Reports

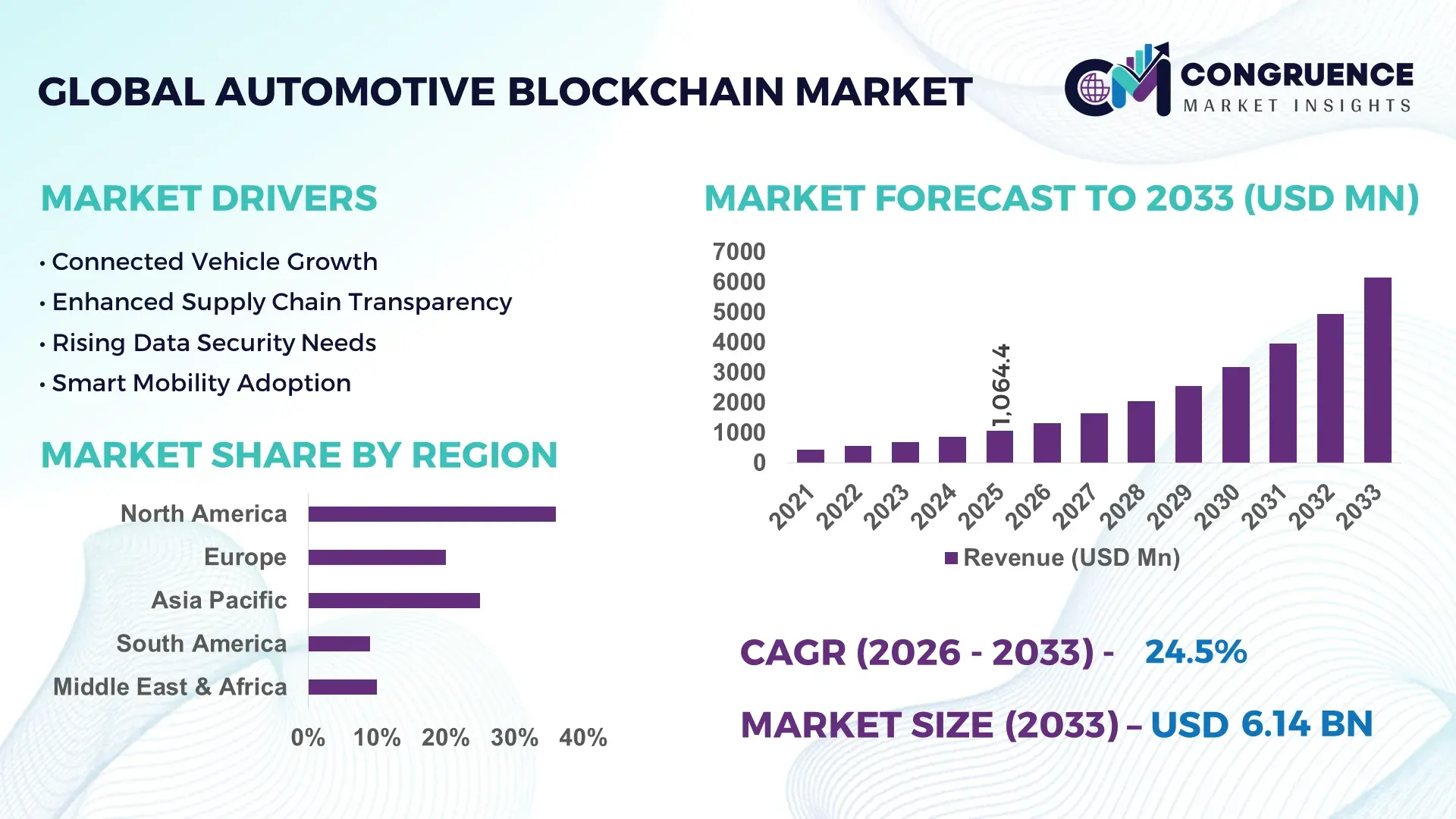

The Global Automotive Blockchain Market was valued at USD 1064.4 Million in 2025 and is anticipated to reach a value of USD 6144.13 Million by 2033 expanding at a CAGR of 24.5% between 2026 and 2033. Growth is accelerating through connected vehicle ecosystems, EV battery traceability mandates, smart-contract enabled mobility payments, and rising OEM investment in decentralized automotive supply-chain authentication platforms.

