Reports

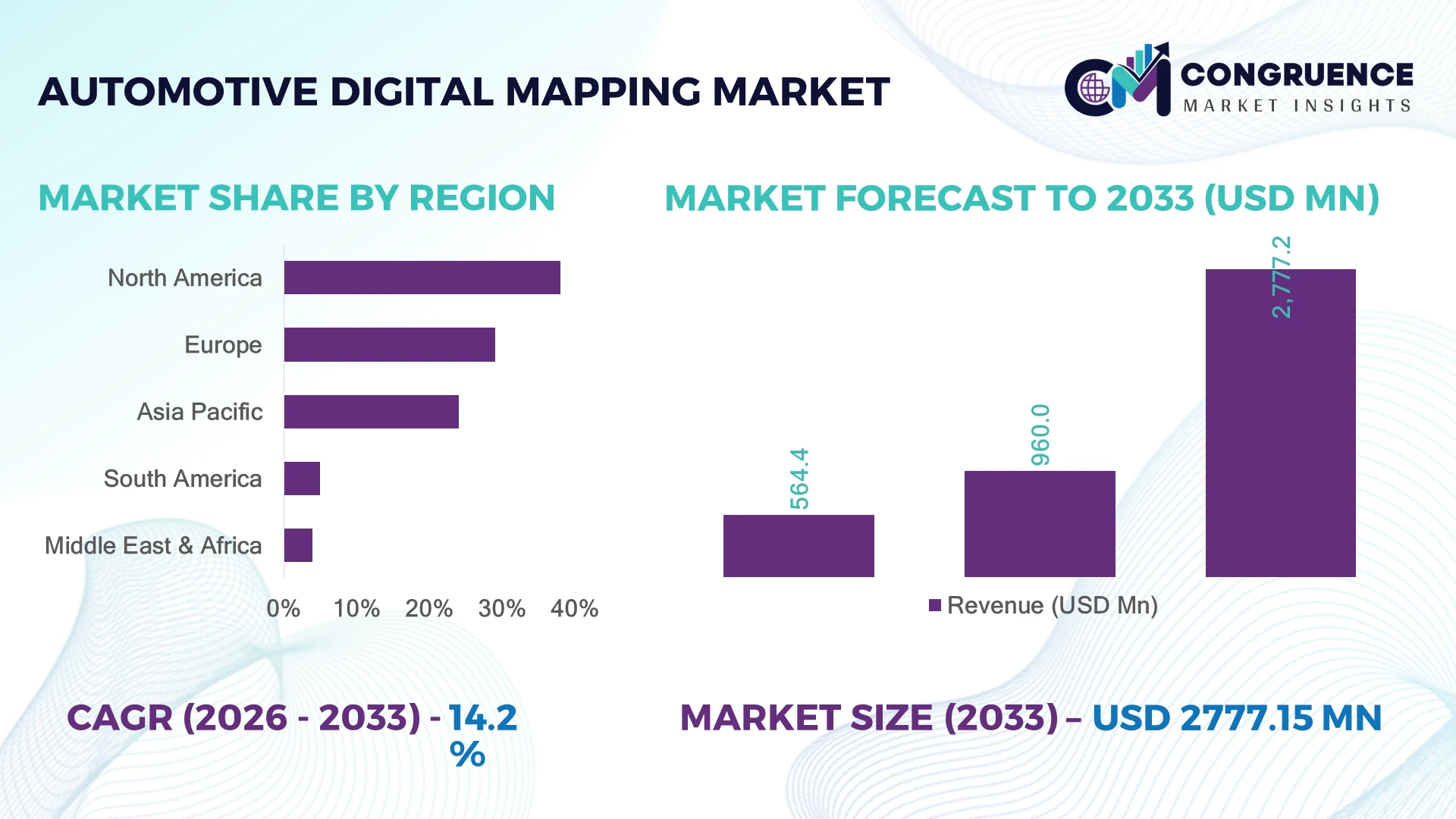

The Global Automotive Digital Mapping Market was valued at USD 960.0 Million in 2025 and is anticipated to reach a value of USD 2,777.2 Million by 2033 expanding at a CAGR of 14.2% between 2026 and 2033. Growth is driven by rapid deployment of ADAS-enabled vehicles, expanding autonomous driving programs, and increasing integration of high-definition mapping with connected mobility ecosystems.

The United States leads the global automotive digital mapping market with approximately 31% market share, supported by more than USD 8 billion in autonomous vehicle and intelligent transportation investments, widespread ADAS deployment, and strong participation from technology and automotive leaders. Compared with Germany, which emphasizes premium automotive engineering and HD map integration, the U.S. benefits from broader real-world autonomous testing under the U.S. Infrastructure Investment and Jobs Act, accelerating nationwide digital road infrastructure modernization.

Strategic investments in scalable, AI-powered mapping platforms and real-time location intelligence will determine long-term competitive leadership across connected mobility ecosystems.

Market Size & Growth: USD 960.0 Million (2025) projected to reach USD 2,777.2 Million by 2033 at 14.2% CAGR, driven by expanding HD mapping for connected and autonomous vehicles.

Top Growth Drivers: ADAS adoption exceeds 48%, connected vehicle penetration reaches 42%, and AI-powered mapping updates improve navigation accuracy by 35%.

Short-Term Forecast: By 2028, real-time map update latency declines by 40%, improving fleet routing efficiency and autonomous driving performance.

Emerging Technologies: AI-generated HD maps, LiDAR mapping, and cloud-based digital twins accelerate high-precision navigation and predictive route optimization.

Regional Leaders: North America (~USD 940 Million), Europe (~USD 720 Million), and Asia-Pacific (~USD 690 Million) lead through smart mobility expansion and vehicle digitalization.

Consumer/End-User Trends: More than 55% of premium vehicle buyers prefer advanced navigation integrated with driver assistance systems.

Pilot/Case Example: In 2024, connected HD mapping pilots improved lane-level navigation accuracy by approximately 30% in urban mobility corridors.

Competitive Landscape: HERE Technologies holds nearly 25% market presence alongside TomTom, Google, Mapbox, and Bosch.

Regulatory & ESG Impact: Intelligent transport initiatives reduce routing inefficiencies by nearly 15% while supporting lower transport emissions across urban networks.

Investment & Funding: More than USD 5 Billion supports AI mapping partnerships, automotive software expansion, and next-generation mobility platforms amid global supply-chain localization.

Innovation & Future Outlook: Edge AI, vehicle-to-everything integration, and continuously updated HD maps strengthen next-generation autonomous mobility strategies.

Automotive Digital Mapping Market demand continues expanding across autonomous mobility, connected vehicles, fleet management, and intelligent transportation infrastructure. AI-enabled HD maps, LiDAR-based road modeling, and cloud-native mapping platforms are improving positioning precision and real-time route intelligence, while map refresh cycles have accelerated by nearly 40%. Increasing smart-city deployment and evolving vehicle safety regulations are reinforcing adoption, setting the foundation for broader strategic market transformation.

Automotive digital mapping has become a strategic capability for automakers, mobility providers, and technology companies seeking competitive differentiation through safer, connected, and software-defined vehicles. Infrastructure modernization, intelligent transportation initiatives, and expanding autonomous vehicle testing are reshaping investment priorities. At the same time, supply-chain restructuring is encouraging regional development of mapping platforms and location data services to improve resilience and reduce dependence on external providers.

Compared with conventional navigation databases, AI-powered HD mapping platforms deliver lane-level accuracy while reducing manual map maintenance costs by approximately 30% through automated data collection and continuous cloud updates. North America remains the largest deployment region because of extensive autonomous driving programs, whereas Asia-Pacific is recording faster implementation through smart-city expansion, 5G connectivity, and intelligent highway development. Over the next two to three years, connected vehicle penetration is expected to exceed 50% across several developed automotive markets, accelerating demand for continuously updated digital maps.

Leading companies are expanding strategic alliances with automotive OEMs, cloud providers, and sensor technology developers to strengthen real-time mapping capabilities. Fleet operators are also deploying dynamic mapping platforms to optimize routing, reduce traffic delays, and improve operational efficiency. Organizations that establish scalable mapping ecosystems, high-quality location intelligence, and seamless software integration will secure stronger competitive positioning as connected and autonomous mobility becomes mainstream.

The rapid integration of advanced driver assistance systems (ADAS) and autonomous driving technologies is fundamentally reshaping automotive digital mapping requirements. More than 48% of newly launched premium vehicles now incorporate advanced navigation linked with lane-level positioning, while HD maps improve autonomous perception accuracy by nearly 35% compared with conventional navigation datasets. The United States continues expanding connected highway infrastructure under national transportation modernization initiatives, enabling large-scale real-world validation of digital mapping platforms. This shift increases demand for continuously updated cloud-based maps capable of supporting dynamic road conditions. In response, automotive OEMs and mapping technology providers are strengthening partnerships, expanding AI-driven map generation, and investing in real-time data ecosystems that shorten update cycles while improving operational reliability and software-defined vehicle capabilities.

Developing and maintaining high-definition automotive maps requires substantial investment in LiDAR surveys, cloud processing, and continuous validation, creating structural cost barriers for large-scale deployment. HD mapping programs typically generate 60–70% more geospatial data than traditional navigation platforms, while maintaining lane-level accuracy can increase operational expenses by approximately 30%. Germany's fragmented road-data standards across mobility ecosystems continue to complicate interoperability between mapping providers and automotive manufacturers. These challenges delay deployment, increase software integration costs, and reduce scalability for smaller suppliers. To mitigate operational risks, companies are localizing data processing, adopting standardized mapping frameworks, establishing long-term cloud infrastructure agreements, and diversifying sensor technologies to improve deployment efficiency while controlling lifecycle costs.

Emerging intelligent mobility ecosystems are creating high-value opportunities beyond traditional in-vehicle navigation. AI-enabled automated mapping workflows reduce manual processing requirements by approximately 40%, while digital twin technologies improve road asset monitoring efficiency by nearly 25%. Japan's investment in smart transportation corridors and connected infrastructure is accelerating adoption of high-definition digital mapping for both passenger and commercial mobility applications. Companies are expanding R&D around edge AI, vehicle-to-everything communication, and predictive location intelligence that supports logistics optimization and autonomous fleet operations. A notable strategic opportunity lies in subscription-based mapping services, allowing continuous software updates and recurring service models that strengthen customer retention while reducing dependence on one-time vehicle platform integration.

Maintaining accurate, real-time digital maps across millions of connected vehicles presents a complex long-term execution challenge. Traffic conditions, construction activity, and temporary road changes can affect nearly 20% of urban road segments annually, while cybersecurity incidents targeting connected mobility platforms have increased by over 25% in recent years. China's rapid expansion of connected vehicle infrastructure requires mapping providers to synchronize enormous volumes of location data without compromising latency or data integrity. Companies must invest in secure cloud architectures, AI-driven validation engines, and standardized over-the-air update frameworks to ensure deployment consistency. Organizations capable of combining scalable infrastructure with resilient cybersecurity and high-frequency data synchronization will sustain stronger competitive advantages as software-defined mobility ecosystems continue expanding.

AI-Driven HD Map Automation – Automotive manufacturers are accelerating AI-enabled map generation to reduce manual processing and improve update frequency. Automated mapping workflows now shorten data validation cycles by nearly 40%, while cloud-based processing increases map refresh efficiency by around 35%. Technology transitions toward software-defined vehicles are encouraging strategic partnerships between mapping providers, OEMs, and cloud companies, allowing continuous deployment of lane-level navigation services with lower operational complexity.

Connected Vehicle Data Expansion – Connected vehicles are becoming continuous data sources for live map updates, with more than 45% of newly produced premium vehicles transmitting telematics data for navigation optimization. Fleet-generated road intelligence has improved incident detection by approximately 30%, helping reduce routing delays. In the United States, intelligent transportation infrastructure programs are accelerating deployment, prompting companies to strengthen edge computing capabilities and expand real-time data processing platforms.

LiDAR Mapping Gains Momentum – LiDAR-equipped mapping vehicles are replacing conventional surveying methods for high-definition road modeling. Survey productivity has improved by nearly 50%, while positional accuracy has increased by approximately 25% for autonomous driving applications. Automotive technology suppliers are expanding sensor partnerships and integrating AI-based point-cloud processing to accelerate digital road infrastructure development while reducing engineering workloads.

Cloud-Native Mapping Ecosystems – Automotive companies are shifting from static navigation databases toward cloud-native mapping platforms supporting over-the-air updates. Continuous software deployment reduces update latency by nearly 40% and improves navigation reliability by around 20%. Growing cybersecurity requirements and digital mobility regulations are encouraging vendors to restructure software architectures, invest in secure cloud infrastructure, and develop subscription-based mapping ecosystems that strengthen long-term customer engagement.

HD Maps represent the leading segment, accounting for nearly 48% of market demand due to their superior lane-level precision, real-time localization, and seamless integration with advanced driver assistance systems and autonomous driving platforms. Automotive OEMs increasingly rely on HD maps to support adaptive cruise control, automated lane changes, and predictive navigation. Their ability to process dynamic road information significantly improves operational safety while reducing localization errors by almost 30%. Meanwhile, 2D Maps continue serving entry-level navigation systems because of lower implementation costs, whereas Satellite Imagery remains strategically important for large-scale geographic validation and route verification. 3D Maps are emerging as the fastest-growing segment as next-generation vehicles require highly detailed environmental visualization. Adoption has increased by approximately 34% among autonomous vehicle development programs, particularly in the United States and Japan. Mapping providers are expanding AI-powered reconstruction capabilities, strengthening LiDAR partnerships, and investing in cloud-native HD mapping platforms to improve scalability. Investment priorities are increasingly shifting toward intelligent map ecosystems capable of supporting software-defined vehicles rather than conventional navigation databases.

Advanced Driver Assistance Systems (ADAS) remain the dominant application because virtually every modern safety platform depends on highly accurate digital maps for positioning, predictive routing, and hazard recognition. Nearly 55% of newly launched premium vehicles now integrate HD mapping with driver assistance features, while navigation-assisted safety functions improve route prediction accuracy by approximately 28%. Logistics Control Systems continue expanding across commercial fleet operations through dynamic route optimization, whereas Other Applications include insurance telematics, intelligent transportation management, and connected mobility services supporting broader digital ecosystems. Autonomous Cars represent the fastest-growing application as manufacturers intensify real-world testing and intelligent mobility deployments. High-definition mapping adoption within autonomous development programs has increased by almost 36%, driven by sensor fusion and AI-powered perception systems. Automotive companies are scaling cloud-based mapping infrastructure, integrating over-the-air updates, and strengthening software partnerships to support continuous vehicle learning. Demand is increasingly shifting toward integrated navigation platforms capable of combining localization, perception, and predictive traffic intelligence into unified mobility solutions.

Passenger Vehicles account for the largest share of automotive digital mapping adoption, representing approximately 72% of total deployment due to rising production of connected, premium, and software-defined vehicles. Increasing consumer demand for intelligent navigation, predictive routing, and integrated safety technologies continues strengthening implementation across electric and conventional vehicle platforms. Real-time mapping capabilities improve navigation efficiency by roughly 22%, while over-the-air software updates reduce maintenance complexity. Manufacturers are differentiating products through embedded AI navigation, cloud connectivity, and subscription-based digital services that enhance long-term customer engagement. Commercial Vehicles are the fastest-growing end-user segment as logistics operators increasingly deploy digital mapping for fleet optimization, route planning, and operational visibility. Fleet operators have reported fuel efficiency improvements approaching 18% through dynamic route optimization and predictive traffic management. Automotive technology providers are developing customized mapping platforms, expanding fleet management partnerships, and integrating predictive analytics with transportation software. Competitive positioning is increasingly centered on scalable enterprise mapping ecosystems capable of supporting connected commercial mobility and intelligent logistics operations.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 16.1% between 2026 and 2033.

North America remains the largest regional market owing to its advanced autonomous vehicle ecosystem, extensive connected vehicle deployment, and mature digital infrastructure. The region contributes approximately 38% of global demand, supported by large-scale investments in intelligent transportation systems, cloud-native mobility platforms, and AI-powered mapping technologies. Automotive OEMs, mapping companies, and cloud service providers continue expanding strategic collaborations to accelerate lane-level mapping and real-time data processing. More than 50% of autonomous vehicle pilot programs globally are concentrated in the United States, strengthening deployment activity and accelerating commercial adoption of HD mapping solutions. Continuous over-the-air software updates and expanding vehicle connectivity are reinforcing operational efficiency while supporting long-term software-defined mobility strategies.

United States Market Outlook: The United States serves as the technological center of the regional market through its strong automotive software ecosystem, advanced cloud infrastructure, and active autonomous vehicle testing environment. More than 35 states permit autonomous vehicle testing under varying regulatory frameworks, creating one of the world's largest real-world mapping datasets. Leading automotive manufacturers, digital mapping companies, and AI developers continue expanding strategic partnerships to improve localization accuracy, sensor fusion, and predictive navigation capabilities while strengthening intelligent transportation infrastructure.

Europe maintains a strong position through premium automotive manufacturing, intelligent mobility investments, and harmonized vehicle safety regulations. The region accounts for nearly 29% of global market activity, with automotive manufacturers increasingly integrating high-definition mapping into advanced driver assistance systems and next-generation vehicle platforms. Digital road infrastructure modernization, connected mobility initiatives, and vehicle software standardization continue driving deployment across multiple countries. Automotive suppliers are strengthening collaborations with mapping technology providers to improve real-time localization while reducing software integration complexity. Regulatory emphasis on vehicle safety and intelligent transport systems further supports deployment consistency throughout the automotive value chain.

Germany Market Outlook: Germany remains Europe's leading automotive digital mapping hub due to its premium vehicle manufacturing base, engineering expertise, and advanced automotive software ecosystem. Nearly 70% of premium vehicle production incorporates sophisticated navigation and driver assistance technologies requiring highly accurate digital mapping. Leading OEMs continue investing in AI-powered mapping, sensor integration, and connected mobility platforms while collaborating with software developers to strengthen autonomous driving capabilities and intelligent transportation infrastructure.

Asia-Pacific is emerging as the fastest-growing regional market due to rapid vehicle production, expanding connected mobility infrastructure, and government-backed smart transportation initiatives. The region represents approximately 24% of current market demand while recording the highest deployment momentum across intelligent transportation networks. Large-scale investments in 5G connectivity, digital highways, and AI-enabled mobility platforms are accelerating adoption of high-definition mapping technologies. Automotive manufacturers are increasing cloud-based navigation integration and expanding software partnerships to support autonomous driving development and connected vehicle ecosystems across high-volume production markets.

China Market Outlook: China has established itself as the region's most influential market through its extensive electric vehicle production, intelligent transportation investment, and digital infrastructure development. Connected vehicle penetration continues rising rapidly, supported by large-scale deployment of smart highways and urban mobility platforms. Domestic technology companies and automotive manufacturers are expanding AI mapping capabilities, cloud infrastructure, and high-definition localization technologies to strengthen autonomous driving competitiveness while supporting nationwide intelligent mobility modernization.

South America is witnessing gradual expansion as commercial fleet modernization, logistics optimization, and connected mobility initiatives gain momentum. The region contributes roughly 5% of global market activity, supported by increasing adoption of digital navigation systems across freight transportation and urban mobility services. Infrastructure limitations continue affecting deployment speed, yet enterprise investment in cloud-based fleet management and intelligent routing solutions is improving operational efficiency. Automotive technology providers are forming strategic partnerships with logistics operators and mobility service companies to strengthen regional implementation while addressing road network variability and digital infrastructure constraints.

Brazil Market Outlook: Brazil represents the largest automotive digital mapping market in South America due to its extensive automotive manufacturing capacity, expanding logistics sector, and growing connected fleet deployments. Commercial transportation operators increasingly implement AI-assisted route optimization and predictive navigation to reduce fuel consumption and delivery times. Vehicle manufacturers and digital mobility providers continue investing in localized mapping databases and cloud-enabled navigation platforms to improve operational performance across the country's diverse transportation network.

The Middle East & Africa market is expanding steadily through smart city investments, intelligent transportation projects, and growing digital infrastructure development. The region accounts for approximately 4% of global demand, supported by government-led modernization initiatives and increasing deployment of connected mobility technologies. Large infrastructure programs are encouraging adoption of cloud-based navigation, digital road management, and AI-driven mapping solutions. Technology providers are expanding regional partnerships while integrating mapping platforms with urban mobility systems to improve transportation planning, operational visibility, and intelligent traffic management across rapidly developing metropolitan areas.

United Arab Emirates Market Outlook: The United Arab Emirates leads regional market development through ambitious smart city strategies, advanced digital infrastructure, and widespread investment in intelligent transportation systems. Dubai and Abu Dhabi continue deploying AI-enabled mobility platforms, connected road infrastructure, and autonomous transportation pilots supporting high-definition digital mapping adoption. Government-backed digital transformation programs and strategic partnerships with global technology companies continue strengthening the country's position as a regional innovation hub for connected and autonomous mobility.

The market is led by HERE Technologies, TomTom, Google, Mapbox, and Esri, while regional geospatial specialists and automotive software providers compete for localized deployments. Global platform leaders compete on HD map precision and software-defined vehicle integration, whereas regional firms emphasize localization, compliance, and cost efficiency. The top five players collectively control approximately 68% of the market. Competition increasingly centers on AI-enabled mapping, cloud delivery, and real-time updates rather than pricing alone. Leading platforms reduce map refresh cycles by nearly 40% and improve lane-level localization accuracy by approximately 30%, creating measurable operational advantages for OEMs. Companies are strengthening positions through long-term automotive partnerships, cloud integration, acquisitions, and vertical integration across mapping, navigation, and location intelligence. The competitive landscape is shifting toward software ecosystems supporting autonomous mobility and connected vehicles, raising barriers through proprietary datasets, AI models, and validation infrastructure. Success increasingly depends on scalable HD mapping, continuous data collection, enterprise partnerships, and seamless integration across intelligent mobility ecosystems.

TomTom

Google Maps Platform

Mapbox

Esri

Garmin Ltd.

Hexagon AB

Trimble Inc.

Genesys International Corporation

Pioneer Corporation

Bosch Mobility Platform and Solutions

Dynamic Map Platform Co., Ltd.

Artificial intelligence, HD mapping, LiDAR, and cloud-native geospatial platforms are redefining automotive digital mapping. AI-based feature extraction reduces manual map generation effort by nearly 40%, while automated validation improves update accuracy by approximately 30%. More than 55% of new connected vehicle programs now integrate cloud-delivered mapping services, enabling continuous over-the-air updates and predictive navigation. These technologies provide faster localization, lower maintenance requirements, and stronger software-defined vehicle capabilities for automotive manufacturers.

Modern HD maps significantly outperform traditional navigation databases by delivering lane-level positioning with nearly 35% greater localization precision and reducing map refresh times by around 45% through automated cloud synchronization. OEMs, autonomous driving developers, and logistics providers benefit most because sensor fusion with cameras, radar, and LiDAR creates highly reliable positioning under dynamic road conditions. Companies investing in edge computing and AI-based digital twins are strengthening competitive differentiation while lowering lifecycle operating costs.

Between 2026 and 2028, vehicle-to-everything communication, generative AI for map maintenance, and crowdsourced real-time road intelligence will become mainstream deployment priorities. Automotive suppliers are expanding strategic technology partnerships to support autonomous mobility, predictive routing, and intelligent transportation infrastructure. Organizations that rapidly adopt scalable AI-powered mapping ecosystems will achieve stronger operational resilience, faster software deployment, and sustained competitive advantage.

January 2025 – HERE Technologies expanded its strategic collaboration with BMW Group to deploy AI-powered lane-level mapping for automated driving. The platform already supports more than 53 million vehicles, strengthening software-defined vehicle capabilities and regulatory compliance. Source: www.here.com

July 2025 – HERE Technologies and Genesys International announced a partnership to develop next-generation in-car navigation for India, combining real-time traffic, ADAS, and hazard alerts. The solution targets improved road safety and connected driving adoption across Indian vehicles.

June 2025 – Bosch Mobility Platform and Solutions partnered with HERE Technologies to integrate precision mapping into its Logistics Operating System, enabling faster deployment of routing and fleet services while improving operational efficiency for enterprise mobility platforms.

January 2026 – HERE Technologies and Hyundai AutoEver expanded their navigation partnership to support Hyundai, Kia, and Genesis software-defined vehicles with continuously updated online maps and real-time location intelligence, strengthening digital cockpit performance across future vehicle platforms.

The report provides comprehensive analysis of the automotive digital mapping ecosystem across three mapping types, four application segments, and two end-user categories, supported by detailed evaluation of North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. It assesses adoption patterns across passenger and commercial vehicles, autonomous mobility, ADAS, logistics systems, and connected transportation while examining AI-enabled HD mapping, LiDAR, cloud-native platforms, digital twins, and real-time location intelligence. Company benchmarking covers more than 10 leading technology and mapping providers.

The study delivers strategic insights into competitive positioning, technology deployment, enterprise partnerships, regional investment priorities, and evolving software-defined vehicle ecosystems between 2026 and 2033. It highlights deployment trends, operational shifts, and emerging opportunities across intelligent transportation infrastructure, helping stakeholders evaluate expansion strategies, product development priorities, partnership opportunities, supply-chain decisions, and long-term investment planning through data-driven market intelligence and forward-looking competitive assessment.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 960.0 Million |

| Market Revenue (2033) | USD 2,777.2 Million |

| CAGR (2026–2033) | 14.2% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | HERE Technologies; TomTom; Google Maps Platform; Mapbox; Esri; Garmin Ltd.; Hexagon AB; Trimble Inc.; Genesys International Corporation; Pioneer Corporation; Bosch Mobility Platform and Solutions; Dynamic Map Platform Co., Ltd. |

| Customization & Pricing | Available on Request (10% Customization Free) |