Reports

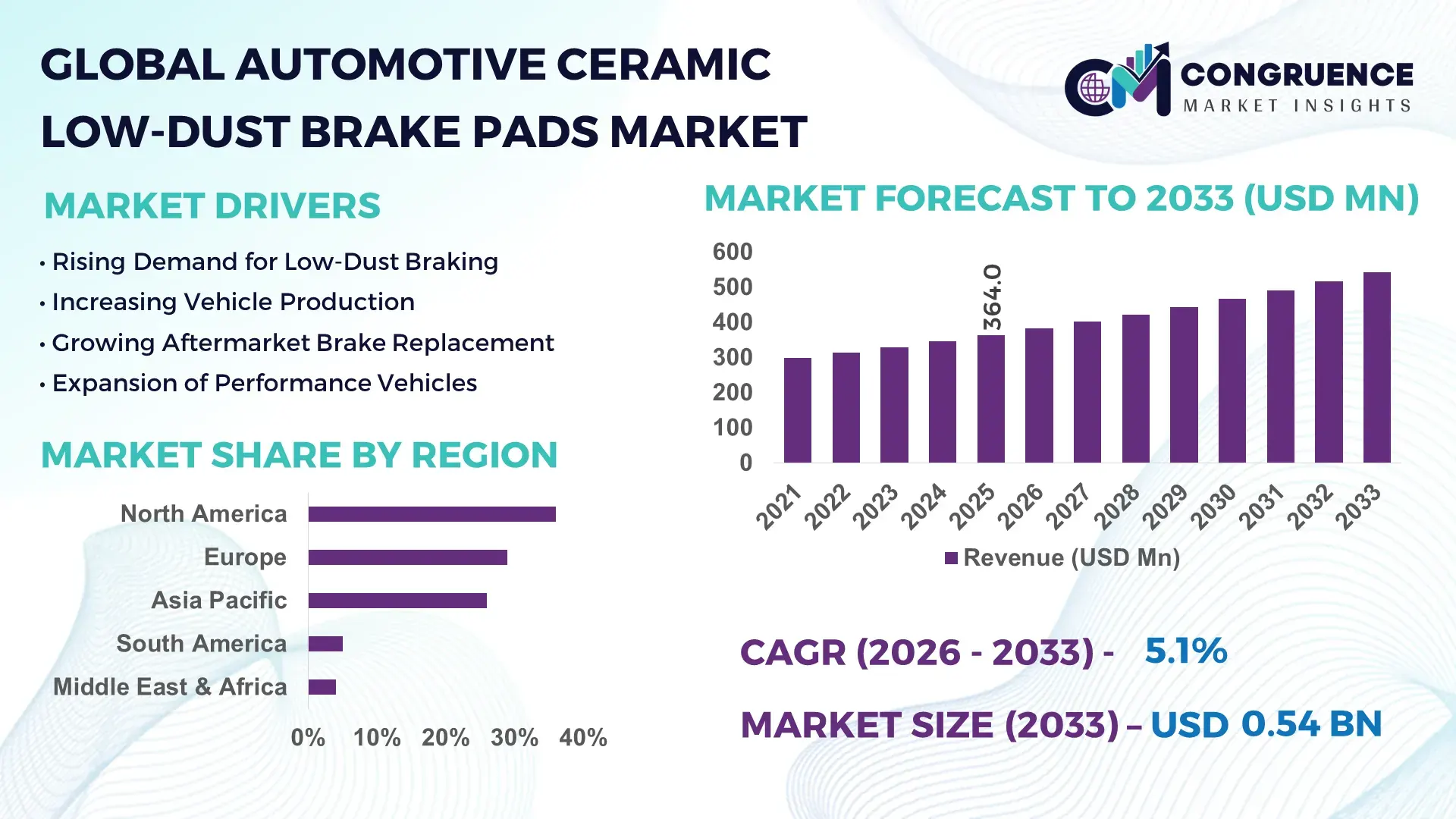

The Global Automotive Ceramic Low-Dust Brake Pads Market was valued at USD 364.0 Million in 2025 and is anticipated to reach a value of USD 541.9 Million by 2033 expanding at a CAGR of 5.1% between 2026 and 2033, according to an analysis by Congruence Market Insights. The growth is primarily attributed to increasing demand for cleaner braking systems that reduce particulate emissions and improve vehicle maintenance efficiency.

The United States plays a significant role in the Automotive Ceramic Low-Dust Brake Pads Market due to its advanced automotive manufacturing ecosystem and large aftermarket service industry. The country produces over 10 million vehicles annually, creating extensive demand for high-performance braking systems. Ceramic brake pad adoption in passenger vehicles has exceeded 45% in premium and mid-segment vehicles, driven by stricter brake particulate emission standards and consumer demand for low-maintenance components. In addition, more than 70% of North American brake pad manufacturing facilities incorporate automated friction material mixing and high-temperature sintering technologies, enabling consistent low-dust formulations. Investments in electric vehicle manufacturing have also increased demand for advanced braking materials, with over 3 million EVs on U.S. roads requiring quieter and longer-lasting ceramic brake pads.

Market Size & Growth: The market was valued at USD 364.0 Million in 2025 and is projected to reach USD 541.9 Million by 2033, expanding at 5.1% CAGR due to rising adoption of low-emission braking components in passenger vehicles and EVs.

Top Growth Drivers: Increasing EV adoption (35% rise in EV registrations), consumer preference for low-maintenance components (40% adoption in premium vehicles), and regulatory pressure to reduce brake particulate emissions (30% tightening in emission norms).

Short-Term Forecast: By 2028, improved ceramic composite friction materials are expected to enhance braking durability by 18% and reduce brake dust emissions by 22%.

Emerging Technologies: Development of nano-ceramic friction materials, AI-based brake wear monitoring systems, and graphene-reinforced ceramic compounds improving braking efficiency and heat resistance.

Regional Leaders: North America projected at USD 198 Million by 2033 driven by aftermarket demand; Europe estimated at USD 172 Million due to strict particulate emission rules; Asia-Pacific expected at USD 141 Million supported by growing vehicle production.

Consumer/End-User Trends: Passenger vehicle owners increasingly prefer ceramic brake pads for quieter braking and minimal wheel dust, with over 38% of vehicle service centers recommending ceramic replacements during routine maintenance.

Pilot or Case Example: In 2024, an automotive supplier introduced ceramic composite brake pads in EV fleets, reducing brake wear by 27% and extending replacement intervals by 30%.

Competitive Landscape: Bosch holds approximately 18% market presence, followed by Akebono Brake Industry, Brembo, Federal-Mogul (DRiV), and ADVICS.

Regulatory & ESG Impact: Governments in Europe and North America have introduced brake particulate emission standards targeting up to 50% reduction in non-exhaust emissions, accelerating adoption of low-dust brake pad materials.

Investment & Funding Patterns: More than USD 1.1 Billion has been invested globally in advanced friction material R&D and automated brake component manufacturing lines over the last five years.

Innovation & Future Outlook: Integration of smart braking sensors, advanced ceramic composites, and predictive maintenance platforms is expected to reshape vehicle safety systems and extend brake pad lifecycle.

The Automotive Ceramic Low-Dust Brake Pads Market is strongly influenced by demand from passenger vehicles (around 52% of applications), followed by light commercial vehicles at approximately 28% and performance vehicles contributing about 20%. Recent product innovations include nano-ceramic friction compounds and heat-resistant binder materials designed to reduce brake dust emissions by over 20%. Environmental regulations limiting particulate emissions from braking systems are accelerating adoption, particularly in Europe and North America. Rising EV production and consumer preference for quieter, longer-lasting braking systems continue to shape the market’s technological roadmap and long-term demand outlook.

The Automotive Ceramic Low-Dust Brake Pads Market is strategically relevant to the global automotive industry as vehicle manufacturers seek braking systems that improve durability, reduce maintenance cycles, and meet stricter environmental standards. Ceramic friction materials are increasingly integrated into braking systems due to their ability to minimize particulate emissions and provide stable braking performance across a wide temperature range. Compared to traditional semi-metallic brake pads, advanced ceramic composite brake pads deliver nearly 25% lower brake dust generation and 18% longer operational life, making them attractive for passenger vehicles, electric vehicles, and high-performance automobiles.

Regional production patterns demonstrate varied adoption trends. Asia-Pacific dominates in production volume, supported by large automotive manufacturing bases in China, Japan, and South Korea. Meanwhile, Europe leads in adoption with nearly 48% of premium vehicle manufacturers integrating ceramic brake pads as part of advanced braking systems designed to meet upcoming particulate emission regulations. These regional dynamics are shaping supply chains and encouraging investments in advanced friction material manufacturing facilities.

Technological innovation is also reshaping the market. Ceramic friction compounds enhanced with graphene and nano-ceramic particles deliver up to 15% higher thermal stability compared to conventional ceramic pads, improving performance under high-temperature braking conditions. By 2028, predictive maintenance platforms integrated with brake wear sensors are expected to reduce unexpected brake system failures by 20%, especially in electric vehicle fleets where regenerative braking changes wear patterns.

Environmental and sustainability commitments are further influencing market strategy. Automotive component manufacturers are committing to up to 30% recyclable friction material content by 2030, aligning with global ESG targets aimed at reducing non-exhaust emissions and manufacturing waste.

A micro-scenario demonstrates the impact of innovation. In 2024, a Japanese automotive component manufacturer deployed automated ceramic friction material processing technology, improving production consistency and reducing brake dust particulate levels by 22% in newly developed brake pads. Such initiatives highlight the growing importance of precision material engineering.

Looking forward, the Automotive Ceramic Low-Dust Brake Pads Market is positioned as a critical pillar supporting vehicle safety, environmental compliance, and sustainable automotive manufacturing as global vehicle fleets transition toward cleaner mobility systems.

The Automotive Ceramic Low-Dust Brake Pads Market is influenced by evolving vehicle safety standards, environmental regulations targeting non-exhaust emissions, and growing consumer demand for low-maintenance braking components. Ceramic brake pads have gained popularity because they produce significantly less dust compared with semi-metallic alternatives, helping maintain vehicle aesthetics and reducing airborne particulate matter generated during braking. Automakers are increasingly integrating ceramic friction materials into braking systems, particularly in passenger vehicles and electric vehicles where noise reduction and durability are key performance metrics. Technological advancements in friction material chemistry, including the use of nano-ceramic additives and high-temperature binders, are improving heat resistance and wear characteristics. In addition, the rapid expansion of global vehicle fleets and aftermarket service networks is increasing replacement demand for premium braking components. Rising adoption of advanced driver-assistance systems and performance braking systems in modern vehicles further supports the use of high-performance ceramic brake pads capable of maintaining consistent braking performance under diverse operating conditions.

Stricter environmental regulations targeting non-exhaust particulate emissions from vehicles are significantly accelerating the adoption of ceramic low-dust brake pads. Brake wear contributes a measurable share of urban particulate pollution, prompting regulatory authorities to introduce emission standards covering braking systems. Ceramic brake pads produce up to 30% less particulate dust compared with conventional semi-metallic pads, making them a preferred solution for vehicle manufacturers seeking compliance with new emission limits. Increasing consumer awareness about cleaner automotive components is also driving demand, particularly in urban regions where vehicle pollution monitoring is intensifying. Passenger vehicle manufacturers have begun integrating ceramic friction materials into mid-range and premium vehicle models, where quiet operation and reduced maintenance are important purchase considerations. Electric vehicles are another major driver because regenerative braking systems alter traditional wear patterns and benefit from the durability and thermal stability of ceramic brake pads. As global EV adoption increases and urban emission policies tighten, demand for ceramic low-dust braking solutions continues to expand across both OEM and aftermarket channels.

Despite their performance advantages, ceramic low-dust brake pads face challenges related to higher manufacturing costs compared with conventional friction materials. Ceramic formulations require advanced raw materials, including high-purity ceramic fibers, specialized bonding resins, and high-temperature sintering processes that increase production complexity. Manufacturing facilities often need precision mixing equipment and controlled heating technologies to maintain consistent friction properties, which raises capital expenditure for brake component producers. Additionally, ceramic brake pads typically undergo longer testing cycles to meet safety certification requirements, further increasing development costs. These factors result in higher product prices, making ceramic brake pads less accessible in cost-sensitive vehicle segments such as entry-level passenger vehicles and commercial fleets focused on minimizing maintenance costs. Supply chain variability in advanced friction materials can also affect production volumes. Consequently, while demand is growing, cost barriers continue to limit rapid penetration in certain markets and vehicle categories where affordability remains a key purchasing criterion.

The rapid expansion of electric vehicle production is creating substantial opportunities for ceramic low-dust brake pad manufacturers. Electric vehicles emphasize quiet operation, thermal efficiency, and long component lifecycles, characteristics that align well with ceramic braking technologies. Regenerative braking systems reduce mechanical braking frequency but require brake pads that remain durable even during intermittent use, making ceramic materials particularly suitable. With global EV fleets surpassing 25 million vehicles worldwide, automotive manufacturers are increasingly integrating advanced braking systems designed to complement regenerative braking. Ceramic pads also contribute to improved vehicle aesthetics by minimizing wheel dust accumulation, an important feature in premium electric vehicle designs. Furthermore, EV manufacturers are experimenting with integrated braking control systems that combine electronic braking with advanced friction materials. As EV production expands across Asia-Pacific, Europe, and North America, opportunities are emerging for suppliers specializing in lightweight ceramic friction materials capable of delivering stable performance under diverse operating conditions.

The rapid evolution of automotive braking technologies presents a significant challenge for ceramic low-dust brake pad manufacturers. Modern vehicles increasingly integrate regenerative braking systems, brake-by-wire technologies, and advanced electronic braking controls that alter traditional friction wear patterns. These technologies reduce mechanical braking frequency, which can affect the expected wear rate and operational lifecycle of brake pads. Manufacturers must redesign ceramic friction formulations to maintain performance even when braking is applied less frequently but under higher load conditions. In addition, integration with electronic stability systems and autonomous driving features requires brake pads capable of responding quickly under automated braking scenarios. Testing and validation requirements for these new braking systems are extensive, requiring manufacturers to invest heavily in simulation tools, high-temperature testing, and vehicle compatibility studies. Meeting these technical requirements while maintaining cost efficiency remains a complex challenge for suppliers operating in the automotive braking component industry.

Increasing Adoption in Electric and Hybrid Vehicles: Electric and hybrid vehicles are increasingly integrating ceramic low-dust brake pads to support quieter operation and longer component lifespan. In 2025, approximately 42% of premium electric vehicles were equipped with ceramic friction brake pads to minimize brake noise and particulate emissions. EV braking systems experience different wear patterns due to regenerative braking, prompting manufacturers to adopt ceramic pads capable of maintaining performance after extended idle periods. Automotive testing programs have demonstrated up to 18% longer service intervals for ceramic brake pads in EV applications compared with traditional materials.

Development of Advanced Nano-Ceramic Friction Materials: Brake component manufacturers are introducing nano-ceramic friction compounds designed to improve heat dissipation and durability. Laboratory testing indicates that nano-ceramic materials can withstand braking temperatures exceeding 650°C, improving thermal stability by 15% compared with conventional ceramic formulations. These innovations also reduce microscopic particulate generation, lowering brake dust output by approximately 20% during repeated high-speed braking cycles.

Expansion of Automated Brake Pad Manufacturing Facilities: Automotive suppliers are investing in automated friction material mixing and precision pressing technologies. Automated production lines can improve consistency in ceramic pad formulations by up to 25%, reducing variability in braking performance. Several new brake component plants in Asia-Pacific and Europe have incorporated automated sintering systems capable of producing over 3 million ceramic brake pads annually, supporting growing demand from OEM vehicle manufacturers and the global aftermarket sector.

Growing Aftermarket Replacement Demand: The global automotive aftermarket is increasingly promoting ceramic brake pads as premium replacement components due to their durability and cleaner operation. Surveys among vehicle service centers indicate that nearly 37% of brake pad replacements in mid-range passenger vehicles now involve ceramic pads, compared with less than 25% five years ago. Improved consumer awareness of brake dust reduction and wheel cleanliness has also influenced adoption, especially among owners of luxury and performance vehicles.

The Automotive Ceramic Low-Dust Brake Pads Market is segmented based on type, application, and end-user, reflecting diverse automotive braking requirements and evolving vehicle technologies. Product types vary primarily by friction material composition, which influences braking performance, durability, and particulate emission levels. Applications are largely associated with different vehicle categories, including passenger vehicles and commercial transportation fleets. End-user segments focus on the channels through which brake pads are adopted, including original equipment manufacturers and the global automotive aftermarket. Increasing vehicle production, rising replacement demand, and regulatory pressure to reduce brake particulate emissions are shaping the segmentation landscape. Technological developments such as advanced ceramic composites and heat-resistant friction materials are influencing adoption patterns across segments. Additionally, regional automotive manufacturing hubs and aftermarket service networks play a major role in determining segment demand distribution.

The Automotive Ceramic Low-Dust Brake Pads Market includes standard ceramic brake pads, performance ceramic brake pads, and hybrid ceramic composite brake pads. Standard ceramic brake pads currently lead the market with approximately 46% adoption, primarily due to their balance between durability, reduced brake dust generation, and compatibility with a wide range of passenger vehicles. These brake pads are widely used in mid-range and premium vehicles where quiet braking and wheel cleanliness are valued by consumers. Performance ceramic brake pads account for about 32% adoption, particularly in high-performance and luxury vehicles that require enhanced heat resistance and consistent braking under high-speed conditions. Hybrid ceramic composite brake pads represent the fastest-growing type, expanding at nearly 6.3% CAGR, driven by innovations combining ceramic fibers with metallic or carbon additives that improve friction stability and extend component lifespan. The remaining niche variants, including specialized ceramic pads designed for heavy-duty braking systems, collectively contribute around 22% of total demand, often used in performance vehicles and specialized automotive applications.

• In 2025, a major automotive testing institute evaluated ceramic brake pads across multiple passenger vehicles and found that advanced ceramic composite pads reduced brake dust accumulation on wheels by nearly 24% compared with semi-metallic brake pads.

Applications of Automotive Ceramic Low-Dust Brake Pads are categorized into passenger vehicles, light commercial vehicles, and performance vehicles. Passenger vehicles dominate this segment with approximately 58% adoption, as ceramic brake pads are widely integrated into sedans, SUVs, and premium electric vehicles due to their quiet operation and minimal dust production. Light commercial vehicles account for about 24% adoption, mainly in delivery fleets and utility vehicles where durability and reduced maintenance downtime are key considerations. However, the performance vehicle segment is growing fastest at nearly 6.8% CAGR, supported by demand for high-temperature braking stability and precision braking response in sports cars and luxury vehicles. The remaining 18% includes niche applications such as specialized braking systems used in high-performance automotive racing and premium aftermarket upgrades. Consumer adoption data indicates that over 41% of premium vehicle owners prefer ceramic brake pads due to reduced wheel dust and longer service intervals. Additionally, surveys of automotive service centers show that nearly 35% of brake pad replacements in urban passenger vehicles now involve ceramic materials.

• In 2024, a large automotive testing program evaluating braking systems in electric vehicles reported that ceramic brake pads improved braking consistency during repeated high-speed stops across multiple EV models.

End-user segments in the Automotive Ceramic Low-Dust Brake Pads Market include original equipment manufacturers (OEMs), automotive aftermarket service providers, and performance vehicle manufacturers. OEMs represent the leading end-user group with approximately 49% adoption, as automakers increasingly integrate ceramic brake pads into new vehicle models to meet consumer expectations for quieter braking and cleaner wheel surfaces. Automotive aftermarket service providers account for about 34% of the market, supported by rising replacement demand as vehicle fleets age and consumers upgrade braking components during routine maintenance. The performance vehicle manufacturer segment is expanding fastest at nearly 6.5% CAGR, driven by growing production of high-performance sports cars and luxury electric vehicles requiring advanced friction materials capable of handling high braking temperatures. Other niche end-users, including specialized automotive modification workshops and fleet operators, contribute the remaining 17% of demand. Industry adoption statistics indicate that over 36% of global automotive service centers recommend ceramic brake pads as premium replacements due to durability and reduced brake dust. Additionally, nearly 40% of luxury vehicle owners report choosing ceramic brake pads during brake system upgrades.

• In 2025, a global automotive maintenance survey reported that large vehicle service networks adopted ceramic brake pads in over 30% of their premium brake replacement programs to improve customer satisfaction and reduce brake dust complaints.

North America accounted for the largest market share at 36% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.2% between 2026 and 2033.

North America’s leadership is supported by its mature automotive manufacturing ecosystem, strong aftermarket demand, and early adoption of advanced friction materials. The region hosts more than 120 brake component manufacturing facilities, with the United States producing over 10 million vehicles annually, which generates strong demand for high-performance braking systems. Europe follows with approximately 29% share, supported by stringent particulate emission regulations that target non-exhaust vehicle emissions. Asia-Pacific represents about 26% of global demand, driven by high vehicle production volumes exceeding 55 million vehicles annually across China, Japan, and India. South America accounts for roughly 5%, largely concentrated in Brazil and Argentina where vehicle assembly plants exceed 60 facilities. The Middle East & Africa contribute close to 4%, with increasing adoption in high-end vehicles and fleet upgrades. Regional demand patterns are influenced by vehicle ownership rates, regulatory frameworks, and expansion of automotive aftermarket service networks.

North America holds approximately 36% of the global Automotive Ceramic Low-Dust Brake Pads Market, supported by high vehicle ownership levels and advanced automotive manufacturing capacity. The United States and Canada collectively produce more than 11 million vehicles annually, creating strong demand for high-performance braking systems. Passenger vehicles account for nearly 63% of brake pad installations in the region, while light commercial vehicles contribute around 27%. Environmental regulations targeting non-exhaust particulate emissions have encouraged adoption of low-dust friction materials in new vehicle models and aftermarket replacements. Technological innovation is also a major driver, with manufacturers integrating automated friction material mixing systems and precision sintering technologies that improve brake pad durability and reduce particulate output. A regional example includes Akebono Brake Industry, which operates advanced manufacturing facilities in the United States and produces millions of ceramic brake pads annually for OEM and aftermarket supply chains. Consumer behavior in this region shows a strong preference for premium replacement components, with over 40% of automotive service centers recommending ceramic brake pads due to their reduced noise and lower dust generation.

Europe represents approximately 29% of the Automotive Ceramic Low-Dust Brake Pads Market, driven by strict environmental regulations and strong automotive engineering capabilities. Key markets include Germany, the United Kingdom, France, and Italy, which collectively produce more than 15 million vehicles annually. European regulatory frameworks addressing non-exhaust vehicle emissions have significantly accelerated the adoption of low-dust brake pads. Policies aimed at reducing particulate emissions encourage automakers to incorporate advanced ceramic friction materials into braking systems. European automotive manufacturers are also integrating advanced brake control systems and electronic braking technologies that work effectively with ceramic friction materials. A regional industry example includes Brembo, headquartered in Italy, which has expanded production of advanced ceramic braking solutions and high-performance friction materials for both premium passenger vehicles and motorsports applications. Consumer behavior across Europe reflects strong sustainability awareness, with vehicle owners prioritizing components that reduce environmental impact and improve long-term vehicle efficiency.

Asia-Pacific ranks as the largest automotive manufacturing hub globally, producing over 55 million vehicles annually across China, Japan, South Korea, and India. The region accounts for roughly 26% of the Automotive Ceramic Low-Dust Brake Pads Market and continues to expand rapidly due to increasing vehicle ownership and growing demand for advanced braking systems. China remains the largest consumer with more than 25 million vehicles produced annually, followed by Japan with approximately 8 million vehicles and India with nearly 6 million vehicles produced each year. Automotive component manufacturing clusters across these countries support large-scale brake pad production and innovation. Technology hubs in Japan and South Korea are developing high-temperature ceramic friction materials and automated brake component manufacturing processes. A notable regional participant, ADVICS, produces advanced braking components and supplies ceramic brake pads to several global vehicle manufacturers. Consumer adoption patterns across Asia-Pacific show increasing preference for durable and low-maintenance components, particularly in urban markets where vehicle density and service frequency are high.

South America represents about 5% of the Automotive Ceramic Low-Dust Brake Pads Market, with demand concentrated primarily in Brazil and Argentina. Brazil accounts for more than 70% of the region’s vehicle production, operating over 30 automotive assembly plants and producing approximately 2.3 million vehicles annually. Argentina contributes another 450,000 vehicles per year, creating a growing need for durable braking components across passenger and commercial vehicle fleets. Infrastructure expansion and logistics development are increasing the number of commercial vehicles operating across long-distance routes, which drives demand for longer-lasting braking systems. Trade agreements and regional manufacturing incentives have encouraged international brake component manufacturers to establish production facilities within Brazil’s automotive clusters. Regional consumer behavior indicates increasing interest in premium aftermarket brake components, particularly among fleet operators seeking reduced maintenance frequency and improved braking reliability.

The Middle East & Africa region accounts for approximately 4% of the Automotive Ceramic Low-Dust Brake Pads Market, supported by rising vehicle imports and expanding transportation infrastructure. Countries such as the United Arab Emirates, Saudi Arabia, and South Africa are among the primary automotive markets within the region. The UAE alone imports over 300,000 vehicles annually, creating steady demand for aftermarket automotive components including brake pads. Infrastructure development projects and growing logistics networks across the Gulf Cooperation Council countries have increased the number of commercial vehicles in operation, which contributes to brake pad replacement demand. Automotive modernization initiatives and trade partnerships have encouraged international automotive suppliers to expand distribution networks within the region. Consumer behavior reflects strong demand for durable automotive components capable of performing under extreme temperature conditions, particularly in desert climates where braking systems experience higher thermal loads.

United States – 28% Market Share: Strong automotive production exceeding 10 million vehicles annually and a mature aftermarket ecosystem drive high demand for advanced braking components.

China – 24% Market Share: Massive vehicle manufacturing output above 25 million vehicles per year and rapid electric vehicle adoption support large-scale demand for ceramic braking materials.

The Automotive Ceramic Low-Dust Brake Pads Market features a moderately fragmented competitive landscape, with more than 60 global and regional manufacturers actively producing ceramic friction materials and brake pad systems. The top five companies collectively account for approximately 42% of the global market, while numerous regional suppliers compete within the aftermarket segment. Competition is largely driven by product performance, durability, noise reduction, and environmental compliance.

Major automotive component manufacturers are investing heavily in advanced friction material research and automated production technologies to improve product consistency and heat resistance. Several companies operate manufacturing facilities capable of producing over 5 million ceramic brake pads annually, supplying both original equipment manufacturers and aftermarket service networks. Strategic collaborations between brake component producers and automotive manufacturers are increasing, particularly for electric vehicle platforms that require braking systems optimized for regenerative braking patterns.

Product innovation also plays a central role in competitive differentiation. Manufacturers are developing nano-ceramic friction compounds, graphene-reinforced materials, and advanced heat-resistant binders to improve braking stability and reduce particulate emissions. Additionally, global suppliers are expanding their manufacturing footprints across Asia-Pacific and North America to support rising vehicle production and reduce supply chain risks. Competitive strategies increasingly focus on sustainability initiatives, including friction materials designed to reduce brake dust emissions by more than 20% while extending brake pad service intervals.

Robert Bosch GmbH

Akebono Brake Industry Co., Ltd.

ADVICS Co., Ltd.

Nisshinbo Holdings Inc.

TMD Friction Holdings GmbH

Honeywell International Inc.

MAT Holdings Inc.

Hawk Performance

EBC Brakes

Sangsin Brake Co., Ltd.

Fras-le S.A.

Winhere Auto-Part Manufacturing Co., Ltd.

Remsa S.A.

Power Stop LLC

Technological advancements in friction materials and braking system integration are significantly shaping the Automotive Ceramic Low-Dust Brake Pads Market. Ceramic brake pads are engineered using advanced composite formulations that combine ceramic fibers, copper substitutes, fillers, and specialized resins designed to maintain stable friction characteristics under high temperature conditions. Modern ceramic friction compounds can tolerate braking temperatures exceeding 600°C, allowing consistent braking performance during repeated high-speed stops.

Manufacturers are increasingly introducing nano-ceramic and graphene-enhanced friction materials that improve heat dissipation and wear resistance. These advanced formulations reduce particulate emissions by approximately 20–30% compared with conventional semi-metallic brake pads. The development of copper-free brake pads is another major technological milestone, particularly in markets where environmental regulations restrict copper content in friction materials.

Automated production technologies are also transforming brake pad manufacturing. Modern production lines integrate robotic mixing systems, automated pressing equipment, and high-temperature sintering furnaces capable of producing millions of brake pads annually with consistent friction properties. These automated systems can reduce manufacturing variability by nearly 25%, improving product reliability and safety.

Another emerging technological trend involves the integration of smart brake wear sensors and digital vehicle diagnostics. These systems monitor brake pad thickness and temperature in real time, enabling predictive maintenance and reducing unexpected brake failures. With vehicle electrification expanding rapidly, braking technologies are evolving to complement regenerative braking systems. Ceramic friction materials provide stable braking performance even after long periods of inactivity, which is essential for electric vehicles that rely heavily on regenerative braking.

Research efforts are also focusing on lightweight ceramic composites that reduce component weight while maintaining structural integrity. Lighter braking components can improve vehicle efficiency and reduce unsprung mass, contributing to better vehicle handling and energy efficiency.

• In November 2025, Brembo unveiled its XTRA Ceramic Severe Duty Brake Pads at the AAPEX automotive aftermarket event. The new ceramic pads demonstrated 18% shorter stopping distances, 10% better fade resistance, 33% lower noise levels, and 13% improved wear performance during testing, targeting pickup trucks, SUVs, and commercial fleets. Source: www.aapexshow.com

• In September 2024, Brembo showcased an expanded range of aftermarket braking solutions at Automechanika Frankfurt, including its Xtra Ceramic pad line and copper-free friction materials designed to reduce environmental impact while improving braking performance and durability for passenger vehicles.

• In October 2025, Akebono Brake Corporation expanded its ProACT® and EURO® ultra-premium ceramic brake pad lines by introducing seven new part numbers, increasing product coverage for more than 2 million additional vehicles including Audi, Lexus, Nissan, Mercedes-Benz, and Toyota models.

• In November 2024, Akebono Brake Corporation announced that its EURO® Ultra-Premium Ceramic Brake Pads (EUR1867) received the Import Vehicle Community (IVC) Award for Best Overall Aftermarket Product, recognizing the product’s performance, durability, and advanced ceramic friction technology for European vehicle applications.

The Automotive Ceramic Low-Dust Brake Pads Market Report provides a comprehensive analysis of the global industry landscape, focusing on advanced braking technologies designed to reduce particulate emissions and improve braking performance. The report evaluates key market segments including product types, vehicle applications, and end-user channels, providing detailed insights into the adoption of ceramic friction materials across passenger vehicles, light commercial vehicles, and performance vehicles.

Geographically, the report covers five major regions—North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, analyzing regional production capacity, vehicle manufacturing volumes, and consumer adoption patterns. The analysis highlights the influence of automotive manufacturing clusters, regulatory frameworks targeting non-exhaust emissions, and the expansion of global automotive aftermarket service networks.

The report also examines emerging technological innovations such as nano-ceramic friction compounds, graphene-reinforced brake materials, automated brake pad manufacturing systems, and smart brake wear monitoring technologies. These innovations are influencing product development strategies among brake component manufacturers and improving braking efficiency across modern vehicle platforms.

Additionally, the report explores the role of electric vehicle adoption, advanced driver-assistance systems, and regenerative braking technologies in shaping the future demand for ceramic braking materials. The scope includes evaluation of supply chain dynamics, manufacturing trends, and product innovation strategies among leading brake component producers.

Industry stakeholders including automotive manufacturers, brake component suppliers, and aftermarket distributors can use this report to assess market opportunities, evaluate competitive positioning, and identify emerging technology trends shaping the global Automotive Ceramic Low-Dust Brake Pads Market.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 364.0 Million |

| Market Revenue (2033) | USD 541.9 Million |

| CAGR (2026–2033) | 5.1% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Brembo S.p.A.; Robert Bosch GmbH; Akebono Brake Industry Co., Ltd.; ADVICS Co., Ltd.; Nisshinbo Holdings Inc.; TMD Friction Holdings GmbH; Honeywell International Inc.; MAT Holdings Inc.; Hawk Performance; EBC Brakes; Sangsin Brake Co., Ltd.; Fras-le S.A.; Winhere Auto-Part Manufacturing Co., Ltd.; Remsa S.A.; Power Stop LLC |

| Customization & Pricing | Available on Request (10% Customization Free) |