China accounted for approximately 34% of global automotive blockchain deployment activity in 2026, supported by large-scale EV production capacity, over USD 2.8 billion in smart mobility infrastructure investments, and rapid integration of blockchain-based battery passport systems across automotive manufacturing clusters. Germany followed with nearly 18% market participation through advanced automotive cybersecurity frameworks and digital vehicle identity programs. Ongoing semiconductor supply-chain restructuring after Red Sea trade disruptions increased blockchain-backed logistics tracking adoption by 27% among major automotive suppliers.

Strategic expansion increasingly depends on integrating blockchain with vehicle lifecycle management, cross-border parts verification, and software-defined vehicle ecosystems to secure long-term operational resilience and compliance efficiency.

Market Size & Growth: USD 1064.4 Million in 2025 reaching USD 6144.13 Million by 2033, driven by connected mobility platforms, EV traceability systems, and secure automotive data exchange infrastructure.

Top Growth Drivers: EV battery tracking adoption increased 31%, smart mobility transactions rose 28%, and automotive cybersecurity integration expanded 24% globally.

Short-Term Forecast: By 2028, blockchain-enabled supply-chain verification reduces counterfeit automotive components by 35% and improves logistics transparency by 29%.

Emerging Technologies: AI-integrated blockchain analytics, decentralized vehicle identity systems, and smart-contract automation accelerate processing efficiency by over 32%.

Regional Leaders: Asia-Pacific exceeds USD 2.4 billion through EV manufacturing digitization, Europe surpasses USD 1.7 billion via regulatory compliance adoption, while North America crosses USD 1.3 billion through connected vehicle ecosystems.

Consumer/End-User Trends: Nearly 41% of premium EV buyers prioritize transparent battery origin tracking and digital ownership authentication features.

Pilot/Case Example: In 2026, blockchain-based automotive logistics pilots reduced customs processing delays by 22% across multi-country vehicle shipment corridors.

Competitive Landscape: Leading providers collectively control nearly 46% market concentration, with major activity centered around IBM, Microsoft, Oracle, SAP, and AWS-integrated mobility platforms.

Regulatory & ESG Impact: Digital battery passport regulations improved material traceability compliance rates by 38% across European automotive manufacturing operations.

Investment & Funding: Global investments exceeded USD 3.1 billion, led by OEM partnerships, mobility-tech joint ventures, and advanced automotive cybersecurity expansion programs.

Innovation & Future Outlook: Tokenized vehicle services, blockchain-enabled autonomous fleet management, and software-defined vehicle ecosystems reshape high-growth automotive digital infrastructure strategies.

Automotive blockchain adoption is expanding across EV battery traceability, connected insurance systems, digital vehicle identity management, and cross-border automotive logistics networks. More than 44% of advanced mobility platforms now integrate decentralized data verification to reduce fraud exposure and accelerate transaction processing. Rising regulatory focus on battery passport compliance and supply-chain transparency is pushing automakers toward interoperable blockchain ecosystems, creating stronger operational alignment between manufacturers, suppliers, and mobility service providers ahead of broader software-defined vehicle transformation.

Automotive blockchain platforms are becoming strategically critical as automakers shift toward software-defined vehicles, connected mobility ecosystems, and digitally verified supply chains. More than 36% of global EV manufacturers now integrate blockchain-enabled traceability for battery sourcing, ownership authentication, and lifecycle compliance management. The market is also benefiting from supply-chain restructuring following semiconductor disruptions and stricter battery passport regulations introduced across Europe and China, forcing OEMs to modernize data-sharing infrastructure with tamper-resistant transaction systems.

Blockchain-enabled vehicle logistics platforms process supplier verification workflows nearly 42% faster than legacy ERP-based tracking environments while reducing administrative reconciliation costs by approximately 28%. Germany and South Korea are prioritizing blockchain deployment within advanced automotive manufacturing clusters, whereas China leads large-scale commercialization through EV production ecosystems and smart mobility payment integration. Over the next 2–3 years, digital vehicle identity adoption across premium EV platforms is expected to exceed 48%, supported by rising integration between AI-driven analytics, connected fleet management, and decentralized automotive databases.

Automotive suppliers are increasingly forming partnerships with cloud infrastructure firms and mobility software providers to accelerate blockchain interoperability across procurement, warranty management, and aftermarket operations. A growing number of OEMs now deploy blockchain-enabled battery tracking systems to improve ESG compliance and reduce counterfeit component exposure. Companies securing scalable automotive blockchain ecosystems are strengthening operational resilience, regulatory readiness, and long-term competitive positioning across next-generation mobility networks.

Rapid electrification and connected vehicle deployment are accelerating blockchain adoption across automotive manufacturing ecosystems. Nearly 39% of EV battery suppliers now use blockchain-backed material traceability systems to comply with digital passport regulations and critical mineral verification standards. China increased smart automotive infrastructure investments by over 26% in 2026, while Germany expanded blockchain-based supplier authentication programs across major automotive clusters. The shift toward software-defined vehicles and over-the-air service ecosystems is pushing OEMs to secure real-time transactional data through decentralized platforms. In response, automotive companies are increasing partnerships with cloud providers, cybersecurity firms, and semiconductor suppliers to strengthen supply-chain transparency and reduce counterfeit component exposure. A key operational advantage is the reduction of warranty fraud processing times by approximately 31% through immutable service-record verification systems.

Automotive blockchain deployment remains constrained by fragmented digital infrastructure and inconsistent interoperability standards across OEM networks. Nearly 44% of automotive suppliers still operate on legacy ERP environments that lack compatibility with decentralized transaction protocols, increasing integration costs and deployment delays. Cross-border automotive logistics networks also face data synchronization inefficiencies, particularly between North American and Southeast Asian supplier ecosystems. Rising energy consumption linked to certain blockchain validation models has increased operational scrutiny among manufacturers pursuing carbon reduction targets. To reduce scalability pressure, companies are shifting toward permissioned blockchain architectures and localized data-processing frameworks. Several Japanese automakers are also restructuring vendor contracts to standardize API integration and reduce implementation complexity, creating a more controlled transition pathway for enterprise-grade automotive blockchain adoption.

Automotive blockchain platforms are creating new monetization models through digital vehicle identity, connected insurance services, and autonomous fleet transaction ecosystems. More than 33% of premium vehicle manufacturers are testing blockchain-enabled ownership verification and usage-based mobility payment systems to improve transaction security and customer lifecycle management. India and the UAE are emerging as attractive deployment hubs due to rapid smart mobility digitization and expanding EV charging infrastructure investments. Blockchain-integrated smart contracts can lower fleet settlement processing costs by nearly 24% compared to traditional centralized clearing systems. Companies are increasingly investing in AI-enabled decentralized mobility platforms, battery recycling traceability tools, and tokenized automotive service ecosystems. A significant strategic opportunity lies in aftermarket parts authentication, where blockchain verification is reducing counterfeit distribution risks across global automotive supply chains.

Long-term market expansion depends on solving high-volume data governance, cybersecurity coordination, and cross-platform scalability challenges. Connected vehicles generate large transactional datasets, yet nearly 37% of automotive firms report difficulties integrating blockchain networks with real-time telematics and edge-computing infrastructure. Regulatory divergence between the European Union, China, and the United States is also complicating decentralized data-storage compliance frameworks for automotive manufacturers operating across multiple jurisdictions. Rising ransomware attacks targeting automotive software ecosystems have intensified pressure on blockchain security validation standards and digital identity controls. Companies must strengthen interoperability testing, encryption frameworks, and cloud-edge synchronization capabilities to maintain deployment consistency. Automotive OEMs investing early in standardized blockchain governance architecture and cybersecurity partnerships are expected to secure stronger operational resilience and supplier network stability over the next decade.

• Battery Passport Integration Accelerates Automotive manufacturers are rapidly integrating blockchain-backed battery passport systems following stricter EV traceability mandates across Germany and China. More than 43% of premium EV suppliers upgraded material verification workflows during 2026, reducing compliance reporting delays by 31%. Companies are restructuring procurement systems and expanding cloud-based blockchain partnerships to secure mineral sourcing transparency, improve recycling traceability, and reduce counterfeit battery component exposure across multi-country supply chains.

• Smart Contracts Reshape Logistics Blockchain-enabled smart contracts are transforming automotive logistics workflows by automating customs validation, inventory reconciliation, and supplier settlements. Cross-border automotive shipment processing times declined by nearly 27%, while payment disputes dropped 22% across digitally integrated supplier networks. Japanese and South Korean manufacturers are scaling decentralized logistics platforms to offset semiconductor supply volatility and port congestion risks, improving operational continuity through real-time shipment authentication and automated transaction execution.

• Connected Vehicle Data Monetization Automotive OEMs are increasingly monetizing connected vehicle ecosystems through decentralized data-sharing frameworks. Nearly 38% of software-defined vehicle programs now integrate blockchain-based digital identity layers for usage tracking, predictive maintenance, and insurance verification. U.S. mobility platforms are deploying tokenized transaction models to support subscription-based mobility services, while automakers are expanding cybersecurity investments to secure vehicle-generated telematics data against rising ransomware threats targeting automotive software infrastructure.

• Dealer Networks Digitize Ownership Records Automotive dealer ecosystems are replacing paper-based ownership verification and warranty documentation with blockchain-backed digital record systems. Vehicle title transfer processing improved by approximately 34% in pilot deployments across the UAE and Singapore, while fraudulent warranty claims declined 26%. Companies are responding through dealership software modernization, API-based integration with insurance providers, and expansion of blockchain-enabled aftersales ecosystems to improve transaction speed, resale transparency, and lifecycle service management.

Private blockchain remains the dominant segment due to stronger scalability control, enterprise-grade cybersecurity, and compatibility with automotive OEM infrastructure requirements. Nearly 48% of automotive blockchain deployments in 2026 operated through private blockchain environments, particularly across EV battery traceability, supplier authentication, and connected manufacturing systems. Automotive manufacturers in Germany and Japan increasingly prefer permissioned architectures to improve data governance and reduce operational latency by approximately 29% compared to public-chain transaction models. Companies are expanding private blockchain integration through cloud partnerships, cybersecurity upgrades, and API-based supplier onboarding programs.

Hybrid blockchain is emerging as the fastest-growing segment as automakers seek balanced interoperability between internal enterprise systems and external mobility ecosystems. Smart contracts are also gaining strategic relevance through automated warranty settlements, fleet payments, and digital vehicle ownership verification, reducing administrative processing workloads by nearly 24%. Consortium blockchain adoption is expanding among logistics providers and semiconductor suppliers to improve cross-enterprise transparency, while public blockchain remains concentrated within mobility payment pilots and tokenized automotive service experiments. Automotive software vendors are increasingly prioritizing modular blockchain platforms to support multi-network deployment flexibility.

Supply Chain Management remains the leading application segment due to rising pressure for real-time supplier visibility, battery mineral traceability, and counterfeit component reduction. More than 46% of automotive blockchain deployments in 2026 focused on logistics authentication, procurement tracking, and parts verification workflows. Automotive manufacturers in China and Germany accelerated blockchain integration following semiconductor supply disruptions and stricter EV compliance standards. Companies are strengthening deployment through automated inventory reconciliation, cloud-based supplier coordination, and decentralized shipment verification systems that reduced logistics processing delays by approximately 28%.

Mobility Services represents the fastest-growing application as software-defined vehicle ecosystems expand across connected transportation networks. Blockchain-enabled mobility payments and digital identity management platforms improved transaction authentication efficiency by nearly 33% across shared mobility operations. Vehicle Data Security is also gaining strategic importance as connected cars generate large telematics datasets requiring tamper-resistant storage and decentralized access controls. Digital Payments adoption is increasing across autonomous fleet settlement systems, while Vehicle Tracking continues expanding through blockchain-integrated telematics infrastructure. Automotive technology firms are responding through AI-integrated blockchain deployment, interoperability partnerships, and expansion of decentralized mobility platforms targeting urban transportation ecosystems.

Automotive Manufacturers represent the dominant end-user segment due to extensive deployment across production networks, battery traceability systems, connected vehicle platforms, and supplier authentication infrastructure. Nearly 51% of automotive blockchain implementation activity in 2026 originated from OEM-led manufacturing ecosystems, particularly in China, Germany, and South Korea. Large automakers are integrating decentralized verification tools into procurement, quality assurance, and aftersales operations to reduce counterfeit component exposure and improve workflow transparency. Companies are expanding blockchain adoption through cloud infrastructure alliances, cybersecurity investments, and vertically integrated digital supply-chain modernization strategies.

Mobility Service Providers are emerging as the fastest-growing end-user group as subscription-based mobility platforms and autonomous fleet ecosystems expand. Blockchain-enabled payment verification and decentralized customer identity systems improved transaction processing efficiency by approximately 32% across digitally integrated ride-sharing operations. Fleet Operators and Logistics Companies are increasingly adopting blockchain-backed tracking systems to improve cargo visibility and automate settlement processes, while Insurance Companies are deploying smart-contract frameworks to accelerate claims validation and fraud detection. Automotive Dealers are modernizing ownership transfer workflows through blockchain-enabled documentation systems. Technology providers are responding with sector-specific deployment models, scalable pricing structures, and ecosystem-focused interoperability partnerships targeting high-volume mobility operators.

Asia-Pacific accounted for the largest market share at 41% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 27.1% between 2026 and 2033.

Connected Mobility Infrastructure Expansion

North America remains a high-value automotive blockchain deployment hub driven by connected vehicle ecosystems, advanced cloud infrastructure, and enterprise-grade cybersecurity integration. The region contributed approximately 28% of global deployment activity in 2025, supported by strong adoption across EV supply-chain verification, smart-contract logistics, and mobility payment platforms. U.S.-based automotive technology firms accelerated blockchain integration within software-defined vehicle programs, while logistics operators increased decentralized shipment authentication deployments by nearly 24%. Strategic alliances between automotive OEMs, cloud providers, and semiconductor companies are strengthening blockchain interoperability across procurement and fleet management systems. Growing pressure to secure vehicle-generated telematics data is also increasing enterprise investment in decentralized digital identity frameworks and blockchain-enabled compliance management infrastructure.

United States Market Outlook: The United States leads regional deployment through large-scale connected mobility infrastructure, advanced automotive software ecosystems, and strong enterprise blockchain integration capabilities. More than 46% of North American automotive blockchain pilot programs originated from U.S.-based OEMs and mobility technology companies during 2026. Automotive firms are prioritizing blockchain deployment for EV battery authentication, digital vehicle ownership verification, and automated insurance settlement systems. Strong venture investment activity and partnerships between cloud hyperscalers and automotive manufacturers continue accelerating commercialization of decentralized mobility transaction platforms across premium vehicle and autonomous fleet ecosystems.

Regulatory-Driven Traceability Transformation

Europe is strengthening its position through regulatory-led automotive digitization, battery traceability modernization, and advanced vehicle lifecycle management systems. The region accounted for nearly 25% of global automotive blockchain deployment activity in 2025, driven by strict EV battery passport regulations and carbon-traceability requirements. Germany, France, and the Netherlands are increasing blockchain integration across automotive manufacturing and supplier verification ecosystems to improve compliance transparency and reduce counterfeit component risks. Automotive logistics operators reduced cross-border shipment reconciliation delays by approximately 21% through decentralized transaction platforms. Enterprise focus is shifting toward permissioned blockchain environments capable of supporting real-time compliance auditing, secure supplier collaboration, and automated sustainability reporting within high-volume EV manufacturing networks.

Germany Market Outlook: Germany remains the regional technology and manufacturing leader due to its advanced automotive engineering ecosystem and large-scale EV production infrastructure. More than 38% of Europe’s automotive blockchain enterprise deployments were concentrated within German automotive manufacturing clusters in 2026. OEMs and Tier-1 suppliers are aggressively integrating blockchain-backed procurement tracking, battery traceability, and digital warranty systems to strengthen export competitiveness and regulatory readiness. Industrial partnerships between automotive manufacturers, cybersecurity firms, and industrial cloud providers are also accelerating deployment of scalable blockchain governance frameworks across connected factory operations.

Large-Scale EV Ecosystem Integration

Asia-Pacific dominates the automotive blockchain market through extensive EV manufacturing capacity, high-volume supplier ecosystems, and rapid smart mobility digitization. The region represented approximately 41% of global adoption activity in 2025, supported by aggressive deployment across battery traceability, automotive logistics authentication, and digital mobility payments. China, Japan, and South Korea are scaling blockchain integration within automotive procurement and connected vehicle infrastructure to reduce counterfeit component exposure and improve production visibility. Automotive supply-chain operators across the region improved inventory synchronization efficiency by nearly 32% through decentralized transaction systems. Enterprise investment is increasingly focused on blockchain-enabled telematics, AI-driven logistics optimization, and scalable smart-contract deployment across export-oriented automotive production corridors.

China Market Outlook: China leads the global automotive blockchain ecosystem through unmatched EV production scale, integrated digital infrastructure, and strong state-backed smart mobility initiatives. More than 34% of worldwide automotive blockchain implementation activity originated from Chinese automotive and mobility ecosystems in 2026. Domestic automakers are rapidly integrating blockchain-enabled battery lifecycle management and decentralized supplier verification systems to strengthen export compliance and production resilience. Large-scale investments in connected transportation infrastructure and cloud-based industrial platforms continue accelerating deployment of blockchain-supported vehicle identity management and cross-border automotive logistics authentication solutions.

Supply-Chain Digitization Gains Momentum

South America is gradually expanding automotive blockchain deployment through logistics modernization, fleet digitization, and cross-border trade verification initiatives. The region accounted for nearly 4% of global automotive blockchain activity in 2025, with adoption concentrated in automotive manufacturing and aftermarket logistics operations. Brazil and Argentina are increasing investment in decentralized shipment authentication and digital inventory coordination to reduce operational inefficiencies across fragmented supplier networks. Automotive logistics providers improved cargo verification accuracy by approximately 18% through blockchain-supported tracking systems during pilot deployments. Infrastructure limitations and uneven cloud integration continue constraining enterprise-scale adoption, yet growing pressure for supply-chain transparency is accelerating partnerships between regional manufacturers, software vendors, and logistics technology providers.

Brazil Market Outlook: Brazil remains the region’s most strategically significant automotive blockchain market due to its large vehicle manufacturing base and expanding logistics digitization programs. Automotive suppliers and fleet operators are deploying blockchain-backed inventory validation and shipment authentication systems to reduce customs processing delays and counterfeit component risks. In 2026, blockchain-enabled fleet coordination projects improved logistics workflow efficiency by nearly 19% across selected automotive transport corridors. Regional automotive enterprises are also prioritizing cloud integration partnerships and decentralized procurement management systems to strengthen supply-chain continuity and export competitiveness.

Smart Mobility Modernization Expands

Middle East & Africa is emerging as the fastest-transforming automotive blockchain market through smart city investment, mobility infrastructure modernization, and digital trade integration. The region represented approximately 2% of global deployment activity in 2025 but is rapidly scaling blockchain integration within connected transportation and vehicle authentication ecosystems. The UAE and Saudi Arabia are increasing investment in decentralized mobility payment systems, blockchain-backed customs verification, and intelligent logistics infrastructure supporting EV ecosystem expansion. Automotive transaction processing efficiency improved by nearly 23% across selected blockchain-enabled trade and fleet management pilots. Governments and enterprise operators are accelerating partnerships with cloud infrastructure providers and mobility technology firms to support secure digital transportation networks and scalable smart-contract deployment.

United Arab Emirates Market Outlook: The UAE is positioning itself as a regional blockchain mobility innovation hub through advanced smart city programs, digital government infrastructure, and integrated transportation modernization strategies. More than 45% of automotive blockchain pilot deployments across the Middle East during 2026 were concentrated within UAE-based mobility and logistics ecosystems. Automotive dealers, fleet operators, and customs authorities are deploying blockchain-supported ownership verification and shipment authentication systems to improve operational transparency and transaction speed. Strong enterprise cloud adoption and national digital transformation initiatives continue supporting rapid commercialization of decentralized automotive service platforms.

Global technology providers including IBM, Microsoft, Oracle, SAP, and Amazon Web Services compete directly with automotive-focused blockchain integrators and mobility software firms for enterprise-scale deployment contracts. The top five players collectively control nearly 49% of enterprise automotive blockchain integration activity through cloud infrastructure dominance, cybersecurity capabilities, and OEM partnerships. Competition increasingly centers on interoperability speed, transaction scalability, and supply-chain visibility, with blockchain-enabled logistics workflows reducing verification delays by 27% and administrative processing costs by 24%. Automotive OEMs are partnering with cloud hyperscalers to vertically integrate battery traceability, digital identity, and connected mobility ecosystems, while regional software providers compete through lower deployment costs and customization flexibility. The competitive landscape is shifting toward consortium-led ecosystems and AI-integrated blockchain platforms as automakers prioritize software-defined vehicle infrastructure. High integration complexity, regulatory compliance requirements, and cybersecurity certification remain major entry barriers. Winning requires scalable interoperability, enterprise-grade security architecture, and deep automotive supply-chain integration expertise.

IBM Corporation

Microsoft Corporation

Oracle Corporation

SAP SE

Amazon Web Services

Infosys Limited

Accenture plc

Guardtime

BigchainDB GmbH

VeChain Foundation

HCL Technologies

NXP Semiconductors

XAIN AG

MOBI (Mobility Open Blockchain Initiative)

Automotive blockchain infrastructure is shifting from standalone pilot environments toward enterprise-scale integration with AI-driven supply-chain orchestration, connected vehicle identity systems, and EV battery traceability platforms. Nearly 46% of premium automotive manufacturers now deploy permissioned blockchain frameworks for procurement verification and logistics synchronization. Compared with legacy ERP reconciliation systems, blockchain-integrated workflows reduce transaction validation time by approximately 34% while improving inventory accuracy by 27%. Automotive OEMs are increasingly integrating blockchain with cloud-native telematics platforms to strengthen cybersecurity, automate warranty validation, and improve cross-border parts authentication efficiency.

Emerging technologies between 2026 and 2028 include decentralized vehicle identity architecture, zero-knowledge proof authentication, and smart-contract enabled mobility settlement systems. More than 31% of mobility service providers are testing tokenized payment ecosystems linked with blockchain-secured digital ownership verification. AI-enabled blockchain analytics platforms are also reducing supplier fraud detection cycles by nearly 22% compared to manual audit frameworks. German and South Korean automakers are scaling interoperability-focused blockchain ecosystems to support software-defined vehicle infrastructure and automated compliance management.

Disruptive momentum is accelerating around blockchain-integrated battery passports and autonomous fleet transaction systems. Hybrid blockchain models improve processing flexibility by nearly 29% over fully public-chain deployments while lowering operational latency across multi-vendor automotive ecosystems. Cloud hyperscalers, cybersecurity firms, and connected mobility providers are securing competitive advantage through vertically integrated blockchain deployment platforms. Companies delaying infrastructure modernization risk weaker supply-chain visibility, slower compliance execution, and reduced positioning within next-generation automotive data ecosystems.

April 2024 – MOBI and Gaia-X 4 moveID launched a cross-industry interoperability initiative integrating Vehicle Identity and Battery Birth Certificate standards using W3C frameworks, improving decentralized automotive identity compatibility across multiple ecosystems. The initiative strengthened battery traceability and digital compliance execution within EV supply chains. Source: MOBI

March 2025 – SAP and Catena-X expanded blockchain-enabled automotive quality management integration, targeting faster recall identification and supplier traceability across manufacturing ecosystems. German automakers reported potential optimization of recall-response workflows linked to annual reserve exposures exceeding EUR 1.4 billion, improving operational transparency and cross-enterprise data synchronization. Source: SAP News Center

May 2025 – SAP introduced AI-powered network-centric supply-chain innovations supporting blockchain-compatible automotive data orchestration and real-time supplier collaboration. The upgraded ecosystem improved enterprise workflow visibility and accelerated intelligent logistics coordination, strengthening digital synchronization across automotive procurement and manufacturing operations under increasingly complex global trade conditions. Source: SAP News Center

March 2026 – IBM, Yubico, and Auth0 formed a partnership focused on cryptographically verified authorization frameworks for high-risk AI-driven enterprise workflows. The initiative strengthened governance controls for automated decentralized transaction environments, improving secure execution capability for blockchain-supported automotive identity verification and mobility infrastructure management systems. Source: IBM

The Automotive Blockchain Market report provides comprehensive analysis across blockchain types including Public Blockchain, Private Blockchain, Consortium Blockchain, Hybrid Blockchain, and Smart Contracts, with detailed evaluation of deployment efficiency, interoperability trends, and enterprise integration strategies. The study covers major applications such as Supply Chain Management, Vehicle Tracking, Digital Payments, Vehicle Data Security, and Mobility Services across automotive manufacturers, fleet operators, logistics companies, insurance providers, and mobility service platforms. More than 45% of enterprise blockchain activity remains concentrated within supply-chain and battery traceability ecosystems, highlighting growing operational reliance on decentralized automotive data infrastructure.

The report delivers region-wise assessment across North America, Europe, Asia-Pacific, South America, and Middle East & Africa, focusing on deployment concentration, EV ecosystem modernization, regulatory digitization, and connected mobility infrastructure expansion between 2026 and 2033. It also evaluates AI-integrated blockchain platforms, decentralized vehicle identity systems, smart-contract automation, and battery passport technologies shaping future automotive operations. Strategic insights support investment prioritization, technology adoption planning, partnership evaluation, competitive benchmarking, and long-term digital mobility positioning across high-growth automotive blockchain ecosystems.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 1064.4 Million |

|

Market Revenue in 2033 |

USD 6144.13 Million |

|

CAGR (2026 - 2033) |

24.5% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

IBM Corporation, Microsoft Corporation, Oracle Corporation, SAP SE, Amazon Web Services, Infosys Limited, Accenture plc, Guardtime, BigchainDB GmbH, VeChain Foundation, HCL Technologies, NXP Semiconductors, XAIN AG, MOBI (Mobility Open Blockchain Initiative) |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |