Reports

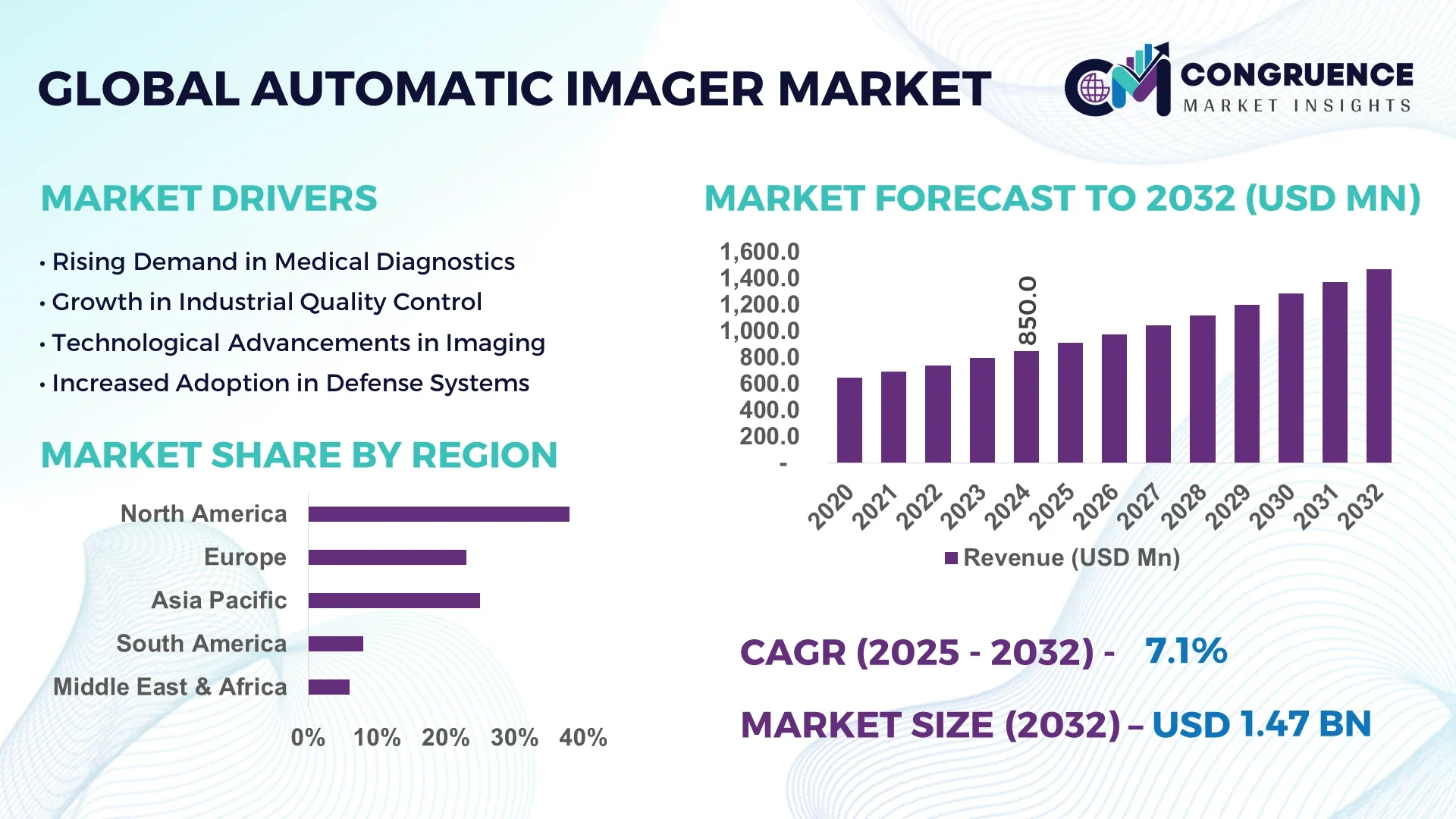

The Global Automatic Imager Market was valued at USD 850.0 Million in 2024 and is anticipated to reach a value of USD 1,471.4 Million by 2032 expanding at a CAGR of 7.1% between 2025 and 2032.

To Learn More About This Report, Request A Free Sample Copy

North America dominates the Automatic Imager Market due to its advanced healthcare infrastructure and strong adoption of cutting-edge imaging technologies. The presence of major market players and extensive research activities in medical diagnostics significantly contribute to the region's leadership. Continuous investments in innovation and favorable government initiatives to enhance healthcare capabilities further consolidate this dominance.

The Automatic Imager Market is characterized by rapid technological advancements that improve image resolution, speed, and automation. Applications span from medical diagnostics and pharmaceuticals to industrial inspection and automotive manufacturing. Increasing demand for precise imaging solutions in cancer detection, cell analysis, and quality control drives market expansion. Moreover, integration with robotics and AI enhances operational efficiency and accuracy, enabling real-time decision-making and data analysis. The market also benefits from growing investments in R&D and rising adoption in emerging markets. Continuous innovation in sensor technology, software algorithms, and cloud-based imaging platforms is shaping the future landscape of the Automatic Imager Market.

Artificial Intelligence (AI) is revolutionizing the Automatic Imager Market by enhancing image processing capabilities and automating complex analyses. AI algorithms enable high-throughput image acquisition and interpretation, reducing human error and increasing consistency in results. Deep learning models assist in detecting subtle patterns within images, which improves diagnostic accuracy and speeds up the workflow in clinical and industrial applications. Moreover, AI-powered image enhancement techniques improve clarity and resolution, enabling more detailed visualization without requiring expensive hardware upgrades.

AI facilitates predictive maintenance for imaging equipment by analyzing operational data, thereby minimizing downtime and maintenance costs. The integration of AI with cloud platforms allows for scalable image data storage and remote access, supporting collaborative research and telemedicine. Automated classification and segmentation of images using AI accelerate drug discovery and cell biology research by efficiently identifying cellular structures and anomalies. Furthermore, AI-driven analytics provide actionable insights from vast imaging datasets, supporting personalized medicine and quality assurance in manufacturing processes. These advancements have resulted in improved throughput, cost savings, and new application possibilities within the Automatic Imager Market.

“In 2024, a major breakthrough occurred with the deployment of AI-enabled automatic imaging platforms that reduced image processing time by up to 40%, enhancing real-time diagnostics and industrial inspection efficiency.”

The rising demand for high-precision and high-throughput imaging solutions across healthcare, pharmaceuticals, and industrial sectors is a primary driver. Advances in imaging technologies enable better disease diagnosis, improved drug development processes, and enhanced quality control in manufacturing. These factors stimulate market growth by encouraging the adoption of automatic imagers that offer superior accuracy and efficiency.

The substantial upfront cost of acquiring advanced automatic imaging systems, coupled with ongoing maintenance expenses, restrains market growth. Small and medium-sized enterprises often face budget constraints that limit their ability to adopt these technologies. Additionally, the complexity of operation and need for skilled personnel further restrict widespread implementation in certain regions and industries.

Emerging markets present lucrative opportunities due to increasing healthcare infrastructure investments and industrial modernization efforts. Growing awareness and demand for automated imaging solutions in countries across Asia-Pacific, Latin America, and the Middle East are expanding the customer base. The rising prevalence of chronic diseases and industrial automation initiatives further enhance the growth potential in these regions.

Integrating automatic imaging systems with legacy infrastructure and diverse software platforms poses a significant challenge. Compatibility issues can lead to increased costs, delays in deployment, and suboptimal system performance. Additionally, data security concerns and compliance with regional regulatory standards complicate market adoption, requiring ongoing adaptation and customization by vendors.

Rise in Modular and Prefabricated Construction: The adoption of modular design in automatic imaging equipment manufacturing is streamlining production and reducing lead times. Prefabricated components allow for easier upgrades and customization, meeting the specific needs of different industry verticals.

Integration of AI and Machine Learning: Increasing integration of AI-driven analytics and machine learning models within automatic imagers is enhancing image processing speed and accuracy, facilitating more informed decision-making in clinical diagnostics and industrial quality control.

Growth of Cloud-Based Imaging Platforms: Cloud-enabled imaging systems provide scalable storage and facilitate remote access, enabling collaborative research and telehealth applications. This trend is particularly prominent in healthcare institutions looking to improve data accessibility and security.

Focus on Miniaturization and Portability: Development of compact, portable automatic imagers is expanding their application range, including point-of-care diagnostics and field inspections. Portable devices offer flexibility and real-time imaging capabilities outside traditional laboratory settings, fostering market expansion globally.

The Automatic Imager Market is segmented based on type, application, and end-user, offering diverse insights into industry dynamics. Types include optical imagers, X-ray imagers, and thermal imagers, each catering to different imaging needs. Applications span healthcare diagnostics, industrial inspection, automotive, and defense sectors, highlighting the versatility of automatic imaging technologies. End-users range from hospitals and research laboratories to manufacturing units and government agencies, reflecting broad adoption. This segmentation helps in understanding market demands, technological advancements, and user preferences, enabling stakeholders to tailor strategies for targeted growth.

The Automatic Imager Market by type includes optical imagers, X-ray imagers, thermal imagers, and others. Optical imagers currently lead the market due to their widespread use in medical diagnostics, microscopy, and quality control, accounting for over 40% of total market revenue. Their ability to provide high-resolution and color-accurate images makes them preferred in clinical and industrial environments. Thermal imagers are the fastest-growing segment, driven by expanding applications in industrial maintenance, security, and automotive sectors, where non-contact temperature measurement is critical. These imagers help in early fault detection and preventive maintenance, reducing downtime and costs. X-ray imagers hold a significant share, especially in healthcare and material testing, owing to their capability for detailed internal imaging. Each segment's growth is propelled by increasing technological integration and expanding application fields.

Applications of Automatic Imagers cover healthcare diagnostics, industrial inspection, automotive, aerospace, and defense. Healthcare diagnostics dominate the market, representing more than 50% of the application revenue, due to the critical need for accurate imaging in disease detection, treatment planning, and research. Rapid advances in imaging technologies have enhanced diagnostic precision, leading to increased adoption in hospitals and clinics globally. Industrial inspection is the fastest-growing application segment, driven by rising automation and quality control demands in manufacturing, electronics, and energy sectors. Automatic imagers enable defect detection, process monitoring, and compliance with safety standards. The automotive sector also shows robust growth, integrating imaging for driver assistance and vehicle safety systems. Expanding use in aerospace and defense for surveillance and maintenance further diversifies application opportunities.

The Automatic Imager Market serves end-users such as hospitals, research institutes, manufacturing industries, and government agencies. Hospitals lead the market, contributing approximately 55% of total revenue, fueled by rising healthcare expenditures and increasing demand for advanced diagnostic tools. Research institutes are rapidly growing as end-users due to their continuous need for high-precision imaging in biological studies and drug development. Manufacturing industries represent a substantial segment, leveraging automatic imagers for quality control, defect detection, and process optimization, which enhances production efficiency. Government and defense agencies utilize imaging technologies for surveillance, security, and infrastructure inspection, with increased investments supporting market expansion. Each segment’s growth is influenced by evolving technological requirements and increasing automation trends across sectors.

North America accounted for the largest market share at 38% in 2024; however, the Asia-Pacific region is expected to register the fastest growth, expanding at a CAGR of 8.5% between 2025 and 2032.

To Learn More About This Report, Request A Free Sample Copy

North America’s dominance is driven by advanced healthcare infrastructure and early adoption of cutting-edge imaging technologies. Europe follows closely with significant investments in medical research and industrial automation. Meanwhile, Asia-Pacific benefits from rapid industrialization, growing healthcare expenditure, and increasing adoption of automatic imaging systems in countries like China and India. South America and the Middle East & Africa regions are emerging markets showing steady demand due to expanding healthcare facilities and industrial modernization efforts.

Innovation and Integration Lead North America’s Growth

North America’s Automatic Imager Market is characterized by a strong focus on innovation and integration of AI technologies into imaging systems. The U.S. leads the region with widespread use of automatic imagers in healthcare diagnostics and industrial applications, accounting for nearly 25% of the global market share. Canada contributes significantly through investments in biomedical research and industrial inspection automation. The demand for portable and cloud-enabled imaging devices is rising, supporting telehealth and remote diagnostics. Meanwhile, government initiatives promoting smart manufacturing and digital healthcare are accelerating adoption across the region.

Sustainability and Precision Drive European Market

Europe emphasizes precision imaging combined with sustainable manufacturing practices. Germany and the UK lead with robust investments in healthcare imaging solutions and industrial automation, collectively representing around 18% of the global market. The region sees increased deployment of thermal and optical imagers for energy-efficient industrial processes and advanced medical diagnostics. European regulatory frameworks prioritize patient safety and data privacy, shaping product innovation and market strategies. Additionally, rising demand for automated quality control in automotive and aerospace sectors is fueling growth in imaging applications.

Rapid Industrialization and Healthcare Expansion in Asia-Pacific

Asia-Pacific is experiencing rapid growth driven by industrial modernization and expanding healthcare infrastructure. China and India dominate the region with a combined market share of over 20% in automatic imagers. The region witnesses increased use of automatic imaging for pharmaceutical manufacturing, disease diagnosis, and automotive safety. Growing urbanization and government funding to upgrade healthcare facilities are key contributors. Additionally, rising adoption of AI-powered imaging solutions in industrial inspection and research accelerates market expansion. The demand for affordable, portable automatic imagers is also growing to meet the needs of remote and rural areas.

Healthcare Modernization and Industrial Automation Spur Growth

South America’s market growth is led by Brazil and Argentina, which hold the largest shares in the region. The increasing focus on healthcare modernization drives demand for advanced diagnostic imaging, accounting for approximately 5% of the global market. Industrial sectors are gradually adopting automatic imaging for quality control and infrastructure inspection. The trend toward telemedicine and digital healthcare solutions further boosts demand. Despite slower adoption compared to other regions, investments in manufacturing automation and healthcare facility upgrades are creating new opportunities for market players.

Emerging Healthcare and Security Needs Fuel Demand

The Middle East & Africa region shows rising adoption of automatic imagers, driven by expanding healthcare infrastructure and heightened security concerns. The UAE and Saudi Arabia lead regional demand, focusing on medical imaging, industrial inspection, and surveillance applications. Investments in smart city projects and digital health initiatives contribute to market growth. Increasing government focus on healthcare quality and safety standards encourages deployment of advanced imaging technologies. Additionally, the region is witnessing growing interest in portable imaging devices for remote diagnostics and on-site industrial inspections, enhancing market penetration.

United States - holds the highest market share at USD 323 Million, driven by advanced healthcare infrastructure and strong R&D in imaging technologies.

China - follows with USD 210 Million, supported by rapid industrialization, growing healthcare investments, and increasing adoption of automated imaging systems in multiple sectors.

The Automatic Imager Market is highly competitive, characterized by a mix of established multinational corporations and emerging technology firms. Key players focus on innovation, product diversification, and strategic partnerships to maintain their market position. Investment in R&D has led to advancements such as AI integration, enhanced image resolution, and faster processing speeds. Companies are also prioritizing the development of portable and user-friendly devices to expand application across healthcare, industrial, and defense sectors. Competitive pricing strategies and expansion into emerging markets further intensify rivalry. Collaborations with technology providers and healthcare institutions enable players to tailor solutions for specific end-user requirements, fueling continuous product improvements. Market leaders dominate with extensive distribution networks and strong brand recognition, which act as significant barriers for new entrants.

Canon Inc.

FLIR Systems, Inc.

Teledyne Technologies Incorporated

Hamamatsu Photonics K.K.

Leica Microsystems

Olympus Corporation

Sony Corporation

GE Healthcare

Samsung Electronics

Nikon Corporation

Technological advancements are shaping the Automatic Imager Market with significant strides in sensor technology, AI-driven image processing, and miniaturization. The integration of deep learning algorithms enhances image accuracy and interpretation, enabling real-time analysis in medical diagnostics and industrial inspections. Advances in CMOS and CCD sensor technologies have improved sensitivity and resolution, facilitating clearer and more precise images across diverse applications. Additionally, developments in 3D imaging and hyperspectral imaging allow for comprehensive analysis beyond traditional 2D images, benefiting sectors like defense and quality control. Portable and handheld automatic imagers are becoming increasingly popular due to their ease of use and mobility, particularly in remote healthcare and field inspections. Cloud connectivity and IoT integration also enable seamless data sharing and remote monitoring, supporting telemedicine and automated manufacturing systems. The continuous improvement of software platforms paired with hardware innovations is expanding the capabilities and adoption of automatic imagers globally.

In February 2024, Canon Inc. launched the EOS R7 Mark II, featuring advanced automatic imaging with improved autofocus and image stabilization, enhancing performance in medical and industrial imaging applications.

In August 2023, FLIR Systems introduced the FLIR A500-EST, a thermal imaging camera designed for industrial monitoring with enhanced temperature accuracy and rugged design for harsh environments.

In November 2023, Sony Corporation unveiled the IMX700 series image sensors optimized for automatic imagers, delivering ultra-high resolution and low noise for healthcare diagnostics and security surveillance.

In April 2024, GE Healthcare released its Revolution Apex CT scanner with integrated automatic imaging software, enabling faster scan times and improved image reconstruction for diagnostic clarity.

The scope of the Automatic Imager Market Report encompasses a detailed analysis of market trends, segmentation, regional insights, and competitive landscape, aimed at providing stakeholders with actionable intelligence. It covers various types of automatic imagers including optical, thermal, and X-ray systems, along with their applications across healthcare, industrial inspection, automotive, and defense sectors. The report highlights technological innovations, regulatory frameworks, and end-user adoption patterns that influence market dynamics. Geographic segmentation includes key regions such as North America, Europe, Asia-Pacific, South America, and Middle East & Africa, offering comprehensive coverage of emerging and established markets. Additionally, the report discusses market drivers, restraints, opportunities, and challenges to equip businesses with strategic foresight. It serves as a critical tool for manufacturers, investors, and policymakers to understand competitive positioning and identify growth avenues in the rapidly evolving automatic imager market.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Name | Global Automatic Imager Market |

| Market Revenue (2024) | USD 850.0 Million |

| Market Revenue (2032) | USD 1,471.4 Million |

| CAGR (2025–2032) | 7.1% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape, Technological Insights, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Canon Inc., FLIR Systems, Inc., Teledyne Technologies Incorporated, Hamamatsu Photonics K.K., Leica Microsystems, Olympus Corporation, Sony Corporation, GE Healthcare, Samsung Electronics, Nikon Corporation |

| Customization & Pricing | Available on Request (10% Customization is Free) |