems, and electric motor cooling, underscoring their critical role in enhancing vehicle performance and efficiency. It highlights the integration of advanced technologies like variable displacement, thermal management, and real-time monitoring, which are driving innovation in the sector. Furthermore, the report identifies emerging market segments and niche applications, offering a forward-looking perspective on potential growth areas. It serves as a valuable resource for industry professionals, providing data-driven insights to inform strategic decision-making and investment planning in the automotive electric oil pump market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 19807.32 Million |

|

Market Revenue in 2032 |

USD 28384.37 Million |

|

CAGR (2025 - 2032) |

4.6% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

BorgWarner, Continental, Denso, Valeo, Aisin Seiki, Bosch, Mahle, Pierburg, Federal-Mogul, Hitachi Automotive Systems |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |