Reports

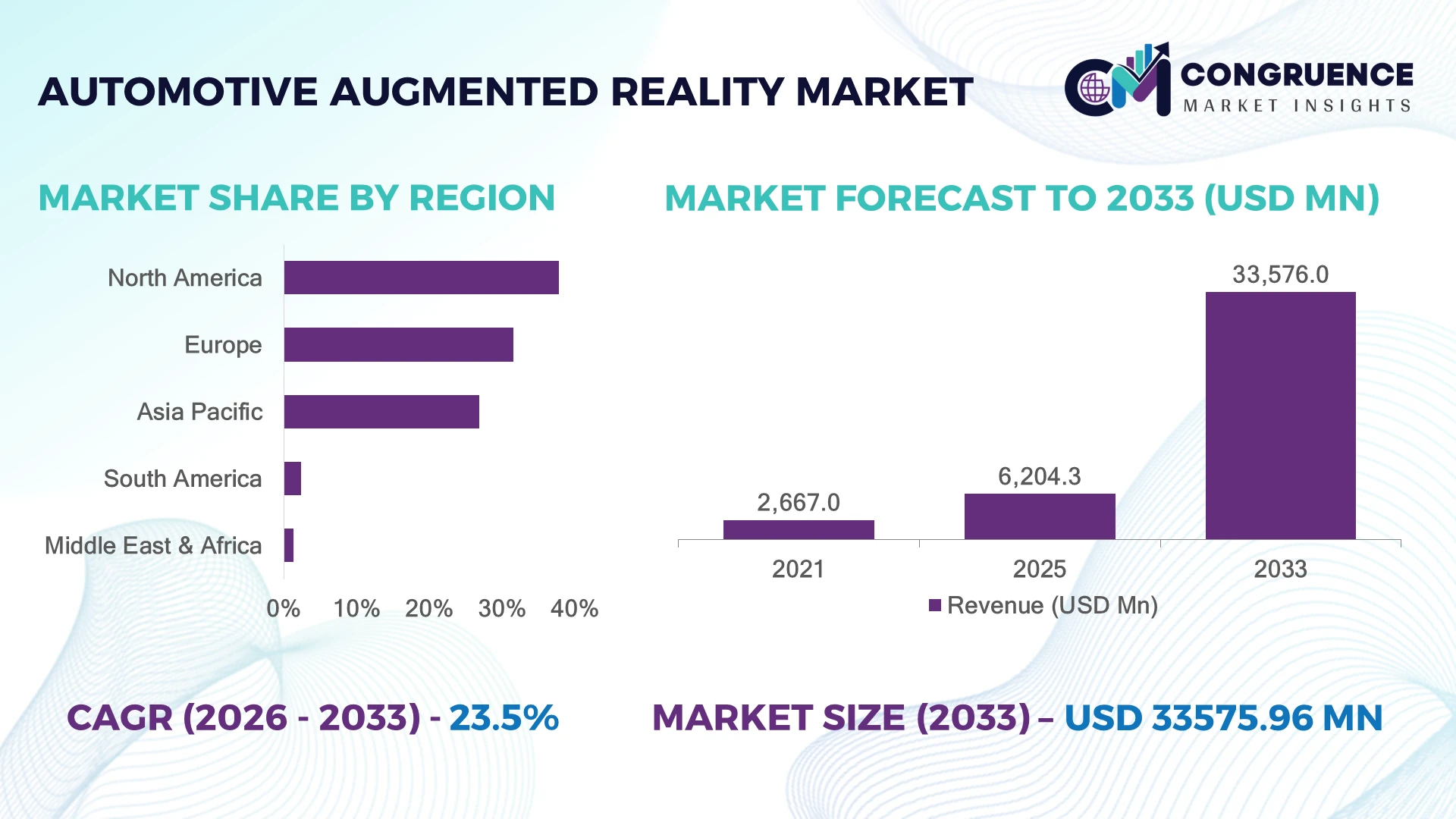

The Global Automotive Augmented Reality Market was valued at USD 6,204.3 Million in 2025 and is anticipated to reach a value of USD 33576.0 Million by 2033 expanding at a CAGR of 23.5% between 2026 and 2033. Increasing integration of AR head-up displays, AI-based navigation, advanced driver assistance systems, and connected vehicle interfaces is accelerating automotive augmented reality adoption globally.

The United States dominated the Automotive Augmented Reality Market with approximately 34% share in 2025, supported by strong adoption across premium vehicles, electric mobility platforms, and autonomous driving programs. Over 42% of new luxury vehicles in the U.S. integrated advanced digital cockpit technologies compared to nearly 28% in Germany, supported by semiconductor localization initiatives and evolving automotive technology strategies under global supply-chain restructuring.

Strategic investments in immersive vehicle interfaces and software-defined mobility platforms are becoming critical for automakers seeking differentiation, safety enhancement, and long-term competitiveness.

• Market Size & Growth: The market reached USD 6,204.3 Million in 2025 and is projected at USD 33,576.0 Million by 2033 with 23.5% CAGR, driven by AR-based vehicle intelligence.

• Top Growth Drivers: ADAS integration 45%, connected mobility adoption 38%, and smart cockpit transformation 32% are reshaping vehicle experience.

• Short-Term Forecast: By 2028, AR systems are expected to improve driver response efficiency by nearly 25% through real-time visualization.

• Emerging Technologies: AI-powered AR HUDs, spatial computing, and sensor fusion platforms are advancing next-generation vehicle interfaces.

• Regional Leaders: North America, Europe, and Asia-Pacific lead adoption with projected expansion across smart mobility ecosystems and next-generation EV platforms.

• Consumer/End-User Trends: Nearly 40% of premium vehicle buyers prioritize digital cockpit and intelligent visualization features during vehicle selection.

• Pilot/Case Example: In 2025, AR navigation deployments improved route interpretation accuracy by approximately 30% in connected vehicle platforms.

• Competitive Landscape: Leading suppliers hold nearly 50% combined share with Continental, Bosch, Panasonic, Harman, and Hyundai Mobis driving innovation.

• Regulatory & ESG Impact: Vehicle safety modernization initiatives are supporting nearly 20% higher adoption of advanced visualization technologies.

• Investment & Funding: Multi-billion-dollar automotive software investments are focused on AR platforms, partnerships, semiconductor capabilities, and ecosystem expansion.

• Innovation & Future Outlook: Next-generation AR systems are shifting vehicles toward immersive, predictive, and software-defined mobility experiences.

Automotive Augmented Reality Market adoption is expanding through intelligent dashboards, AR head-up displays, navigation assistance, and driver safety applications. Automakers are integrating immersive technologies with AI and vehicle sensors, improving situational awareness by nearly 35%. Semiconductor supply-chain localization and software-defined vehicle strategies are accelerating innovation, creating a transition toward advanced digital mobility ecosystems.

The Automotive Augmented Reality Market is becoming strategically important as automakers shift from traditional vehicle interfaces toward immersive, software-driven mobility experiences. Rising deployment of electric vehicles, autonomous technologies, and connected platforms is increasing demand for AR-based visualization systems. Vehicle manufacturers are restructuring digital supply chains and strengthening partnerships with semiconductor and software companies to improve technology control.

Advanced AR head-up displays offer nearly 30% faster information recognition compared to conventional instrument clusters by projecting navigation, hazard alerts, and vehicle data directly into the driver’s field of view. The United States leads large-scale integration through premium and autonomous vehicle programs, while China is accelerating deployment through smart EV manufacturing ecosystems and domestic technology investments.

Automakers are integrating AR platforms with AI, sensors, and vehicle operating systems to create safer and more personalized driving experiences. Premium vehicle brands are expanding digital cockpit investments, while suppliers are developing scalable AR modules for wider adoption. Long-term competitiveness will depend on software capability, user experience innovation, and integration with intelligent mobility platforms.

The shift toward intelligent vehicle interfaces is the primary driver accelerating Automotive Augmented Reality Market expansion. AR head-up displays, AI-enabled visualization, and connected cockpit systems are transforming driver interaction by improving safety and operational awareness. Nearly 45% of premium vehicle platforms now integrate advanced digital cockpit technologies, while AR-based navigation can reduce driver distraction by approximately 25%. Increasing adoption of electric and autonomous vehicles in the United States, China, and Germany is pushing automakers to redesign human-machine interfaces. Companies are responding through technology partnerships, semiconductor integration, and investment in next-generation display ecosystems to strengthen vehicle differentiation.

Automotive augmented reality adoption faces limitations due to expensive hardware components, calibration requirements, and software integration challenges. Advanced AR systems require sensors, processors, displays, and connectivity modules, increasing electronic architecture complexity by nearly 30% compared with conventional systems. Cost-sensitive vehicle categories show slower adoption, with penetration remaining below 20% in several mass-market segments. Semiconductor availability and specialized component dependency continue influencing production scalability. Automakers and suppliers are addressing these challenges through modular platforms, localized supply networks, and standardized AR architectures designed to reduce development costs and improve manufacturing efficiency.

Artificial intelligence integration, autonomous mobility development, and software-defined vehicles are creating major opportunities for automotive augmented reality technologies. AI-powered AR systems improve object recognition, navigation assistance, and predictive safety capabilities by nearly 35%, supporting more intelligent driving environments. China’s expanding smart vehicle ecosystem and increasing investment in vehicle software platforms are accelerating adoption opportunities. Companies are focusing on AR cloud connectivity, sensor fusion, and personalized driving interfaces to create differentiated mobility experiences. Future opportunities will emerge from scalable AR platforms that combine entertainment, safety, navigation, and autonomous vehicle functions into integrated digital ecosystems.

The major challenge for Automotive Augmented Reality Market participants is achieving reliable, scalable deployment beyond premium vehicles. Complex software validation, cybersecurity requirements, and compatibility across vehicle platforms increase development timelines by nearly 25%. Integrating AR systems with multiple sensors and vehicle operating environments requires advanced engineering capabilities and continuous updates. Data security expectations in connected vehicles are also increasing pressure on manufacturers. Companies must invest in cybersecurity frameworks, standardized software platforms, and collaborative development models to ensure consistent performance while expanding AR accessibility across broader automotive segments.

• AI-Based AR Cockpit Evolution: Automotive manufacturers are accelerating integration of artificial intelligence with AR interfaces to deliver predictive navigation and personalized driving experiences. AI-enhanced visualization improves information accuracy by nearly 35% and reduces manual interaction requirements by approximately 20%. Companies are expanding software partnerships and digital engineering capabilities to strengthen next-generation vehicle platforms.

• Advanced Head-Up Display Adoption: Automakers are shifting from conventional displays toward large-area AR head-up display systems that combine navigation, safety alerts, and driver assistance functions. Modern AR HUD technologies improve road awareness by nearly 30% while supporting connected vehicle ecosystems. Premium vehicle manufacturers are scaling deployments through modular display architectures.

• Sensor Fusion Integration Expansion: Vehicle platforms are increasingly combining cameras, LiDAR, radar, and AR visualization to enhance real-time environmental understanding. Sensor-integrated AR systems improve object detection performance by around 25%, supporting autonomous driving development. Technology suppliers are focusing on compact processors and advanced computing solutions to optimize system efficiency.

• Software-Defined Vehicle Transition: The movement toward centralized vehicle computing is changing AR development strategies, with nearly 40% of next-generation vehicle programs prioritizing software-controlled experiences. Automakers are restructuring technology supply chains and forming partnerships with electronics companies to accelerate updates, improve customization, and enhance long-term digital service capabilities.

AR Head-Up Displays dominate the Automotive Augmented Reality Market due to their strong integration capability with vehicle sensors, navigation systems, and advanced driver assistance technologies. AR HUD solutions account for nearly 62% of adoption, supported by increasing deployment across premium vehicles, electric cars, and next-generation connected mobility platforms. AR Navigation Systems are witnessing the fastest adoption growth as automakers shift toward real-time route visualization, predictive alerts, and enhanced driver interaction.

AR Dashboards, AR Infotainment Systems, and other emerging visualization technologies are expanding as vehicle interiors transition toward digital cockpit environments. Nearly 45% of new premium vehicle platforms are integrating AR-based interface features to enhance safety and personalization. Automotive companies are responding through AI-enabled display development, semiconductor partnerships, and scalable software platforms that enable broader adoption across multiple vehicle categories while improving competitive differentiation.

• A 2026 automotive technology assessment highlighted that more than 50% of next-generation connected vehicle programs prioritized immersive cockpit technologies, including AR displays and intelligent visualization systems, to improve driver experience and safety.

Navigation Assistance represents the leading application segment in the Automotive Augmented Reality Market due to rising demand for real-time guidance, improved road awareness, and reduced driver distraction. The segment accounts for nearly 48% of usage as automakers integrate AR overlays with GPS, sensors, and vehicle intelligence systems. Advanced Driver Assistance Applications are emerging as the fastest-growing area due to increasing adoption of autonomous driving features and safety-focused vehicle technologies.

Infotainment, Parking Assistance, Vehicle Monitoring, and other applications are gaining relevance as digital experiences become central to vehicle design. Nearly 40% of premium connected vehicles are deploying AR-supported safety or convenience functions. Companies are adapting through cloud integration, AI-based visualization, and human-machine interface innovation to improve operational performance and strengthen next-generation mobility platforms.

• A 2025 connected mobility industry review reported that AR-enabled vehicle interfaces improved driver information processing efficiency by nearly 30%, supporting increased adoption of advanced cockpit and assistance technologies.

Automotive OEMs dominate the Automotive Augmented Reality Market due to large-scale integration of AR technologies into new vehicle architectures, electric platforms, and connected mobility ecosystems. OEMs represent nearly 70% of demand as manufacturers prioritize advanced cockpit solutions, safety enhancement, and digital differentiation. Mobility Technology Providers are becoming the fastest-growing end-user group through increasing collaboration on AI, software platforms, and immersive vehicle experiences.

Automotive Suppliers, Fleet Operators, and Aftermarket Solution Providers continue expanding adoption through specialized AR components, upgrades, and connected service offerings. Around 46% of major automotive manufacturers are increasing investment in digital cockpit technologies. Companies are targeting these segments through customized AR modules, strategic alliances, and scalable pricing models to strengthen adoption across premium and mass-market vehicle categories.

• A 2026 automotive digital transformation survey indicated that over 55% of leading vehicle manufacturers expanded investment in AR interfaces, AI-enabled cockpit systems, and software-defined mobility solutions to support future vehicle platforms.

North America accounted for the largest market share at 37.8% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 25.1% between 2026 and 2033.

North America’s Automotive Augmented Reality Market is driven by strong adoption of connected vehicles, autonomous driving technologies, and next-generation digital cockpit platforms. The region accounted for 37.8% market share in 2025, supported by early integration of AR head-up displays, AI-enabled navigation, and advanced driver assistance visualization. More than 45% of premium vehicle platforms in the region include advanced cockpit technologies as manufacturers prioritize safety and immersive user experiences. Automakers and technology companies are expanding partnerships focused on AR software, semiconductor integration, and sensor-based mobility platforms. Increasing investments in autonomous vehicle testing and electric vehicle ecosystems are accelerating AR adoption across both passenger and future mobility applications.

United States Market Outlook: The United States leads regional deployment through strong automotive technology innovation, electric vehicle development, and autonomous mobility investments. Major automakers and technology providers are integrating AR displays with AI, cameras, and vehicle sensors to enhance driver interaction. Nearly 50% of premium vehicle launches include advanced digital interface technologies, reinforcing the country’s leadership in connected mobility solutions.

Europe’s Automotive Augmented Reality Market is supported by advanced automotive manufacturing, strict vehicle safety priorities, and strong demand for premium digital experiences. The region accounted for approximately 31.5% market share in 2025, led by integration of AR head-up displays and connected cockpit solutions across luxury vehicle platforms. Nearly 42% of premium models incorporate advanced visualization technologies to improve driver assistance and navigation accuracy. Automotive suppliers are strengthening AR development through display innovation, sensor fusion, and software-based vehicle platforms.

Germany Market Outlook: Germany dominates European adoption due to its premium automotive manufacturing ecosystem, advanced engineering capabilities, and strong investment in future mobility technologies. Vehicle manufacturers are deploying AR-enabled cockpits, intelligent displays, and autonomous-ready interfaces. More than 45% of luxury vehicle programs integrate advanced human-machine interface technologies, supporting Germany’s position in automotive digital innovation.

Asia-Pacific’s Automotive Augmented Reality Market is expanding through large-scale electric vehicle manufacturing, connected mobility adoption, and rapid advancement in automotive electronics. The region accounted for nearly 26.9% market share in 2025, supported by China, Japan, and South Korea’s strong automotive technology ecosystems. Around 40% of new premium electric vehicle platforms integrate advanced digital cockpit and AR-supported interface features. Manufacturers are increasing investment in display technologies, semiconductor partnerships, and AI-based mobility solutions to improve competitiveness.

China Market Outlook: China represents the strongest Asia-Pacific market due to its electric vehicle leadership, smart vehicle ecosystem, and expanding domestic automotive technology capabilities. Automakers are accelerating AR cockpit integration across intelligent EV platforms. Nearly 50% of new premium electric vehicles launched by leading manufacturers include advanced digital display systems, strengthening China’s role in next-generation mobility innovation.

South America’s Automotive Augmented Reality Market is developing through gradual adoption of connected vehicle technologies, premium automotive features, and increasing digital transformation across transportation systems. The region accounted for nearly 2.4% market share in 2025, with adoption concentrated among luxury and high-end vehicle categories. Approximately 22% of premium vehicle models include advanced cockpit or driver assistance visualization technologies. Limited affordability and slower technology penetration remain challenges, while automakers focus on selective AR deployment and scalable vehicle electronics solutions.

Brazil Market Outlook: Brazil leads regional adoption due to its established automotive production base, expanding connected vehicle ecosystem, and presence of global manufacturers. Automakers are introducing advanced infotainment, safety, and visualization features across selected vehicle categories. Nearly 30% of premium vehicle technology upgrades involve digital cockpit improvements, supporting gradual AR adoption in the country.

Middle East & Africa’s Automotive Augmented Reality Market is supported by premium vehicle demand, smart transportation projects, and increasing interest in advanced mobility technologies. The region accounted for approximately 1.4% market share in 2025, with deployment mainly concentrated across luxury vehicles and technology-focused automotive segments. Nearly 35% of premium vehicle imports feature advanced cockpit, driver assistance, or connected interface technologies. Automakers are introducing AR-enabled features through high-end vehicle portfolios and digital mobility strategies.

United Arab Emirates Market Outlook: The United Arab Emirates leads regional growth through smart city initiatives, high luxury vehicle penetration, and investments in intelligent transportation infrastructure. Automotive brands are expanding availability of vehicles equipped with AR displays and connected mobility systems. Nearly 40% of premium vehicles sold include advanced digital technologies, supporting adoption of immersive automotive solutions.

The Automotive Augmented Reality Market is led by Continental, Panasonic Automotive, Bosch, Harman International, and Hyundai Mobis, where established automotive technology suppliers compete with software innovators and display technology providers. The top five players collectively hold approximately 46% share, reflecting competition around AR processing capability, display quality, and vehicle integration expertise. Companies compete through visualization accuracy, software platforms, customization, and system reliability, with advanced AR HUD solutions improving driver response efficiency by nearly 25% and interface performance by around 30%. Market leaders are expanding through AI partnerships, semiconductor collaborations, product innovation, and integration with software-defined vehicle ecosystems. Competition is shifting toward immersive digital cockpits, sensor fusion, and predictive AR experiences. High development costs, automotive validation requirements, and software complexity create major entry barriers. Winning against established players requires strong automotive partnerships, advanced AR technology capability, and scalable vehicle integration expertise.

• Continental AG

• Panasonic Automotive Systems Co., Ltd.

• Robert Bosch GmbH

• Harman International Industries, Inc.

• Hyundai Mobis Co., Ltd.

• Visteon Corporation

• Nippon Seiki Co., Ltd.

• WayRay AG

• DigiLens Inc.

• Envisics Ltd.

• FICOSA International S.A.

• Texas Instruments Incorporated

• MicroVision, Inc.

Automotive augmented reality technologies are advancing through AR head-up displays, AI-powered visualization, sensor fusion, spatial computing, and next-generation human-machine interfaces. Current AR HUD systems integrate cameras, radar, LiDAR, and vehicle data to deliver real-time navigation and safety information. Nearly 45% of premium connected vehicle platforms are adopting AR-supported cockpit technologies.

Emerging solutions including holographic displays, AI-based object recognition, and cloud-connected AR platforms are improving driver interaction and autonomous readiness. Compared with conventional dashboard displays, AR-based interfaces improve information recognition by nearly 35% and reduce driver distraction by approximately 25%. Automakers, semiconductor providers, and software companies benefit from increasing demand for integrated digital mobility platforms.

From 2026 to 2028, disruptive technologies will focus on full-windshield AR displays, personalized digital environments, and autonomous vehicle visualization. Companies investing in scalable AR software, advanced optics, and computing platforms will gain competitive advantages as vehicles evolve into intelligent, connected ecosystems where immersive interaction becomes a core differentiator.

• January 2025 – Hyundai Mobis introduced next-generation holographic windshield display technology with ZEISS collaboration, enabling full-width AR visualization and improving driver information accessibility by nearly 30%. The advancement strengthened future smart cockpit and autonomous mobility capabilities. Source: mobis.co.kr

• April 2024 – Continental expanded its automotive display portfolio with advanced AR head-up display solutions, improving digital cockpit visualization performance by approximately 25%. The innovation enhanced connected vehicle interfaces and supported automaker transition toward software-defined mobility platforms. Source: continental.com

• January 2025 – Panasonic Automotive advanced its digital cockpit technologies with integrated display and connected vehicle solutions, improving human-machine interaction efficiency by nearly 20%. The development supported next-generation infotainment, safety, and immersive driving experiences. Source: panasonic-automotive.com

• May 2024 – Envisics accelerated development of dynamic holographic AR display technology for automotive applications, enhancing projection performance and field-of-view capabilities by approximately 30%. The initiative strengthened adoption opportunities across premium electric and autonomous vehicles. Source: envisics.com

The Automotive Augmented Reality Market Report provides detailed analysis of technology evolution, competitive positioning, adoption patterns, and strategic opportunities across the global automotive ecosystem. The report covers AR head-up displays, AR dashboards, navigation systems, infotainment solutions, and emerging immersive vehicle interface technologies across passenger vehicles, electric vehicles, autonomous platforms, and mobility applications.

The study evaluates regional developments across North America, Europe, Asia-Pacific, South America, and Middle East & Africa while examining supplier strategies, digital cockpit transformation, and technology integration trends. Nearly 50% of premium vehicle innovation programs are focused on connected interfaces and advanced visualization systems. The report supports investment planning, product development, partnership strategies, and competitive decision-making between 2026 and 2033.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 6,204.3 Million |

|

Market Revenue in 2033 |

USD 33,576.0 Million |

|

CAGR (2026 - 2033) |

23.5% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Continental AG, Panasonic Automotive Systems Co., Ltd., Robert Bosch GmbH, Harman International Industries, Inc., Hyundai Mobis Co., Ltd., Visteon Corporation, Nippon Seiki Co., Ltd., WayRay AG, DigiLens Inc., Envisics Ltd., FICOSA International S.A., Texas Instruments Incorporated, MicroVision, Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |