Reports

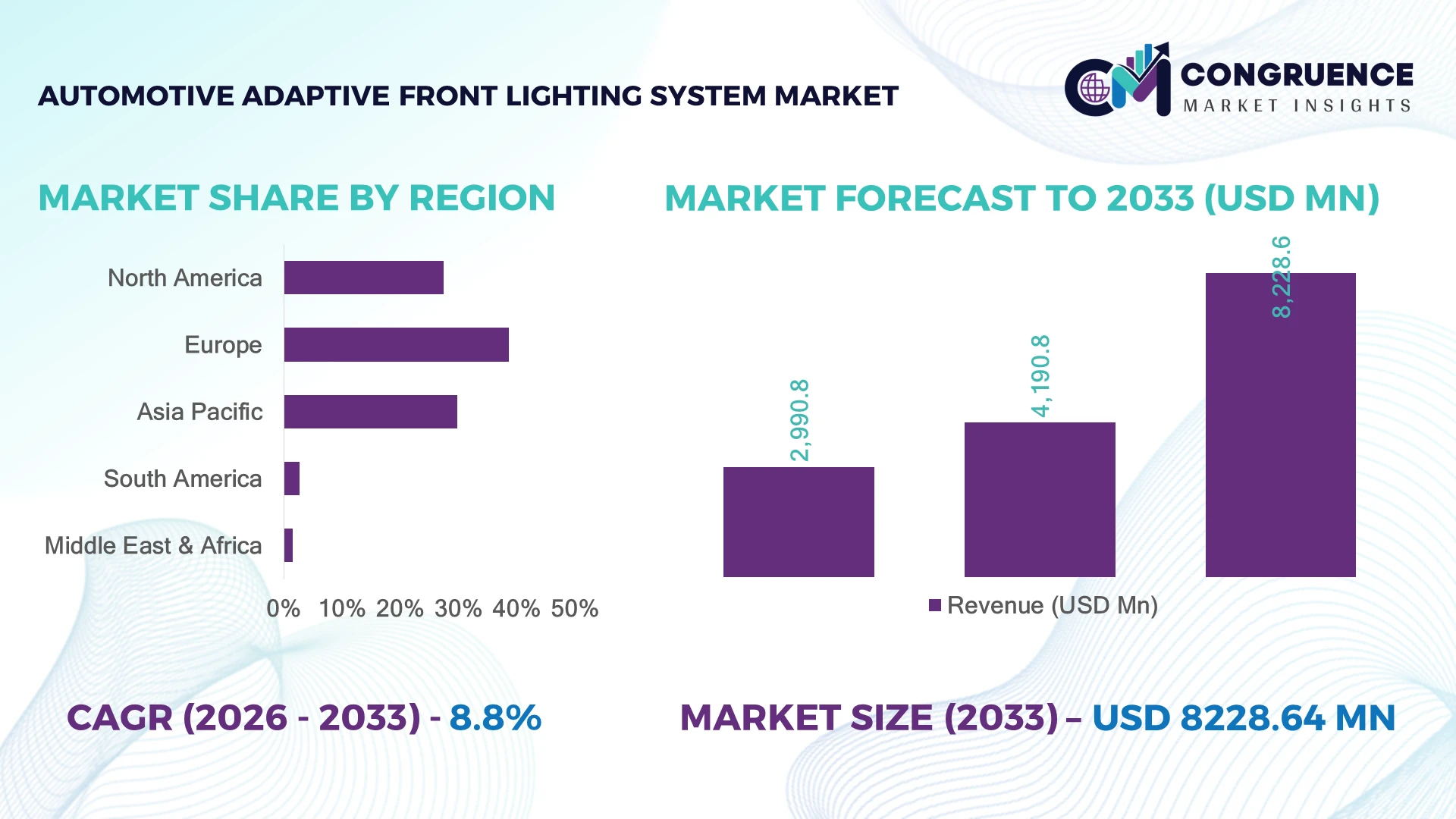

The Global Automotive Adaptive Front Lighting System Market was valued at USD 4,190.8 Million in 2025 and is anticipated to reach a value of USD 8228.6 Million by 2033 expanding at a CAGR of 8.8% between 2026 and 2033. Increasing adoption of intelligent vehicle safety systems, matrix LED technologies, and sensor-integrated lighting platforms is accelerating adaptive front lighting deployment globally.

Germany dominates the Automotive Adaptive Front Lighting System Market with approximately 31% share in 2025, supported by premium automotive manufacturing, advanced vehicle electronics, and strong integration of intelligent lighting technologies. Compared with Japan’s 24% adoption concentration, Germany maintains leadership through luxury vehicle production and innovation from automotive technology suppliers. The 2026 shift toward software-defined vehicles and advanced driver assistance systems is increasing demand for adaptive illumination solutions.

Automakers investing in intelligent lighting platforms are strengthening vehicle safety differentiation, regulatory readiness, and next-generation mobility competitiveness.

• Market Size & Growth: USD 4,190.8 Million in 2025 reaching USD 8,228.6 Million by 2033 at 8.8% CAGR, driven by ADAS integration and smart vehicle technologies.

• Top Growth Drivers: Vehicle safety upgrades 42%, LED adoption 38%, and premium vehicle electrification 35% are accelerating demand.

• Short-Term Forecast: By 2028, adaptive lighting systems are expected to improve night-driving visibility performance by nearly 30%.

• Emerging Technologies: AI-powered lighting, matrix LED systems, sensor fusion, and laser-based illumination are transforming vehicle lighting architecture.

• Regional Leaders: Europe USD 2.6 Billion, Asia-Pacific USD 3.1 Billion, and North America USD 1.9 Billion supported by smart mobility adoption.

• Consumer/End-User Trends: Nearly 45% of new premium vehicles integrate adaptive lighting features for enhanced safety and driving experience.

• Pilot/Case Example: 2026 intelligent lighting deployments improved automated beam adjustment accuracy by approximately 28% through camera-based control.

• Competitive Landscape: Leading manufacturers hold nearly 48% share, including Valeo, HELLA, Marelli, Koito, and Stanley Electric.

• Regulatory & ESG Impact: Advanced lighting efficiency improvements reduced vehicle lighting energy consumption by nearly 20% through LED transition.

• Investment & Funding: Over USD 5 Billion investments support automotive electronics, smart lighting innovation, and production expansion.

• Innovation & Future Outlook: Next-generation lighting is shifting toward AI-controlled, connected, and software-defined vehicle illumination systems.

The Automotive Adaptive Front Lighting System Market is transforming through intelligent illumination technologies, vehicle electrification, and advanced safety requirements. Automakers are integrating adaptive headlights with sensors, cameras, and driver assistance platforms, with nearly 50% of premium vehicle programs prioritizing smart lighting features. Supply-chain localization and semiconductor availability strategies are reshaping automotive lighting production models.

The Automotive Adaptive Front Lighting System Market is becoming strategically important as automakers compete through vehicle intelligence, safety enhancement, and premium driving experiences. The transition toward connected and software-defined vehicles is increasing demand for lighting systems capable of real-time adjustment based on road, traffic, and environmental conditions. Automotive manufacturers are restructuring electronics supply chains to improve technology control and production resilience.

Compared with conventional halogen-based lighting systems, advanced adaptive LED platforms improve illumination efficiency by nearly 40% and reduce power consumption by approximately 30%. Europe leads through luxury vehicle integration and safety-focused innovation, while Asia-Pacific benefits from large-scale vehicle production and rapid adoption of advanced electronic systems.

Automakers are deploying matrix LEDs, camera-linked lighting controls, and predictive illumination technologies across next-generation models. Suppliers are increasing investments in software capabilities, sensor integration, and strategic partnerships with vehicle manufacturers. Future competitive positioning will depend on intelligent lighting performance, electronic architecture compatibility, and ability to support autonomous driving ecosystems.

Increasing focus on advanced vehicle safety systems is driving adoption of automotive adaptive front lighting technologies. Nearly 45% of premium and next-generation vehicles integrate adaptive illumination features to improve visibility and driver assistance capabilities. Camera-based lighting control improves road visibility response by around 35%, while LED-based adaptive systems reduce energy usage by nearly 30%. Germany’s automotive innovation ecosystem and global safety technology transition are accelerating deployment. Companies are responding through sensor integration, advanced lighting platforms, and partnerships with automakers to enhance intelligent mobility solutions.

Advanced adaptive front lighting systems face limitations from higher component costs, semiconductor dependency, and integration complexity. Smart lighting modules can increase lighting system costs by nearly 25%, while electronic control requirements create challenges for mass-market vehicle adoption. Supply-chain fluctuations affecting automotive chips continue influencing production strategies in major manufacturing hubs. Companies are reducing risks through localized sourcing, modular lighting architectures, and improved electronic component efficiency to support broader vehicle segment penetration.

The transition toward AI-enabled vehicles and software-controlled automotive platforms creates significant opportunities for adaptive lighting innovation. Nearly 40% of future vehicle electronics development is shifting toward intelligent systems capable of predictive decision-making and personalization. AI-supported lighting technologies improve adaptive response accuracy by approximately 28% through environmental analysis and sensor data processing. Companies are expanding R&D investments, developing connected lighting ecosystems, and collaborating with automotive technology providers to strengthen next-generation mobility capabilities.

Scaling adaptive front lighting technologies requires overcoming vehicle architecture compatibility, software integration, and regulatory alignment challenges. Nearly 30% of automotive technology programs face complexity related to integrating sensors, lighting controls, and electronic platforms. Increasing software dependency requires stronger cybersecurity, validation processes, and engineering expertise. Automakers and suppliers must invest in standardized platforms, advanced testing capabilities, and collaborative development models to ensure reliable deployment across different vehicle categories and global markets.

• AI-Enabled Lighting Control: Artificial intelligence integration is transforming adaptive lighting performance through predictive beam adjustment, object recognition, and road condition analysis. Nearly 40% of advanced vehicle programs are incorporating AI-based control systems, improving response accuracy by approximately 28%. Companies are expanding software capabilities and sensor partnerships to enhance intelligent driving experiences.

• Matrix LED Technology Expansion: Automakers are increasing deployment of matrix LED systems for precise illumination control and improved nighttime safety. Advanced LED platforms improve energy efficiency by nearly 30% and enhance visibility range by around 25%. Manufacturers are scaling production capacity and modular lighting designs to support wider vehicle adoption.

• Sensor Fusion Integration: Adaptive lighting systems are increasingly connected with cameras, radar, and vehicle control units for real-time environmental response. Around 45% of next-generation vehicle platforms integrate lighting with driver assistance technologies. Companies are restructuring development strategies around connected electronic architectures and software-defined mobility.

• Premium Features Moving Mainstream: Technologies previously limited to luxury vehicles are expanding into mid-range models through cost optimization and electronics advancement. Adaptive lighting adoption in non-premium segments increased by nearly 22%, supported by component standardization and safety expectations. Suppliers are developing scalable platforms to capture broader automotive demand.

LED-Based Adaptive Front Lighting Systems dominate the Automotive Adaptive Front Lighting System Market due to superior energy efficiency, longer operating life, flexible design integration, and compatibility with advanced vehicle electronics. LED systems account for nearly 58% of adoption, supported by increasing deployment across premium and mid-range vehicles. Matrix LED Adaptive Lighting is witnessing the fastest adoption growth as automakers shift toward precise beam control, sensor-based adjustment, and software-defined lighting architectures.

Xenon-Based Systems, Laser-Based Lighting Systems, and other advanced lighting technologies continue serving specialized applications where high-intensity illumination and premium performance are required. Nearly 45% of next-generation vehicle platforms are integrating adaptive lighting with cameras and driver assistance technologies. Companies are responding through advanced LED module development, AI-based lighting controls, and partnerships with automotive manufacturers to improve safety performance while expanding intelligent lighting availability across broader vehicle categories.

• A 2026 automotive technology assessment highlighted that vehicles equipped with adaptive LED and matrix lighting technologies improved nighttime visibility performance by nearly 30%, supporting enhanced driver safety and advanced mobility development.

Passenger Vehicles represent the leading application segment in the Automotive Adaptive Front Lighting System Market due to increasing consumer demand for safety technologies, premium features, and intelligent driving assistance. The segment accounts for nearly 72% of deployment as automakers integrate adaptive headlights into electric vehicles, luxury models, and next-generation connected cars. Electric Vehicles are emerging as the fastest-growing application area due to advanced electronic architectures and greater adoption of smart mobility technologies.

Commercial Vehicles and Autonomous Vehicle Platforms are expanding adoption as fleet operators prioritize visibility, driver safety, and operational efficiency. Nearly 40% of newly developed vehicle platforms are incorporating adaptive lighting compatibility during design stages. Automakers are adapting through scalable lighting systems, software integration, and electronic platform optimization to support wider deployment across different vehicle segments.

• A 2025 automotive safety technology review reported that integration of intelligent lighting and driver assistance systems increased across new vehicle platforms by approximately 35%, strengthening demand for adaptive illumination technologies.

Automotive OEMs dominate the Automotive Adaptive Front Lighting System Market due to direct integration of intelligent lighting technologies into new vehicle platforms and large-scale production programs. OEMs account for nearly 68% of demand, supported by increasing adoption of connected vehicle architectures, safety-focused designs, and advanced driver assistance features. Aftermarket Providers are becoming the fastest-growing end-user group as vehicle owners upgrade conventional lighting systems with advanced illumination solutions.

Fleet Operators, Mobility Service Providers, and Automotive Technology Companies are expanding adoption through safety improvement initiatives and smart transportation development. Around 42% of automotive manufacturers are prioritizing adaptive lighting integration within next-generation vehicle programs. Suppliers are targeting these groups through customized modules, strategic partnerships, and scalable technology platforms to strengthen competitive positioning in intelligent vehicle ecosystems.

• A 2026 automotive innovation survey indicated that over 50% of major vehicle manufacturers increased investment in smart lighting and electronic safety systems, accelerating integration of adaptive front lighting technologies across future vehicle platforms.

Europe accounted for the largest market share at 38.6% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.5% between 2026 and 2033.

North America’s Automotive Adaptive Front Lighting System Market is supported by increasing deployment of intelligent vehicle safety technologies, premium vehicle demand, and advanced automotive electronics integration. The region accounted for approximately 27.4% market share in 2025, driven by strong adoption of adaptive LED systems, connected vehicle platforms, and driver assistance technologies. Nearly 42% of premium vehicle models integrate adaptive illumination systems to improve visibility and driving safety. Automakers are expanding partnerships with lighting technology providers and investing in software-controlled lighting architectures for next-generation mobility platforms.

United States Market Outlook: The United States leads regional adoption due to its advanced automotive technology ecosystem, strong electric vehicle development, and increasing integration of intelligent safety features. Vehicle manufacturers are deploying adaptive headlights with sensors, cameras, and ADAS platforms. Nearly 45% of newly launched premium vehicles include smart lighting capabilities, strengthening demand for advanced front lighting technologies.

Europe dominates the Automotive Adaptive Front Lighting System Market through strong luxury vehicle production, advanced automotive engineering, and early adoption of intelligent safety technologies. The region accounted for 38.6% market share in 2025, supported by Germany, France, and Italy’s automotive manufacturing strength. More than 50% of premium vehicle platforms integrate adaptive LED or matrix lighting systems for enhanced road visibility and safety performance. Automotive suppliers are focusing on AI-enabled lighting control, energy-efficient designs, and software-based illumination solutions to maintain technology leadership.

Germany Market Outlook: Germany represents the leading European market due to its premium automotive manufacturing base, advanced component ecosystem, and strong innovation in vehicle electronics. Automakers are increasing deployment of matrix LED, laser lighting, and adaptive beam technologies. Around 55% of luxury vehicle programs incorporate intelligent lighting systems, reinforcing Germany’s position in advanced automotive technology development.

Asia-Pacific’s Automotive Adaptive Front Lighting System Market is expanding rapidly through high vehicle production volumes, electric vehicle adoption, and increasing integration of advanced safety technologies. The region accounted for nearly 29.8% market share in 2025, supported by China, Japan, and South Korea’s automotive manufacturing capabilities. More than 40% of next-generation vehicle development programs include adaptive lighting compatibility and connected electronics integration. Companies are expanding manufacturing capacity, local technology partnerships, and cost-efficient lighting solutions to support wider adoption.

China Market Outlook: China leads Asia-Pacific adoption through its large automotive production ecosystem, rapid electric vehicle expansion, and increasing investment in intelligent vehicle technologies. Domestic and international manufacturers are integrating adaptive lighting features into connected vehicle platforms. Nearly 48% of new premium electric vehicle models include advanced lighting technologies, supporting China’s transition toward smart mobility leadership.

South America’s Automotive Adaptive Front Lighting System Market is developing through gradual adoption of advanced vehicle safety systems, automotive production upgrades, and increasing premium vehicle penetration. The region accounted for approximately 2.7% market share in 2025, with Brazil representing the primary automotive manufacturing hub. Nearly 25% of new higher-end vehicle launches include advanced lighting technologies as automakers introduce global safety features locally. Cost sensitivity and infrastructure limitations influence adoption speed, while manufacturers focus on scalable lighting solutions.

Brazil Market Outlook: Brazil leads regional demand due to its established automotive manufacturing base, expanding vehicle technology adoption, and presence of global automakers. Companies are introducing adaptive lighting features across premium and selected mid-range vehicles. Around 30% of advanced vehicle technology upgrades focus on safety and electronic systems, supporting gradual adoption of intelligent front lighting solutions.

Middle East & Africa’s Automotive Adaptive Front Lighting System Market is supported by premium vehicle adoption, smart transportation initiatives, and increasing demand for advanced safety features. The region accounted for nearly 1.5% market share in 2025, with adoption concentrated across luxury vehicles and technologically advanced automotive segments. Nearly 35% of premium vehicle imports include adaptive lighting features, reflecting growing preference for intelligent mobility solutions. Automakers are strengthening regional offerings through advanced vehicle configurations and technology-focused product strategies.

United Arab Emirates Market Outlook: The United Arab Emirates leads regional adoption through strong luxury vehicle demand, smart mobility initiatives, and advanced transportation infrastructure development. Automotive brands are increasing availability of vehicles equipped with adaptive LED and intelligent lighting technologies. Nearly 40% of premium vehicle sales include advanced driver assistance and lighting features, supporting demand for next-generation automotive systems.

The Automotive Adaptive Front Lighting System Market is led by Valeo, HELLA, Marelli, Koito Manufacturing, and Stanley Electric, where global lighting technology suppliers compete with automotive electronics specialists and advanced mobility innovators. The top five players collectively hold approximately 48% share, reflecting a technology-intensive structure focused on intelligent illumination and vehicle integration. Competition is based on lighting performance, software capability, customization, and manufacturing efficiency, with matrix LED systems improving visibility by nearly 30% and energy optimization by around 25%. Companies are competing through sensor integration, AI-based lighting development, production expansion, and partnerships with global automakers. The market is shifting toward software-defined lighting platforms, connected vehicle ecosystems, and adaptive safety technologies. High R&D investment, automotive qualification standards, and electronics integration complexity create strong entry barriers. Winning against established players requires advanced optical engineering, scalable production capability, and strong OEM collaboration.

• Valeo SA

• HELLA GmbH & Co. KGaA

• Marelli Holdings Co., Ltd.

• Koito Manufacturing Co., Ltd.

• Stanley Electric Co., Ltd.

• Hyundai Mobis Co., Ltd.

• ZKW Group GmbH

• Varroc Engineering Limited

• Lumax Industries Limited

• Continental AG

• ams-OSRAM AG

• Nichia Corporation

Automotive adaptive front lighting technologies are evolving through matrix LED systems, laser lighting, AI-based beam control, and sensor-integrated illumination platforms. Current systems combine cameras, electronic control units, and adaptive algorithms to improve visibility and driving safety. Nearly 50% of premium vehicle platforms are integrating intelligent lighting technologies with advanced driver assistance systems.

Compared with traditional halogen lighting systems, adaptive LED and matrix lighting technologies improve illumination efficiency by approximately 40% and reduce power consumption by nearly 30%. Emerging technologies including AI-driven predictive lighting, digital projection headlights, and vehicle-to-infrastructure connected lighting enable real-time road adaptation. Premium automakers and suppliers with strong software and semiconductor capabilities gain competitive advantages through faster innovation cycles.

Between 2026 and 2028, technology development will focus on fully digital lighting systems, autonomous vehicle compatibility, and personalized illumination experiences. Companies adopting advanced optical platforms will strengthen safety performance, reduce energy consumption, and improve differentiation as intelligent lighting becomes a critical component of future mobility ecosystems.

• January 2025 – Valeo advanced its intelligent lighting technologies with adaptive beam and software-driven illumination solutions, improving visibility optimization by nearly 30%. The innovation strengthened next-generation vehicle safety features and integration with connected mobility platforms. Source: valeo.com

• April 2024 – HELLA expanded its automotive lighting portfolio with advanced digital headlamp technologies supporting adaptive vehicle functions, improving lighting precision by approximately 25%. The development enhanced smart illumination capabilities for premium and electric vehicles. Source: hella.com

• February 2025 – Marelli strengthened its automotive lighting innovation strategy through next-generation electronic lighting solutions, increasing adaptive control efficiency by nearly 20%. The advancement supported automakers transitioning toward software-defined vehicle architectures and intelligent safety systems. Source: marelli.com

• September 2024 – Koito Manufacturing expanded development of advanced automotive lighting systems with sensor-integrated technologies, improving adaptive illumination response and energy efficiency by approximately 22%. The initiative strengthened vehicle safety applications and smart mobility solutions. Source: koito.co.jp

The Automotive Adaptive Front Lighting System Market Report provides comprehensive analysis of lighting technologies, vehicle applications, end-user adoption, regional trends, and competitive strategies shaping intelligent automotive illumination. The report covers LED-based adaptive systems, matrix lighting, laser lighting, and advanced electronic lighting solutions used across passenger vehicles, commercial vehicles, electric vehicles, and autonomous mobility platforms.

The study evaluates developments across North America, Europe, Asia-Pacific, South America, and Middle East & Africa, focusing on technology adoption, production ecosystems, and automotive innovation trends. Nearly 45% of premium vehicle platforms are integrating adaptive lighting solutions to enhance safety and driving experience. The report supports strategic planning, product development, investment evaluation, and competitive positioning across the evolving automotive lighting ecosystem between 2026 and 2033.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 4,190.8 Million |

|

Market Revenue in 2033 |

USD 8,228.6 Million |

|

CAGR (2026 - 2033) |

8.8% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Valeo SA, HELLA GmbH & Co. KGaA, Marelli Holdings Co., Ltd., Koito Manufacturing Co., Ltd., Stanley Electric Co., Ltd., Hyundai Mobis Co., Ltd., ZKW Group GmbH, Varroc Engineering Limited, Lumax Industries Limited, Continental AG, ams-OSRAM AG, Nichia Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |