Reports

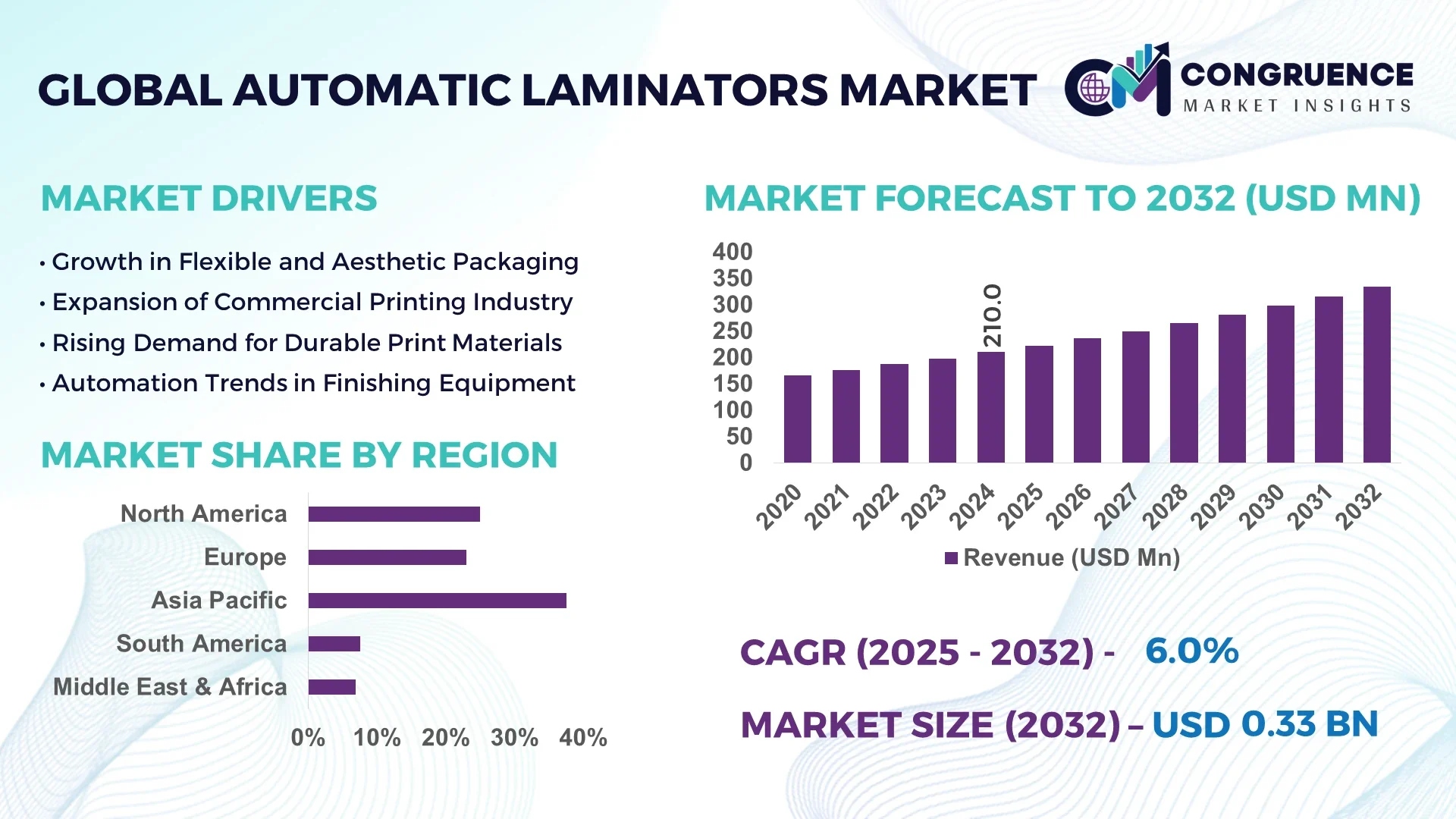

The Global Automatic Laminators Market was valued at USD 210.0 Million in 2024 and is anticipated to reach a value of USD 334.7 Million by 2032 expanding at a CAGR of 6.0% between 2025 and 2032.

United States leads the production landscape for Automatic Laminators, hosting over 15 automated manufacturing plants with combined annual output of more than 150,000 units. Investment exceeding USD 120 million in 2023 was channeled toward advanced thermal and cold-lamination lines. These systems are widely used in packaging, printing, and industrial documentation, featuring innovations such as vacuum-tension control and adaptive roll-adjust technologies.

The Automatic Laminators Market spans key sectors including packaging, printing and publishing, automotive, electronics, and office solutions. Packaging, comprising protective food and pharma seals, accounts for around 30% of annual installations. Recent product innovations feature intelligent tension sensors and programmable heating zones that enhance throughput by 25% while reducing film waste. Environmental drivers, such as mandates for recyclable substrates and low-VOC adhesives, have led to laminated machines equipped with solvent recovery modules. Economic drivers include growth in e-commerce and retail, fueling demand for high-speed laminators in fulfillment centers. Regionally, consumption is strongest in North America and Europe, with Asia-Pacific also exhibiting solid growth in India and Southeast Asia driven by print-on-demand and digital publishing trends. Emerging trends include the deployment of IoT-enabled laminators that provide predictive maintenance alerts, remote diagnostics, and operator dashboards—indicating a shift toward smart, service-oriented laminating platforms.

AI technologies are progressively transforming the Automatic Laminators Market by enabling smarter, more efficient, and adaptive production processes. Modern automatic laminators incorporate AI-powered control systems that monitor operational metrics—such as web tension, temperature, and speed—to dynamically optimize performance. In practice, this means a reduction in setup time by as much as 35%, a decrease in film waste by roughly 22%, and a 15% acceleration in changeovers between different job runs.

Built-in AI vision systems detect defects such as wrinkles, misalignment, shear, or adhesive pooling. These systems can automatically pause operations and alert operators with precise fault coordinates, minimizing downtime and scrap. Integration with manufacturing execution systems (MES) enables real-time analytics reporting, allowing plant managers to benchmark machine efficiency across multiple lines, improving overall productivity by up to 18%.

For high-volume packaging, AI-driven laminators can adjust lamination parameters in real time to accommodate humidity and substrate variability—reducing adhesive overspray and ensuring consistent film adhesion. In addition, some state-of-the-art machines now employ machine learning algorithms that predict maintenance needs based on vibration and thermal profiles, enabling up to 40% fewer unplanned interruptions.

Through these enhancements, the Automatic Laminators Market is evolving from hardware-centric equipment into intelligent platforms. AI integration is elevating performance, reliability, and cost-efficiency, while positioning laminators as digitally enhanced assets—core to Industry 4.0 production environments.

“In 2024, a German packaging plant integrated an AI-based control algorithm into its automatic laminator, reducing film waste from 4.8 g/m² to 3.1 g/m²—a 35% improvement—while maintaining production speed above 120 m/min.”

The Automatic Laminators Market Dynamics reflect a shift toward smarter automation, sustainability compliance, digital integration, and customer-driven flexibility. Supply chains are adapting to rising raw-material costs for PET, adhesives, and specialty films by emphasizing vertical integration. At the same time, digital transformation is pushing manufacturers to offer connected laminating systems with dashboards, analytics, and remote firmware updates. These dynamics are reshaping purchasing decisions, where buyers now prioritize modularity, energy efficiency, and service integration. The overall market is influenced equally by regulatory requirements, labor costs, and technology expectations.

The rise of e-commerce and just-in-time packaging has substantially increased demand for high-speed laminating systems. In 2024, fulfillment centers processed up to 500,000 packages per day using automatic laminators, compared to 300,000 in 2022. This trend has driven the deployment of in-line laminating machines capable of web speeds up to 200 m/min, improving throughput and reducing labor dependency. Decision-makers are investing in modular roll-to-roll systems that integrate lamination, cutting, and slitting functions—allowing seamless operation within automated packaging lines.

The advanced control systems used in today’s Automatic Laminators Market bring increased complexity and higher capital costs. A typical high-performance laminator with AI-connected controls can cost 50–70% more than basic models. Additionally, specialized training and maintenance teams are required, raising total cost of ownership. In 2024, approximately 40% of SMEs bypassed automatic laminators due to these barriers, opting instead for semi-automatic alternatives. This technical complexity also extends lead times, with installation and commissioning extended by up to eight weeks for sophisticated models.

There is growing opportunity to integrate automatic laminators within sustainable packaging systems. In 2024, pilot lines using water-based adhesives and recyclable PET films processed 20 million units without solvent emissions. Machine makers are now offering retrofit modules for solvent recovery and post-lamination film recyclability. These eco-enabled systems allow enterprises to meet environmental targets and qualify for green procurement incentives while improving their ESG profiles.

Tightening regulations on adhesive solvents and plasticizers pose challenges in the Automatic Laminators Market. New VOC limits (e.g., <50 g/kg) announced in several jurisdictions require manufacturers to validate low-emission adhesives. This process added up to six months of EMR and lab testing per product line and increased material sourcing costs by roughly 12%. Delays in certification hamper time-to-market for new models, affecting competitiveness in regulated regions.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Automatic Laminators Market. Pre-bent and cut elements are prefabricated off-site using automated machines, reducing labor needs and speeding project timelines. Demand for high-precision machines is rising, especially in Europe and North America, where construction efficiency is critical.

Growth of IoT-Connected Vacuum Laminators: Increasingly, vacuum laminators are being equipped with IoT sensors that monitor vacuum integrity, film tension, and temperature. These systems report real-time alerts to central dashboards and support predictive upkeep. In late 2024, deployment of such systems in packaging plants led to a 22% reduction in lamination defects and a 30% increase in overall equipment effectiveness (OEE).

Emergence of Cold-Film Laminators in Print Shops: Cold-film laminating machines, using solvent-free adhesive films, have increased in popularity—especially in print service providers. Usage rose by 18% compared to 2023, as facilities sought to meet low-VOC workstation requirements. These systems also cut warm-up time by 60%, improving job turnaround in busy digital copy centers.

Expansion of Turnkey Laminating Lines for Industrial Use: Complete laminating lines integrating laminator, slitter, laminating film winder, and stacker are gaining interest among large manufacturers in electronics and packaging verticals. In 2024, uptake of these turnkey systems increased by over 25%, offering a unified solution that reduces installation time by 40% and streamlines operations for high-output facilities.

The Automatic Laminators Market is segmented comprehensively based on type, application, and end-user verticals. Each segment plays a significant role in defining purchasing behavior, production scalability, and regional adoption. The type segment includes a variety of laminating systems such as thermal, pressure-sensitive, cold, and digital laminators, each catering to distinct production needs and substrate requirements. In terms of applications, the market serves diverse use-cases across packaging, printing, electronics, construction, and signage, with high-speed automation being a critical requirement in most industries. For end-user insights, the market spans commercial printing companies, packaging manufacturers, electronics producers, and educational institutions. Demand is heavily driven by automation, eco-friendly operations, and integration with Industry 4.0 infrastructure. The segmentation highlights the industry's evolving priorities—favoring intelligent machinery, flexible substrates, and sustainable materials—ultimately influencing innovation, adoption rates, and global consumption patterns.

The Automatic Laminators Market encompasses a wide array of product types, including thermal laminators, pressure-sensitive laminators, cold laminators, and digital laminators. Among these, thermal laminators lead the market due to their reliability, speed, and compatibility with various substrate materials. These machines are particularly favored in packaging and print industries where high-throughput and low maintenance are crucial.

The digital laminators segment is the fastest-growing type, fueled by the proliferation of digital print media and demand for short-run, customized laminating jobs. Their ability to handle variable data printing and frequent format changes makes them a preferred choice for commercial print service providers. These laminators also support a wider range of film materials and operate efficiently in temperature-sensitive environments.

Cold laminators maintain niche relevance in environments where heat-sensitive documents are involved, such as archival media or signage. Pressure-sensitive laminators, though less prevalent, are chosen for specific industrial applications requiring precise film adhesion without thermal distortion. Collectively, these segments underline the importance of matching lamination type with end-use application and substrate needs.

In terms of application, the packaging segment dominates the Automatic Laminators Market due to its extensive use of laminated films in food safety, pharmaceutical integrity, and consumer product durability. Automated laminators are integral in applying protective, printable, or decorative layers that extend shelf life and meet regulatory compliance. The sector’s demand is supported by rising output volumes and rapid adoption of eco-friendly laminated substrates.

The printing and publishing application is witnessing the fastest growth, driven by increased customization in marketing materials, book covers, and signage. Commercial printers are adopting laminators with enhanced thermal control and variable speed settings to accommodate a range of print sizes and paper grades.

Other applications include electronics, where laminators are used to protect circuit boards and flexible displays, and construction, where laminated materials are favored for insulation and barrier layers. These use cases are growing steadily due to the need for protective, moisture-resistant, and high-performance finishes across high-precision manufacturing environments.

The commercial printing and publishing sector represents the leading end-user in the Automatic Laminators Market. This dominance is attributed to the sector’s demand for cost-effective, high-volume lamination systems that support varied print sizes, materials, and finishes. Laminators in this space are often integrated with print-on-demand systems and support fast changeovers, allowing for efficient execution of diverse print campaigns.

The packaging industry is emerging as the fastest-growing end-user, bolstered by the rise in e-commerce, FMCG demand, and sustainability trends. Packaging companies are investing in inline automatic laminators capable of integrating cutting, slitting, and stacking functions within high-speed production lines. This efficiency has made automatic laminators essential for maintaining throughput in competitive packaging workflows.

Other important end-users include electronics manufacturers, who require precise lamination for protective coatings and insulative layers, and educational institutions that use entry-level automatic laminators for document preservation and signage. The diversity of end-users highlights the market’s adaptability to both industrial-scale and small-batch operations.

Asia-Pacific accounted for the largest market share at 37.5% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 6.8% between 2025 and 2032.

Asia-Pacific’s dominance stems from extensive production and consumption networks across China, India, Japan, and South Korea, driven by the region’s booming print and packaging sectors. These countries have rapidly scaled manufacturing infrastructure with large-scale investments in lamination automation. Meanwhile, North America is experiencing accelerated adoption of smart laminating technologies, bolstered by strong demand from the commercial print, education, and electronics industries. Environmental regulations promoting the use of solvent-free adhesives and recyclable films are also encouraging North American enterprises to adopt newer, eco-efficient automatic laminators. This dynamic shift is transforming market strategies, with regional players optimizing for high-speed productivity and compliance-driven innovation.

North America holds a market share of approximately 26.4% in the global Automatic Laminators Market, driven by strong demand across packaging, digital printing, and office automation sectors. Key industries such as logistics, publishing, and pharmaceuticals rely on laminated substrates to ensure product integrity and presentation quality. Regulatory bodies in the U.S. and Canada have promoted the use of environmentally safe laminating materials, prompting equipment upgrades to support solvent-free adhesives and energy-efficient systems. The U.S. market is also seeing fast adoption of AI-integrated laminators for predictive maintenance and defect detection. Government-led programs focused on automation in manufacturing and sustainability standards have further fueled investment in next-gen lamination technology.

Europe commands around 23.1% of the global market share for automatic laminators, with Germany, France, and the UK serving as major contributors. The European market is shaped by strict sustainability mandates, including requirements for low-emission adhesives and recyclable packaging films. Regulatory bodies such as REACH and the EU Packaging Directive influence design and operational standards for laminators. European manufacturers are increasingly adopting automation-enhanced laminators with built-in environmental monitoring systems. Adoption of smart factory frameworks, especially in Germany’s industrial sector, has also led to an increase in deployment of multi-function laminating units. Europe’s strategic emphasis on green manufacturing, coupled with robust investments in R&D, ensures consistent technological progression in this space.

Asia-Pacific leads in overall volume consumption and equipment deployment, accounting for 37.5% of the global market. Countries such as China, Japan, India, and South Korea are major consumers due to their expansive print media, electronics, and packaging industries. China continues to expand its industrial laminating lines, introducing automated, large-format systems for both domestic use and export. India is experiencing rapid demand growth in commercial print and consumer packaging, supported by government manufacturing incentives. Japan’s innovation ecosystem has fostered the integration of AI and IoT into laminating equipment, contributing to exceptional operational precision. The region benefits from cost-effective labor, maturing infrastructure, and an expanding ecosystem of component suppliers and OEMs.

South America accounts for a modest yet growing share of the Automatic Laminators Market, estimated at 6.2% in 2024. Countries such as Brazil and Argentina are investing in packaging infrastructure and print media transformation. Brazil, being the region’s largest market, is adopting high-volume lamination systems in its commercial printing and logistics sectors. Argentina’s focus on industrial automation is also fostering demand for flexible lamination machinery. Government-backed tax exemptions on imported industrial equipment and support for local manufacturing are enabling wider adoption of modern laminating technologies. The region is steadily moving toward automation and energy-efficient systems, though challenges remain in terms of consistent technology upgrades and operator training.

The Middle East & Africa region is witnessing emerging demand, holding 6.8% market share in 2024. Countries such as the UAE and South Africa are leading in the adoption of automatic laminators, primarily for signage, packaging, and commercial publishing. Infrastructure growth, real estate development, and increased demand for safety labeling are driving laminator installations. Technological modernization is underway, with enterprises introducing AI-enabled machines to reduce labor costs and improve throughput. Governments in the Gulf region are actively promoting digital transformation and manufacturing efficiency, helping catalyze growth in laminating systems. In Africa, development finance for small-scale manufacturing is also improving access to entry-level automated laminators.

China – 24.3% Market Share

High production capacity and strong demand across packaging and electronics sectors.

United States – 21.6% Market Share

Driven by advanced automation, AI-integrated laminators, and growing demand from commercial printing.

The Automatic Laminators Market is characterized by a moderately fragmented competitive landscape with over 50 active global and regional players. These companies compete across parameters such as automation capabilities, product reliability, machine versatility, and after-sales support. Market leaders are distinguished by their strong R&D capabilities, global distribution networks, and broad product portfolios catering to varied industry applications including packaging, publishing, signage, and electronics.

Recent years have seen an uptick in strategic collaborations and mergers aimed at expanding geographical presence and integrating smart technologies. Key players are increasingly focusing on the integration of AI, IoT, and cloud-based analytics into laminators, enabling real-time monitoring, predictive maintenance, and defect detection. Innovation in eco-friendly adhesives and recyclable laminate films has also driven new product development. Additionally, companies are launching modular systems that allow end-users to customize laminator configurations for specific substrates and production lines. Competition is intensifying in Asia-Pacific and North America due to rising investments in automation and sustainability.

Komfi spol. s r.o.

GMP Co., Ltd.

D&K Group

Shanghai Dragon Printing Machinery Co., Ltd.

TAULER Laminating Tech

Vivid Laminating Technologies

Kompac Technologies, LLC

YDF Machinery

ROLLLAM Machinery Co., Ltd.

Hangzhou Kangdexin Machinery Manufacturing Co., Ltd.

Morgana Systems Ltd.

Autobond Ltd.

Tamerica Products, Inc.

Technological advancements in the Automatic Laminators Market are reshaping equipment performance, efficiency, and application versatility. One of the most significant trends is the integration of AI-based control systems for intelligent automation. These systems allow real-time defect tracking, pressure adjustments, and energy optimization, enhancing both operational uptime and product consistency.

IoT-enabled laminators are gaining traction, providing end-users with remote diagnostics, usage analytics, and maintenance scheduling. Manufacturers are embedding sensors and edge computing modules to collect machine-level data, which is then used for performance benchmarking and predictive maintenance. This significantly reduces downtime and improves cost efficiency for high-volume production facilities.

Another important advancement is the use of environmentally friendly laminating films and adhesives, driven by global sustainability regulations. Machines are being adapted to support biodegradable substrates, solvent-free adhesives, and recyclable film materials. Additionally, the adoption of modular design architecture in laminating systems allows flexibility in upgrading or customizing machine parts based on production needs.

In high-precision industries such as electronics, thermal laminators with micron-level accuracy are now being deployed. These systems offer advanced tension control and automated alignment systems to meet stringent performance specifications. As digital printing continues to evolve, laminators are also being optimized to handle variable data formats and on-demand print volumes, ensuring compatibility with short-run, high-speed printing setups.

• In March 2024, Komfi introduced the Amiga 52 Double, an advanced dual-sided laminator designed for short-run digital printers. The system features intelligent sheet detection and dual hot roller technology, increasing throughput by over 35%.

• In September 2023, GMP Co., Ltd. unveiled a new eco-laminating machine line compatible with biodegradable films. These models are optimized for food and pharma packaging applications requiring strict compliance with environmental regulations.

• In February 2024, Shanghai Dragon Printing Machinery launched an IoT-enabled laminator featuring real-time diagnostics and cloud-based process tracking. Early deployments report a 28% reduction in machine downtime.

• In December 2023, TAULER Laminating Tech expanded its presence in South America through a strategic partnership, enabling localized support and installation of its compact automatic laminators for commercial print houses.

The Automatic Laminators Market Report provides a comprehensive analysis of the global landscape, focusing on key market segments, regional dynamics, technological innovations, and competitive strategies. It explores the segmentation by type, including thermal, pressure-sensitive, cold, and digital laminators; application areas, such as packaging, printing, signage, and electronics; and end-user verticals, ranging from commercial printers and packaging manufacturers to electronics and educational institutions.

Geographically, the report covers insights across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with country-level analysis for top contributors such as China, the U.S., India, and Germany. It outlines regional production trends, adoption rates, and regulatory frameworks shaping investment patterns.

The report also delves into technological evolution, detailing the integration of AI, IoT, modular designs, and sustainability-compliant materials into modern laminator systems. Furthermore, it highlights areas of emerging demand, including smart packaging, short-run digital printing, and eco-friendly lamination solutions.

Strategic insights on recent product launches, facility expansions, digital transformation initiatives, and market positioning of key players provide decision-makers with actionable intelligence for future planning, investment evaluation, and competitive benchmarking.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 210.0 Million |

| Market Revenue (2032) | USD 334.7 Million |

| CAGR (2025–2032) | 6.0% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Market Dynamics, Growth Drivers & Restraints, Technology Insights, Trends, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Komfi spol. s r.o., GMP Co., Ltd., D&K Group, Shanghai Dragon Printing Machinery Co., Ltd., TAULER Laminating Tech, Vivid Laminating Technologies, Kompac Technologies, LLC, YDF Machinery, ROLLLAM Machinery Co., Ltd., Hangzhou Kangdexin Machinery Manufacturing Co., Ltd., Morgana Systems Ltd., Autobond Ltd., Tamerica Products, Inc. |

| Customization & Pricing | Available on Request (10% Customization is Free) |