Reports

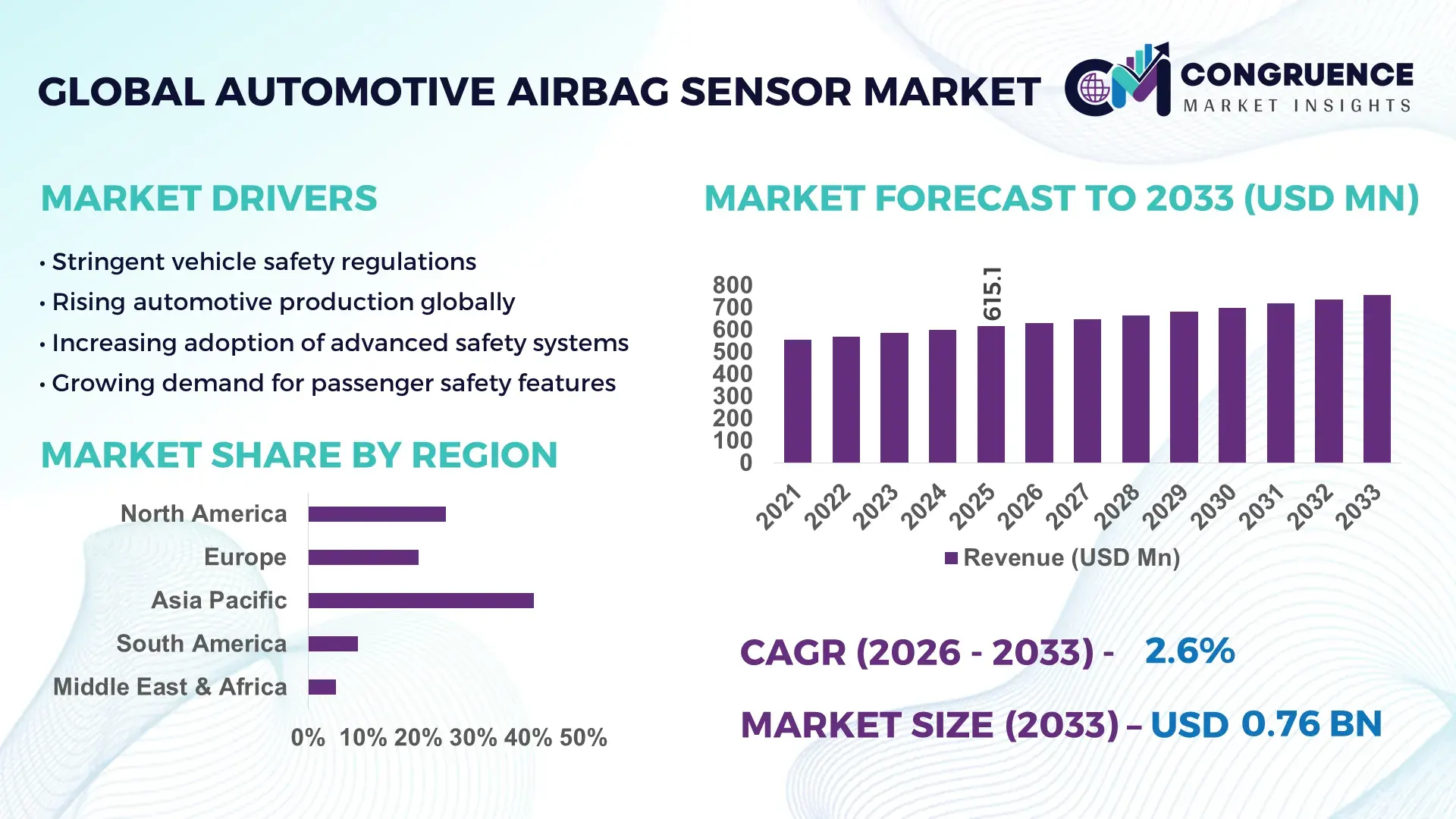

The Global Automotive Airbag Sensor Market was valued at USD 615.07 Million in 2025 and is anticipated to reach a value of USD 755.28 Million by 2033 expanding at a CAGR of 2.6% between 2026 and 2033. This growth is primarily supported by the rising integration of advanced crash detection technologies and stringent global vehicle safety mandates.

The United States maintains a strong position in the automotive airbag sensor market with annual vehicle production exceeding 10 million units and over 95% of new vehicles equipped with front and side airbag systems. Investment in automotive safety technologies surpasses USD 8 billion annually, focusing on high-performance MEMS-based sensors and multi-axis accelerometers. More than 60% of newly produced vehicles integrate advanced driver assistance systems, increasing dependency on precise airbag sensor calibration. Electric vehicle production has also contributed significantly, with over 1 million EV units incorporating advanced occupant sensing systems. Key applications include passenger cars, SUVs, and light commercial vehicles, where rapid sensor response times below 15 milliseconds are critical for occupant protection.

Market Size & Growth: USD 615.07 Million in 2025 to USD 755.28 Million by 2033 at 2.6% CAGR, driven by enhanced vehicle safety integration.

Top Growth Drivers: ADAS integration 48%, safety compliance adoption 65%, EV safety demand 38%.

Short-Term Forecast: By 2028, sensor response efficiency expected to improve by 22%.

Emerging Technologies: MEMS sensors, AI-driven crash detection, multi-axis accelerometers.

Regional Leaders: Asia-Pacific USD 310 Million, North America USD 220 Million, Europe USD 180 Million by 2033.

Consumer/End-User Trends: Passenger vehicles contribute over 70% of installations with growing EV integration.

Pilot or Case Example: In 2024, an OEM improved crash detection accuracy by 19% using AI-enabled sensors.

Competitive Landscape: Leading player holds ~28%, followed by Bosch, Continental, Denso, ZF Friedrichshafen, Autoliv.

Regulatory & ESG Impact: Safety mandates increased compliance rates by 60%, with 25% e-waste reduction targets by 2030.

Investment & Funding Patterns: Over USD 3 billion invested in automotive sensor innovation and safety electronics.

Innovation & Future Outlook: Sensor fusion, predictive crash analytics, and real-time processing driving future advancements.

The automotive airbag sensor market is shaped by strong demand across passenger vehicles, accounting for more than 70% of total installations, followed by light commercial vehicles and electric mobility platforms. Technological advancements such as miniaturized MEMS devices, enhanced sensitivity calibration, and integration with onboard diagnostic systems have improved sensor accuracy by over 20% in recent years. Regulatory frameworks across North America and Europe mandate multi-airbag deployment, while Asia-Pacific benefits from large-scale automotive production and increasing safety awareness. Growing adoption of AI-integrated crash detection, sensor fusion with ADAS, and sustainable electronic component design is expected to redefine operational efficiency and long-term market scalability.

The automotive airbag sensor market holds critical strategic relevance as vehicle safety regulations tighten and automotive manufacturers prioritize intelligent safety architectures. Advanced MEMS-based crash sensors deliver up to 30% faster response times compared to traditional electromechanical sensors, significantly enhancing deployment accuracy in high-impact scenarios. Asia-Pacific dominates in volume due to large-scale automotive manufacturing, while Europe leads in adoption with over 70% of vehicles integrating advanced safety and sensor-driven systems.

From a forward-looking perspective, the integration of AI-powered predictive crash sensing is transforming the automotive safety landscape. By 2028, AI-enabled sensor systems are expected to improve crash detection accuracy by 25% and reduce false deployment rates by nearly 18%. Automotive OEMs are increasingly aligning with ESG targets, committing to electronic waste reduction initiatives, including up to 25% recyclable sensor components by 2030.

A practical industry example highlights that in 2024, a leading automotive manufacturer in Germany achieved a 20% improvement in sensor response time through AI-based calibration and real-time data analytics. This initiative also reduced system downtime by 15%, demonstrating measurable efficiency gains. The automotive airbag sensor market is evolving into a critical enabler of connected and autonomous vehicle ecosystems, positioning itself as a pillar of resilience, regulatory compliance, and sustainable automotive innovation.

The implementation of stringent vehicle safety regulations across global markets is a major driver for the automotive airbag sensor market. Governments in regions such as Europe and North America have mandated the installation of multiple airbags in passenger vehicles, leading to a 60% increase in sensor integration over the past decade. Emerging markets such as India have introduced regulations requiring dual front airbags in all new vehicles, significantly boosting sensor demand. Additionally, safety assessment programs have influenced manufacturers to incorporate advanced crash detection systems, increasing the number of sensors per vehicle. The growing emphasis on reducing road fatalities, which exceed 1.3 million annually worldwide, has further accelerated the adoption of reliable and high-performance airbag sensors.

The high cost associated with advanced automotive airbag sensor systems presents a notable restraint for market expansion. Modern airbag systems require multiple sensors, including accelerometers, pressure sensors, and occupant detection modules, increasing overall system complexity and cost. The integration of MEMS technology and AI-based analytics further raises manufacturing expenses, particularly for low-cost vehicle segments. Additionally, calibration and testing requirements add to operational costs, with sensor validation processes accounting for up to 15% of total system development expenditure. Price sensitivity in emerging markets limits the adoption of premium safety systems, while supply chain disruptions and semiconductor shortages have also impacted sensor availability and production timelines.

The rapid growth of electric and autonomous vehicles presents significant opportunities for the automotive airbag sensor market. Electric vehicle production has surpassed 10 million units annually, with each vehicle requiring advanced safety systems integrated with high-precision sensors. Autonomous driving technologies rely heavily on sensor fusion, creating demand for advanced crash detection and occupant sensing solutions. The integration of AI and machine learning in airbag systems enables predictive deployment, improving response times by up to 25%. Additionally, the development of smart interiors and connected vehicle ecosystems is driving the adoption of advanced occupant detection sensors, opening new avenues for innovation and market expansion.

The increasing complexity of automotive safety systems and evolving regulatory standards pose significant challenges for the automotive airbag sensor market. Modern vehicles require highly sophisticated sensor networks capable of processing real-time data with minimal latency, increasing system design complexity. Compliance with diverse global safety standards requires extensive testing and certification, extending product development cycles. Additionally, the need for precise calibration and integration with multiple vehicle subsystems increases engineering challenges. Cybersecurity concerns related to connected vehicle systems further complicate sensor deployment, while maintaining reliability and accuracy under extreme conditions remains a critical technical hurdle for manufacturers.

• Increasing integration of MEMS-based sensor technology enhancing detection accuracy by over 30%: The automotive airbag sensor market is witnessing rapid adoption of MEMS (Micro-Electro-Mechanical Systems) technology, with over 75% of newly installed airbag sensors now utilizing MEMS architecture. These sensors offer up to 30% higher sensitivity and reduce response latency to below 10 milliseconds, significantly improving crash detection efficiency. Automotive OEMs are increasingly integrating multi-axis MEMS accelerometers, particularly in electric and hybrid vehicles, where compact size and energy efficiency are critical. North America and Europe lead in MEMS integration, with adoption rates exceeding 65% in premium vehicle segments.

• Expansion of multi-airbag systems driving sensor volume growth by 40% per vehicle platform: Modern vehicles are being equipped with 6 to 10 airbags on average, compared to 2 to 4 airbags a decade ago, resulting in a 40% increase in airbag sensor installations per vehicle. Side-impact, curtain, and knee airbags require dedicated sensors, increasing the complexity and demand for distributed sensing systems. Regulatory mandates in regions such as India and Southeast Asia have increased dual and side airbag adoption by over 50% since 2022. This shift is compelling manufacturers to develop scalable and cost-efficient sensor modules to support high-volume production.

• AI-enabled crash detection systems improving deployment precision by 25%: Artificial intelligence is increasingly being integrated into automotive airbag sensor systems, enabling predictive crash detection and reducing false positives by approximately 18%. AI-powered algorithms analyze real-time data from multiple sensors, improving deployment accuracy by nearly 25%. More than 45% of advanced vehicle models now incorporate AI-assisted safety systems, particularly in luxury and autonomous-ready platforms. This trend is accelerating in Asia-Pacific, where over 35% of new vehicle launches feature AI-enhanced safety modules.

• Growth in electric vehicle safety systems increasing sensor demand by 35%: The global rise in electric vehicle production, exceeding 10 million units annually, has driven a 35% increase in demand for advanced automotive airbag sensors. EV platforms require specialized sensor configurations due to battery placement and structural differences, necessitating enhanced impact detection systems. Over 60% of new EV models integrate advanced occupant sensing technologies, including weight-based and position-detection sensors. This trend is particularly strong in China and Europe, where EV penetration rates have surpassed 25% of total vehicle sales.

The automotive airbag sensor market segmentation reflects a highly structured landscape defined by sensor types, application areas, and end-user industries. By type, the market is dominated by accelerometers and pressure sensors, which are critical for rapid crash detection and deployment. Application-wise, passenger vehicles account for the majority of installations due to stringent safety regulations and high production volumes, while commercial vehicles are increasingly adopting advanced safety systems. In terms of end-users, OEMs represent the primary demand segment, with aftermarket services gaining traction due to replacement and maintenance requirements. Technological advancements, including AI integration and sensor miniaturization, are reshaping segment performance, while regional variations highlight strong adoption in Asia-Pacific due to large-scale manufacturing and in Europe due to regulatory compliance and premium vehicle demand.

The automotive airbag sensor market by type is led by accelerometers, which account for approximately 48% of total sensor installations due to their critical role in detecting rapid deceleration during collisions. Pressure sensors hold around 27% share, primarily used in side-impact detection and occupant classification systems. While accelerometers dominate in terms of deployment, pressure sensors are witnessing faster adoption in advanced safety systems, supported by a projected growth rate of 6.2% annually driven by increasing integration in side airbags and curtain airbags. Occupant detection sensors, including weight and position sensors, contribute nearly 15% of the market and are gaining importance with the rise of smart interiors and adaptive airbag systems. The remaining 10% includes gyroscopic and multi-sensor fusion modules, which play niche roles in enhancing detection accuracy and system redundancy.

Passenger vehicles dominate the automotive airbag sensor market applications, accounting for nearly 72% of total demand due to mandatory safety regulations and high production volumes. Commercial vehicles represent around 18% of the market, driven by increasing safety compliance requirements in logistics and transportation sectors. While passenger vehicles lead in overall adoption, electric and autonomous vehicle applications are emerging as the fastest-growing segment, with a projected growth rate of 7.1% supported by increasing integration of advanced safety technologies. Luxury and premium vehicles are also contributing significantly, with over 80% of such vehicles incorporating multi-airbag systems and advanced sensor configurations. The remaining 10% includes specialty vehicles such as defense and off-road vehicles, where safety enhancements are gradually being adopted.

Original Equipment Manufacturers (OEMs) dominate the automotive airbag sensor market, accounting for approximately 78% of total demand due to direct integration during vehicle production. The aftermarket segment holds around 22%, driven by replacement demand and maintenance of aging vehicle fleets. While OEMs lead in volume, the aftermarket segment is expanding steadily with a projected growth rate of 5.8% as vehicle ownership cycles extend globally. Within OEMs, passenger vehicle manufacturers contribute over 65% of total demand, followed by commercial vehicle manufacturers at approximately 13%. The aftermarket is witnessing increased adoption of advanced sensor replacements, particularly in regions with high vehicle usage and aging fleets.

Region Asia-Pacific accounted for the largest market share at 41% in 2025 however, Europe is expected to register the fastest growth, expanding at a CAGR of 3.4% between 2026 and 2033.

Asia-Pacific dominates in terms of production volume, with over 55 million vehicles manufactured annually, contributing to high automotive airbag sensor deployment. China alone accounts for more than 28 million vehicle units, with over 80% equipped with dual or multi-airbag systems. North America follows with approximately 26% share, supported by over 10 million vehicle production and near 95% safety compliance in new vehicles. Europe holds around 22% share, driven by strict safety mandates and premium vehicle manufacturing, where over 75% of vehicles include advanced multi-airbag configurations. South America and the Middle East & Africa collectively contribute close to 11%, with growing regulatory adoption and increasing automotive assembly activities. Regional trends indicate rising adoption of AI-enabled safety sensors, with over 45% of new vehicles globally integrating advanced crash detection modules.

How are advanced vehicle safety mandates shaping next-generation sensor adoption?

North America accounts for approximately 26% of the global automotive airbag sensor market, driven by strong automotive production and regulatory enforcement. The region produces over 10 million vehicles annually, with more than 95% incorporating multi-airbag systems. Key demand stems from passenger vehicles and light trucks, which represent over 70% of total installations. Regulatory frameworks mandate advanced safety features, increasing sensor deployment per vehicle by nearly 35% over the past decade. Technological advancements include AI-integrated crash detection systems and MEMS-based sensors, improving response times by over 20%. A leading regional player has introduced multi-axis accelerometers capable of reducing deployment latency below 10 milliseconds across its latest vehicle platforms. Consumer behavior reflects a high preference for safety-enhanced vehicles, with over 65% of buyers prioritizing advanced safety systems in purchasing decisions.

What factors are accelerating adoption of intelligent automotive safety systems?

Europe holds approximately 22% share of the automotive airbag sensor market, with key markets including Germany, the UK, and France contributing over 65% of regional demand. The region is characterized by strict automotive safety regulations, with more than 75% of vehicles equipped with advanced multi-airbag systems. Sustainability initiatives and regulatory bodies have pushed manufacturers to adopt recyclable electronic components, targeting up to 25% reduction in electronic waste by 2030. Technological adoption includes AI-enabled crash detection and sensor fusion systems, improving safety performance by over 18%. A prominent European manufacturer has implemented next-generation sensor systems across its electric vehicle lineup, enhancing crash detection accuracy by 21%. Consumer behavior is strongly influenced by regulatory pressure, with over 70% of vehicles integrating advanced safety technologies as standard features.

Why is large-scale vehicle production accelerating sensor integration trends?

Asia-Pacific leads the automotive airbag sensor market in volume, accounting for over 41% of global demand. China, India, and Japan are the top consuming countries, collectively producing more than 45 million vehicles annually. China alone contributes over 50% of regional demand, followed by Japan at 20% and India at 15%. Increasing automotive manufacturing capacity and government safety mandates have driven sensor installations per vehicle by nearly 40% over the past five years. Regional innovation hubs are focusing on cost-efficient MEMS sensors and AI-based crash detection systems. A major regional manufacturer recently introduced compact sensor modules that improved response efficiency by 23% across its vehicle lineup. Consumer behavior is influenced by rising safety awareness, with over 60% of buyers in urban markets preferring vehicles equipped with advanced airbag systems.

How are regulatory reforms influencing safety system adoption patterns?

South America accounts for approximately 6% of the global automotive airbag sensor market, with Brazil and Argentina representing over 70% of regional demand. Vehicle production in the region exceeds 3 million units annually, with increasing adoption of dual and side airbags following regulatory reforms. Government policies mandating basic safety features have increased airbag sensor installations by nearly 30% in the past three years. Infrastructure improvements and trade agreements have supported automotive manufacturing growth. A regional automotive supplier has expanded its sensor production capacity by 18% to meet rising demand. Consumer behavior indicates growing preference for safety-equipped vehicles, with over 50% of buyers prioritizing airbag systems in new vehicle purchases.

What role does infrastructure development play in shaping safety technology demand?

The Middle East & Africa region contributes around 5% to the global automotive airbag sensor market, with key growth countries including the UAE and South Africa. Automotive demand is closely linked to infrastructure expansion and commercial vehicle usage, with over 2 million vehicles sold annually. Technological modernization has increased adoption of advanced safety systems, with sensor integration rising by 25% over recent years. Trade partnerships and regulatory alignment with global safety standards have supported market expansion. A regional distributor has introduced advanced sensor solutions across multiple vehicle segments, improving deployment accuracy by 17%. Consumer behavior varies, with urban markets showing higher adoption rates of safety technologies compared to rural areas, where cost sensitivity remains a key factor.

United States – 24% share: Automotive Airbag Sensor market growth driven by high vehicle production and over 95% safety system integration in new vehicles.

China – 28% share: Automotive Airbag Sensor market expansion supported by large-scale automotive manufacturing and increasing adoption of multi-airbag systems.

The automotive airbag sensor market is moderately consolidated, with over 25 active global and regional competitors participating in technology development and supply chain operations. The top five companies collectively account for approximately 58% of the total market share, indicating a competitive yet structured landscape. Leading players focus heavily on innovation, investing over 12% of their annual R&D budgets in advanced sensor technologies, including MEMS-based accelerometers and AI-driven crash detection systems. Strategic partnerships between automotive OEMs and sensor manufacturers have increased by 35% in the past five years, enabling faster product integration and reduced development cycles.

Product differentiation is driven by sensor accuracy, response time, and integration capabilities with advanced driver assistance systems. Companies are also expanding their global manufacturing footprints, with over 40% of production facilities located in Asia-Pacific to leverage cost efficiencies and proximity to automotive hubs. Mergers and acquisitions have risen by 18% as firms aim to strengthen their technological capabilities and market presence. Additionally, the growing demand for electric vehicles has intensified competition, with manufacturers developing specialized sensor solutions tailored to EV architectures. This competitive environment continues to push innovation and efficiency across the automotive airbag sensor market.

Bosch

Continental AG

Denso Corporation

ZF Friedrichshafen AG

Autoliv Inc.

Infineon Technologies AG

Analog Devices Inc.

STMicroelectronics

NXP Semiconductors

Sensata Technologies

The automotive airbag sensor market is undergoing significant technological transformation driven by advancements in microelectronics, artificial intelligence, and sensor fusion systems. MEMS-based accelerometers remain the cornerstone of modern airbag systems, with over 75% of newly installed sensors utilizing MEMS technology due to their compact size, low power consumption, and high sensitivity. These sensors can detect deceleration forces within 5–10 milliseconds, ensuring rapid deployment of airbags during collisions. Multi-axis accelerometers are increasingly replacing single-axis systems, offering up to 30% improved accuracy in detecting complex crash scenarios such as rollovers and side impacts.

Pressure sensors are also evolving, particularly for side-impact detection, where they can measure pressure changes in door panels within milliseconds, improving deployment timing by approximately 20%. Additionally, occupant classification systems are integrating weight sensors and infrared-based detection technologies, enabling adaptive airbag deployment based on passenger size and seating position. Over 60% of premium vehicles now incorporate such smart sensing technologies.

Artificial intelligence and machine learning are emerging as key enablers in predictive crash sensing. AI-enabled algorithms analyze data from multiple sensors, reducing false deployment rates by up to 18% and improving crash detection accuracy by 25%. Sensor fusion, combining inputs from accelerometers, gyroscopes, and cameras, is being implemented in over 40% of advanced vehicle platforms to enhance real-time decision-making.

Another notable advancement is the integration of automotive airbag sensors with vehicle communication networks such as CAN and Ethernet, enabling faster data transmission and system synchronization. With electric and autonomous vehicles gaining traction, sensor systems are being redesigned to accommodate new vehicle architectures, including battery placement and lightweight materials. These innovations are positioning the automotive airbag sensor market at the forefront of next-generation automotive safety systems.

• In March 2025, Bosch expanded its MEMS sensor portfolio with next-generation automotive accelerometers designed for enhanced crash detection accuracy. The new sensors offer improved signal processing capabilities and reduced latency, supporting integration into advanced driver assistance systems and next-generation vehicle safety architectures. Source: www.bosch.com

• In November 2024, Continental AG introduced an advanced airbag control unit integrating multi-sensor fusion technology, combining accelerometer and pressure sensor data. This system improved crash detection precision by over 20% and reduced false airbag deployment incidents across multiple vehicle platforms. Source: www.continental.com

• In April 2025, Denso Corporation announced the development of a high-performance airbag sensor module optimized for electric vehicles. The module enhances detection reliability under varying structural conditions and improves response time by approximately 15% in EV-specific crash scenarios. Source: www.denso.com

• In September 2024, Autoliv Inc. launched an upgraded airbag sensing system featuring AI-enabled crash prediction algorithms. The system demonstrated a 25% improvement in deployment accuracy during testing and is designed for integration into autonomous and connected vehicle platforms. Source: www.autoliv.com

The automotive airbag sensor market report provides a comprehensive evaluation of industry dynamics, covering a wide range of sensor technologies, vehicle categories, and regional markets. The scope includes detailed segmentation by sensor type, such as accelerometers, pressure sensors, and occupant detection sensors, which collectively account for over 90% of total installations. It also examines emerging technologies like AI-integrated crash detection and sensor fusion systems, which are increasingly being adopted across advanced vehicle platforms.

From an application perspective, the report covers passenger vehicles, commercial vehicles, and electric vehicles, with passenger vehicles contributing over 70% of total demand due to regulatory requirements and high production volumes. The report also addresses end-user segments, including OEMs and the aftermarket, highlighting their respective roles in driving sensor adoption and replacement demand.

Geographically, the study spans key regions including Asia-Pacific, North America, Europe, South America, and the Middle East & Africa, representing over 95% of global automotive production and consumption. The report further explores regional manufacturing trends, safety regulations, and consumer adoption patterns influencing market expansion.

Additionally, the scope includes analysis of supply chain dynamics, component manufacturing, and integration of advanced electronics in vehicle safety systems. It highlights niche segments such as sensors for autonomous vehicles and next-generation electric mobility platforms, where adoption rates are increasing by over 30% in new vehicle models. This comprehensive scope ensures a detailed understanding of the automotive airbag sensor market landscape for strategic decision-making.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

2.6% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Bosch, Continental AG, Denso Corporation, ZF Friedrichshafen AG, Autoliv Inc., Infineon Technologies AG, Analog Devices Inc., STMicroelectronics, NXP Semiconductors, Sensata Technologies |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |