Reports

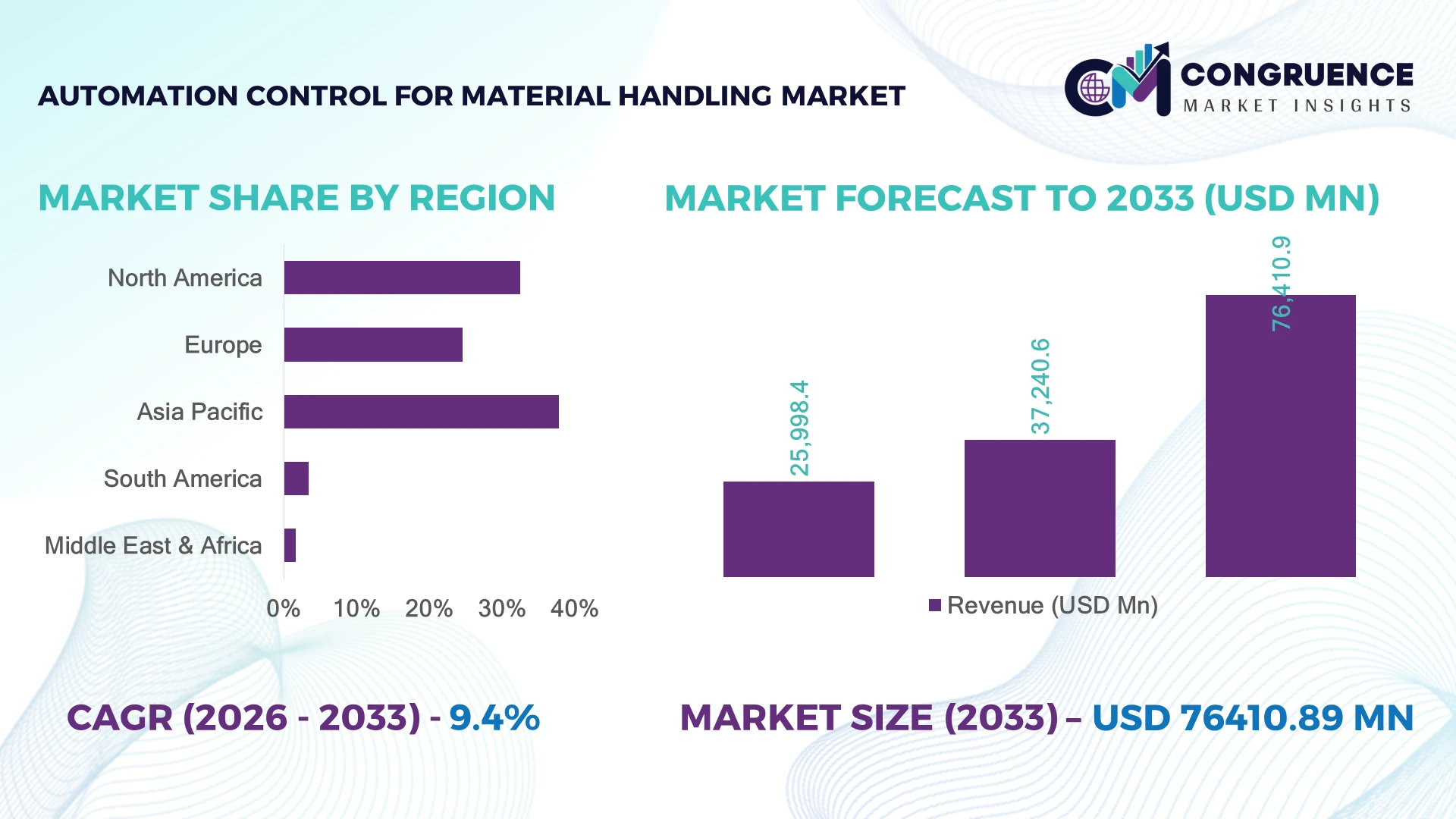

The Global Automation Control for Material Handling Market was valued at USD 37,240.6 Million in 2025 and is anticipated to reach a value of USD 76,410.9 Million by 2033 expanding at a CAGR of 9.4% between 2026 and 2033. Rising warehouse automation, smart manufacturing adoption, AI-powered logistics optimization, and industrial robotics deployment are accelerating automation control integration across material handling operations.

The United States dominated the Automation Control for Material Handling Market with approximately 34% share in 2025, supported by advanced manufacturing facilities, automated warehouse networks, and strong Industry 4.0 adoption. The U.S. maintains over 45% automation penetration across large-scale logistics facilities compared with nearly 30% adoption in Germany’s industrial ecosystem. Supply-chain restructuring after global logistics disruptions has accelerated investment in intelligent automation platforms and resilient production networks.

Companies adopting advanced automation control systems are gaining operational advantages through higher productivity, reduced downtime, and improved supply-chain responsiveness.

• Market Size & Growth: USD 37,240.6 Million in 2025 reaching USD 76,410.9 Million by 2033 at 9.4% CAGR, driven by smart factory and warehouse automation expansion.

• Top Growth Drivers: Robotics adoption 42%, warehouse digitization 38%, and AI-based process optimization 35% are strengthening automation demand.

• Short-Term Forecast: By 2028, intelligent material handling systems are expected to improve operational efficiency by nearly 30%.

• Emerging Technologies: AI control systems, autonomous mobile robots, digital twins, and IoT-enabled automation platforms are transforming industrial workflows.

• Regional Leaders: North America USD 24.5 Billion, Asia-Pacific USD 28.7 Billion, and Europe USD 18.2 Billion through manufacturing modernization.

• Consumer/End-User Trends: Over 50% of large warehouses are adopting automated control solutions to improve throughput and accuracy.

• Pilot/Case Example: 2026 smart warehouse deployments improved order processing efficiency by approximately 32% through integrated automation systems.

• Competitive Landscape: Leading providers hold nearly 40% share, including Siemens, Honeywell, Rockwell Automation, ABB, and Schneider Electric.

• Regulatory & ESG Impact: Energy-efficient automation systems reduced industrial energy consumption by nearly 20% across optimized facilities.

• Investment & Funding: Over USD 15 Billion investments support robotics expansion, industrial automation projects, and smart logistics infrastructure.

• Innovation & Future Outlook: Next-generation automation is shifting toward autonomous operations, predictive control, and connected industrial ecosystems.

Automation Control for Material Handling is transforming industrial operations through robotics, sensors, programmable control systems, and intelligent software platforms. Automated warehouses and smart factories are increasing deployment of integrated control solutions, with nearly 55% of enterprises prioritizing digital workflow optimization. Labor availability challenges and supply-chain resilience strategies are accelerating adoption of flexible automation technologies.

The Automation Control for Material Handling Market is becoming strategically important as manufacturers, logistics providers, and retailers modernize operations to improve speed, accuracy, and scalability. Increasing demand for resilient supply chains, labor optimization, and real-time operational visibility is driving investments in connected automation ecosystems. Industrial companies are shifting from isolated equipment automation toward fully integrated digital control platforms.

Compared with conventional manual material handling processes, automated control systems improve throughput efficiency by nearly 35% and reduce operational errors by approximately 30%. North America leads in advanced warehouse digitization and software integration, while Asia-Pacific demonstrates large-scale deployment strength through electronics manufacturing, automotive production, and logistics expansion.

Enterprises are deploying automated storage systems, robotics, IoT-enabled controls, and predictive analytics to enhance operational flexibility. Companies are increasing partnerships with automation providers, upgrading manufacturing infrastructure, and investing in intelligent control technologies. Future competitiveness will depend on automation scalability, system integration capability, and data-driven operational performance.

Increasing adoption of smart factories and automated logistics networks is accelerating demand for automation control systems in material handling. Nearly 45% of large manufacturing facilities are integrating robotics, sensors, and intelligent controllers to optimize production flow. Automated systems improve inventory accuracy by around 35% and reduce handling delays by nearly 30%. Supply-chain modernization initiatives in the United States and China are increasing investment in flexible automation platforms. Companies are responding through robotics expansion, software integration, and strategic partnerships focused on improving operational productivity.

Complex system integration and existing infrastructure limitations restrict automation adoption across traditional industrial environments. Nearly 35% of small and medium manufacturers face challenges related to equipment compatibility, implementation costs, and digital readiness. Legacy production facilities require extensive upgrades before deploying advanced control platforms, increasing transition complexity by approximately 25%. Industrial operators are reducing risks through phased automation strategies, modular solutions, and technology partnerships. Successful implementation depends on balancing automation benefits with infrastructure modernization requirements.

Artificial intelligence, autonomous robots, and predictive control technologies are creating new opportunities for next-generation material handling automation. Nearly 40% of industrial automation investments are shifting toward intelligent systems capable of real-time decision-making and adaptive workflow management. AI-enabled platforms improve resource utilization by approximately 28% through predictive optimization and automated scheduling. Companies are expanding R&D programs, developing connected ecosystems, and partnering with technology providers to capture opportunities from fully automated industrial environments.

Scaling automation control systems creates challenges related to workforce adaptation, cybersecurity protection, and operational technology integration. Nearly 32% of manufacturers identify skill shortages as a barrier to advanced automation deployment, while connected systems increase demand for secure industrial networks. Smart factories require specialized expertise in robotics, software, and data management. Companies must invest in workforce training, cybersecurity frameworks, and interoperable platforms to maintain reliable automation performance and long-term operational resilience.

• Autonomous Warehouse Operations: Warehouses are accelerating adoption of automated storage systems, robotics, and intelligent control platforms. Nearly 50% of large logistics facilities are integrating automation technologies, improving fulfillment speed by approximately 35%. Companies are scaling robotic fleets and connected warehouse ecosystems to increase productivity.

• AI-Based Process Optimization: Artificial intelligence is enhancing material flow planning, equipment monitoring, and predictive decision-making. AI-enabled control platforms improve operational efficiency by nearly 30% and reduce unplanned downtime by around 25%. Industrial companies are deploying analytics-driven automation solutions for greater process reliability.

• Connected Industrial Ecosystems: IoT-enabled controllers, sensors, and cloud platforms are improving visibility across manufacturing and logistics operations. Around 45% of smart factory projects include connected automation infrastructure. Companies are integrating data platforms and control systems to improve coordination across complex supply chains.

• Flexible Robotics Deployment: Modular robots and adaptive automation systems are replacing fixed material handling processes. Flexible solutions reduce production changeover time by nearly 30% and improve scalability across changing workflows. Manufacturers are investing in collaborative robots and configurable automation platforms to support dynamic operations.

Conveyor Control Systems dominate the Automation Control for Material Handling Market due to their scalability, reliability, and integration across manufacturing, logistics, and warehouse operations. Conveyor-based automation accounts for nearly 42% of adoption, supported by high-volume material movement requirements and compatibility with sensors, robotics, and warehouse management platforms. Robotic Control Systems are witnessing the fastest adoption growth as industries shift toward flexible automation, autonomous operations, and labor-efficient production environments.

Automated Storage and Retrieval System (AS/RS) Controls, Programmable Logic Controllers (PLCs), and Warehouse Control Systems continue expanding as companies prioritize connected infrastructure and intelligent workflow management. Nearly 48% of industrial facilities are upgrading control architectures to improve equipment coordination and operational visibility. Automation providers are responding through AI-enabled software platforms, modular control solutions, and strategic technology partnerships to support flexible production models and future-ready material handling ecosystems.

• A 2026 industrial automation assessment highlighted that manufacturers deploying integrated material handling control systems improved operational throughput by nearly 32%, supporting faster production cycles and intelligent warehouse transformation.

Warehouse Automation represents the leading application segment in the Automation Control for Material Handling Market due to rising demand for faster fulfillment, inventory accuracy, and integrated logistics operations. The segment accounts for nearly 46% of deployment as retailers, manufacturers, and logistics providers implement automated conveyors, robotics, and digital control platforms. Smart Manufacturing is emerging as the fastest-growing application area due to Industry 4.0 adoption and increasing use of connected production technologies.

Packaging Automation, Assembly Line Automation, and Distribution Center Operations continue expanding as companies improve productivity, consistency, and process visibility. Nearly 50% of large enterprises are investing in automation technologies to optimize material flow and reduce operational bottlenecks. Companies are adapting through robotics integration, intelligent software deployment, and scalable automation architectures to strengthen efficiency and supply-chain responsiveness.

• A 2025 smart logistics industry review reported that automated warehouse facilities achieved nearly 30% improvement in order processing efficiency through robotics, advanced control systems, and real-time operational monitoring.

Manufacturing represents the dominant end-user segment in the Automation Control for Material Handling Market due to extensive deployment across production lines, assembly operations, and industrial logistics environments. The segment accounts for approximately 45% of demand as automotive, electronics, and industrial manufacturers depend on automation controls for continuous operations and productivity improvement. E-commerce and logistics companies are becoming the fastest-growing end-user group due to rapid fulfillment requirements and warehouse digitization.

Retail, food and beverage, pharmaceuticals, and third-party logistics providers continue increasing adoption through automated storage, tracking, and handling technologies. Around 43% of enterprises are prioritizing flexible automation systems to address labor constraints and changing operational requirements. Solution providers are targeting these industries through customized platforms, service partnerships, and integrated control ecosystems to improve competitive positioning.

• A 2026 enterprise automation survey indicated that organizations implementing advanced material handling automation reduced manual processing dependency by nearly 35%, accelerating investment in robotics and intelligent industrial control technologies.

Asia-Pacific accounted for the largest market share at 37.8% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 10.1% between 2026 and 2033.

North America’s Automation Control for Material Handling Market is driven by advanced warehouse digitization, industrial automation investments, and large-scale adoption of intelligent logistics technologies. The region accounted for nearly 32.5% market share in 2025, supported by automated fulfillment centers, robotics integration, and Industry 4.0 transformation programs. More than 55% of large logistics facilities are deploying automated control platforms to improve throughput and operational visibility. Companies are expanding AI-enabled warehouse systems, predictive control technologies, and robotics partnerships to address labor constraints and supply-chain optimization requirements.

United States Market Outlook: The United States leads regional adoption through advanced manufacturing networks, e-commerce infrastructure, and strong automation technology deployment. Industrial companies are increasing investments in robotics, warehouse management systems, and intelligent material flow solutions. Nearly 60% of large-scale distribution facilities use automated handling technologies, improving productivity and supporting resilient supply-chain operations.

Europe’s Automation Control for Material Handling Market is supported by smart factory modernization, industrial efficiency programs, and increasing deployment of connected automation systems. The region accounted for approximately 24.6% market share in 2025, with Germany, France, and Italy leading adoption across automotive, manufacturing, and logistics industries. Nearly 50% of advanced manufacturing facilities are integrating robotics, sensors, and digital control platforms to optimize operations. Companies are focusing on energy-efficient automation, modular control systems, and intelligent production technologies to enhance competitiveness.

Germany Market Outlook: Germany represents the leading European market due to its strong industrial base, automation engineering expertise, and advanced manufacturing ecosystem. Automotive and machinery manufacturers are deploying intelligent material handling solutions to improve production efficiency. Around 58% of major industrial facilities have adopted smart factory technologies, strengthening demand for automated control and connected production systems.

Asia-Pacific dominates the Automation Control for Material Handling Market due to large-scale manufacturing operations, expanding logistics infrastructure, and rapid industrial automation adoption. The region accounted for 37.8% market share in 2025, supported by China, Japan, South Korea, and India’s investments in smart factories and automated warehouses. More than 50% of new manufacturing modernization projects include robotics, control systems, or intelligent material handling technologies. Companies are expanding local automation production, industrial software capabilities, and integrated solutions for high-volume operations.

China Market Outlook: China leads Asia-Pacific adoption through its extensive manufacturing ecosystem, automation investments, and smart factory transformation initiatives. Industrial enterprises are increasing deployment of robotics, automated conveyors, and intelligent control platforms. Nearly 55% of advanced manufacturing upgrades include digital automation technologies, supporting productivity improvements and strengthening China’s position in industrial automation deployment.

South America’s Automation Control for Material Handling Market is developing through manufacturing upgrades, warehouse modernization, and increasing adoption of automated logistics solutions. The region accounted for approximately 3.4% market share in 2025, with demand concentrated across automotive, food processing, and distribution sectors. Nearly 30% of large industrial facilities are introducing automation technologies to improve efficiency and reduce operational limitations. Infrastructure gaps and investment constraints influence adoption pace, while companies are deploying scalable automation systems and technology partnerships.

Brazil Market Outlook: Brazil represents the leading regional market due to its industrial manufacturing base, logistics expansion, and growing adoption of automation technologies. Automotive, consumer goods, and warehousing companies are investing in material handling modernization. Around 35% of major industrial transformation initiatives include robotics or automated control systems to improve operational performance and production reliability.

Middle East & Africa’s Automation Control for Material Handling Market is expanding through logistics infrastructure development, industrial diversification, and investment in advanced manufacturing capabilities. The region accounted for nearly 1.7% market share in 2025, with adoption focused on smart warehouses, ports, and large industrial facilities. More than 25% of major logistics modernization initiatives include automation technologies to improve efficiency and capacity utilization. Companies are forming technology partnerships and deploying scalable control systems to support industrial transformation strategies.

United Arab Emirates Market Outlook: The United Arab Emirates leads regional adoption through smart logistics investments, advanced infrastructure projects, and digital transformation initiatives. Warehousing, aviation logistics, and industrial zones are increasing automation deployment to improve operational efficiency. Nearly 40% of major logistics development projects integrate smart technologies, supporting wider adoption of automated material handling control systems.

The Automation Control for Material Handling Market is led by Siemens, ABB, Honeywell International, Rockwell Automation, and Schneider Electric, where global automation technology providers compete with robotics specialists and warehouse automation solution developers. The top five players collectively hold approximately 42% share, reflecting a competitive structure driven by intelligent control platforms, software integration, and industrial ecosystem strength. Competition focuses on automation accuracy, customization, and deployment speed, with advanced control systems improving productivity by nearly 35% and reducing process downtime by around 25%. Companies are competing through robotics expansion, AI-based software development, strategic partnerships, and vertically integrated automation solutions. The market is shifting toward autonomous operations, connected factories, and predictive control technologies. High integration complexity, cybersecurity requirements, and technical expertise create strong entry barriers. Winning against established players requires scalable automation platforms, advanced software capability, and reliable industrial deployment expertise.

• Siemens AG

• ABB Ltd.

• Honeywell International Inc.

• Rockwell Automation Inc.

• Schneider Electric SE

• Mitsubishi Electric Corporation

• Omron Corporation

• Emerson Electric Co.

• Bosch Rexroth AG

• KUKA AG

• Daifuku Co., Ltd.

• Dematic

Automation control technologies for material handling are advancing through AI-enabled control platforms, industrial IoT, robotics integration, programmable logic controllers, and cloud-connected automation systems. Current technologies focus on improving real-time monitoring, equipment coordination, and operational reliability. Nearly 55% of advanced manufacturing and logistics facilities are adopting connected automation systems to enhance material flow visibility and process optimization.

Compared with conventional fixed automation systems, AI-powered and sensor-integrated platforms improve operational efficiency by approximately 30% and reduce unplanned downtime by nearly 25%. Emerging technologies including autonomous mobile robots, digital twins, machine vision, and predictive analytics are enabling flexible production environments. Automation providers with strong software ecosystems and robotics capabilities benefit as enterprises shift toward intelligent, data-driven operations.

Between 2026 and 2028, automation control development will focus on autonomous decision-making, adaptive robotics, and fully connected industrial ecosystems. Companies adopting advanced technologies will gain advantages through faster fulfillment, improved asset utilization, lower operational risks, and greater manufacturing flexibility.

• March 2025 – Siemens expanded its industrial automation portfolio with advanced AI-enabled automation capabilities, improving production optimization and engineering efficiency by nearly 30%. The development strengthened intelligent factory operations and next-generation material handling control deployment. Source: siemens.com

• June 2024 – ABB enhanced its robotics and automation solutions with next-generation control technologies supporting flexible manufacturing operations, increasing robotic system efficiency by approximately 25%. The advancement improved automated material handling performance across industrial environments. Source: abb.com

• February 2025 – Rockwell Automation expanded smart manufacturing solutions through integrated control and digital platforms, improving connected production capabilities by nearly 20%. The initiative supported manufacturers adopting scalable automation and intelligent material handling ecosystems. Source: rockwellautomation.com

• September 2024 – Honeywell strengthened warehouse automation technologies through advanced software and control system innovation, improving fulfillment productivity by approximately 30%. The expansion enhanced automated logistics operations, inventory accuracy, and supply-chain performance. Source: honeywell.com

The Automation Control for Material Handling Market Report analyzes control technologies, system types, applications, end-users, regional developments, and competitive strategies influencing global industrial automation adoption. The report covers conveyor controls, robotic control systems, automated storage and retrieval controls, PLC-based platforms, and warehouse control systems deployed across manufacturing, logistics, retail, and industrial environments.

The study evaluates automation trends across North America, Europe, Asia-Pacific, South America, and Middle East & Africa, highlighting technology deployment, infrastructure development, and investment priorities. Nearly 50% of large industrial enterprises are accelerating adoption of intelligent handling solutions to improve productivity and operational resilience. The report provides strategic insights for expansion planning, product development, competitive positioning, and future automation opportunities between 2026 and 2033.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 37,240.6 Million |

|

Market Revenue in 2033 |

USD 76,410.9 Million |

|

CAGR (2026 - 2033) |

9.4% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Siemens AG, ABB Ltd., Honeywell International Inc., Rockwell Automation Inc., Schneider Electric SE, Mitsubishi Electric Corporation, Omron Corporation, Emerson Electric Co., Bosch Rexroth AG, KUKA AG, Daifuku Co., Ltd., Dematic |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |