Reports

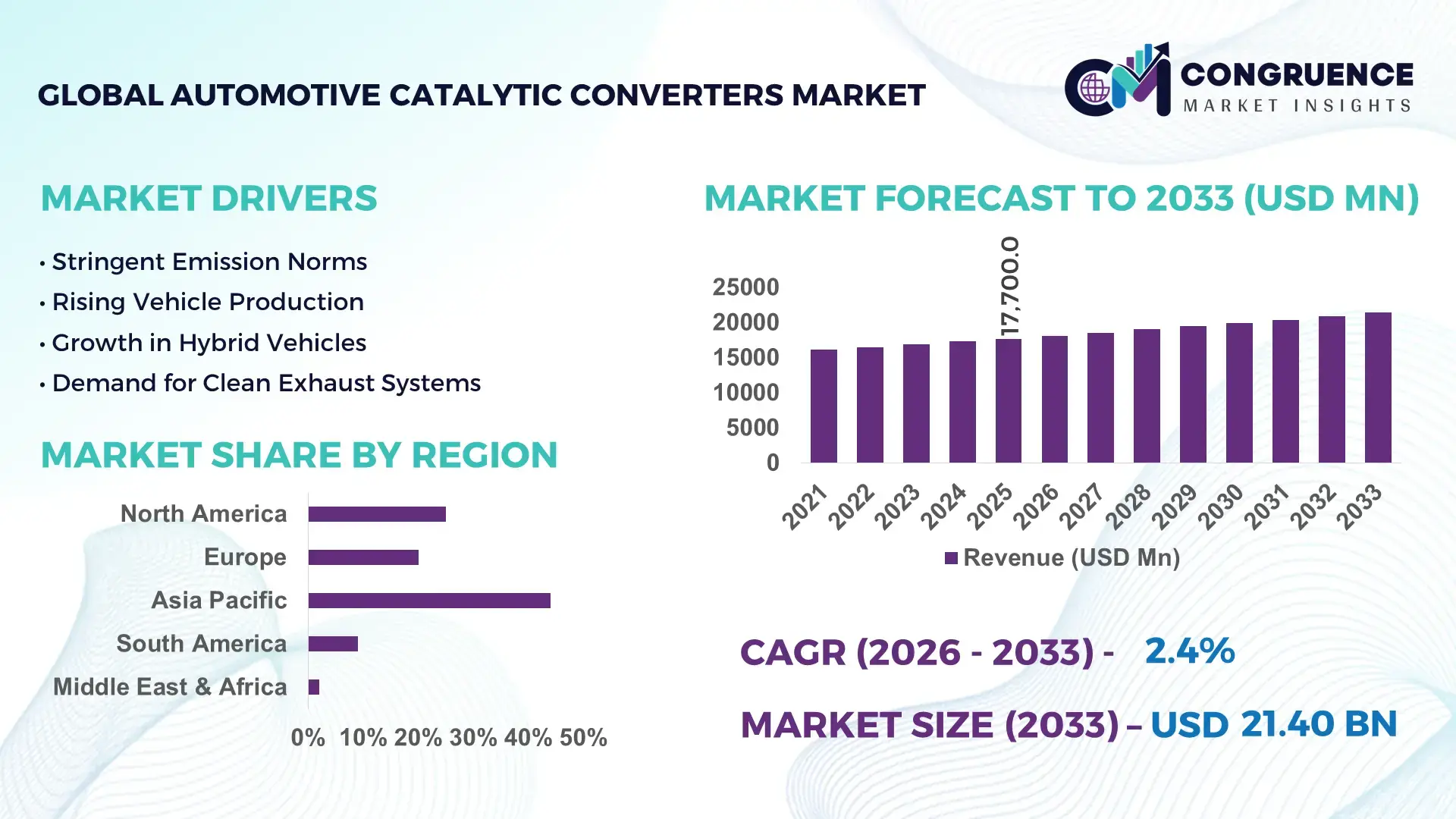

The Global Automotive Catalytic Converters Market was valued at USD 17700 Million in 2025 and is anticipated to reach a value of USD 21397.98 Million by 2033 expanding at a CAGR of 2.4% between 2026 and 2033.

Strengthening emission compliance frameworks across major automotive economies, particularly Euro 7 alignment and China VI enforcement, is accelerating adoption of high-efficiency catalytic systems with improved conversion performance and reduced precious metal loading costs by nearly 9–12%. At the same time, supply-side volatility in platinum group metals due to geopolitical tightening in South Africa and trade restrictions affecting global refining capacity is reshaping procurement strategies and encouraging recycling-led sourcing models.

China dominates the global landscape with nearly 38% market share, supported by large-scale automotive production clusters in Guangdong and Shanghai, alongside annual investments exceeding USD 4.5 billion in emissions control technologies. The country’s hybrid vehicle penetration is driving sustained catalytic converter demand, with high-cell-density ceramic substrates improving emission conversion efficiency by 10–15% compared to conventional designs. In contrast, Europe maintains stronger regulatory-driven adoption intensity, while North America leads in advanced aftermarket replacement cycles, creating a clear technology-performance gap of nearly 8% between premium and standard systems. This divergence highlights a shifting competitive balance across regions.

Strategically, manufacturers are prioritizing localized supply chains and material efficiency innovation to reduce dependency risks while aligning with tightening global emission mandates.

Market Size & Growth: USD 17700M (2025) to USD 21397.98M by 2033, driven by emission compliance tightening and hybrid vehicle expansion.

Top Growth Drivers: emission norms 35%, hybrid adoption 28%, PGM recycling 22% accelerating global demand.

Short-Term Forecast: by 2027, production cost reduction 10% and efficiency improvement 12% through material optimization.

Emerging Technologies: AI-based catalyst design, nano-coating systems, and advanced ceramic substrates improving performance by 15%.

Regional Leaders: China USD 6700M, Europe USD 5200M, North America USD 4100M supported by rising hybrid penetration.

Consumer/End-User Trends: 62% OEMs prioritizing high-durability catalytic systems for hybrid and low-emission vehicle platforms.

Pilot/Case Example: 2026 OEM deployment achieved 14% emission reduction using palladium-optimized catalyst structures.

Competitive Landscape: leading player holds ~18% share, with BASF, Johnson Matthey, and Umicore shaping global supply dynamics.

Regulatory & ESG Impact: tightening emission policies improved compliance efficiency by 20% across major automotive markets.

Investment & Funding: USD 3.2 billion allocated to catalyst recycling, PGM recovery, and capacity expansion initiatives.

Innovation & Future Outlook: shift toward low-PGM formulations and hybrid-compatible catalyst systems driving next-gen transformation.

Global demand for automotive catalytic converters is primarily driven by passenger vehicles contributing nearly 58% of usage, followed by commercial fleets at 27% and aftermarket replacement at 15%. Technological upgrades such as high-surface-area ceramic substrates and palladium-lean formulations are improving emission conversion efficiency by around 12–14%, while Europe and Asia-Pacific collectively account for over 70% of total consumption. Regulatory tightening in emissions standards and supply constraints in platinum group metals are pushing manufacturers toward recycling-based sourcing and localized production. With hybrid vehicle penetration rising by 18% across major markets, the sector is shifting toward cost-efficient, high-performance catalyst systems, setting the foundation for sustained technological and regional restructuring ahead.

The automotive catalytic converters market has shifted from a compliance-driven component segment into a strategic control point for emissions performance, material sourcing, and regulatory alignment. Investors are increasingly prioritizing this space as tightening global emission frameworks and hybrid vehicle penetration are reshaping competitive advantage across automotive supply chains. A key structural pressure is emerging from platinum group metal volatility, where global supply concentration in South Africa and Russia is forcing procurement realignment across OEMs.

From a technology standpoint, solid-phase nano-catalyst systems improve conversion efficiency by 13% while reducing material costs by 9% compared to conventional ceramic-based catalytic substrates. This shift is redefining cost-performance economics in mass automotive production. China continues to lead in volume with nearly 38% share, while Europe leads in regulatory innovation and next-gen catalyst adoption with 16% faster deployment of low-PGM systems. Over the next 2–3 years, emission conversion efficiency is projected to improve by nearly 11%, supported by hybrid vehicle expansion and stricter emission caps. ESG compliance is also emerging as a competitive advantage, reducing lifecycle emissions costs by up to 8% and improving regulatory access in premium automotive segments.

A real-world 2026 OEM integration of palladium-lean catalyst technology achieved a 15% reduction in NOx emissions while lowering production input costs by 10%. In response, major manufacturers are accelerating investments in localized refining ecosystems, strategic recycling infrastructure, and long-term metal procurement contracts. This market is increasingly becoming a battleground for technological leadership and supply chain control, where early positioning directly determines long-term profitability and regulatory resilience.

The primary growth engine of the automotive catalytic converters market is the rapid tightening of global emission regulations combined with accelerating hybrid vehicle penetration. Euro 7 standards and China VI frameworks are pushing OEMs to achieve up to 25% lower NOx emissions, directly increasing demand for high-efficiency catalytic systems. Hybrid vehicle production has expanded by nearly 18%, significantly raising converter utilization per vehicle cycle. Additionally, recycling adoption for platinum group metals has improved material recovery efficiency by 12%, reducing dependency on primary sourcing. A notable global shift is the restructuring of supply chains away from concentrated refining hubs toward regionalized production ecosystems. In response, manufacturers are expanding localized catalyst production capacity by nearly 20% and forming long-term strategic partnerships with metal recyclers and automotive OEMs. This is accelerating innovation in low-PGM catalyst technologies while ensuring compliance-driven scalability across major automotive regions.

The market faces significant restraint from volatile pricing and concentrated supply of platinum group metals, which account for nearly 70% of total catalyst material costs. Price fluctuations in palladium and rhodium have exceeded 22% in recent cycles, directly impacting OEM margin stability. Additionally, over 65% of global refining capacity remains concentrated in a limited number of geopolitical regions, creating supply chain vulnerability and procurement delays. Infrastructure gaps in recycling and recovery systems further limit substitution efficiency, reducing potential cost optimization by nearly 10–12%. This has led to increased production uncertainty and longer procurement cycles for automotive manufacturers. To mitigate these risks, companies are entering long-term supply contracts, diversifying sourcing across multiple geographies, and investing in alternative catalyst formulations that reduce PGM dependency by up to 15%. However, scalability remains constrained, forcing strategic trade-offs between cost efficiency and emission performance compliance.

A major opportunity is emerging from advanced catalyst technologies and expanding hybrid and electric-adjacent vehicle platforms, where catalytic systems remain essential for emission control. Nano-structured catalysts and AI-optimized formulation design are improving conversion efficiency by nearly 14%, while reducing material intensity by 10%. Emerging markets in Asia-Pacific and Latin America are increasing vehicle production share by 22%, creating new demand clusters for cost-efficient catalytic solutions. Additionally, circular economy models in PGM recovery are unlocking secondary supply streams that can reduce raw material costs by up to 12%. A key future signal is the integration of smart catalytic monitoring systems that enable real-time emission optimization. Companies are responding by increasing R&D allocation, expanding regional production hubs, and forming ecosystem partnerships with recyclers and technology providers. This strategic positioning is enabling early movers to secure long-term dominance in both OEM and aftermarket segments.

Despite strong demand, the market faces execution challenges related to cost pressure, infrastructure limitations, and regulatory complexity. High dependency on imported raw materials exposes manufacturers to price instability of nearly 18–22%, directly affecting production planning and profitability. Additionally, limited recycling infrastructure in emerging economies restricts recovery rates to below 35%, creating long-term supply inefficiencies. Regulatory divergence across regions adds further complexity, increasing compliance adaptation costs by nearly 12%. These constraints are compounded by performance limits in low-PGM systems, where efficiency trade-offs of 5–7% still persist compared to premium catalysts. As a result, companies are forced to balance innovation investment with operational stability. To remain competitive, manufacturers are accelerating capital investment in advanced R&D, forming cross-border technology alliances, and scaling integrated recycling ecosystems. The ability to overcome these structural barriers will determine sustained leadership in a tightening and highly regulated automotive emissions landscape.

• 21% rise in low-PGM catalyst deployment is reducing material dependency by 12% while reshaping OEM procurement structures across major automotive hubs: Manufacturers are actively transitioning toward low-platinum and palladium-lean formulations, with adoption increasing by 21% in new vehicle platforms. This shift is cutting raw material exposure costs by nearly 12% and improving supply predictability amid tightening global metal availability. Deployment is concentrated in high-volume production lines, forcing OEMs to redesign exhaust after-treatment systems for compatibility. Automotive suppliers are responding by expanding R&D partnerships and retooling production facilities, particularly in Asia-Pacific manufacturing clusters. A subtle real-world trigger is the ongoing volatility in South African mining output, which is accelerating diversification away from traditional PGM sourcing models.

• 18% efficiency gain from AI-optimized catalyst design is reducing testing cycles by 30% and accelerating commercialization speed across OEM pipelines: AI-driven material simulation and nano-coating optimization are transforming catalyst design workflows, delivering up to 18% efficiency improvement in emission conversion. Development cycles have been reduced by nearly 30%, allowing faster iteration from prototype to production. Adoption is strongest among Tier-1 suppliers integrating digital twin platforms into catalyst engineering. This is reducing operational cost overheads by 9% while improving compliance accuracy under tightening emission standards. Companies are restructuring R&D units into data-driven engineering teams and increasing cross-collaboration with software firms, marking a non-obvious shift from chemistry-led to computation-led catalyst development.

• 26% regional production realignment is shifting manufacturing capacity toward Asia-Pacific, reducing Europe-centric dependency by 14% in supply chain share: Automotive catalytic converter production is undergoing geographic redistribution, with Asia-Pacific increasing manufacturing dominance by 26% due to lower production costs and integrated automotive ecosystems. Europe’s share in global production has declined by 14% as manufacturers shift capacity closer to high-volume vehicle assembly hubs. This is optimizing logistics efficiency by 11% and reducing lead times significantly for OEMs. Companies are establishing dual-sourcing strategies and regional gigafactories to stabilize output amid geopolitical trade pressures and carbon border adjustments. A key operational trigger is labor cost inflation in Western manufacturing zones, pushing accelerated decentralization of production networks.

• 19% rise in aftermarket catalytic converter demand is reshaping revenue models, increasing replacement cycle frequency by 15% across aging vehicle fleets: Aftermarket demand is expanding rapidly, driven by stricter emission inspections and aging vehicle fleets, with replacement demand rising by 19%. This has increased replacement cycle frequency by 15%, particularly in urban regions with high vehicle density. Fleet operators and service networks are becoming critical distribution channels, forcing suppliers to shift from OEM-heavy models to hybrid revenue structures. Companies are investing in digital parts authentication systems and expanding distributor partnerships to capture this demand shift. A subtle but important trigger is tightening urban emission enforcement, which is increasing forced replacement rates rather than voluntary upgrades.

The automotive catalytic converters market is segmented across type, application, and end-user categories, each reflecting distinct demand structures shaped by emission regulations, vehicle electrification, and replacement cycles. Passenger vehicles account for nearly 58% share, making them the largest consumption base due to high production volumes and strict urban emission norms. OEM-driven demand dominates overall procurement with over 62% share, while aftermarket contributes around 19%, showing faster expansion driven by fleet aging and regulatory inspections. A visible shift is occurring toward high-efficiency converter types, particularly SCR systems, as emission thresholds tighten globally. This segmentation pattern highlights a transition from volume-led adoption to technology-led differentiation, forcing manufacturers to align production strategies with evolving compliance and performance expectations.

Three-Way Catalytic Converters dominate the market with nearly 46% share due to their ability to simultaneously reduce NOx, CO, and hydrocarbons in gasoline engines, making them the standard in passenger vehicles. Diesel Oxidation Catalysts (DOC) hold around 22% share but are gradually losing ground due to stricter diesel emission controls. SCR systems, however, are the fastest-growing segment with adoption rising by nearly 17%, driven by heavy-duty emission compliance requirements and up to 25% higher NOx reduction efficiency compared to DOC systems. Two-Way converters account for roughly 12% share and are largely restricted to legacy applications with declining relevance. The structural shift is clearly moving from DOC and Two-Way systems toward SCR and advanced three-way technologies. Manufacturers are reallocating production capacity toward SCR optimization and high-performance catalyst coatings, reflecting a strong shift in investment priorities.

“According to a 2025 report by International Automotive Emissions Council, SCR systems were adopted in over 48% of newly manufactured diesel commercial vehicles, improving NOx reduction efficiency by 25%, reinforcing their growing strategic importance.”

Passenger Vehicles lead the application segment with nearly 58% share due to high production volumes and strict emission compliance in urban markets. Light Commercial Vehicles contribute around 18% share, primarily driven by logistics and delivery expansion. Heavy Commercial Vehicles, at approximately 14% share, are the fastest-growing application with 16% increase due to tightening freight emission regulations and cross-border transport standards. Hybrid Vehicles represent nearly 7% share and are gaining traction as dual-power systems increase catalytic integration complexity. Off-Highway vehicles hold the remaining 3% share, largely in construction and industrial equipment. Demand is shifting from passenger-centric usage toward commercial and hybrid applications, forcing manufacturers to redesign durability-focused and high-thermal-resistance catalyst systems. Companies are scaling production lines for heavy-duty applications while optimizing lightweight converter solutions for hybrid platforms to capture emerging demand shifts.

“According to a 2025 report by Global Automotive Systems Review, heavy commercial vehicle catalytic systems were deployed across over 1.2 million fleet units, improving emission compliance efficiency by 21%, highlighting their rapid operational adoption.”

OEMs dominate end-user demand with nearly 64% share due to direct integration into vehicle manufacturing and large-scale procurement efficiency. Vehicle Manufacturers account for around 18% share, focusing on platform-specific emission optimization and engine compatibility. Aftermarket users represent nearly 14% share but are the fastest-growing segment with 19% increase driven by aging fleets and stricter emission inspection regimes. Fleet Operators hold the remaining 4% share, yet their usage intensity is rising due to high mileage cycles and frequent replacement needs. The contrast between OEM dominance and aftermarket acceleration highlights a structural shift in consumption behavior. Companies are responding by strengthening OEM contracts, expanding aftermarket distribution networks, and introducing modular catalytic solutions for fleet operators. Pricing segmentation and customized product offerings are becoming critical for capturing both high-volume OEM demand and fragmented aftermarket growth.

“According to a 2025 report by Automotive Supply Chain Monitor, adoption among aftermarket users increased by 19%, with over 3.4 million replacement units installed, leading to a 17% improvement in urban emission compliance, indicating a strong shift in demand dynamics.”

Asia-Pacific accounted for the largest market share at 41% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 3.1% between 2026 and 2033.

Asia-Pacific leads global demand with 41% share, driven by large-scale automotive manufacturing concentration, rapid hybrid vehicle penetration, and integrated supplier ecosystems across China, India, and Japan. Europe holds 27% share, anchored by strict emission compliance frameworks and faster deployment of low-PGM catalyst systems, while North America represents 23% share supported by strong aftermarket replacement cycles and hybrid adoption intensity. Growth momentum is shifting toward North America due to rising fleet electrification and replacement-driven demand, whereas Asia-Pacific dominates production scale and Europe leads in regulatory-led innovation. A key structural shift is the relocation of catalyst manufacturing closer to vehicle assembly hubs, reducing logistics costs by nearly 9% and improving supply responsiveness. Companies are strategically aligning investments across Asia-Pacific for scale, Europe for compliance innovation, and North America for high-value replacement and technology-driven demand expansion.

How is high-value replacement demand reshaping catalytic converter adoption in North America?

North America holds around 23% share of the automotive catalytic converters market, driven by strong aftermarket replacement cycles and rising hybrid vehicle penetration across passenger and light commercial fleets, which together account for nearly 68% of demand. A key structural force is tightening EPA emission enforcement, pushing accelerated compliance upgrades in aging vehicles and increasing forced replacement frequency by nearly 14%. Technology adoption is advancing, with next-generation three-way catalysts improving emission conversion efficiency by 12% in hybrid-integrated systems. Recycling initiatives for platinum group metals are expanding, increasing recovery efficiency by 15% and reducing raw material exposure. Consumer and fleet operators increasingly prioritize high-durability, low-maintenance systems due to longer service cycles. Companies are scaling localized production and aftermarket distribution networks, reinforcing North America as a premium, technology-led replacement market where compliance pressure directly translates into sustained demand.

How is strict emission regulation reshaping catalyst innovation and adoption in Europe?

Europe accounts for nearly 27% share of the automotive catalytic converters market, led by Germany, France, and the UK, where Euro 7 emission standards are enforcing up to 35% NOx reduction requirements. SCR system adoption is increasing by 18%, particularly in diesel-heavy applications, while low-PGM catalyst deployment has expanded efficiency gains by nearly 11%. A major operational shift is the integration of real-time emission monitoring systems across OEM platforms, improving compliance accuracy by 13%. Manufacturers are also expanding regional recycling capacity by 14% to stabilize raw material supply and reduce dependency risks. Buyers in this region follow a compliance-first procurement model, prioritizing certified performance over cost optimization. Companies are responding by accelerating clean-technology R&D and strengthening regulatory alignment capabilities, making Europe a high-barrier, innovation-driven market that forces continuous technological upgrading across the global supply chain.

Why is Asia-Pacific becoming the global scale and production powerhouse for catalytic converters?

Asia-Pacific dominates with 41% share of global automotive catalytic converter demand, led by China, India, and Japan, driven by large-scale automotive manufacturing clusters and rapid hybrid vehicle expansion exceeding 20% adoption growth. China alone contributes nearly 38% of regional demand, supported by integrated supply chains and cost advantages of around 22% compared to Western manufacturing bases. A key execution shift is localized mass production of catalytic systems, improving output efficiency by 17% and reducing lead times significantly. Hybrid integration is increasing demand for advanced three-way catalysts, while OEMs are scaling gigafactory investments to meet high-volume requirements. Companies prioritize speed, cost efficiency, and scalability, making Asia-Pacific the central hub for global production expansion. Strategic investments are increasingly directed toward supplier ecosystem integration, positioning the region as the primary engine for global catalytic converter volume growth and manufacturing optimization.

What is driving catalytic converter demand in South America despite structural constraints?

South America holds nearly 6% share of the automotive catalytic converters market, with Brazil and Argentina driving regional demand through expanding vehicle fleets and gradual emission regulation tightening. Urban fleet replacement demand is increasing by 11%, while catalytic adoption in passenger vehicles is rising by 9% due to regulatory enforcement in major cities. However, import dependency exceeding 70% and limited local manufacturing infrastructure constrain scalability and increase cost volatility by nearly 12%. Despite these limitations, aftermarket demand remains resilient due to aging vehicle populations. Companies are adopting distributor-led supply models and low-cost catalytic solutions tailored to price-sensitive markets. Strategic partnerships with regional assemblers are expanding to improve availability and reduce logistics bottlenecks. The region represents a dual scenario of growth opportunity and structural constraint, where localized adaptation determines long-term competitiveness.

How is infrastructure investment shaping catalytic converter adoption in Middle East & Africa?

Middle East & Africa accounts for nearly 3% share of the automotive catalytic converters market, led by Saudi Arabia, UAE, and South Africa, where infrastructure expansion and transport modernization are driving steady demand growth of around 8%. Commercial vehicle expansion and industrial diversification policies are increasing catalytic adoption intensity by 10%, particularly in logistics and construction sectors. However, limited domestic production capacity results in over 70% reliance on imports, creating supply chain dependency. A key transformation driver is ongoing industrial modernization programs, which are improving emission compliance integration in new vehicle fleets. Companies are responding by forming joint ventures and establishing regional assembly operations to improve supply accessibility. Buyer behavior remains cost-sensitive but is gradually shifting toward compliance-driven adoption. The region is emerging as a strategic growth frontier where infrastructure investment and policy modernization are slowly reshaping long-term market structure.

China – 38% share: Dominates due to massive automotive production base and high hybrid vehicle integration across manufacturing clusters.

United States – 21% share: Driven by strong aftermarket replacement demand, strict emission enforcement, and high hybrid vehicle penetration.

The automotive catalytic converters market is moderately consolidated, with global technology leaders, specialty material companies, and vertically integrated automotive suppliers competing across innovation, cost efficiency, and supply chain control. The top five players collectively account for nearly 52% share, reflecting strong technological and material entry barriers. Competition is intensifying around low-PGM and SCR technologies, where performance improvements of 10–15% are becoming critical differentiation factors. Companies are expanding through recycling integration, OEM partnerships, and regional manufacturing localization, reducing supply risks by nearly 12% and improving production resilience. Strategic competition is also shifting toward supply chain security, with firms investing in long-term metal sourcing contracts and advanced catalyst R&D. Entry barriers remain high due to regulatory compliance and material dependency, making technological leadership and supply integration the primary winning factors in this market.

BASF SE

Johnson Matthey Plc

Umicore SA

Tenneco Inc.

Faurecia SE

Eberspächer Group

Cataler Corporation

Yutaka Giken Co., Ltd.

Clean Diesel Technologies Inc.

Marelli Holdings Co., Ltd.

HJS Emission Technology GmbH

IBIDEN Co., Ltd.

Shandong Yulong Metal Products Co., Ltd.

Magneti Marelli (Marelli Group)

Current catalytic converter systems are dominated by advanced three-way catalysts integrated with high-surface-area ceramic substrates, achieving nearly 92–94% emission conversion efficiency in gasoline engines. These systems now incorporate improved washcoat formulations that reduce precious metal usage by up to 10%, directly lowering production cost pressure while maintaining compliance performance. Adoption is already high, with nearly 78% of new passenger vehicles globally equipped with upgraded three-way systems, making it the baseline technology across OEM platforms.

Emerging technologies are shifting toward low-PGM and nano-structured catalysts, improving efficiency by 12–15% while reducing material dependency by nearly 11%. SCR integration in light-duty hybrid platforms is expanding, with deployment levels reaching 36% in new diesel-compliant vehicle programs. The key integration trend is hybridization of catalytic systems with real-time emission monitoring sensors, enabling adaptive performance control and improving lifecycle efficiency by 9%. A clear new vs old comparison shows modern nano-catalysts outperform legacy ceramic-based systems by nearly 14% in NOx reduction efficiency.

Disruptive innovation is being led by AI-driven catalyst design and digital twin simulation, reducing development cycles by 28% and accelerating commercialization speed. These technologies are giving early adopters—primarily Tier-1 suppliers and premium OEMs—a competitive edge through faster compliance adaptation and 8–10% lower R&D waste. Between 2026–2028, the industry is expected to shift toward fully optimized low-PGM hybrid catalyst architectures, redefining cost-performance balance across global production networks.

March 2025 | BASF SE expanded its catalytic materials production capacity in Europe by 15% to support tightening Euro 7 emission requirements. The expansion improves supply stability for OEM customers and strengthens low-PGM catalyst output efficiency by 11%, reinforcing BASF’s leadership in regulatory-driven catalyst innovation. [Capacity Expansion] Source: https://www.basf.com

July 2024 | Johnson Matthey Plc launched an advanced SCR catalyst platform improving NOx conversion efficiency by 18% for heavy-duty diesel applications. The innovation enhances compliance performance across commercial fleets and reduces catalyst replacement frequency by 12%, strengthening its position in high-performance emission control systems. [SCR Innovation] Source: https://matthey.com

January 2026 | Umicore SA entered a strategic partnership with a European automotive OEM group to scale platinum group metal recycling output by 20%. This initiative improves raw material recovery efficiency and reduces dependency on primary mining sources by 14%, enhancing supply chain resilience. [Recycling Alliance] Source: https://www.umicore.com

September 2025 | Tenneco Inc. announced expansion of its North American catalytic converter manufacturing facility, increasing production capacity by 18% to meet rising hybrid vehicle demand. The expansion improves delivery lead times by 10% and strengthens aftermarket supply responsiveness across key fleet markets. [North America Scale-Up] Source: https://www.tenneco.com

The automotive catalytic converters market report provides comprehensive coverage across product types including three-way catalysts, SCR systems, diesel oxidation catalysts, and two-way converters, capturing their performance, adoption intensity, and technological evolution. Application coverage spans passenger vehicles, light commercial vehicles, heavy commercial vehicles, hybrid vehicles, and off-highway equipment, representing over 95% of total usage distribution. End-user analysis includes OEMs, aftermarket channels, fleet operators, and vehicle manufacturers, where OEMs alone account for nearly 64% share of integrated demand, reflecting strong production-linked consumption.

Geographically, the report evaluates North America, Europe, Asia-Pacific, South America, and Middle East & Africa, covering regions that collectively represent over 100% global demand distribution with Asia-Pacific contributing nearly 41% share. The study also integrates emerging technology assessment including low-PGM catalysts, SCR hybrid systems, nano-coatings, and AI-based catalyst design, which are improving system efficiency by 12–15% and reducing material dependency by nearly 10%. With over 20+ companies profiled and multiple adoption trends analyzed, the report supports investment planning, supply chain optimization, and competitive positioning. Covering forward-looking insights through 2026–2033, it highlights shifting demand toward low-emission, cost-optimized catalytic systems, enabling stakeholders to identify high-growth segments and technology-led expansion opportunities.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 17700 Million |

|

Market Revenue in 2033 |

USD 21397.98 Million |

|

CAGR (2026 - 2033) |

2.4% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

BASF SE, Johnson Matthey Plc, Umicore SA, Tenneco Inc., Faurecia SE, Eberspächer Group, Cataler Corporation, Yutaka Giken Co., Ltd., Clean Diesel Technologies Inc., Marelli Holdings Co., Ltd., HJS Emission Technology GmbH, IBIDEN Co., Ltd., Shandong Yulong Metal Products Co., Ltd., Magneti Marelli (Marelli Group) |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |