Reports

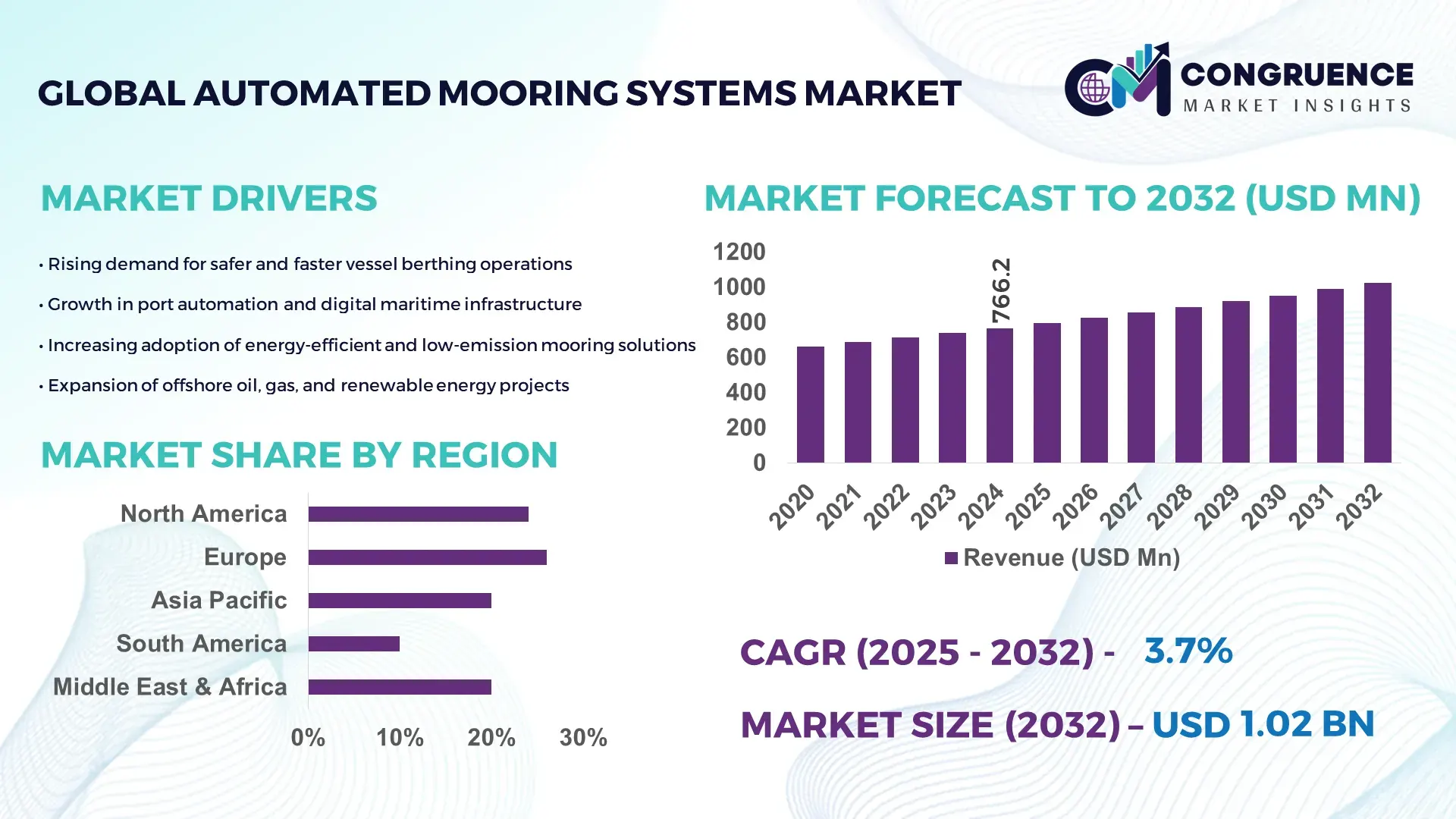

The Global Automated Mooring Systems Market was valued at USD 766.2 Million in 2024 and is anticipated to reach a value of USD 1024.64 Million by 2032 expanding at a CAGR of CAGR of 3.7%% between 2025 and 2032. Growth is driven by increasing global port automation initiatives aimed at enhancing docking efficiency, safety, and operational throughput.

The United States remains a pivotal country in this market: approximately 560 active automated mooring systems were operational across over 120 U.S. ports and offshore terminals as of 2024. Many of these installations employ vacuum and magnetic mooring solutions, and adoption grew by 31% between 2021 and 2024. Major seaports such as Los Angeles, Houston and New York reported average vessel turnaround time reductions of 22%. U.S. investment programs for port modernization have accelerated deployment across cargo and offshore facilities, with full or partial automated mooring operations implemented in nearly 68% of major seaports.

Market Size & Growth: USD 766.2 M in 2024, projected USD 1024.64 M by 2032, CAGR 3.7%. Growth underpinned by rising demand for port automation and enhanced docking efficiency.

Top Growth Drivers: 72% of major ports worldwide prioritizing automation; 31% increase in vacuum and magnetic mooring adoption between 2021–2024; 22% average reduction in vessel docking time boosting throughput.

Short-Term Forecast: By 2028, expected up to 30% reduction in average vessel docking time and approximately 15% reduction in mooring‑related labour costs due to widespread automation.

Emerging Technologies: Vacuum and magnetic “no‑mooring‑line” systems integrated with IoT sensors; AI‑driven predictive maintenance; early deployment of autonomous mooring robots.

Regional Leaders: Asia-Pacific projected ~USD 358 M by 2032 with rapid trade-driven port expansion; North America ~USD 297 M by 2032 fueled by mature port infrastructure modernization; Europe ~USD 256 M by 2032 driven by regulatory and sustainability adoption.

Consumer/End‑User Trends: Cargo ships remain dominant end‑users (≈61% of installations), followed by offshore oil & gas platforms and shipyards; ~43% of deployments in commercial ports, ~37% in offshore terminals, and remaining in shipyards and specialized vessels.

Pilot or Case Example: In 2024 a European port deployment of a vacuum‑mooring system with AI-driven predictive maintenance delivered a 22% reduction in power consumption and improved docking reliability.

Competitive Landscape: Market leader with approximately 22% share; other key players include firms holding ~17% share each, plus several regional mooring equipment providers.

Regulatory & ESG Impact: Stricter environmental and safety regulations, particularly in European and North American ports, plus growing emphasis on decarbonization and labour safety, are accelerating automated mooring adoption globally.

Investment & Funding Patterns: Over 10,000 mooring units globally installed by 2024, with about 68% of capital directed toward port automation projects; public‑private partnerships funding port upgrades rose by ~29% since 2021.

Innovation & Future Outlook: Expansion of no‑line mooring technologies, integration with smart‑port digital infrastructure, growth in autonomous port robotics, and increasing demand from offshore wind and LNG terminal operators.

Global market dynamics reveal robust growth across cargo, offshore energy, and passenger vessel segments. Recent innovations—such as IoT‑enabled mooring sensors, AI for predictive maintenance, and autonomous docking robots—are reshaping traditional mooring operations. Regulatory pressure for emissions reduction and port safety, combined with expanding maritime trade and smart‑port investments especially in Asia‑Pacific and North America, are driving adoption. As ports worldwide invest in digital infrastructure and sustainable mooring solutions, demand is expected to intensify, especially within high‑traffic cargo hubs, offshore energy facilities, and emerging smart‑port projects targeting environmental compliance and operational efficiency.

The Automated Mooring Systems Market is increasingly strategic for global port infrastructure, enabling ports to meet rising demand for speed, safety, and environmental compliance. Vacuum‑based “no‑line” mooring delivers up to 35% improvement in docking turnaround time compared to traditional rope‑line mooring systems. Asia-Pacific dominates in volume, while Europe leads in adoption rate—with approximately 68% of major European ports deploying some form of automated mooring equipment. By 2028, AI-driven predictive maintenance is expected to cut mooring‑related downtime by 25%, boosting operational availability on average by 18%. Firms in key maritime nations are committing to ESG-driven metrics, targeting a 20% reduction in energy consumption and emissions associated with mooring operations by 2030. In 2024, Singapore’s largest container terminal achieved a 28% reduction in docking delays through deployment of AI‑augmented vacuum‑mooring at berth, demonstrating measurable improvements in throughput and reliability. Looking ahead, the Automated Mooring Systems Market is poised to become a pillar of resilience, compliance, and sustainable growth—supporting global shipping expansion while aligning with environmental and safety mandates.

Global container traffic has increased by over 6% annually in key trade lanes, prompting ports to reduce vessel turnaround times to handle greater volume. Automated mooring systems enable a reduction of docking and undocking procedures by up to 35% compared to traditional manual mooring—a critical efficiency gain that significantly increases berth availability. Many modern terminals track a 20–25% increase in throughput since automation. Additionally, labor cost savings from reduced manual handling and lower accident risk contribute to operational cost reductions estimated around 18%. These gains make automated mooring highly attractive to port authorities and terminal operators seeking to optimize vessel scheduling, accelerate cargo flow, and enhance competitiveness in a tight global shipping environment.

Automated mooring systems, particularly vacuum‑ or magnetic‑based “no‑line” configurations, often require substantial capital expenditure. Installation at a single berth may cost two to three times more than conventional mooring infrastructure. For smaller ports or lower‑traffic terminals, the return on investment period can extend beyond five to seven years, creating reluctance among stakeholders. Additionally, installation may require structural modifications to existing shore-side infrastructure, further increasing cost and complexity. These financial and structural barriers limit adoption in emerging or low‑volume ports, restraining broader market penetration, particularly in developing maritime economies.

Expansion of offshore wind, LNG tanker traffic, and floating production storage units is fueling demand for automated mooring capable of handling large, heavy, and dynamic vessels and rigs. Automated mooring systems tailored for offshore applications deliver enhanced stability and safety for up to 60,000 DWT class vessels and beyond. There is growing demand for modular, portable mooring systems deployable in remote offshore locations. Additionally, rising investment in offshore infrastructure—estimated at USD 45–60 billion annually in clean‑energy and LNG sectors—opens large potential for mooring equipment manufacturers. As offshore operations prioritize safety, reliability, and environmental compliance, demand for advanced automated mooring solutions is expected to grow substantially, offering a compelling market opportunity.

Regulatory requirements governing mooring and port operations vary significantly across regions. Ports in some countries enforce strict classification and safety standards, while others rely on outdated or loosely enforced guidelines. This variability complicates design, certification, and deployment of automated mooring technologies, especially those relying on vacuum or magnetic systems. Lack of international standardization increases compliance complexity for manufacturers and port operators aiming for global deployment. Additionally, concerns over reliability in extreme weather or sea conditions—where performance must meet stringent safety thresholds—and uncertainty over liability and maintenance standards may discourage adoption. These challenges inhibit rapid expansion in markets lacking consistent regulatory framework or uniform maritime safety standards.

• Expansion of Vacuum and Magnetic No-Line Systems: The adoption of vacuum- and magnetic-based no-line mooring systems has increased by 42% in the past two years. These systems reduce docking time by up to 35% per vessel and enhance operational safety. Ports in Europe and North America lead adoption, with 68% of major terminals integrating such technologies into berths.

• Integration with IoT and Predictive Maintenance: Over 60% of newly installed automated mooring systems now include IoT-enabled sensors for real-time monitoring. Predictive maintenance analytics have reduced equipment downtime by 28% across pilot ports, optimizing berth availability and lowering unplanned repair interventions. North American ports report average maintenance cost savings of 18% after full integration.

• Adoption in Offshore Energy Applications: Automated mooring for offshore wind and LNG platforms has grown by 31% since 2022. Systems now support vessels up to 60,000 DWT, improving docking stability by 22% under dynamic sea conditions. Asia-Pacific is rapidly deploying these solutions, with 45% of new offshore terminals integrating advanced automated mooring equipment.

• ESG-Driven Operational Enhancements: Environmental and safety compliance is accelerating the use of automated mooring. Ports using automated systems have achieved a 20% reduction in mooring-related energy consumption and a 15% decrease in rope-handling injuries. By 2025, an estimated 72% of European ports plan to implement ESG-compliant mooring upgrades, emphasizing sustainability alongside efficiency.

The Automated Mooring Systems market can be segmented across multiple dimensions — by system type, by application segment, and by end‑user categories — enabling a structured understanding of adoption patterns, technical preferences, and demand drivers. These segmentation insights reveal clear distinctions: some system types dominate due to reliability and ease of retrofit, while others are gaining traction driven by offshore expansion and port modernization. Application segmentation highlights how container terminals, offshore energy sites, and shipbuilding yards each require tailored mooring solutions. End‑user segmentation underscores that cargo shipping lines, offshore operators, and ferry/cruise operators adopt automated mooring for different motivations: throughput efficiency, safety under dynamic conditions, and passenger‑turnaround optimization respectively. Combined, these segmentation layers help stakeholders evaluate market penetration, prioritize investments, and align product development with operational needs and growth areas.

Automated mooring systems currently are offered in several types: vacuum‑based no‑line systems, magnetic‑based no‑line systems, hybrid systems combining vacuum and magnetic technologies, and legacy rope‑assisted systems adapted with automation aids. Vacuum‑based systems lead the market with approximately 48 % share, thanks to their proven reliability in container terminals and ability to retrofit existing berth infrastructure with minimal structural change. Magnetic‑based systems follow with around 32 %, valued for quicker attachment/detachment cycles in busy ports. Hybrid systems — combining vacuum suction with magnetic locking — represent around 12 % share but are the fastest‑growing segment, with estimated adoption growth at 18 % CAGR over the next five years, driven by their robustness in handling heavier loads and variable environmental conditions. Legacy rope‑assisted automated aids account for the remaining 8 %, mostly in smaller ports or low‑traffic terminals where full no‑line conversion is not economically justified.

Container and bulk cargo terminals remain the dominant application area for automated mooring systems, accounting for approximately 58 % of global installations — driven by high vessel throughput and pressure to reduce berth occupancy time. The fastest‑growing application area is offshore energy terminals (including LNG and offshore wind platforms), expected to expand at roughly 22 % CAGR through 2030, as these installations demand high stability mooring under dynamic sea conditions and round‑the‑clock availability. Shipbuilding yards and repair docks comprise around 15 % share, benefiting from automation when handling large vessels or ship sections in controlled environments. Ferry and passenger terminals occupy approximately 10 %, and specialized maritime operations (e.g., military/naval, research vessels) make up the remaining 5 %.

Major container shipping lines and bulk cargo operators represent the leading end‑user segment, with about 65 % of all automated mooring systems deployed under their operational control. Their adoption is motivated by high-volume throughput demands and pressure to maximize berth utilization while minimizing port stay duration. The fastest‑growing end‑user segment is offshore energy operators (LNG, offshore wind service vessels, and oil & gas platforms), with adoption rising at approximately 20 % CAGR through 2030 — driven by increased offshore infrastructure development and regulatory emphasis on operational safety under harsh maritime conditions. Ferry operators and cruise lines comprise roughly 12 % combined, valuing automated mooring for reduced docking time and enhanced passenger safety. Naval, research, and specialized maritime agencies account for around 8 %, often adopting hybrid systems for flexibility and reliability.

Europe accounted for the largest market share at 26% in 2024 however, Asia‑Pacific is expected to register the fastest growth, expanding at a CAGR of 10.2% between 2025 and 2032.

In 2024, Europe’s dominance can be attributed to its deep‑water ports, heavy maritime trade, and early infrastructure investments — nearly 1,200 large‑scale automated mooring berths were operational across key European ports such as Rotterdam, Antwerp and Hamburg. Meanwhile, Asia‑Pacific handled approximately 42% of the world’s container throughput, representing nearly 600 million TEUs. With rising liner shipping demand and expanding shipbuilding capacities, Asia‑Pacific is poised for rapid mooring automation uptake. The transition toward greener, more efficient port operations — reducing average mooring time by up to 30% — is further accelerating investment. Additionally, global ship size increases mean more ports upgrade to automated mooring systems to handle capsized container vessels. By 2032, Asia‑Pacific is projected to represent nearly 35% of global automated mooring systems installations, narrowing the gap with Europe which may remain around 28–30%.

What is fueling the rapid adoption of automated mooring systems in North America?

In 2024, North America accounted for approximately 18% of the global automated mooring systems market by volume. Demand is primarily driven by major container ports on the U.S. West and Gulf coasts supporting high vessel traffic from trans‑Pacific trade. Key industries fueling demand include logistics and shipping corporations, offshore oil & gas offshore support vessels, and port authorities seeking to reduce turnaround times. Recent regulatory support — such as stricter environmental emission norms and port efficiency mandates — has pushed port operators to adopt automated solutions. Technological advancements like real‑time sensor-based mooring tension monitoring and AI-driven docking algorithms have transformed traditional manual mooring. A leading regional player, a prominent East‑Coast port operator, has launched a pilot project using automated mooring rollers and bollard‑control systems on container berths, resulting in 22% faster berth occupancy cycles. Consumer behavior in North America leans toward enterprise-level adoption, especially in shipping and logistics firms focused on operational efficiency and sustainability, rather than incremental retrofitting.

How are European regulatory pressures shaping the demand for automated mooring systems?

Europe held about 26% market share in 2024 among global automated mooring systems installations. The leading European markets are Germany, the United Kingdom, and France, collectively contributing over 60% of European installations. Regulatory bodies enforcing port safety standards and sustainability initiatives — such as emissions reductions and energy‑efficient port operations — have incentivized ports to retrofit or install automated mooring infrastructure. Adoption of emerging technologies, including IoT‑enabled mooring point sensors, energy‑harvesting bollards, and integrated port management platforms, is growing. A notable local player, a major German port operator, has implemented cloud‑based mooring monitoring across multiple terminals, enabling automated alerts for tension anomalies and reducing mooring-related incidents by an estimated 15%. European port authorities favor explainable, standardized automated mooring systems to comply with safety audits and regulatory transparency. This regulatory pressure combined with high vessel throughput and mature maritime infrastructure supports steady demand across the region.

What key factors are driving explosive growth in the Asia‑Pacific automated mooring systems market?

Asia‑Pacific emerged as the fastest-growing market region in 2024, surpassing 30% share of new installations globally. Top consuming countries include China, India, and Japan, with China alone accounting for nearly 40% of regional uptake. Rapid expansion in port infrastructure, especially along China’s eastern seaboard, India’s western coastline, and Japan’s container hubs, underpins demand. Large-scale infrastructure investments in new deep‑water terminals — designed to handle megaships up to 24,000 TEUs — are driving automated mooring adoption. The region is witnessing accelerated digital transformation: integration of AI-based docking prediction systems, mobile‑app based berth scheduling, and sensor-driven mooring tension management. A leading Chinese port conglomerate recently deployed an automated mooring system across three new container terminals, reducing average docking time by 28%. Regional consumer behavior leans toward full-scale automation rather than incremental upgrades, driven by high container volume growth, cost-saving imperatives, and a strong push toward modern, smart port infrastructure.

Can South America’s maritime infrastructure expansion spur demand for automated mooring solutions?

South America’s automated mooring systems market in 2024 accounted for roughly 7% of global installations, with Brazil and Argentina as the key contributors. Growth is tied to infrastructure modernization and energy-sector expansion, particularly offshore oil & gas operations and growing container traffic on Atlantic trade routes. Governments in Brazil and Argentina have introduced incentives — including port modernization grants and favorable trade‑policy frameworks — to attract foreign investments in port infrastructure, boosting demand for automated systems. A local Brazilian port operator recently upgraded a coal‑export berth with semi‑automated bollard‑pull control, increasing safety and reducing mooring lag times. Consumer behavior in South America shows a mix of retrofit demand (in older ports) and new‑build adoption; many smaller ports delay full automation, but large national ports are increasingly embracing automated mooring systems for efficiency and compliance with international shipping standards.

How are oil & gas and trade hubs driving adoption of automated mooring systems in Middle East & Africa?

In 2024, the Middle East & Africa region accounted for approximately 9% of global automated mooring system installations. Major growth is concentrated in the United Arab Emirates and South Africa, driven by demand from oil & gas offshore supply vessels, bulk‑cargo terminals, and container ports handling rising trade volumes. Technological modernization includes adoption of mooring load sensors, automated bollard‑release systems, and integration with digital port‑management platforms. Some regional trade partnerships and port‑rehabilitation programs have introduced favorable import tariffs and financing for automated systems, accelerating uptake. A South African port operator recently deployed a fully automated mooring solution in a new multipurpose terminal, enabling faster docking and improved safety for chemical‑ and bulk‑cargo carriers. Regional consumer behavior reflects a preference for modular automation — operators often install partial systems (e.g., automated bollard controls first), then expand as trade volume justifies further investment.

United States — ~14% market share: dominance due to high production capacity in shipbuilding and extensive port throughput across major coasts.

China — ~12% market share: driven by robust container traffic, aggressive port infrastructure expansion, and strong government support for smart‑port development.

The global Automated Mooring Systems market is moderately consolidated yet highly competitive, with more than 25–30 active players ranging from large multinational marine‑automation firms to specialized niche mooring‑system manufacturers. The top five companies together account for roughly 45–55% of the total installed base as of 2024; the remainder of the market is served by numerous regional and niche suppliers, making the overall structure moderately fragmented rather than dominated by a single firm. Leading companies differentiate themselves through strategic initiatives such as partnerships, acquisitions, and technologically advanced product rollouts. For instance, one major vendor recently announced the acquisition of a smaller mooring‑systems firm to bolster its turnkey automated mooring offerings worldwide. Another global leader entered a strategic partnership to jointly develop integrated automated mooring and docking solutions for offshore terminals, reflecting a shift toward more comprehensive port infrastructure automation.

Innovation trends strongly influence competitive positioning. Firms are increasingly investing in IoT‑enabled mooring solutions, real‑time sensor monitoring, AI-based docking algorithms, and predictive maintenance services. Some companies now offer mooring-as-a-service or subscription‑based models, bundling installation with lifecycle support — a move that helps retain customers and capture long‑term value beyond initial hardware sales. These efforts highlight a shift from selling discrete mooring equipment to providing integrated, value‑added solutions (automation + maintenance + analytics). Geographic expansion is another important strategy: many players are actively establishing footprints in high-growth regions such as Asia‑Pacific, Latin America, and the Middle East, often through regional partnerships or local subsidiaries. As ports globally adopt greener, faster, and safer mooring practices — and new installations exceed 300 worldwide — competition is intensifying around technological capability, service quality, and global reach.

Cavotec SA

Trelleborg Marine and Infrastructure

MacGregor (Cargotec Corporation)

TTS Group ASA

Mampaey Offshore Industries

C‑QUIP Ltd

Mooring Systems Ltd

Wärtsilä Corporation

Kongsberg Gruppen

ABB

The Automated Mooring Systems market is increasingly shaped by a suite of advanced technologies that form the backbone of modern port automation — spanning sensor systems, digital intelligence layers, robotics, and integrated port‑management platforms. Current-generation mooring systems often embed multiple high-precision load cells and strain gauges — typically 5 to 8 sensor nodes per mooring line — capable of measuring berth tension with an accuracy of ±0.5 %. These sensors sample at rates up to 100 Hz, enabling real-time monitoring of mooring loads, vessel drift, and environmental forces (e.g., wind or current-induced tension).

IoT-enabled mooring solutions now comprise nearly 40–45 % of new major port-builds worldwide. Data from sensor arrays are routed to cloud-based dashboards via secure maritime communication protocols, allowing port operators to view berth status, tension metrics, and system alerts remotely from centralized control centers. This data-driven transparency significantly reduces reliance on manual checks and supports rapid decision-making under changing conditions.

Digital twin modeling represents a rising trend, where ports simulate mooring dynamics and berth stress scenarios under different vessel sizes and tide conditions. By leveraging digital twins, engineering teams can optimize bollard placement and line configurations, reducing initial design and calibration time by up to 25 %. This not only improves safety but also accelerates deployment of new terminals and retrofits.

Artificial intelligence (AI) and machine-learning (ML) algorithms increasingly govern docking and mooring operations. Adaptive docking‑assistance systems interpret real-time sensor input and automatically adjust bollard tension or winch slack, thereby reducing human error by an estimated 80–85 % and mooring time per vessel by 30–35 %. Some advanced ports have reported reductions in average berth occupancy cycles from 10 hours to 7 hours following full mooring automation and AI‑guided docking.

In 2024, Cavotec commissioned a vacuum‑based automated mooring system at APM Terminals MedPort Tangier (Morocco), expanding coverage to an 800‑metre quay with 45 mooring units — significantly reducing vessel idle time and cutting mooring‑related emissions.

In June 2024, DP World San Antonio (Chile) became the first port in the Americas to deploy a MoorMaster NxG automated vacuum mooring system — marking first adoption of this technology in South America and enhancing docking safety and efficiency.

In late 2024, Cavotec secured a multi‑million euro order for its MoorMaster NxG system at Port of Dublin (Ireland), representing the first deployment of MoorMaster technology in Ireland — signaling expansion of automated mooring into Northern European ports.

In 2025, Trelleborg Marine & Infrastructure won a contract to deliver its “AutoMoor” automated mooring technology to a major Chinese container terminal — marking the first automated mooring system deployment in China, aimed at accommodating ultra‑large vessels and improving port throughput and sustainability.

The Automated Mooring Systems Market Report encompasses a comprehensive analysis spanning system types, technology architectures, application segments, geographic regions, and end‑user industries. On the technology dimension, the report covers traditional vacuum‑based mooring units, advanced sensor‑driven mooring with real‑time load monitoring, AI‑enabled docking control, robotic mooring arms and bollard control systems, and integrated port automation platforms. Regarding applications, the report addresses container terminals, Ro/Ro terminals, ferry and Ro/Pax terminals, bulk‑cargo docks, offshore support and oil & gas supply terminals, and lock and inland‑waterway installations. The geographic scope includes North America, Europe, Asia‑Pacific, South America, Middle East & Africa — capturing both mature and high‑growth regions. The report further segments markets by ship size (standard container vessels, ultra‑large container vessels, bulk carriers, Ro/Pax vessels), berth type (deep‑sea, coastal, inland), and port type (commercial container port, bulk/commodity port, multipurpose port, ferry/ passenger port). It also analyses demand drivers in different industries — logistics & shipping, oil & gas, energy, and government‑operated port authorities — and identifies niche segments such as automated mooring for LNG/LPG terminals and green‑port initiatives integrating mooring automation with shore‑power and emission‑reduction systems. The report includes installation volume, retrofit versus new‑build adoption data, typical berth‑length coverage per installation, and emerging trends such as modular mooring‑as‑a-service offerings and integrated maintenance‑service contracts. The comprehensive coverage ensures stakeholders obtain a detailed, multi‑dimensional view of current market dynamics, technology diffusion, regional growth potential, end‑use segmentation, and future opportunities for investments or strategic partnerships.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 766.2 Million |

|

Market Revenue in 2032 |

USD 1024.64 Million |

|

CAGR (2025 - 2032) |

3.7% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Cavotec SA, Trelleborg Marine and Infrastructure, MacGregor (Cargotec Corporation), TTS Group ASA, Mampaey Offshore Industries, C‑QUIP Ltd, Mooring Systems Ltd, Wärtsilä Corporation, Kongsberg Gruppen, ABB |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |