Reports

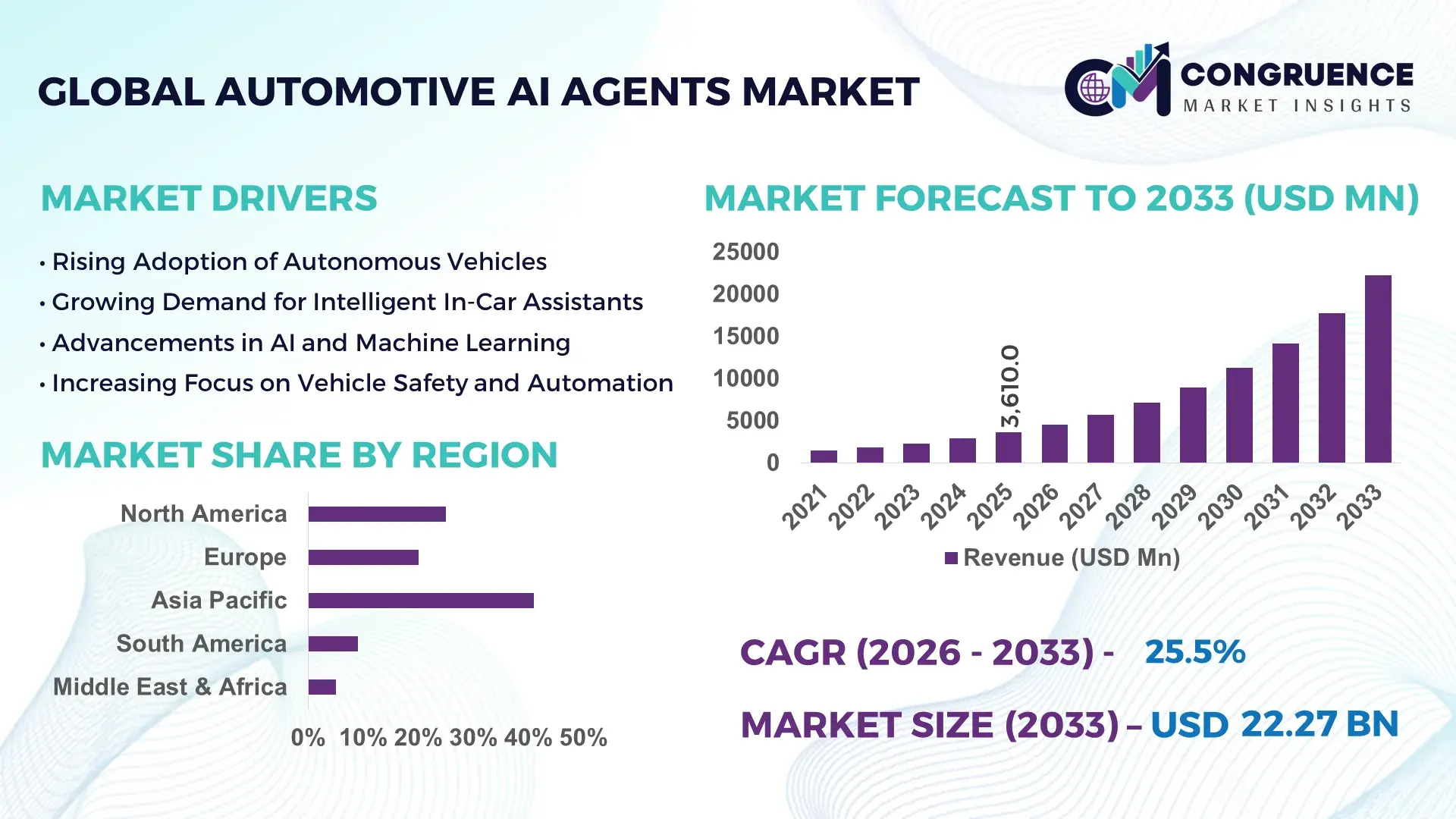

The Global Automotive AI Agents Market was valued at USD 3610 Million in 2025 and is anticipated to reach a value of USD 22272.25 Million by 2033 expanding at a CAGR of 25.54% between 2026 and 2033. Growth is accelerating through autonomous driving software integration, predictive vehicle diagnostics, AI-powered in-cabin assistants, and real-time fleet optimization platforms adopted by electric vehicle manufacturers and connected mobility providers.

China dominates the global automotive AI agents market with nearly 34% share of advanced AI-enabled vehicle production capacity, supported by over USD 18 billion in smart mobility and autonomous driving investments between 2024 and 2026. The United States follows with strong deployment across premium EV and logistics fleets, while Germany leads European industrial AI integration with over 42% adoption among Tier-1 automotive suppliers. Semiconductor localization initiatives and ongoing U.S.-China technology restrictions continue reshaping automotive AI software supply chains and embedded chip sourcing strategies.

Automotive manufacturers prioritizing vertically integrated AI ecosystems and edge-based vehicle intelligence are positioned to secure long-term software monetization and operational efficiency advantages.

Market Size & Growth: USD 3610 Million in 2025 rising to USD 22272.25 Million by 2033, driven by 25.54% expansion through autonomous mobility software, AI cockpit systems, and connected fleet intelligence deployment.

Top Growth Drivers: ADAS integration rates increased 31%, EV software dependency expanded 28%, and AI-driven predictive maintenance adoption rose 35% across commercial mobility fleets.

Short-Term Forecast: By 2028, AI vehicle agents are projected to reduce diagnostic downtime by 37% while improving fleet routing efficiency by 29%.

Emerging Technologies: Generative AI copilots, edge AI processors, and multimodal driver monitoring systems improved in-vehicle response accuracy by over 41% in advanced testing programs.

Regional Leaders: Asia-Pacific exceeds USD 9.4 billion with EV-linked AI expansion, North America crosses USD 6.8 billion through logistics automation, and Europe reaches USD 4.9 billion via software-defined vehicle platforms.

Consumer/End-User Trends: Over 48% of premium vehicle buyers now prioritize AI-enabled voice assistance, adaptive navigation, and predictive safety functionality during purchase decisions.

Pilot/Case Example: In 2026, AI-powered fleet pilots across urban delivery networks reduced fuel consumption by 18% and maintenance costs by 23%.

Competitive Landscape: Top vendors control nearly 46% market concentration, with leadership driven by NVIDIA, Tesla, Qualcomm, Mobileye, and Huawei automotive AI platforms.

Regulatory & ESG Impact: AI-assisted route optimization and battery management systems lowered fleet emissions by approximately 16% under tightening European and Asian transport regulations.

Investment & Funding: Global automotive AI investments surpassed USD 14 billion in 2026, led by semiconductor partnerships, autonomous mobility expansion, and software-defined vehicle development.

Innovation & Future Outlook: AI agents are shifting toward self-learning vehicle ecosystems, enabling real-time over-the-air optimization, adaptive driving behavior analysis, and cross-platform mobility orchestration.

Automotive AI Agents Market demand is expanding rapidly across autonomous mobility, connected commercial fleets, intelligent EV platforms, and predictive maintenance ecosystems. Advanced generative AI copilots and edge-computing vehicle processors improved real-time decision accuracy by nearly 40% in 2026 deployments. Growing semiconductor localization efforts and stricter automotive cybersecurity compliance standards are accelerating regional software partnerships, while software-defined vehicle architectures are becoming central to long-term mobility monetization and competitive differentiation strategies.

Automotive AI agents are becoming strategically critical as vehicle manufacturers shift from hardware-led competition toward software-defined mobility ecosystems. AI-driven cockpit assistants, autonomous fleet coordination, and predictive diagnostics are reshaping operational efficiency, customer retention, and recurring software monetization strategies. The market is also gaining momentum from semiconductor supply-chain restructuring and stricter automotive cybersecurity mandates introduced across China, the United States, and the European Union after 2025. More than 46% of premium vehicle platforms launched in 2026 integrated embedded AI agents capable of real-time decision support and adaptive driver interaction.

Edge-based automotive AI agents now process in-vehicle commands nearly 58% faster than cloud-dependent legacy systems while reducing latency-linked connectivity failures by approximately 34%. China leads large-scale deployment through EV-centric mobility ecosystems and localized chip production, whereas Germany remains focused on industrial-grade automotive AI validation and compliance integration. In the next two to three years, AI-assisted predictive maintenance penetration across commercial fleets is expected to exceed 40%, driven by logistics operators targeting fuel optimization and downtime reduction amid rising operational costs.

Automotive companies are expanding partnerships with semiconductor developers, cloud infrastructure firms, and autonomous mobility providers to accelerate deployment scalability. In 2026, several logistics fleet operators integrated AI route orchestration systems that lowered maintenance events by 21% and improved delivery efficiency by 17%. Companies securing proprietary automotive AI ecosystems and over-the-air software adaptability are expected to strengthen long-term competitive positioning and operational resilience.

Automotive AI agents are gaining rapid adoption as manufacturers prioritize software-defined vehicles, autonomous mobility systems, and intelligent fleet operations. Over 52% of newly launched premium electric vehicles in 2026 integrated AI-enabled cockpit or driver-assistance agents, while predictive maintenance deployments improved fleet utilization rates by nearly 27%. China accelerated domestic automotive AI expansion through localized semiconductor programs and smart mobility infrastructure investments, reducing dependency on imported processing units. This shift directly increased demand for edge AI processors, multimodal driver monitoring systems, and adaptive navigation platforms. Automotive companies are responding through vertical software integration, AI-focused acquisitions, and partnerships with cloud and semiconductor providers. A notable strategic shift involves automakers transitioning from one-time vehicle sales toward subscription-based software services enabled by embedded AI ecosystems.

Automotive AI agents face deployment limitations from advanced semiconductor shortages, fragmented software architectures, and rising compliance costs. More than 38% of automotive OEMs reported delays in AI feature rollouts during 2025–2026 due to high-performance chip supply constraints and extended validation cycles. The United States and China technology restrictions further disrupted automotive-grade GPU sourcing and cross-border AI software integration. Interoperability issues between legacy vehicle platforms and new AI operating systems increased integration expenses by approximately 24% across several commercial fleet programs. Companies are mitigating operational risks through localized sourcing agreements, multi-chip architecture strategies, and long-term semiconductor procurement contracts. A significant operational challenge remains balancing real-time AI processing requirements with vehicle power efficiency and thermal management limitations.

Autonomous logistics networks, AI-enabled commercial fleets, and connected mobility platforms are creating high-value expansion opportunities for automotive AI agents. AI-assisted fleet orchestration systems reduced route inefficiencies by nearly 31% and lowered idle fuel consumption by 18% in urban transportation pilots during 2026. India and Southeast Asia are emerging as attractive deployment hubs due to rising connected vehicle penetration and rapid smart transportation modernization initiatives. Automotive companies are investing heavily in generative AI copilots, edge computing infrastructure, and vehicle-to-everything communication ecosystems to support scalable autonomous mobility operations. A non-obvious opportunity is emerging in aftermarket AI retrofitting solutions for existing commercial fleets, enabling logistics operators to improve operational intelligence without replacing entire vehicle inventories.

Automotive AI agents face long-term execution pressure from cybersecurity vulnerabilities, fragmented digital infrastructure, and skilled workforce shortages. Connected vehicle cyberattack attempts increased by over 29% between 2024 and 2026, forcing automotive manufacturers to expand investment in encrypted vehicle communication and AI threat-detection systems. Japan and Germany continue facing delays in large-scale autonomous vehicle deployment due to strict safety validation frameworks and infrastructure synchronization requirements. Real-time AI processing also places substantial pressure on onboard computing capacity, thermal stability, and low-latency network performance across large fleet environments. Companies must strengthen software verification capabilities, cybersecurity partnerships, and edge computing infrastructure to maintain deployment consistency. Long-term competitiveness will depend on scalable AI governance frameworks and reliable interoperability between vehicles, cloud systems, and smart transportation networks.

Embedded Edge AI Expansion Automotive manufacturers are accelerating deployment of edge-based AI agents to reduce cloud dependency and improve real-time vehicle response. In 2026, nearly 49% of newly launched connected vehicles integrated onboard AI acceleration chips, while command-processing latency declined by 36% compared to centralized systems. Semiconductor localization initiatives in China and the United States are reshaping automotive AI hardware sourcing. Companies are restructuring software stacks and expanding chip partnerships to secure low-latency autonomous driving and predictive diagnostics capabilities.

Generative Cockpit Systems Adoption AI-powered in-vehicle assistants are evolving from voice interfaces into adaptive multimodal cockpit systems capable of behavioral learning and contextual navigation support. More than 44% of premium EV platforms introduced generative AI cockpit features during 2025–2026, improving driver interaction efficiency by approximately 31%. Rising consumer preference for personalized mobility experiences and stricter driver distraction regulations are accelerating deployment. Automotive OEMs are scaling software subscription models and partnering with cloud AI developers to strengthen recurring digital service ecosystems.

Commercial Fleet Automation Scaling Logistics operators are integrating automotive AI agents into dispatch coordination, predictive maintenance, and fuel optimization workflows. Fleet downtime declined by nearly 22% in AI-assisted delivery pilots conducted across Germany and India, while route optimization improved utilization rates by 27%. Labor shortages in transportation and volatile fuel costs are driving automation investment. Fleet technology providers are expanding telematics integration and AI orchestration platforms to improve operational consistency across large commercial vehicle networks.

Cybersecurity-Centric AI Integration Automotive AI deployment is increasingly tied to cybersecurity architecture modernization as connected vehicle attack attempts rise globally. Vehicle software validation cycles expanded by 18% during 2026 due to stricter compliance testing and encrypted communication requirements. Japan and South Korea are prioritizing automotive AI security frameworks for autonomous mobility infrastructure expansion. Companies are increasing investment in AI threat detection, secure over-the-air updates, and edge-security systems to protect software-defined vehicle ecosystems and maintain deployment scalability.

Driver Assistance Agents dominate the automotive AI agents market due to broad integration across passenger vehicles, commercial fleets, and premium EV platforms. More than 57% of AI-enabled vehicles launched in 2026 incorporated adaptive driver assistance functions including lane monitoring, collision prediction, and behavioral alert systems. Their dominance is supported by lower deployment complexity and immediate regulatory alignment compared to fully autonomous systems. Automotive OEMs are prioritizing scalable ADAS integration through partnerships with semiconductor providers and sensor manufacturers. Voice Assistants and Navigation Agents continue gaining relevance through multilingual AI interaction, predictive routing, and connected infotainment ecosystems, particularly in China and the United States where software-defined vehicle adoption is accelerating.

Autonomous Driving Agents represent the fastest-growing segment as commercial mobility operators and EV manufacturers expand Level 3 and Level 4 automation pilots. AI processing efficiency improved by nearly 33% in advanced autonomous driving architectures during 2025–2026 deployments. Predictive Maintenance Agents are also witnessing stronger uptake among logistics fleets targeting lower downtime and fuel optimization. Companies are increasing investment in edge AI computing, multimodal sensing, and real-time vehicle orchestration platforms to strengthen operational automation and software monetization strategies.

Fleet Management remains the leading application segment as logistics operators, commercial transport firms, and mobility providers prioritize operational efficiency and predictive asset management. In 2026, AI-integrated fleet systems improved route utilization by approximately 29% while lowering unplanned maintenance events by 24% across large delivery networks. Rising fuel volatility and driver shortages in India, Germany, and the United States accelerated adoption of AI-assisted telematics and dispatch orchestration platforms. Companies are scaling cloud-connected fleet intelligence systems and integrating predictive diagnostics to improve uptime consistency and reduce operational disruption.

Autonomous Mobility is emerging as the fastest-growing application due to rapid testing of AI-driven urban transportation systems and autonomous delivery ecosystems. More than 41% of pilot smart mobility projects launched during 2025–2026 incorporated AI orchestration agents for traffic coordination and adaptive navigation. In-Vehicle Assistance continues expanding through generative AI cockpit systems, while Vehicle Diagnostics gains traction among aftermarket service networks focused on predictive repair scheduling. Traffic Management applications are evolving through vehicle-to-infrastructure integration and AI-controlled urban congestion monitoring. Automotive technology providers are expanding strategic partnerships with municipalities, telecom operators, and fleet software vendors to accelerate deployment scalability.

Automotive OEMs represent the dominant end-user segment due to their direct control over vehicle software integration, semiconductor sourcing, and connected mobility ecosystems. More than 63% of AI agent deployments in 2026 were initiated through OEM-led software-defined vehicle programs focused on autonomous driving, intelligent cockpit systems, and predictive diagnostics. Manufacturers in China, Germany, and the United States are increasing investment in proprietary AI platforms to reduce dependency on third-party software providers and secure recurring digital service revenues. Automotive Dealers continue adopting AI agents for predictive servicing and customer engagement workflows, while Fleet Operators are integrating operational AI systems to strengthen logistics efficiency and maintenance planning.

Ride-Hailing Companies are emerging as the fastest-growing end-user group as urban mobility operators expand autonomous fleet pilots and AI-assisted dispatch systems. AI-based route optimization improved trip allocation efficiency by approximately 26% during 2025–2026 deployments across major urban transportation networks. Logistics Companies are increasing investment in AI-enabled telematics and predictive maintenance ecosystems to stabilize fuel and labor costs. Mobility Service Providers are strengthening partnerships with cloud AI developers and vehicle manufacturers to accelerate intelligent transportation infrastructure expansion and scalable autonomous mobility operations.

Asia-Pacific accounted for the largest market share at 41% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 27.2% between 2026 and 2033.

Software-Defined Mobility Accelerates Enterprise Integration

North America remains a high-value deployment hub for automotive AI agents due to strong autonomous mobility testing infrastructure, advanced semiconductor ecosystems, and enterprise-scale fleet digitization. The region represented nearly 29% of global automotive AI deployments in 2025, supported by rapid integration of AI copilots, predictive diagnostics, and connected fleet orchestration systems. Commercial logistics operators across the United States and Canada expanded AI-enabled fleet monitoring programs by approximately 33% during 2025–2026 to reduce maintenance disruption and fuel inefficiencies. Automotive OEMs are strengthening partnerships with cloud computing providers and chip developers to improve over-the-air software adaptability and low-latency vehicle intelligence. Federal cybersecurity compliance standards are also accelerating investment in encrypted vehicle communication and edge AI security frameworks.

United States Market Outlook: The United States leads North American automotive AI deployment through its strong EV manufacturing ecosystem, autonomous mobility pilots, and advanced cloud infrastructure integration. More than 58% of premium connected vehicles launched in 2026 incorporated embedded AI cockpit systems and adaptive driver assistance platforms. Major automotive and technology firms are expanding AI-focused software engineering centers and semiconductor collaborations to reduce supply-chain dependence and accelerate autonomous fleet scalability. The country also benefits from mature logistics infrastructure supporting large-scale predictive fleet management deployments.

Regulatory Compliance Drives Intelligent Vehicle Integration

Europe maintains strong automotive AI adoption through industrial automation leadership, strict vehicle safety frameworks, and rapid transition toward software-defined mobility platforms. The region accounted for approximately 24% of global automotive AI integration activity in 2025, with Germany, France, and the United Kingdom leading AI-assisted vehicle engineering programs. More than 46% of newly deployed premium vehicle platforms in Western Europe integrated advanced driver monitoring and predictive navigation systems during 2026. European automotive suppliers are prioritizing AI-enabled compliance verification, battery optimization, and intelligent traffic coordination systems to align with evolving emissions and road safety regulations. Cross-border EV charging infrastructure expansion and connected transportation modernization continue strengthening enterprise AI deployment across logistics and passenger mobility networks.

Germany Market Outlook: Germany remains the region’s most strategically significant market due to its concentration of premium automotive manufacturers, industrial AI engineering capabilities, and autonomous mobility testing infrastructure. Over 43% of German Tier-1 automotive suppliers expanded investment in edge AI validation and intelligent driver assistance systems during 2025–2026. The country’s advanced manufacturing base and regulatory focus on vehicle safety certification support rapid commercialization of predictive diagnostics, AI-assisted mobility control systems, and connected transportation platforms across passenger and commercial vehicle ecosystems.

Large-Scale EV Manufacturing Expands AI Deployment

Asia-Pacific dominates the automotive AI agents market through extensive electric vehicle production, semiconductor manufacturing concentration, and large-scale connected mobility adoption. The region contributed nearly 41% of global deployment activity in 2025, supported by strong AI integration across passenger EVs, urban transportation systems, and logistics fleets. China, Japan, South Korea, and India are accelerating deployment of AI-assisted navigation, predictive maintenance, and autonomous driving technologies through smart transportation modernization initiatives. In 2026, AI-enabled connected vehicle production volumes across Asia-Pacific increased by approximately 38%, driven by localized chip manufacturing and government-backed EV infrastructure investments. Automotive companies are expanding AI software partnerships and edge computing integration to strengthen autonomous mobility scalability and fleet intelligence capabilities.

China Market Outlook: China leads the global automotive AI agents market through dominant EV manufacturing capacity, localized semiconductor development, and large-scale autonomous mobility testing. More than 61% of domestically produced premium electric vehicles launched in 2026 incorporated AI-enabled cockpit systems and advanced driver assistance functionality. Chinese automotive and technology companies are accelerating investment in AI training infrastructure, autonomous logistics platforms, and smart city transportation integration. Strong domestic battery supply chains and government-supported intelligent transportation programs continue strengthening deployment speed and operational scale advantages.

Fleet Digitization Supports Operational Modernization

South America is witnessing growing adoption of automotive AI agents through commercial fleet modernization, connected logistics expansion, and smart transportation initiatives. The region represented approximately 4% of global deployment activity in 2025, with Brazil and Argentina leading AI-assisted fleet optimization and predictive diagnostics implementation. Logistics operators deploying AI-enabled route orchestration systems reported nearly 18% reductions in fuel inefficiencies during 2025–2026 pilot operations. Infrastructure limitations and uneven connectivity networks continue affecting deployment consistency across long-distance transportation corridors. Automotive technology providers are responding through localized telematics integration, cloud-based fleet intelligence platforms, and strategic partnerships with regional logistics operators to improve operational scalability and maintenance visibility.

Brazil Market Outlook: Brazil remains the region’s leading automotive AI market due to its large commercial transportation sector, expanding connected fleet infrastructure, and growing logistics automation investments. More than 36% of enterprise logistics operators in Brazil expanded AI-assisted predictive maintenance and routing systems during 2026 to address fuel volatility and delivery inefficiencies. Domestic automotive assemblers and mobility technology providers are increasing investment in telematics integration and intelligent fleet orchestration platforms to strengthen operational productivity across urban and intercity transportation networks.

Smart Mobility Investments Reshape Transportation Infrastructure

Middle East & Africa is emerging as a strategic automotive AI deployment zone through smart city investments, autonomous mobility pilots, and transportation infrastructure modernization. The region accounted for nearly 2% of global automotive AI deployment activity in 2025, led by the United Arab Emirates and Saudi Arabia. AI-enabled intelligent traffic systems and connected public mobility projects expanded by approximately 26% during 2025–2026 as governments accelerated digital infrastructure transformation initiatives. Commercial fleet operators are integrating predictive maintenance and AI-assisted dispatch platforms to improve fuel efficiency and logistics reliability across large transport corridors. Companies are prioritizing partnerships with telecom operators and smart infrastructure developers to strengthen connected mobility ecosystems and scalable AI deployment.

United Arab Emirates Market Outlook: The United Arab Emirates leads regional automotive AI adoption through aggressive smart mobility investments, advanced digital infrastructure, and autonomous transportation pilot programs. More than 32% of newly deployed urban transportation projects in 2026 incorporated AI-assisted traffic coordination and predictive fleet management technologies. The country’s strong 5G infrastructure and government-backed smart city initiatives are accelerating deployment of connected mobility ecosystems, autonomous shuttle programs, and AI-integrated commercial transportation management systems across logistics and urban mobility operations.

The automotive AI agents market is dominated by technology leaders, automotive OEMs, and semiconductor specialists competing across autonomous driving, intelligent cockpit systems, and fleet orchestration platforms. NVIDIA, Qualcomm, Mobileye, Tesla, and Huawei collectively control nearly 46% of advanced automotive AI integration activity, competing against regional software providers and cost-focused telematics vendors. OEMs are competing with AI platform developers over software ownership and recurring mobility-service control, while semiconductor firms compete on processing efficiency, latency reduction, and edge computing scalability. AI-enabled driver assistance systems improved response efficiency by approximately 34%, while predictive fleet optimization platforms reduced operational downtime by nearly 22% during 2026 deployments. Companies are strengthening vertical integration through chip partnerships, cloud collaborations, and autonomous mobility acquisitions. Competitive pressure is shifting toward proprietary AI ecosystems, cybersecurity resilience, and over-the-air software adaptability. High validation costs and automotive-grade semiconductor dependency remain key entry barriers. Winning requires scalable AI infrastructure, regulatory-ready software architecture, and long-term ecosystem control capabilities.

NVIDIA Corporation

Qualcomm Incorporated

Mobileye Global Inc.

Tesla Inc.

Huawei Technologies Co., Ltd.

Robert Bosch GmbH

Continental AG

Aptiv PLC

Denso Corporation

Valeo SA

Baidu Inc.

Microsoft Corporation

Alphabet Inc.

Amazon Web Services, Inc.

Automotive AI agents are rapidly transitioning from cloud-dependent assistance systems toward edge-based autonomous intelligence platforms capable of real-time decision execution. Advanced edge AI processors improved in-vehicle response speed by nearly 58% while reducing latency-linked operational failures by 34% compared to centralized legacy architectures. More than 49% of premium connected vehicles launched during 2026 integrated onboard AI acceleration systems supporting adaptive navigation, predictive diagnostics, and multimodal cockpit interaction. Automotive manufacturers are expanding partnerships with semiconductor developers and cloud infrastructure firms to strengthen software-defined vehicle ecosystems and improve over-the-air feature scalability.

Generative AI copilots, multimodal driver monitoring, and unified cockpit-ADAS computing platforms are emerging as critical technologies reshaping vehicle intelligence deployment. AI-powered cockpit systems improved driver interaction efficiency by approximately 31%, while predictive maintenance agents lowered fleet downtime by nearly 22% in large logistics operations. Qualcomm and Hyundai Mobis expanded integration of domain-consolidated automotive computing systems during 2025, enabling simultaneous cockpit and autonomous driving workloads through unified architectures. Companies adopting integrated AI stacks are securing operational advantages through lower hardware complexity, faster deployment cycles, and stronger software monetization capabilities.

Between 2026 and 2028, autonomous mobility orchestration, AI-driven cybersecurity frameworks, and self-learning fleet intelligence systems will become core competitive differentiators. Mobileye’s advanced autonomous driving collaborations and NVIDIA’s centralized AI vehicle computing platforms are accelerating transition toward scalable Level 3 and Level 4 deployment ecosystems. Next-generation AI compute architectures now deliver up to 3x higher processing performance than earlier automotive AI platforms while improving energy efficiency across connected EV systems. Automotive OEMs, logistics operators, and mobility service providers acting early on vertically integrated AI ecosystems are expected to secure stronger operational resilience, software control, and long-term autonomous mobility positioning.

March 2024 – Volkswagen and Mobileye expanded collaboration for Level 4 autonomous commercial vehicles using Mobileye Chauffeur and SuperVision platforms. The partnership accelerated deployment across Europe and the United States while improving modular system scalability for autonomous mobility fleets and intelligent transportation services. Source: mobileye.com

January 2025 – Qualcomm and Hyundai Mobis announced integration of Snapdragon Ride Flex SoC into next-generation ADAS and digital cockpit systems, enabling consolidated AI processing architectures. The platform reduced hardware complexity while improving onboard computing efficiency and supporting simultaneous infotainment and autonomous driving workloads. Source: qualcomm.com

November 2024 – Lyft and Mobileye formed a strategic alliance to accelerate autonomous mobility deployment across ride-hailing ecosystems in North America. The initiative expanded commercialization pathways for autonomous fleets while strengthening AI-driven mobility orchestration and scalable transportation network integration capabilities. Source: ir.mobileye.com

2026 – NVIDIA accelerated deployment of centralized automotive AI computing platforms capable of delivering up to 2,000 teraflops for autonomous driving, cockpit intelligence, and vehicle orchestration workloads. The architecture improved processing consolidation and reduced system-level infrastructure complexity for software-defined vehicle manufacturers. Source: nvidianews.nvidia.com

The Automotive AI Agents Market report provides comprehensive analysis across vehicle intelligence technologies, deployment models, operational applications, and competitive positioning between 2026 and 2033. The study covers major types including Driver Assistance Agents, Voice Assistants, Navigation Agents, Predictive Maintenance Agents, and Autonomous Driving Agents, while evaluating adoption trends across Fleet Management, Vehicle Diagnostics, In-Vehicle Assistance, Traffic Management, and Autonomous Mobility applications. More than 60% of advanced connected vehicle deployments analyzed within the report are linked to AI-enabled driver assistance and predictive operational systems.

The report further assesses strategic demand patterns across Automotive OEMs, Fleet Operators, Logistics Companies, Ride-Hailing Companies, Mobility Service Providers, and Automotive Dealers across North America, Europe, Asia-Pacific, South America, and Middle East & Africa. It examines semiconductor integration trends, edge AI deployment, generative cockpit systems, autonomous mobility infrastructure, and cybersecurity frameworks shaping enterprise investment decisions. The analysis supports competitive benchmarking, expansion planning, technology partnerships, and long-term operational strategy development across rapidly evolving software-defined mobility ecosystems.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 3610 Million |

|

Market Revenue in 2033 |

USD 22272.25 Million |

|

CAGR (2026 - 2033) |

25.54% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

NVIDIA Corporation, Qualcomm Incorporated, Mobileye Global Inc., Tesla Inc., Huawei Technologies Co., Ltd., Robert Bosch GmbH, Continental AG, Aptiv PLC, Denso Corporation, Valeo SA, Baidu Inc., Microsoft Corporation, Alphabet Inc., Amazon Web Services, Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |