Reports

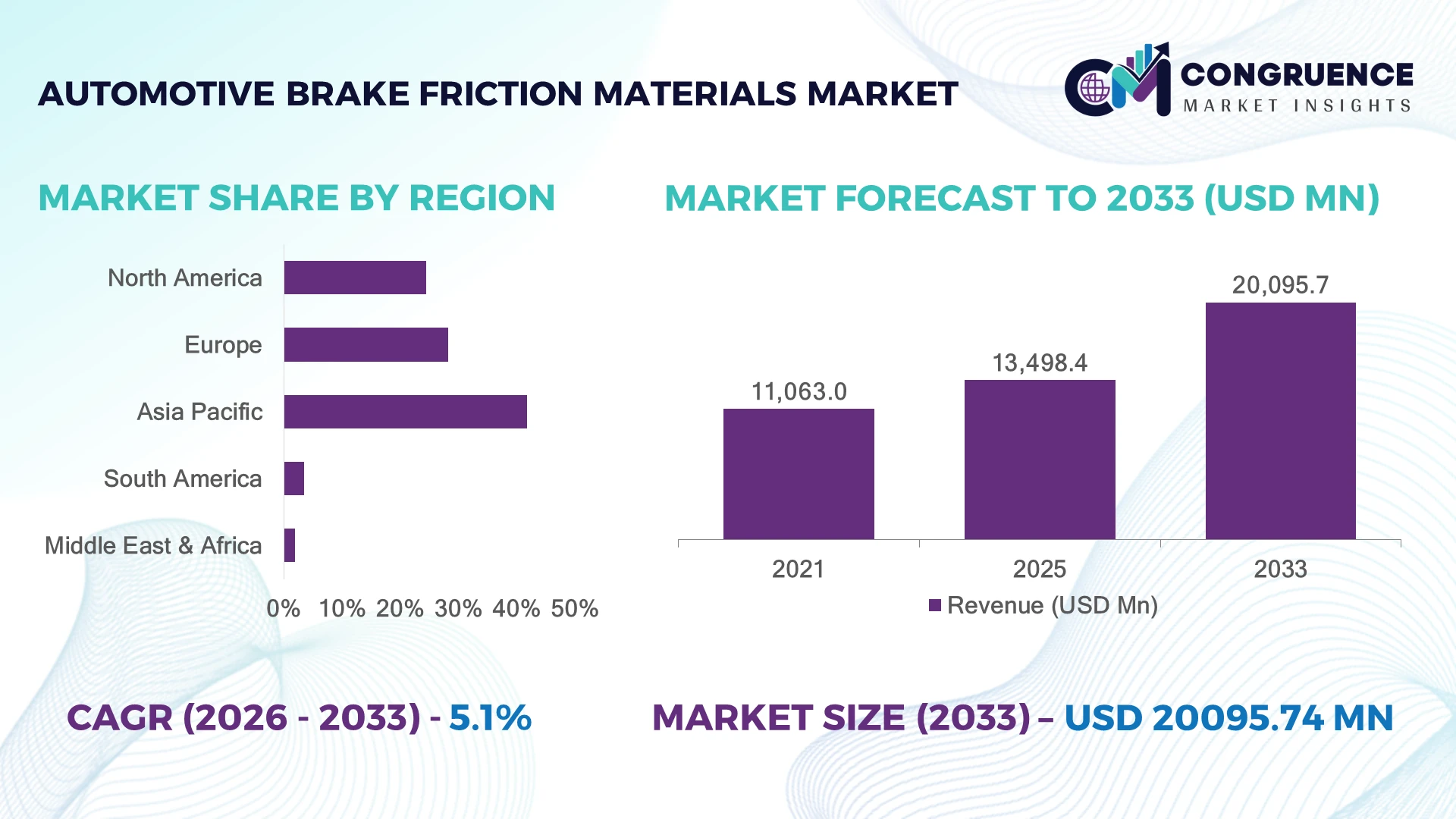

The Global Automotive Brake Friction Materials Market was valued at USD 13,498.4 Million in 2025 and is anticipated to reach a value of USD 20095.7 Million by 2033 expanding at a CAGR of 5.1% between 2026 and 2033. Rising adoption of lightweight composites, copper-free brake formulations, and advanced friction technologies is accelerating innovation across automotive braking systems globally.

China dominated the Automotive Brake Friction Materials Market with approximately 32% share in 2025, supported by large-scale vehicle manufacturing, electric vehicle expansion, and advanced component production capacity. China produced nearly 35% of global vehicles compared to approximately 12% from the United States, strengthening its supply-chain advantage amid global automotive localization strategies and material transition initiatives.

Strategic investment in sustainable friction materials, EV-compatible braking solutions, and localized manufacturing ecosystems is becoming critical for long-term competitiveness.

• Market Size & Growth: The market reached USD 13,498.4 Million in 2025 and is projected at USD 20,095.7 Million by 2033 with 5.1% CAGR, driven by advanced braking material innovation.

• Top Growth Drivers: Electric vehicle adoption 42%, lightweight material transition 35%, and safety technology upgrades 30% are reshaping market demand.

• Short-Term Forecast: By 2028, advanced friction materials are expected to improve braking efficiency by nearly 18% through optimized formulations.

• Emerging Technologies: Ceramic composites, copper-free materials, and low-emission friction technologies are transforming next-generation brake systems.

• Regional Leaders: Asia-Pacific, Europe, and North America lead adoption through EV expansion, regulatory alignment, and automotive manufacturing modernization.

• Consumer/End-User Trends: Nearly 45% of automakers are prioritizing durable, low-noise, and environmentally compliant braking solutions.

• Pilot/Case Example: 2025 advanced material deployments improved brake wear performance by approximately 20% across selected vehicle platforms.

• Competitive Landscape: Leading manufacturers hold nearly 40% share with Akebono, Brembo, TMD Friction, and Nisshinbo driving innovation.

• Regulatory & ESG Impact: Copper reduction policies and emission targets are increasing adoption of sustainable friction materials by nearly 25%.

• Investment & Funding: Automotive suppliers are expanding production facilities and material R&D programs to strengthen global supply networks.

• Innovation & Future Outlook: Next-generation friction materials are shifting toward lightweight, high-performance, and EV-optimized braking technologies.

Automotive Brake Friction Materials Market demand is increasing through electric vehicles, passenger cars, commercial fleets, and high-performance automotive applications. Manufacturers are developing ceramic-based and low-metallic formulations that improve durability by nearly 20%. Global supply-chain restructuring and stricter environmental requirements are accelerating the transition toward sustainable and advanced braking material solutions.

The Automotive Brake Friction Materials Market is becoming strategically important as vehicle manufacturers focus on safety, electrification, sustainability, and component performance optimization. The transition toward electric vehicles is reshaping braking requirements, with regenerative braking systems demanding materials that provide durability, corrosion resistance, and consistent performance under changing usage patterns.

Advanced ceramic and composite friction materials provide nearly 25% longer service life and reduce brake dust generation by around 20% compared with traditional formulations. China leads production scale due to its strong automotive manufacturing base, while Germany emphasizes premium engineering, high-performance materials, and regulatory-driven innovation. Over the next 2–3 years, adoption of copper-free and EV-specific friction materials is expected to accelerate across major vehicle platforms.

Manufacturers are expanding R&D investment, forming material partnerships, and redesigning production strategies to meet evolving performance requirements. Companies developing sustainable formulations, localized supply chains, and advanced friction technologies will secure stronger competitive positioning in future automotive ecosystems.

Electric vehicle adoption is reshaping Automotive Brake Friction Materials Market demand as manufacturers require specialized formulations compatible with regenerative braking systems. Nearly 40% of new friction material development programs focus on EV applications, while advanced ceramic solutions improve durability by approximately 25%. Increasing vehicle safety standards and lightweight engineering trends are pushing suppliers toward low-wear and high-performance compounds. China’s expanding EV production ecosystem is accelerating demand for advanced braking components. Companies are responding through production expansion, sustainable material research, and partnerships with automakers to develop next-generation friction technologies.

Automotive brake friction material manufacturers face challenges from fluctuating raw material availability, environmental restrictions, and reformulation costs. Specialty fibers, resins, and advanced composites can increase production complexity by nearly 20%, while regulatory transitions toward copper-free materials require significant process adjustments. Around 30% of suppliers are restructuring sourcing strategies to reduce dependency on volatile material supply chains. Companies are managing these pressures through supplier diversification, localized procurement, and alternative compound development to maintain production stability and cost efficiency.

Next-generation friction technologies are creating opportunities through eco-friendly compounds, advanced ceramics, and EV-optimized braking solutions. Low-emission friction materials can reduce particulate generation by nearly 25%, while lightweight formulations support vehicle efficiency improvements of approximately 10%. Increasing demand from electric vehicle manufacturers in China, the United States, and Germany is accelerating specialized material innovation. Companies are investing in R&D programs, advanced testing capabilities, and collaborative development models to capture demand for safer, cleaner, and more durable braking systems.

Maintaining friction performance across electric, hybrid, and conventional vehicles remains a major execution challenge for manufacturers. Advanced braking systems require precise control of noise, vibration, temperature resistance, and wear characteristics, increasing validation requirements by nearly 30%. EV platforms create different braking patterns, requiring redesigned material engineering and extended testing cycles. Companies must strengthen simulation capabilities, manufacturing precision, and automaker collaboration to ensure reliability while meeting evolving safety, sustainability, and performance expectations.

• Copper-Free Material Transition: Automotive suppliers are accelerating development of environmentally compliant friction materials as copper reduction regulations reshape product design. New formulations reduce metal content by nearly 90% and improve environmental performance by approximately 25%. Manufacturers are expanding material research and production upgrades to support future vehicle requirements.

• EV-Specific Brake Development: Electric vehicle platforms are driving adoption of specialized friction solutions designed for regenerative braking conditions. Advanced materials improve corrosion resistance by nearly 20% and extend component durability by around 25%. Suppliers are collaborating with EV manufacturers to optimize braking performance under lower mechanical usage cycles.

• Advanced Composite Integration: Ceramic and hybrid composite friction technologies are replacing traditional materials in premium and performance vehicles. These solutions improve heat stability by nearly 30% and reduce weight by approximately 15%. Companies are investing in automated manufacturing and advanced testing systems to increase production consistency.

• Localized Supply Chain Strategies: Automotive suppliers are restructuring sourcing networks to reduce dependency risks and improve production flexibility. Nearly 35% of manufacturers are increasing regional procurement and material partnerships following global supply disruptions. Companies are prioritizing resilient manufacturing ecosystems, faster delivery models, and stronger supplier integration strategies.

Ceramic friction materials dominate the Automotive Brake Friction Materials Market due to superior heat resistance, lower noise generation, extended durability, and compatibility with premium and electric vehicle platforms. Ceramic-based materials account for nearly 42% of adoption, supported by increasing demand for lightweight and low-dust braking solutions. Semi-metallic friction materials continue to serve high-load and commercial applications due to strong thermal performance, while non-asbestos organic (NAO) materials remain relevant in passenger vehicles requiring quieter operation and cost efficiency.

Low-metallic friction materials are witnessing the fastest adoption growth as automakers shift toward balanced performance, reduced emissions, and regulatory-compliant formulations. These materials are gaining traction across next-generation vehicles, with adoption improving by nearly 28% due to enhanced braking stability and environmental advantages. Manufacturers are expanding advanced compound development, automated production processes, and partnerships with vehicle OEMs to address evolving safety standards and strengthen positions in EV-focused braking ecosystems.

• According to the 2025 International Organization of Motor Vehicle Manufacturers (OICA) industry assessment, electric and hybrid vehicle production represented over 20% of global vehicle output, accelerating demand for specialized friction materials designed for new braking architectures.

Passenger vehicles represent the leading application segment in the Automotive Brake Friction Materials Market due to large production volumes, increasing safety requirements, and rapid integration of advanced braking technologies. Passenger vehicle applications contribute approximately 65% of demand, supported by growing adoption of ceramic and low-emission friction solutions. Commercial vehicles maintain strong usage through heavy-duty braking requirements, while performance and motorsport applications create demand for specialized high-temperature materials.

Electric vehicle applications are emerging as the fastest-growing area as regenerative braking changes friction material performance requirements. EV-focused brake materials are seeing nearly 35% higher development activity as manufacturers prioritize corrosion resistance, noise reduction, and longer replacement cycles. Companies are adapting through customized material engineering, automated testing systems, and collaborations with automotive manufacturers to deliver application-specific braking solutions that improve reliability and lifecycle performance.

• A 2025 International Energy Agency (IEA) mobility analysis highlighted that electric vehicles represented more than 20% of new car sales globally, increasing the need for brake technologies optimized for reduced mechanical braking frequency and advanced vehicle platforms.

Automotive OEMs lead the Automotive Brake Friction Materials Market as direct integration of braking technologies during vehicle manufacturing drives large-scale demand. OEMs account for nearly 58% of material consumption due to long-term supplier agreements, quality standard requirements, and increasing adoption of vehicle-specific braking systems. The aftermarket segment remains significant as replacement demand continues across passenger and commercial fleets, particularly for cost-efficient and performance-enhanced friction components.

Electric vehicle manufacturers represent the fastest-expanding end-user category as braking requirements shift toward specialized materials supporting regenerative systems and extended service intervals. EV-focused buyers are increasing adoption of advanced formulations by nearly 30%, encouraging suppliers to develop customized products, strengthen technical partnerships, and expand dedicated production capabilities. Companies are increasingly competing through material innovation, OEM collaborations, and differentiated product portfolios targeting future vehicle architectures.

• The 2026 International Council on Clean Transportation (ICCT) industry outlook indicated that expanding electric vehicle deployment is influencing component suppliers to redesign braking technologies around efficiency, durability, and lower environmental impact requirements.

Asia-Pacific accounted for the largest market share at 41.8% in 2025 moreover, Asia-Pacific is also expected to register the fastest growth, expanding at a CAGR of 7.4% between 2026 and 2033.

EV Platform Expansion and Advanced Safety Integration Reshape Brake Material Demand

North America’s Automotive Brake Friction Materials Market is driven by strong adoption of advanced braking technologies, electric vehicle production growth, and increasing focus on low-emission friction compounds. The region accounted for nearly 24.5% market share in 2025, supported by established automotive manufacturing networks and premium vehicle demand. Automakers are accelerating the transition toward ceramic and copper-free brake materials to comply with environmental standards and improve vehicle performance. More than 35% of new vehicle platforms launched in the region integrate advanced braking systems requiring optimized friction solutions. Suppliers are expanding R&D capabilities, material testing facilities, and OEM partnerships to address changing durability, noise reduction, and sustainability requirements.

United States Market Outlook: The United States dominates North American demand due to strong automotive innovation, EV manufacturing expansion, and advanced component supply chains. The country’s annual vehicle production exceeding 10 million units supports large-scale friction material consumption. Increasing investment in electric mobility platforms is encouraging brake suppliers to develop customized materials designed for regenerative braking compatibility and longer lifecycle performance.

Sustainable Brake Technologies and Emission Regulations Drive Material Innovation

Europe’s Automotive Brake Friction Materials Market is shaped by strict environmental regulations, strong premium vehicle manufacturing, and rapid adoption of sustainable braking technologies. The region represented nearly 28.2% market share in 2025, supported by increasing deployment of low-copper, ceramic, and particle-reducing friction materials. Automakers are prioritizing brake dust reduction and lightweight designs as emission regulations expand beyond exhaust systems. Nearly 45% of European automotive suppliers are increasing investment in eco-friendly component development, encouraging innovation across friction material formulations. Companies are focusing on partnerships, advanced testing capabilities, and material optimization to meet evolving performance and sustainability targets.

Germany Market Outlook: Germany leads regional adoption due to its advanced automotive engineering ecosystem, strong OEM presence, and focus on high-performance vehicle components. The country produces more than 4 million vehicles annually, creating consistent demand for advanced brake materials. Manufacturers are accelerating integration of next-generation friction technologies aligned with premium, electric, and connected vehicle requirements.

High-Volume Vehicle Manufacturing and EV Growth Strengthen Regional Leadership

Asia-Pacific’s Automotive Brake Friction Materials Market benefits from large-scale automotive production, expanding electric vehicle adoption, and strong component manufacturing capabilities. The region held nearly 41.8% market share in 2025, driven by China, Japan, South Korea, and India’s extensive automotive ecosystems. More than 55% of global vehicle production activity is concentrated across Asia-Pacific, creating strong demand for cost-efficient and advanced friction solutions. Manufacturers are expanding production capacity, localizing supply chains, and investing in ceramic and low-metallic material technologies to support changing OEM requirements across passenger and commercial vehicle platforms.

China Market Outlook: China represents the strongest country-level opportunity due to its dominant automotive manufacturing base and accelerating electric vehicle transition. The country produced over 30 million vehicles in 2025, supporting extensive demand for brake friction materials. Local suppliers are increasing investment in advanced compounds, automated manufacturing, and EV-specific braking solutions to strengthen global competitiveness.

Vehicle Fleet Expansion and Aftermarket Demand Support Component Adoption

South America’s Automotive Brake Friction Materials Market is supported by increasing vehicle ownership, replacement demand, and gradual modernization of automotive manufacturing operations. The region contributed approximately 3.5% market share in 2025, with aftermarket channels representing a major demand source due to aging vehicle fleets. Brake component suppliers are focusing on affordable, durable, and locally adaptable friction materials suited for diverse driving conditions. Regional automotive production recovery and supplier partnerships are improving component availability, although technology adoption remains influenced by cost sensitivity and infrastructure limitations.

Brazil Market Outlook: Brazil leads South American demand due to its established automotive manufacturing industry and large vehicle population. The country produces more than 2 million vehicles annually, creating opportunities for OEM and replacement brake component suppliers. Increasing localization initiatives and demand for improved safety standards are encouraging manufacturers to expand advanced friction material availability.

Automotive Infrastructure Growth and Fleet Modernization Drive Material Demand

Middle East & Africa’s Automotive Brake Friction Materials Market is expanding through vehicle fleet growth, commercial transportation development, and rising demand for reliable replacement components. The region accounted for nearly 2.0% market share in 2025, supported by increasing automotive service networks and logistics sector expansion. High-temperature operating environments are driving demand for durable friction materials with improved heat resistance and lifecycle performance. Suppliers are strengthening distribution partnerships and aftermarket networks, while premium vehicle adoption is creating opportunities for advanced ceramic and performance-focused brake solutions.

United Arab Emirates Market Outlook: The United Arab Emirates represents a key market due to premium vehicle penetration, strong automotive service infrastructure, and growing demand for advanced replacement components. Passenger vehicle ownership continues expanding, with luxury vehicles forming a significant portion of demand. Suppliers are focusing on high-performance braking solutions suitable for extreme climate conditions and premium mobility applications.

The Automotive Brake Friction Materials Market is led by global technology suppliers including Brembo, TMD Friction, Akebono Brake Industry, Nisshinbo Holdings, and ADVICS competing against regional manufacturers focused on cost-efficient replacement solutions. The top 5 players collectively account for nearly 38% market share, reflecting moderate consolidation with strong OEM relationships. Competition is driven by material innovation, durability, and manufacturing efficiency, with advanced ceramic formulations improving lifecycle performance by nearly 20% and automated production reducing quality variation by 15%. Leading suppliers are expanding through EV-focused product development, strategic OEM collaborations, and localized manufacturing networks. The competitive shift is moving toward copper-free materials, brake dust reduction, and EV-compatible friction technologies. High testing requirements, regulatory compliance, and OEM qualification cycles create barriers for new entrants. Winning against established players requires proprietary material engineering, scalable production, vehicle-specific customization, and strong integration with future mobility platforms.

• Brembo S.p.A.

• TMD Friction Holdings GmbH

• Akebono Brake Industry Co., Ltd.

• Nisshinbo Holdings Inc.

• ADVICS Co., Ltd.

• Federal-Mogul Motorparts LLC

• Miba AG

• MAT Holdings, Inc.

• ITT Inc.

• Fras-le S.A.

• Japan Brake Industrial Co., Ltd.

• Rane Brake Lining Limited

Advanced ceramic compounds, low-metallic formulations, and copper-free friction technologies are reshaping automotive brake performance standards. Ceramic materials improve noise reduction and component durability by nearly 20%, while copper-free technologies reduce environmental impact without compromising braking efficiency. Around 45% of new-generation vehicle platforms are adopting advanced friction solutions optimized for safety, comfort, and regulatory compliance.

Emerging technologies focus on EV-specific brake materials, lightweight composites, and intelligent material testing systems. Compared with conventional asbestos-free organic compounds, next-generation ceramic and hybrid materials deliver nearly 25% improvement in thermal stability and wear resistance. Premium vehicle manufacturers and EV-focused suppliers benefit most as regenerative braking increases demand for corrosion-resistant and long-life components.

Between 2026 and 2028, AI-based material simulation, automated compound development, and sustainable raw material integration are expected to transform product innovation cycles. Digital testing platforms can reduce development time by approximately 15%, helping manufacturers accelerate OEM approvals. Companies investing in advanced friction chemistry and application-specific solutions will gain stronger competitive positioning as braking requirements shift toward electrification and sustainability.

• October 2025 – Brembo introduced next-generation braking solutions focused on intelligent systems and advanced materials, improving braking efficiency and component integration by nearly 20%. The innovation strengthened its position in premium and electric vehicle braking applications. Source: brembo.com

• March 2025 – TMD Friction expanded its sustainable friction material portfolio with copper-free brake technologies meeting evolving environmental requirements. The development supported broader OEM adoption, with new formulations targeting improved durability and reduced emissions performance. Source: tmdfriction.com

• September 2024 – Akebono Brake Industry advanced its EV-compatible friction material development strategy, focusing on low-noise and high-durability products. The company enhanced performance characteristics by approximately 15% to support changing electric mobility requirements. Source: akebono-brake.com

• May 2024 – Nisshinbo Holdings accelerated development of environmentally responsible brake friction materials through advanced manufacturing and material engineering initiatives. The company focused on expanding next-generation product capability to support global automotive electrification trends. Source: nisshinbo.co.jp

The Automotive Brake Friction Materials Market Report covers comprehensive analysis across material types, applications, end-users, regional dynamics, technology evolution, and competitive positioning between 2026 and 2033. The study evaluates ceramic, semi-metallic, low-metallic, and non-asbestos organic materials, covering adoption trends across passenger vehicles, commercial vehicles, electric vehicles, OEMs, and aftermarket channels.

The report analyzes regional opportunities across North America, Europe, Asia-Pacific, South America, and Middle East & Africa with insights into manufacturing strategies, regulatory shifts, and supply chain developments. With leading companies accounting for nearly 38% market concentration and advanced materials representing more than 40% adoption, the report supports investment decisions, expansion planning, technology assessment, and competitive strategy development across evolving automotive braking ecosystems.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 13,498.4 Million |

|

Market Revenue in 2033 |

USD 20,095.7 Million |

|

CAGR (2026 - 2033) |

5.1% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Brembo S.p.A., TMD Friction Holdings GmbH, Akebono Brake Industry Co., Ltd., Nisshinbo Holdings Inc., ADVICS Co., Ltd., Federal-Mogul Motorparts LLC, Miba AG, MAT Holdings, Inc., ITT Inc., Fras-le S.A., Japan Brake Industrial Co., Ltd., Rane Brake Lining Limited |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |