Reports

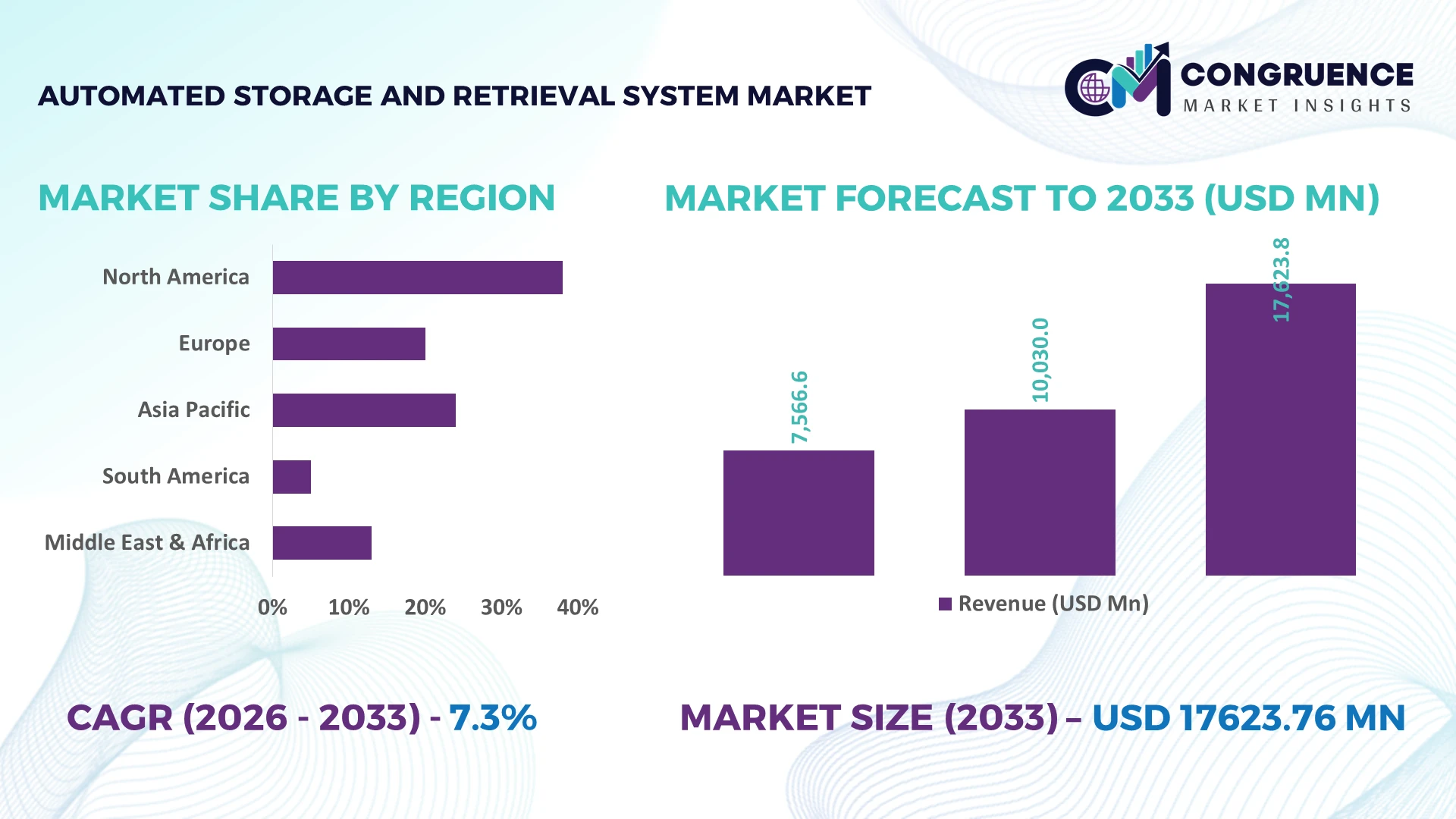

The Global Automated Storage and Retrieval System Market was valued at USD 10030 Million in 2025 and is anticipated to reach a value of USD 17623.76 Million by 2033 expanding at a CAGR of 7.3% between 2026 and 2033. AI-powered warehouse management, high-density storage deployment, and expanding automated fulfillment infrastructure across manufacturing and logistics facilities are accelerating market growth while improving inventory accuracy and operational productivity.

China dominates the global Automated Storage and Retrieval System Market with approximately 31% of total automated warehouse installations, supported by large-scale investments in electronics, automotive, and e-commerce logistics. More than 55% of newly commissioned large distribution centers deploy intelligent storage automation, compared with around 24% in India. Ongoing supply-chain diversification following global manufacturing realignment continues to strengthen automation investments across Asia, reinforcing regional production resilience and warehouse modernization.

Businesses investing in scalable automated storage infrastructure are strengthening inventory visibility, warehouse efficiency, and long-term supply-chain competitiveness.

Market Size & Growth: USD 10030 Million in 2025, projected to reach USD 17623.76 Million by 2033 at a CAGR of 7.3%, driven by AI-enabled warehouse automation and intelligent fulfillment expansion.

Top Growth Drivers: E-commerce warehouse automation (+42%), robotics deployment (+35%), and manufacturing digitalization (+29%) continue accelerating global market expansion.

Short-Term Forecast: By 2028, automated facilities reduce warehouse operating costs by 22% while increasing order fulfillment efficiency by more than 30%.

Emerging Technologies: AI-driven warehouse software, autonomous mobile robots, and digital twin platforms improve storage density, inventory visibility, and predictive operations.

Regional Leaders: Asia-Pacific exceeds USD 7.2 billion, North America reaches nearly USD 4.8 billion, and Europe surpasses USD 3.9 billion as regional automation investments expand alongside supply-chain diversification.

Consumer/End-User Trends: Nearly 68% of large distribution centers prioritize automated storage systems to improve same-day fulfillment performance and inventory accuracy.

Pilot/Case Example: A 2026 automated distribution center deployment increased storage capacity by 35% and reduced order processing time by 28% through AI-controlled retrieval systems.

Competitive Landscape: Leading suppliers collectively hold approximately 38% market share, with competition centered on intelligent software integration, modular systems, and warehouse robotics innovation.

Regulatory & ESG Impact: Energy-efficient warehouse automation reduces electricity consumption by up to 18% while supporting industrial sustainability and operational compliance initiatives.

Investment & Funding: More than USD 5 billion in automation investments supports warehouse expansion, strategic partnerships, robotics integration, and advanced logistics infrastructure worldwide.

Innovation & Future Outlook: AI-powered orchestration, cloud-connected warehouse control, and next-generation robotic storage systems are reshaping global automated logistics strategies amid continued supply-chain transformation.

The Automated Storage and Retrieval System Market continues to expand across e-commerce, automotive, pharmaceuticals, and cold-chain logistics, where intelligent storage optimization and AI-based warehouse control improve throughput and inventory precision. More than 40% of new large warehouse projects incorporate advanced automation technologies as businesses strengthen operational resilience amid evolving supply-chain requirements, creating a strong foundation for the strategic market assessment that follows.

The Automated Storage and Retrieval System Market has become strategically important as manufacturers, retailers, and logistics operators compete on inventory speed, warehouse density, and fulfillment accuracy rather than warehouse size alone. Supply-chain restructuring after global trade disruptions has accelerated investment in intelligent distribution infrastructure, while digital warehouse platforms are transforming inventory management into a real-time operational function. Businesses increasingly prioritize scalable automation to reduce labor dependency and improve throughput across high-volume facilities.

Modern AI-enabled automated storage and retrieval systems process up to 35% more orders and improve storage utilization by nearly 40% compared with conventional rack-and-forklift operations while reducing retrieval errors below 1%. Japan continues to lead precision automation deployment across manufacturing, whereas China scales large automated logistics parks to support expanding industrial output and cross-border commerce. During the next two to three years, over 45% of newly developed large warehouses are expected to integrate intelligent storage automation as warehouse digitalization becomes a standard investment priority.

A leading retail distribution operator deploying shuttle-based automated storage systems shortened order fulfillment cycles by 30% while increasing storage capacity by 28% without expanding floor space. Equipment suppliers are strengthening software partnerships, expanding robotics portfolios, and localizing manufacturing capabilities to improve deployment flexibility. Organizations that integrate intelligent storage automation with enterprise-wide digital operations will secure stronger competitive positioning, higher operational resilience, and sustainable logistics performance.

Rapid warehouse modernization is becoming the primary driver of Automated Storage and Retrieval System Market expansion as businesses optimize inventory accuracy, labor productivity, and space utilization. More than 62% of large distribution centers are investing in warehouse automation, while automated picking improves operational efficiency by approximately 30% and inventory accuracy exceeds 99%. Manufacturing expansion in China and semiconductor investments across Southeast Asia continue increasing demand for high-density storage infrastructure. In response, solution providers are expanding robotics manufacturing, integrating AI-based warehouse software, and forming strategic partnerships with system integrators. Companies deploying modular automated storage platforms achieve faster warehouse commissioning while creating scalable logistics networks capable of supporting fluctuating order volumes and complex fulfillment requirements.

High capital expenditure and integration complexity continue limiting deployment across medium-sized warehouses operating with legacy infrastructure. Nearly 45% of existing facilities require structural modifications before automation implementation, while integration costs account for approximately 25% of total project expenditure. Dependence on imported automation components also creates procurement uncertainty during global supply-chain disruptions, particularly for advanced controllers and precision robotics. Companies are reducing implementation risks through localized manufacturing, multi-supplier procurement strategies, and phased modernization programs that preserve existing warehouse operations. Standardized control architectures and interoperable software platforms are becoming essential for improving scalability while reducing long-term deployment costs and operational disruption.

Artificial intelligence, digital twins, and autonomous warehouse orchestration are creating new opportunities beyond traditional storage automation. AI-assisted warehouse scheduling can increase equipment utilization by approximately 27%, while predictive maintenance reduces unexpected downtime by nearly 22%. India is witnessing accelerated investment in automated logistics parks as industrial corridors and manufacturing clusters expand. Companies are increasing R&D spending, collaborating with robotics developers, and integrating cloud-based warehouse management systems into broader industrial ecosystems. The strongest long-term opportunity lies in combining automated storage, intelligent robotics, and real-time analytics to deliver highly adaptive fulfillment networks capable of supporting omnichannel logistics and resilient manufacturing operations.

Scaling automated storage infrastructure across multi-site warehouse networks remains a significant execution challenge due to software interoperability, cybersecurity, and skilled workforce limitations. Around 38% of industrial facilities report integration difficulties between warehouse management systems and legacy enterprise software, while cybersecurity incidents affecting industrial automation environments have increased by approximately 20% in recent years. Germany's advanced manufacturing sector is prioritizing secure industrial connectivity and standardized automation protocols to address these issues. Companies must strengthen cybersecurity frameworks, invest in workforce training, and expand partnerships with software specialists to ensure consistent automation performance while maintaining long-term operational resilience and competitive efficiency.

Warehouse Robotics Scaling Rapidly AI-enabled robotic storage systems are becoming standard in large fulfillment facilities, with robotic picking deployment increasing by approximately 34% and storage density improving by nearly 38%. Persistent labor shortages and faster delivery expectations are driving adoption. Companies are expanding robotics partnerships, standardizing modular system designs, and integrating warehouse execution software to accelerate deployment while reducing manual intervention across high-volume logistics operations.

Software-Defined Warehouse Operations Cloud-connected warehouse control platforms and digital twin technology are transforming operational visibility. More than 48% of newly automated facilities deploy predictive warehouse software, reducing equipment downtime by about 22% while improving inventory synchronization by nearly 30%. Japanese manufacturers and logistics providers are increasing software integration investments to optimize multi-site warehouse performance through centralized control and real-time operational analytics.

Cold Chain Automation Expansion Pharmaceutical and temperature-controlled food logistics are accelerating automated storage deployment, with automated cold-storage capacity increasing by approximately 27% and product traceability improving by over 35%. Stricter handling requirements and quality compliance are reshaping warehouse operations. Equipment suppliers are developing energy-efficient shuttle systems, automated retrieval technologies, and specialized storage solutions to strengthen operational reliability in temperature-sensitive environments.

Localized Automation Manufacturing Supply-chain diversification is encouraging localized production of warehouse automation equipment, reducing average project lead times by approximately 18% while component localization has increased by nearly 25% in selected manufacturing hubs. Rather than relying solely on imported systems, companies are restructuring supplier networks, expanding regional assembly operations, and strengthening technology partnerships to improve deployment flexibility and reduce procurement risks.

Unit Load Systems remain the leading segment because they efficiently manage heavy palletized goods, maximize warehouse throughput, and integrate seamlessly with automated distribution centers. Nearly 46% of large automated warehouse projects continue to prioritize Unit Load Systems due to their scalability, high storage density, and compatibility with AI-enabled warehouse management platforms. Shuttle Systems represent the fastest-growing segment as e-commerce fulfillment centers increasingly require flexible, high-speed storage capable of supporting rapid order processing. Shuttle deployments have expanded by approximately 32% as businesses modernize fulfillment operations.

Mini Load Systems maintain strong adoption across electronics, pharmaceuticals, and precision manufacturing where compact storage and high retrieval accuracy are essential. Vertical Lift Modules continue gaining traction in facilities with limited floor space by improving vertical storage utilization by nearly 40%, while Carousel Systems remain strategically important for medium-volume inventory operations requiring ergonomic product access. Manufacturers are expanding modular product portfolios, strengthening automation software integration, and collaborating with warehouse solution providers to meet increasingly specialized customer requirements. Investment priorities continue shifting toward intelligent, scalable storage technologies that deliver operational flexibility and lower lifecycle costs.

Warehousing represents the largest application segment as enterprises continue modernizing distribution infrastructure to improve storage density, inventory visibility, and operational efficiency. Approximately 52% of new automated warehouse investments are concentrated in large storage facilities supporting manufacturing and retail supply chains. Order Fulfillment is the fastest-growing application, driven by expanding omnichannel commerce and same-day delivery expectations, with automated fulfillment capacity increasing by roughly 34% across high-volume logistics operations.

Inventory Management continues evolving through AI-enabled stock optimization and real-time warehouse analytics that improve inventory accuracy beyond 99%. Manufacturing facilities increasingly deploy automated storage systems to synchronize production with internal material movement, while Cold Storage applications are expanding rapidly across pharmaceutical and food industries to strengthen traceability and temperature-controlled logistics. Solution providers are scaling cloud-based warehouse platforms, integrating robotics, and expanding implementation partnerships to improve deployment efficiency. Demand is steadily shifting toward highly automated warehouse ecosystems capable of supporting resilient, data-driven supply-chain operations.

E-commerce remains the dominant end-user segment as high-volume fulfillment operations require intelligent storage, rapid picking, and continuous inventory synchronization. Nearly 58% of newly commissioned large automated fulfillment centers primarily support online retail operations where delivery speed directly influences customer satisfaction. Healthcare is emerging as the fastest-growing end-user segment, with automated pharmaceutical storage deployments increasing by approximately 29% as hospitals and medical distributors strengthen inventory traceability and regulatory compliance.

Manufacturing continues investing in automated storage systems to improve production flow and reduce internal material handling delays, while Retail organizations expand automation to support omnichannel distribution and store replenishment. Food & Beverage companies increasingly deploy automated cold-storage technologies to improve product handling, quality assurance, and operational consistency. Equipment suppliers are introducing industry-specific system configurations, expanding strategic partnerships, and offering modular automation platforms that simplify deployment across diverse operating environments. Competitive positioning increasingly depends on customized automation solutions aligned with sector-specific operational requirements.

Asia-Pacific accounted for the largest market share at 43.8% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.1% between 2026 and 2033.

Advanced Fulfillment Automation Driving Enterprise Expansion

North America remains a highly mature Automated Storage and Retrieval System Market, supported by large-scale warehouse modernization, advanced robotics integration, and extensive e-commerce infrastructure. The region represents approximately 27% of global automated warehouse deployments, with retailers, third-party logistics providers, and manufacturers accelerating intelligent storage investments. AI-enabled warehouse execution systems and autonomous material handling continue improving fulfillment performance while reducing labor dependency. During 2026, several logistics operators expanded automated distribution facilities capable of increasing storage density by nearly 30%. Technology vendors are strengthening partnerships with robotics developers and software providers to deliver integrated warehouse automation platforms that improve operational flexibility and inventory precision.

United States Market Outlook: The United States leads regional deployment through its extensive logistics infrastructure, advanced manufacturing base, and strong investment in warehouse digitalization. More than 65% of newly constructed large fulfillment facilities incorporate automated storage technologies integrated with robotics and warehouse management software. Major enterprises continue prioritizing scalable automation, modular system architecture, and AI-driven inventory optimization to improve order fulfillment efficiency while supporting increasingly complex omnichannel distribution networks.

Industrial Modernization Strengthening Intelligent Warehousing

Europe continues expanding automated storage deployment through advanced manufacturing modernization, sustainability initiatives, and smart logistics infrastructure. The region contributes nearly 24% of global automated warehouse installations, supported by automotive, pharmaceutical, and industrial manufacturing sectors. Energy-efficient automation technologies and digital warehouse platforms are becoming standard across new industrial facilities. Multiple warehouse modernization projects completed during 2026 improved operational throughput by approximately 24% while reducing warehouse energy consumption through optimized storage workflows. Equipment suppliers continue investing in modular automation systems that align with industrial digitalization and environmental performance objectives.

Germany Market Outlook: Germany remains the regional technology leader because of its advanced manufacturing ecosystem, strong industrial automation expertise, and high concentration of warehouse equipment suppliers. Approximately 58% of newly automated manufacturing warehouses deploy integrated storage automation linked with Industry 4.0 production systems. Enterprises continue expanding intelligent logistics infrastructure while strengthening collaboration between robotics manufacturers, software developers, and industrial automation specialists.

Manufacturing Scale Accelerates Automation Leadership

Asia-Pacific dominates the Automated Storage and Retrieval System Market through extensive manufacturing capacity, expanding logistics infrastructure, and large-scale warehouse construction. The region accounts for approximately 43.8% of global market activity, supported by electronics, automotive, consumer goods, and e-commerce industries. Automated warehouse deployment continues accelerating as industrial operators increase investment in intelligent storage systems and robotics. During 2026, multiple industrial parks expanded automated logistics capacity, increasing warehouse throughput by approximately 33%. System manufacturers are localizing production, expanding engineering capabilities, and strengthening partnerships with regional logistics providers to support growing automation demand.

China Market Outlook: China leads the regional market through its unmatched manufacturing scale, extensive e-commerce ecosystem, and continuous logistics infrastructure expansion. Around 31% of global automated warehouse installations are concentrated in China, while intelligent distribution centers increasingly integrate AI-driven storage management and robotic retrieval technologies. Domestic equipment manufacturers continue expanding production capacity and exporting advanced warehouse automation solutions to strengthen international competitiveness.

Logistics Modernization Supporting Industrial Automation

South America is steadily adopting automated storage technologies as logistics operators modernize warehouse infrastructure and manufacturers improve supply-chain efficiency. The region contributes approximately 5% of global deployment activity, with adoption centered on retail distribution, food processing, and industrial manufacturing. Infrastructure limitations continue influencing implementation timelines, yet warehouse automation investments increased by roughly 18% during 2026 across major logistics facilities. Companies are prioritizing modular deployment strategies, localized engineering services, and phased automation programs that reduce operational disruption while improving warehouse productivity and inventory control.

Brazil Market Outlook: Brazil represents the largest market within South America due to its extensive industrial base, expanding retail logistics, and growing investment in fulfillment infrastructure. Automated warehouse deployment continues increasing across consumer goods and food distribution networks, with warehouse productivity improving by approximately 25% following intelligent storage implementation. Equipment providers are strengthening local partnerships and expanding technical support capabilities to accelerate project execution and long-term system reliability.

Infrastructure Investment Driving Warehouse Transformation

The Middle East & Africa market is advancing through logistics infrastructure expansion, industrial diversification, and smart warehouse development linked to economic transformation programs. The region contributes approximately 4% of global automated storage deployment, with demand concentrated in logistics hubs, ports, retail distribution, and food supply chains. During 2026, several integrated logistics projects expanded automated warehouse capacity by nearly 20%, improving cargo handling efficiency and inventory visibility. Technology providers are increasing regional partnerships, localized implementation capabilities, and system integration services to support modern distribution infrastructure and industrial development.

Saudi Arabia Market Outlook: Saudi Arabia leads regional adoption through large-scale logistics investments, industrial diversification initiatives, and rapidly expanding distribution infrastructure. Major warehouse developments increasingly incorporate automated storage technologies to support manufacturing, retail, and national logistics objectives. Government-backed industrial projects and private-sector partnerships continue accelerating intelligent warehouse deployment, positioning the country as a strategic automation hub for regional supply-chain operations.

The Automated Storage and Retrieval System Market is led by Daifuku, SSI SCHAEFER, Dematic, Swisslog, and Vanderlande, collectively holding approximately 47% of the global market. These global automation leaders compete directly with regional system integrators and lower-cost equipment manufacturers, while robotics specialists challenge established OEMs through AI-driven warehouse solutions. Competition is centered on intelligent software integration, deployment speed, and lifecycle performance rather than equipment pricing alone. AI-enabled warehouse platforms improve picking efficiency by nearly 30%, modular automation shortens installation time by approximately 25%, and predictive maintenance reduces downtime by around 20%, creating measurable differentiation. Companies are expanding manufacturing capacity, acquiring warehouse software capabilities, forming robotics partnerships, and vertically integrating controls, software, and service operations. The competitive landscape is shifting toward software-defined automation ecosystems where digital capabilities increasingly outweigh mechanical differentiation. High engineering expertise, long implementation cycles, and customer integration requirements remain significant entry barriers. Winning requires scalable automation platforms, strong software ecosystems, reliable execution, and long-term service capabilities that consistently outperform integrated competitors.

Daifuku Co., Ltd.

SSI SCHAEFER Group

Dematic

Swisslog

Vanderlande Industries

Murata Machinery, Ltd.

Honeywell Intelligrated

Mecalux S.A.

BEUMER Group

TGW Logistics Group

KNAPP AG

Bastian Solutions

Toyota Industries Corporation

Körber Supply Chain

Automated Storage and Retrieval System technology is rapidly shifting from mechanical automation toward intelligent, software-defined warehouse ecosystems. AI-driven warehouse management, machine vision, and autonomous mobile robots now coordinate storage, retrieval, and inventory movement through real-time analytics. Compared with conventional rule-based systems, AI-enabled platforms improve warehouse throughput by approximately 32% while reducing retrieval errors by nearly 28%. Around 48% of newly automated large-scale warehouses now deploy AI-assisted control platforms, enabling faster operational decisions and greater inventory visibility across complex logistics environments.

Emerging technologies including digital twins, predictive maintenance, cloud-native warehouse execution systems, and Industrial Internet of Things connectivity are improving equipment utilization and operational resilience. Predictive maintenance lowers unexpected downtime by roughly 22%, while digital twin simulation reduces commissioning time by approximately 18%. Large logistics operators and advanced manufacturers benefit most through synchronized warehouse operations, lower maintenance costs, and improved asset utilization. Companies increasingly integrate robotics, warehouse software, and enterprise planning platforms into unified automation architectures that strengthen operational flexibility.

Between 2026 and 2028, autonomous orchestration, edge AI computing, and collaborative warehouse robotics will become key competitive differentiators. Intelligent warehouse ecosystems are expected to exceed 60% adoption among newly constructed high-capacity fulfillment centers, enabling faster deployment, adaptive inventory optimization, and highly resilient logistics operations. Organizations investing early in integrated automation platforms will strengthen competitive positioning, reduce operating complexity, and accelerate digital warehouse transformation.

July 2025 – Swisslog partnered with Sumitomo Drive Technologies USA to modernize its Virginia warehouse using AutoStore automation and SynQ software. The project includes 14 autonomous robots and 22,872 storage bins, improving throughput while avoiding warehouse expansion and strengthening long-term fulfillment capacity.

September 2024 – AutoStore introduced its Multi-Temperature Solution, enabling automated storage across chilled and frozen environments within one integrated system. The innovation supports multiple temperature zones in a single installation, expanding warehouse automation opportunities for food and pharmaceutical supply chains.

February 2025 – Exotec launched its next-generation Skypod robot-based ASRS featuring integrated buffering, sequencing, and pick-and-pack functionality. The redesigned platform delivers higher storage density and improved operational performance, allowing distribution centers to consolidate automation within a single scalable system.

April 2026 – Swisslog completed deployment of an AutoStore ASRS for Satair's Singapore aerospace logistics hub. The installation operates with 23 robots and 60,000 bins, storing approximately 80% of small and medium-sized parts while improving fulfillment speed, resilience, and regional logistics scalability.

The report provides comprehensive coverage of the Automated Storage and Retrieval System Market across major system types, including Unit Load Systems, Mini Load Systems, Vertical Lift Modules, Carousel Systems, and Shuttle Systems. It evaluates key applications spanning warehousing, order fulfillment, inventory management, cold storage, and manufacturing while assessing demand across e-commerce, manufacturing, retail, healthcare, and food & beverage industries. Regional analysis covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, supported by operational trends, deployment patterns, technology adoption, and competitive benchmarking.

The study examines AI-enabled warehouse automation, robotics, digital twin technology, cloud-based warehouse management, machine vision, and predictive maintenance while highlighting deployment trends where intelligent automation exceeds 60% adoption in newly developed high-capacity logistics facilities. It delivers strategic insights into competitive positioning, expansion opportunities, investment priorities, partnership strategies, supply-chain modernization, emerging warehouse models, and technology-driven operational transformation, enabling informed business planning and long-term decision-making between 2026 and 2033.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 10030 Million |

Market Revenue in 2033 | USD 17623.76 Million |

CAGR (2026 - 2033) | 7.3% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Daifuku Co., Ltd., SSI SCHAEFER Group, Dematic, Swisslog, Vanderlande Industries, Murata Machinery, Ltd., Honeywell Intelligrated, Mecalux S.A., BEUMER Group, TGW Logistics Group, KNAPP AG, Bastian Solutions, Toyota Industries Corporation, Körber Supply Chain |

Customization & Pricing | Available on Request (10% Customization is Free) |