Reports

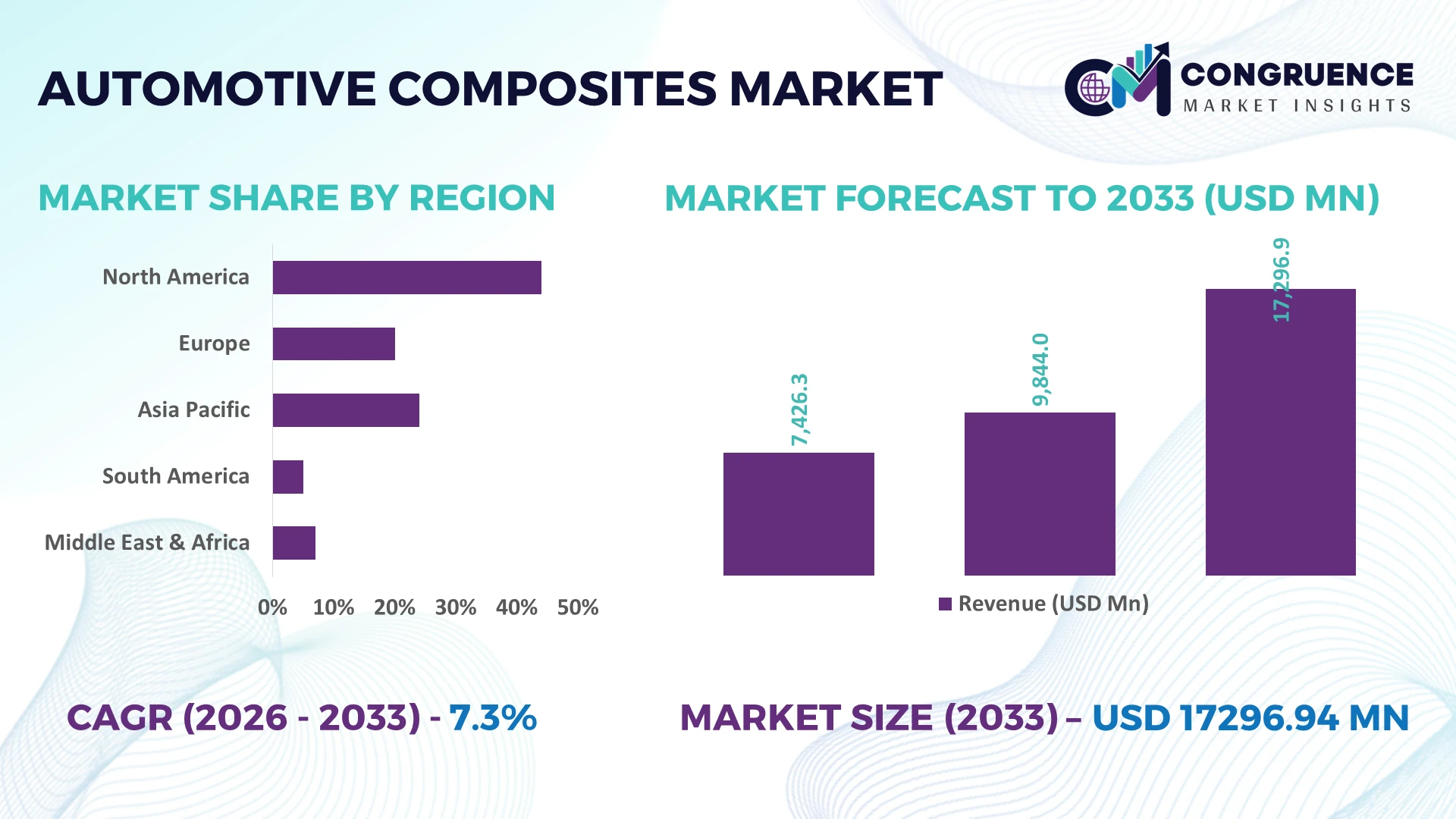

The Global Automotive Composites Market was valued at USD 9844 Million in 2025 and is anticipated to reach a value of USD 17296.94 Million by 2033 expanding at a CAGR of 7.3% between 2026 and 2033. Rising electric vehicle production, stricter vehicle emission standards, and increased adoption of lightweight carbon- and glass-fiber components in structural and semi-structural applications are accelerating automotive composites market expansion across passenger and commercial vehicles.

China dominates the global automotive composites market, contributing approximately 34% of global vehicle production while accounting for over 40% of worldwide EV manufacturing. More than USD 12 billion has been invested in advanced materials and lightweight vehicle manufacturing, strengthening domestic supply chains. Compared with Germany's premium automotive manufacturing base, China's higher production scale and integrated composite processing capabilities provide a competitive advantage amid evolving global trade realignments.

Manufacturers prioritizing localized composite production, automated processing technologies, and resilient raw material sourcing are well positioned to capture long-term opportunities across next-generation vehicle platforms.

Market Size & Growth: Valued at USD 9844 Million in 2025 and projected to reach USD 17296.94 Million by 2033 at a CAGR of 7.3%, driven by lightweight vehicle engineering and rapid electric vehicle production.

Top Growth Drivers: Lightweight vehicle designs improve energy efficiency by over 15%, EV production expands above 20%, and composite component integration increases nearly 18% across advanced vehicle platforms.

Short-Term Forecast: By 2028, automated composite manufacturing is expected to reduce production cycle time by approximately 25% while improving manufacturing consistency and throughput.

Emerging Technologies: AI-enabled quality inspection, automated fiber placement, and recyclable thermoplastic composites are enhancing production precision, sustainability, and manufacturing flexibility.

Regional Leaders: Asia Pacific is projected to exceed USD 8.2 billion, Europe USD 4.5 billion, and North America USD 3.8 billion, supported by EV expansion, sustainability initiatives, and advanced manufacturing investments.

Consumer & End-User Trends: More than 45% of new electric vehicle platforms now incorporate lightweight composite structures to improve battery range, crash performance, and vehicle durability.

Pilot Case Example: In 2026, an automated composite body-panel production program improved manufacturing throughput by 20% while reducing material waste by approximately 18%.

Competitive Landscape: The leading manufacturer holds nearly 14% market share, with Toray Industries, Hexcel, SGL Carbon, Teijin, and Solvay maintaining strong global competitive positions.

Regulatory & ESG Impact: Lightweight vehicle regulations support weight reductions exceeding 10%, while recyclable composite materials help manufacturers meet stricter sustainability and circular economy targets.

Investment & Funding: More than USD 2 billion has been invested in composite manufacturing expansion, strategic partnerships, and regional supply-chain localization following global production shifts.

Innovation & Future Outlook: Advanced thermoplastic composites, digital manufacturing, and closed-loop recycling technologies are reshaping product development while strengthening regional manufacturing resilience.

The Automotive Composites Market continues to gain momentum through expanding electric vehicle manufacturing, commercial transportation, and premium automotive applications requiring lightweight, high-strength materials. Automated thermoplastic molding and recyclable composite technologies are improving manufacturing efficiency, while composite utilization per vehicle has increased by approximately 18%. Ongoing supply-chain localization and evolving sustainability regulations are reinforcing long-term industry transformation, setting the foundation for strategic market evaluation.

Automotive composites have become a strategic differentiator as manufacturers balance vehicle lightweighting, electrification, and stricter sustainability requirements without compromising structural performance. Supply-chain restructuring is encouraging OEMs to localize composite manufacturing and secure long-term fiber material availability, reducing exposure to geopolitical disruptions. The shift toward modular vehicle platforms is also increasing demand for standardized composite components that shorten development cycles and improve production flexibility.

Advanced thermoplastic composites enable production cycle times that are approximately 30% shorter than conventional thermoset systems while supporting up to 15% lower processing costs through automated molding technologies. China continues to lead high-volume deployment through integrated EV manufacturing, whereas Germany focuses on premium composite-intensive vehicles with higher engineering complexity. Over the next two to three years, automated composite processing is expected to exceed 45% adoption across newly commissioned automotive manufacturing lines, improving consistency and factory productivity.

A growing number of manufacturers are deploying composite battery enclosures and lightweight body structures to extend electric vehicle range while reducing assembly complexity. Companies are expanding partnerships with material suppliers, investing in automated fiber placement, and strengthening localized production capabilities. Organizations that integrate advanced composites with digital manufacturing and resilient sourcing strategies will secure stronger competitive positioning and long-term operational advantage.

Automotive manufacturers are expanding composite integration to reduce vehicle weight, improve battery efficiency, and comply with tightening emission regulations. Lightweight composite structures can reduce component weight by up to 50% compared with conventional steel while improving vehicle energy efficiency by approximately 15%. China continues expanding automated composite manufacturing capacity as electric vehicle production grows beyond 20% annually across major domestic producers. These structural shifts are encouraging suppliers to increase investment in carbon- and glass-fiber processing, establish long-term OEM partnerships, and deploy automated manufacturing technologies that improve production consistency while reducing material waste. Companies achieving localized composite production gain stronger supply resilience and faster product commercialization.

Volatility in carbon fiber pricing and dependence on specialized raw material suppliers continue to constrain manufacturing economics. Carbon fiber components remain 30–40% more expensive than conventional metal alternatives, while imported precursor materials account for a significant share of production costs in several manufacturing countries. Periodic logistics disruptions and trade restrictions further increase procurement complexity for global automotive suppliers. In response, manufacturers are diversifying supplier networks, expanding regional production facilities, and increasing recycled composite utilization to stabilize input costs. Businesses capable of strengthening localized sourcing strategies are improving production predictability and protecting long-term operating margins.

Thermoplastic composites are creating new opportunities by enabling faster manufacturing, improved recyclability, and automated large-scale production. Automated processing reduces manufacturing cycle times by approximately 30%, while recyclable thermoplastic systems lower production waste by nearly 20%. Japan and South Korea continue expanding research into high-performance lightweight materials for electric mobility and autonomous vehicle platforms. Companies are increasing investment in automated fiber placement, digital production monitoring, and next-generation recyclable composite formulations. Early adoption of circular manufacturing ecosystems provides competitive differentiation through lower lifecycle costs, improved regulatory compliance, and stronger sustainability performance across future vehicle platforms.

Scaling composite manufacturing for mass-market vehicle production remains a significant operational challenge because advanced material processing requires specialized equipment, skilled labor, and precise quality control. Automated composite production lines require approximately 25% higher capital investment than conventional stamping operations, while quality inspection requirements increase production validation time by nearly 20%. Germany and the United States continue investing in digital manufacturing technologies to improve process repeatability and defect detection. Companies must strengthen workforce capabilities, expand automation, and integrate AI-based inspection systems to achieve consistent production quality while maintaining competitiveness in increasingly complex automotive manufacturing environments.

Advanced Thermoplastic Manufacturing Expansion Automotive manufacturers are replacing conventional thermoset processes with automated thermoplastic molding, reducing production cycle times by nearly 30% while improving component consistency by over 20%. Stricter vehicle efficiency regulations and rising EV production are accelerating deployment. Companies are expanding automated production lines and integrating robotic forming systems to improve throughput, reduce scrap, and strengthen localized manufacturing capabilities.

Localized Composite Supply Networks Supply-chain restructuring is driving OEMs to source composite materials closer to manufacturing hubs, reducing logistics lead times by approximately 25% and lowering inventory requirements by around 15%. China and the United States continue expanding domestic processing capacity to reduce import dependence. Manufacturers are forming long-term supplier partnerships and regional production alliances to improve operational resilience and stabilize raw material availability.

Digital Quality Inspection Adoption AI-enabled inspection and digital manufacturing platforms are increasing defect detection accuracy by over 35% while reducing manual inspection time by nearly 40%. Manufacturers are embedding machine vision and predictive analytics into composite production workflows to improve traceability and minimize rework. This operational shift enables faster product validation while supporting consistent quality across high-volume vehicle manufacturing.

Multi-Material Vehicle Integration Automotive platforms increasingly combine composites with aluminum and high-strength steel, reducing structural weight by approximately 18% while improving crash performance and design flexibility. Battery enclosure development and modular vehicle architectures are accelerating this transition. Companies are expanding engineering collaborations, redesigning production workflows, and investing in hybrid material technologies to optimize manufacturing efficiency and vehicle performance.

Glass Fiber Composites remain the leading segment because they provide an optimal balance of strength, cost efficiency, corrosion resistance, and large-scale manufacturability. They account for an estimated 55% of composite material usage in automotive applications, making them the preferred choice for body structures and semi-structural components. Carbon Fiber Composites represent the fastest-growing segment as premium vehicles and electric vehicle platforms increasingly prioritize weight reduction, with adoption expanding by nearly 18% across next-generation vehicle programs. Manufacturers continue investing in automated processing technologies and localized production to improve affordability and production scale.

Thermoplastic Composites are gaining strategic importance through faster molding cycles and improved recyclability, while Thermoset Composites remain essential for applications requiring high thermal stability and structural durability. Natural Fiber Composites continue expanding within interior applications where sustainable materials and lower component weight support regulatory compliance. Companies are strengthening product portfolios through material innovation, strategic partnerships, and production expansion to address evolving vehicle platform requirements and improve manufacturing flexibility.

Body Panels remain the largest application segment because they maximize vehicle weight reduction while maintaining structural integrity and design flexibility. Composite body panels reduce component weight by up to 50% compared with conventional steel alternatives and continue supporting high-volume passenger vehicle production. Battery Enclosures represent the fastest-growing application as electric vehicle manufacturers prioritize lightweight, impact-resistant structures that improve battery protection and driving range. Companies are increasing automated molding capacity and expanding production lines to meet rising OEM demand.

Interior Components maintain stable adoption through lightweight trim systems and improved cabin sustainability, while Chassis applications continue expanding in premium and performance vehicles requiring enhanced rigidity. Powertrain applications remain comparatively specialized but benefit from increasing thermal-resistant composite solutions. Manufacturers are integrating automated production, digital engineering, and modular component development to improve manufacturing efficiency while supporting evolving vehicle architectures.

Passenger Vehicles remain the dominant end-user segment because of their large production volumes and continuous integration of lightweight materials for efficiency and safety improvements. Composite component utilization has increased by approximately 20% across newly introduced passenger vehicle platforms, reinforcing demand for advanced structural materials. Electric Vehicles represent the fastest-growing end-user segment as battery optimization and extended driving range accelerate composite adoption. Manufacturers are expanding dedicated EV production facilities and strengthening partnerships with advanced material suppliers.

Commercial Vehicles continue increasing composite deployment to improve payload efficiency and reduce operating costs, while Automotive OEMs remain the primary purchasers driving technology adoption through long-term supply agreements. Auto Parts Manufacturers are investing in automated composite fabrication and customized component development to support evolving OEM specifications. Companies are differentiating through localized manufacturing, collaborative engineering, and scalable production capabilities to strengthen long-term competitive positioning.

Asia-Pacific accounted for the largest market share at 47.8% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 8.5% between 2026 and 2033.

Advanced Manufacturing and EV Platform Integration

North America maintains a strong position in the automotive composites market through advanced vehicle manufacturing, established composite material suppliers, and increasing electric vehicle production. The region contributes approximately 24% of global demand, supported by automated manufacturing, lightweight vehicle regulations, and high adoption of carbon- and glass-fiber components. More than 35% of newly commissioned composite production capacity is integrated with robotic manufacturing systems, improving production consistency and reducing processing time. Automotive OEMs continue strengthening supplier partnerships and expanding localized composite processing to improve supply-chain resilience while supporting next-generation vehicle architectures.

United States Market Outlook: The United States leads the regional market through its extensive automotive manufacturing ecosystem, strong electric vehicle investments, and advanced composite material innovation. Composite integration across electric pickup trucks, SUVs, and commercial vehicles continues expanding, while automated manufacturing adoption has increased by approximately 28% across major production facilities. Manufacturers are investing in digital production systems, localized raw material sourcing, and strategic supplier collaborations to improve production efficiency and accelerate lightweight vehicle deployment.

Sustainability-Driven Lightweight Engineering

Europe remains a technology-intensive automotive composites market where strict emission regulations and circular manufacturing initiatives encourage higher composite utilization. The region represents nearly 22% of global market demand, with premium vehicle manufacturers accelerating deployment of recyclable thermoplastic composites and automated production technologies. More than 40% of newly introduced premium vehicle platforms incorporate advanced composite structures to improve energy efficiency and reduce vehicle weight. Companies continue expanding engineering partnerships and strengthening closed-loop manufacturing capabilities to support sustainable automotive production.

Germany Market Outlook: Germany serves as Europe's primary automotive composites hub through its premium vehicle manufacturing base, engineering leadership, and advanced material research capabilities. Composite-intensive production continues expanding across luxury passenger vehicles and electric mobility platforms, with automated composite processing improving manufacturing productivity by approximately 25%. Automotive manufacturers are strengthening collaborations with material developers and technology providers to commercialize next-generation lightweight structures while maintaining high manufacturing precision.

Large-Scale Manufacturing Leadership

Asia-Pacific dominates the global automotive composites market through unmatched vehicle production capacity, expanding electric mobility, and vertically integrated composite supply chains. The region accounts for approximately 47.8% of global market share, supported by large-scale manufacturing facilities and continuous investments in lightweight automotive technologies. Composite utilization across newly developed electric vehicle platforms has increased by nearly 20%, while domestic production capacity continues expanding to strengthen supply security. Manufacturers are scaling automated composite processing and increasing regional partnerships to improve manufacturing flexibility and export competitiveness.

China Market Outlook: China remains the world's largest automotive composites market because of its leadership in electric vehicle manufacturing, advanced composite processing, and localized raw material production. The country contributes more than 40% of global electric vehicle production while continuously expanding automated composite manufacturing facilities. Domestic manufacturers are increasing investments in recyclable composite technologies, integrated supply chains, and intelligent production systems to strengthen international competitiveness and accelerate lightweight vehicle development.

Industrial Modernization Supports Adoption

South America is steadily expanding automotive composite adoption through modernization of vehicle manufacturing and increasing localization of automotive supply chains. The region contributes approximately 4% of global market activity, with commercial vehicles and passenger cars driving material demand. Composite component deployment has increased by nearly 12% across selected manufacturing programs as producers prioritize improved fuel efficiency and durability. Companies are strengthening regional supplier partnerships, modernizing production facilities, and expanding technical capabilities despite infrastructure and logistics constraints that continue influencing manufacturing efficiency.

Brazil Market Outlook: Brazil leads the regional market through its established automotive manufacturing industry and expanding supplier ecosystem. Composite materials are increasingly adopted for commercial vehicles, buses, and passenger vehicle body components, with localized production reducing import dependence. Manufacturers continue investing in production modernization, engineering collaboration, and lightweight component development to improve competitiveness while supporting evolving domestic vehicle manufacturing requirements.

Investment-Led Industrial Transformation

The Middle East & Africa market is advancing through industrial diversification, manufacturing investments, and expanding automotive assembly capabilities. The region contributes approximately 2.5% of global market activity while increasing investment in advanced manufacturing infrastructure and localized automotive production. Composite component utilization has expanded by nearly 15% across selected industrial projects supporting commercial vehicle and specialty automotive manufacturing. Companies are strengthening technology partnerships, developing regional supply capabilities, and investing in modern production infrastructure to reduce import dependency and improve operational efficiency.

Saudi Arabia Market Outlook: Saudi Arabia is emerging as the region's strategic automotive composites market through industrial diversification initiatives, automotive manufacturing investments, and advanced materials development. New industrial programs are encouraging localized vehicle production and composite processing, while manufacturing infrastructure continues expanding to support future mobility initiatives. Companies are prioritizing technology partnerships, workforce development, and integrated supply-chain capabilities to establish a competitive regional automotive manufacturing ecosystem.

Competition in the automotive composites market is led by Toray Industries, Teijin, Hexcel, SGL Carbon, and Solvay, competing against regional composite fabricators, automotive material converters, and specialized Tier-1 suppliers. The top five players collectively control approximately 42% of the global market through advanced material portfolios, long-term OEM relationships, and integrated manufacturing capabilities. Global leaders compete on technology performance and supply security, while regional producers focus on cost efficiency and localized delivery. Automated composite processing lowers production cycle time by nearly 30%, and AI-based quality inspection improves defect detection by over 35%, creating measurable operational advantages. Companies are expanding production facilities, forming strategic partnerships with vehicle manufacturers, and strengthening vertical integration from precursor materials to finished composite components. Competitive momentum is shifting toward recyclable thermoplastic composites and digitally connected manufacturing, while control of carbon fiber supply has become a decisive differentiator. High capital requirements, certification complexity, and advanced engineering expertise remain major entry barriers. Sustained success depends on scalable manufacturing, material innovation, resilient supply chains, and deep collaboration with automotive OEMs.

Toray Industries, Inc.

Teijin Limited

Hexcel Corporation

SGL Carbon SE

Solvay SA

Mitsubishi Chemical Group Corporation

Gurit Holding AG

Owens Corning

BASF SE

SABIC

Covestro AG

Huntsman Corporation

Advanced manufacturing technologies are transforming automotive composite production through automated fiber placement, high-pressure resin transfer molding, and AI-enabled process control. Automated fiber placement improves material utilization by approximately 20% while reducing production time by nearly 30% compared with conventional manual lay-up methods. Around 45% of newly commissioned composite production lines now integrate robotic handling and digital quality monitoring, enabling manufacturers to improve consistency, reduce defects, and support higher-volume vehicle programs.

Emerging technologies are accelerating the adoption of recyclable thermoplastic composites, digital twins, and predictive manufacturing analytics. Thermoplastic processing delivers production cycles nearly 30% faster than traditional thermoset systems while lowering manufacturing waste by approximately 18%. Digital twin technology enables continuous optimization of composite tooling and production workflows, reducing process deviations and supporting faster product validation. Automotive OEMs and advanced material suppliers gain the greatest competitive advantage through integrated digital manufacturing ecosystems.

Between 2026 and 2028, closed-loop composite recycling, AI-driven inspection, and hybrid multi-material engineering will reshape production economics and regulatory compliance. AI-based inspection systems improve defect detection by over 35%, while hybrid composite-metal structures reduce overall vehicle weight by approximately 18% without compromising structural integrity. Companies investing early in automation, intelligent manufacturing platforms, and recyclable material technologies will strengthen operational resilience, shorten product development cycles, and secure long-term competitive differentiation across next-generation vehicle platforms.

October 2025 Toray Industries signed a Strategic Joint Development Agreement with Hyundai Motor Group to co-develop advanced carbon-fiber composite materials and molded components across the mobility value chain. The collaboration spans 100% of the development-to-commercialization process, strengthening lightweight vehicle innovation and accelerating future mobility platforms.

September 2025 Hexcel Corporation expanded its North American advanced composites manufacturing footprint to increase carbon fiber and prepreg production capacity for automotive and electric vehicle applications. The expansion enhances regional supply-chain resilience and supports higher-volume lightweight component manufacturing for OEM customers.

January 2026 SGL Carbon and BMW Group received the JEC Innovation Award for their Natural Fiber Composites project, recognizing lightweight automotive parts developed with flax-fiber prepreg technology. The award-winning solution improves sustainable material adoption while supporting next-generation vehicle component development and lower environmental impact.

March 2026 Hexcel announced next-generation composite solutions at JEC World 2026, introducing rapid-cure prepregs, advanced carbon fibers, and new manufacturing collaborations with multiple industrial partners. Rapid-cure material technology supports higher-rate press molding, enabling faster automotive production while expanding commercialization opportunities for lightweight composite applications.

The report provides a comprehensive assessment of the automotive composites market across major material types, applications, end-users, and key geographic markets. It evaluates Glass Fiber Composites, Carbon Fiber Composites, Natural Fiber Composites, Thermoplastic Composites, and Thermoset Composites while examining adoption across body panels, interior components, chassis, powertrain systems, and battery enclosures. The analysis covers passenger vehicles, commercial vehicles, electric vehicles, automotive OEMs, and auto parts manufacturers, with strategic benchmarking across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa.

The study analyzes technology adoption, manufacturing modernization, supply-chain localization, and competitive positioning supported by operational indicators and deployment trends. It assesses market participation across leading global manufacturers, emerging material innovators, and regional suppliers while highlighting automation, recyclable composites, and digital manufacturing as strategic focus areas. The report supports investment evaluation, expansion planning, product portfolio development, partnership strategies, and long-term competitive decision-making between 2026 and 2033.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 9844 Million |

Market Revenue in 2033 | USD 17296.94 Million |

CAGR (2026 - 2033) | 7.3% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Toray Industries, Inc., Teijin Limited, Hexcel Corporation, SGL Carbon SE, Solvay SA, Mitsubishi Chemical Group Corporation, Gurit Holding AG, Owens Corning, BASF SE, SABIC, Covestro AG, Huntsman Corporation |

Customization & Pricing | Available on Request (10% Customization is Free) |