Reports

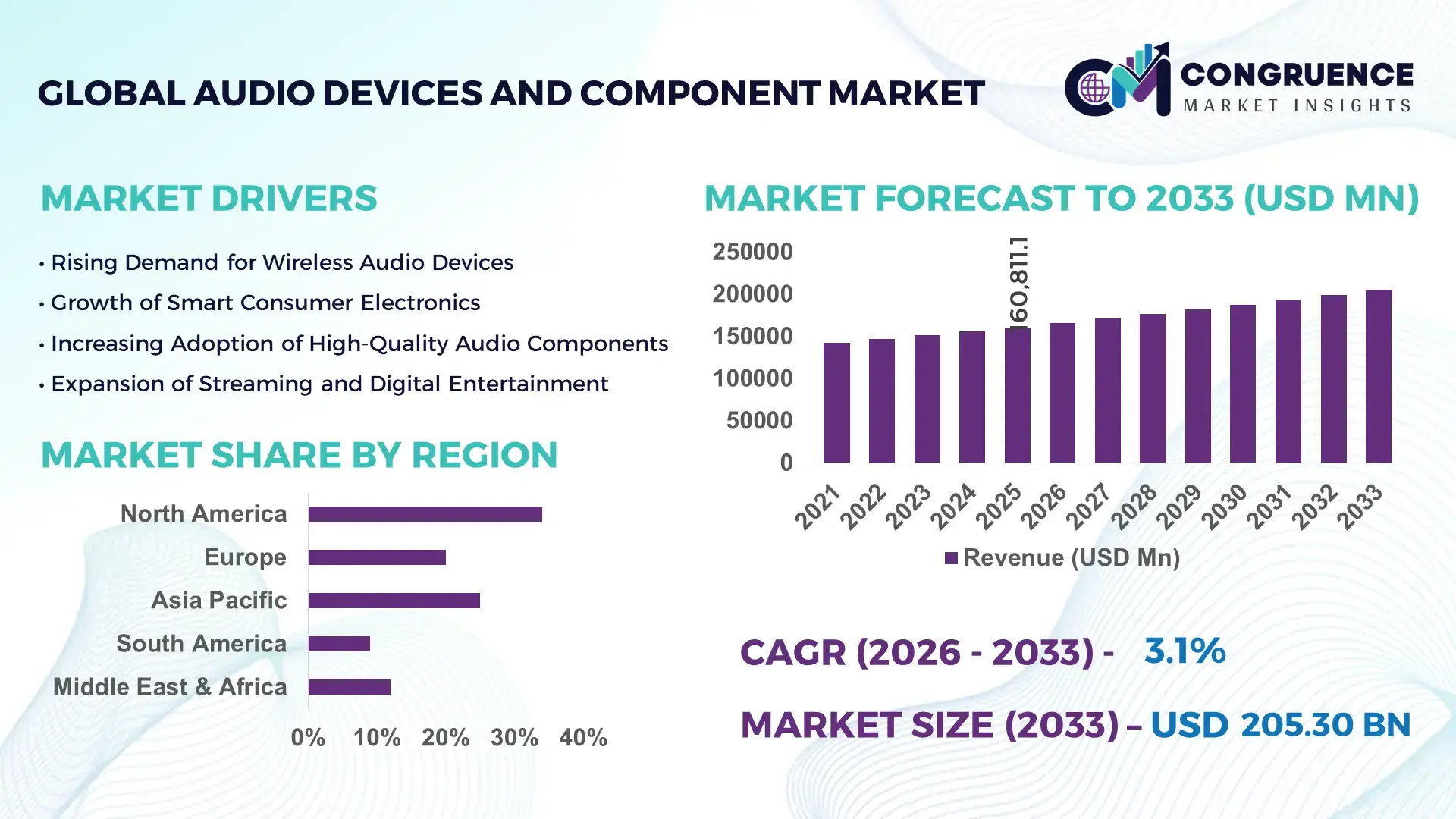

The Global Audio Devices and Component Market was valued at USD 160811.1 Million in 2025 and is anticipated to reach a value of USD 1860005.31 Million by 2033 expanding at a CAGR of 3.1% between 2026 and 2033. Rising consumer demand for high-fidelity sound systems across entertainment, communication, and automotive electronics is accelerating global market expansion.

The United States maintains a dominant operational presence in the Audio Devices and Component market with extensive manufacturing, research investment, and large-scale consumer adoption. The country hosts over 1,200 specialized audio electronics manufacturing facilities and more than 3,500 component suppliers supporting microphones, amplifiers, digital signal processors, and speaker systems. Consumer electronics adoption remains strong, with approximately 78% of U.S. households owning at least one smart audio device such as wireless speakers or soundbars. Automotive audio integration is also significant, with more than 65% of new vehicles produced in the U.S. incorporating advanced multi-speaker audio systems exceeding 10-speaker configurations. Annual R&D investments in audio technology and acoustic engineering exceed USD 5 billion, supporting innovations in spatial audio, noise-cancellation processors, MEMS microphones, and AI-driven sound optimization technologies used across consumer electronics, gaming, broadcasting, and professional audio production industries.

Market Size & Growth: The global Audio Devices and Component market reached USD 160811.1 Million in 2025 and is projected to approach USD 1860005.31 Million by 2033, expanding at 3.1% CAGR, supported by increasing adoption of smart speakers, wireless headphones, and immersive entertainment systems.

Top Growth Drivers: Wireless audio device adoption increased by 62%, automotive premium audio installations rose by 38%, and professional streaming equipment usage grew by 41% across digital content industries.

Short-Term Forecast: By 2028, advanced audio chipset integration and automated acoustic calibration are expected to improve sound processing efficiency by nearly 28% in smart consumer audio systems.

Emerging Technologies: AI-powered sound optimization, spatial and 3D immersive audio processing, and MEMS microphone miniaturization are reshaping next-generation audio electronics.

Regional Leaders: North America is projected to exceed USD 520 billion by 2033 due to premium consumer electronics adoption; Asia-Pacific may reach USD 760 billion driven by manufacturing scale; Europe could surpass USD 420 billion supported by automotive audio innovation.

Consumer/End-User Trends: Smart homes, gaming communities, automotive infotainment users, and streaming content creators represent the fastest-growing user segments in high-performance audio devices.

Pilot or Case Example: In 2024, a smart audio manufacturing facility in South Korea implemented AI-driven acoustic testing systems that reduced production testing time by 35% while improving quality accuracy by 27%.

Competitive Landscape: Apple leads the premium wireless audio device segment with approximately 21% share, followed by Samsung, Sony, Bose, and Harman International across global consumer and automotive audio systems.

Regulatory & ESG Impact: Governments are implementing electronic waste recycling policies and energy-efficient device standards targeting 20% reduction in power consumption in consumer electronics by 2030.

Investment & Funding Patterns: Global investments in advanced semiconductor audio chips, acoustic sensors, and immersive audio technologies exceeded USD 12 billion during the past three years.

Innovation & Future Outlook: Integration of AI voice assistants, spatial audio streaming, and low-latency wireless audio protocols is shaping next-generation connected entertainment ecosystems.

Professional audio equipment, automotive infotainment systems, consumer electronics speakers, and smart home audio devices collectively account for over 70% of global demand. Emerging innovations such as spatial audio rendering, ultra-low-latency wireless chips, and MEMS acoustic sensors are strengthening product performance while supporting sustainable electronic design standards.

The Audio Devices and Component Market plays a strategic role in the global consumer electronics and digital media ecosystem as immersive sound technologies become essential across entertainment, communication, and automotive applications. Advanced digital signal processing and AI-enabled acoustic tuning systems are enabling high-performance audio output in compact hardware environments. For instance, AI-based adaptive audio processing delivers nearly 32% sound clarity improvement compared to traditional fixed equalization standards.

Asia-Pacific dominates production volume due to large-scale electronics manufacturing capacity, while North America leads in adoption with nearly 68% of enterprises deploying advanced conferencing audio systems and professional streaming equipment. The growing digital content industry is pushing manufacturers to develop ultra-low latency audio chips and high-resolution speaker drivers optimized for 4K and spatial media formats.

By 2028, AI-assisted sound optimization and automated acoustic calibration technologies are expected to reduce signal distortion and energy consumption by approximately 26% in premium audio devices. Firms are committing to sustainability goals, including 30% recyclable materials in electronic components and a 25% reduction in manufacturing emissions by 2030. In 2024, a Japanese consumer electronics manufacturer deployed AI-driven acoustic testing in production facilities and achieved a 34% improvement in quality consistency for wireless audio devices. These advancements position the Audio Devices and Component Market as a pillar supporting resilient consumer electronics innovation, regulatory compliance, and sustainable digital infrastructure growth.

The Audio Devices and Component Market is influenced by evolving consumer electronics demand, advancements in wireless audio technologies, and the rapid expansion of digital entertainment platforms. Increasing adoption of smart home devices, gaming headsets, and premium automotive sound systems continues to stimulate industry growth. Innovations in MEMS microphones, high-efficiency amplifiers, and spatial audio processors are improving sound quality while reducing power consumption. The rise of content streaming platforms and remote communication tools has also strengthened demand for professional audio equipment, conferencing devices, and noise-cancellation technologies across enterprise and consumer markets.

Consumer demand for immersive entertainment technologies is significantly driving the Audio Devices and Component Market. Global shipments of wireless headphones surpassed 500 million units annually, while smart speaker installations exceeded 300 million active devices worldwide. Gaming audio peripherals are also expanding rapidly, with over 40% of gamers using dedicated headsets for spatial audio experiences. Automotive infotainment systems now integrate multi-channel surround sound configurations with 10 to 20 speakers in premium vehicles, increasing demand for amplifiers, acoustic processors, and high-performance speaker components across automotive manufacturing.

The Audio Devices and Component Market faces constraints from semiconductor supply limitations and complex global supply chains. Audio chipsets, digital signal processors, and Bluetooth modules rely heavily on specialized semiconductor fabrication, where manufacturing delays have impacted production timelines. In recent years, electronics manufacturers reported component lead times exceeding 20 to 30 weeks for specific audio processing chips. Rising raw material costs for rare earth magnets used in speaker drivers and MEMS sensor components have also increased manufacturing expenses, limiting scalability for mid-range consumer audio products.

The rapid growth of smart home ecosystems and connected vehicles presents major opportunities for the Audio Devices and Component Market. Over 45% of global households are expected to adopt at least one voice-controlled smart audio device within the next decade. In automotive manufacturing, nearly 70% of new vehicles now include integrated infotainment systems with multi-channel audio capabilities. Emerging technologies such as spatial audio rendering, voice recognition microphones, and ultra-low latency wireless transmission chips are creating new product categories for home automation systems, smart assistants, and connected mobility platforms.

Increasing product complexity and evolving regulatory standards create operational challenges for manufacturers in the Audio Devices and Component Market. Modern audio devices integrate wireless connectivity, AI-based processors, and high-density electronic components that require advanced design validation and testing procedures. Regulatory frameworks for electronic waste management, energy consumption limits, and electromagnetic compatibility are becoming stricter across global markets. Compliance testing can extend product development cycles by 6 to 12 months, increasing engineering costs while requiring manufacturers to invest in sustainable materials, recyclable components, and energy-efficient circuit designs.

• Rapid Expansion of True Wireless Audio Devices: True wireless stereo (TWS) earphones have become one of the most dominant product categories in the Audio Devices and Component market. Global shipments exceeded 650 million units in 2024, reflecting a 21% increase in annual adoption. Over 72% of smartphone users now prefer wireless audio accessories compared to wired alternatives. Improvements in Bluetooth Low Energy audio codecs and battery efficiency have extended playback time by nearly 35% compared to models released five years earlier. Manufacturers are also integrating AI-based noise cancellation systems capable of reducing ambient sound by up to 40 decibels, improving user experience in urban environments and travel scenarios.

• Integration of Spatial and Immersive Audio Technologies: Spatial audio and 3D sound technologies are rapidly transforming digital entertainment experiences. Nearly 48% of premium headphones and home audio systems launched in 2024 included spatial audio processing features capable of delivering 360-degree sound environments. Gaming consoles and streaming platforms now support multi-channel audio formats supporting up to 12 independent audio channels. Consumer surveys indicate that 56% of gaming users consider immersive audio capabilities a key purchase factor for headsets and soundbars. Advanced digital signal processors have improved audio localization accuracy by approximately 30%, enabling more realistic audio positioning in virtual environments.

• Growth of Automotive Premium Audio Systems: Automotive manufacturers are increasingly integrating high-performance sound systems into vehicles as infotainment capabilities expand. More than 68% of new vehicles launched globally in 2024 featured advanced audio systems with eight or more speakers. Premium vehicles commonly deploy 14-speaker or higher surround sound configurations. Automotive audio amplifier efficiency has improved by approximately 25% due to new Class-D amplifier technologies, enabling powerful sound performance while maintaining lower energy consumption. Electric vehicle manufacturers are also developing adaptive cabin acoustics systems that adjust sound output dynamically based on vehicle speed and cabin noise levels.

• Miniaturization and MEMS Microphone Innovation: The miniaturization of acoustic components has become a defining trend in the Audio Devices and Component market. MEMS microphones now represent nearly 70% of microphones integrated into smartphones, smart speakers, and wearable electronics. Modern MEMS sensors measure less than 4 millimeters in size yet deliver signal-to-noise ratios exceeding 65 decibels. Consumer electronics manufacturers have increased the number of microphones in smart devices from an average of two units in 2018 to five or more in 2024 to enhance voice recognition accuracy by nearly 35%. These developments support the rapid growth of voice assistants, conferencing devices, and AI-driven communication platforms.

The Audio Devices and Component market is segmented by type, application, and end-user industry, reflecting diverse technology adoption patterns across global markets. Audio output devices such as speakers and headphones represent the largest share due to widespread consumer electronics demand. Applications are heavily concentrated in consumer electronics and automotive infotainment systems, which together account for more than 60% of industry utilization. End-user demand is led by consumer electronics manufacturers, followed by automotive OEMs, professional broadcasting firms, and enterprise communication providers. Increasing demand for immersive audio experiences, voice-enabled smart devices, and digital entertainment platforms continues to expand product diversification across these segments.

The Audio Devices and Component market includes speakers, headphones and earphones, microphones, amplifiers, and audio integrated circuits. Speakers currently represent the leading product segment, accounting for approximately 34% of global adoption due to their extensive use in home entertainment systems, smart speakers, automotive audio installations, and professional sound reinforcement equipment. Headphones and earphones follow with nearly 29% adoption as wireless listening devices continue to expand globally. However, microphones represent the fastest-growing segment, expanding at an estimated 7.2% annual growth due to increasing deployment in smartphones, smart assistants, conferencing systems, and voice-activated devices. MEMS microphones are particularly driving growth, now integrated into over 85% of modern smartphones. Amplifiers and audio integrated circuits collectively contribute about 37% of the market, supporting signal processing, power distribution, and acoustic enhancement in audio equipment.

Consumer electronics represents the largest application segment in the Audio Devices and Component market, accounting for nearly 46% of global utilization due to widespread use in smartphones, smart speakers, headphones, and home entertainment systems. Audio integration within consumer devices continues to increase as streaming services and digital media consumption expand. Automotive infotainment systems represent the fastest-growing application segment, expanding at approximately 6.8% annual growth. Modern vehicles increasingly feature advanced sound systems with 10 to 20 speakers and digital signal processors capable of delivering immersive audio environments for passengers. Professional audio equipment, broadcasting studios, gaming peripherals, and enterprise conferencing systems collectively account for roughly 32% of industry applications, supporting communication, entertainment production, and digital collaboration environments.

Consumer electronics manufacturers represent the leading end-user group in the Audio Devices and Component market, accounting for nearly 52% of total industry demand due to large-scale production of smartphones, tablets, laptops, smart speakers, and wearable audio devices. These manufacturers integrate high-performance speakers, microphones, and audio chips into billions of devices annually. Automotive manufacturers represent the fastest-growing end-user segment, expanding at approximately 6.5% annual growth as advanced infotainment and in-vehicle entertainment systems become standard features. More than 70% of newly manufactured vehicles now include integrated multi-channel audio systems. Other key end-users include professional audio equipment producers, broadcasting organizations, gaming hardware manufacturers, and enterprise communication providers, which together contribute around 48% of industry demand.

Region North America accounted for the largest market share at 34% in 2025 however, Region Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.4% between 2026 and 2033.

North America recorded more than 420 million active smart audio devices and over 72% household adoption of wireless audio products. Europe represents roughly 26% of global demand supported by automotive audio integration in more than 65% of new vehicles. Asia-Pacific contributes over 38% of global electronics manufacturing output, producing nearly 600 million audio devices annually. South America holds approximately 7% share with rising digital media consumption, while Middle East & Africa collectively account for nearly 5% driven by expanding smartphone and streaming adoption.

How Are Advanced Consumer Electronics and Enterprise Communication Systems Accelerating Market Expansion?

The Audio Devices and Component market in this region accounts for approximately 34% of global demand, driven primarily by high adoption of premium consumer electronics, automotive infotainment systems, and professional audio equipment. More than 78% of households own at least one wireless audio device, and nearly 60% of newly sold vehicles integrate multi-speaker digital sound systems. Key industries fueling demand include entertainment streaming, gaming hardware, smart home ecosystems, and enterprise communication solutions. Regulatory frameworks supporting energy-efficient electronics and electronic waste recycling are influencing product design standards across the industry. Technological advancements such as spatial audio processing, AI-based sound optimization, and ultra-low-latency wireless codecs are being rapidly integrated into devices. A prominent example includes Bose Corporation expanding its advanced acoustic R&D initiatives to develop adaptive noise-cancellation systems capable of reducing background noise by nearly 40%. Consumer behavior shows strong demand for premium wireless headphones, soundbars, and smart speakers, with enterprise adoption particularly high across healthcare, finance, and corporate conferencing environments.

How Are Sustainability Regulations and Automotive Audio Innovation Transforming Industry Demand?

Europe represents roughly 26% of the global Audio Devices and Component market, with strong adoption across Germany, the United Kingdom, and France. Automotive manufacturers in these countries increasingly integrate premium multi-channel sound systems into vehicles, with more than 64% of new car models offering advanced infotainment audio features. Regulatory initiatives focused on electronic waste reduction, product recyclability, and energy-efficient electronics are shaping product development across the region. The European Union’s sustainability guidelines encourage manufacturers to incorporate recyclable materials in electronic components, targeting over 30% recyclable content in consumer devices. Technology adoption is also advancing rapidly with the integration of spatial audio rendering, MEMS microphone arrays, and high-efficiency Class-D amplifiers in entertainment systems. A notable example includes Sennheiser expanding professional audio manufacturing and immersive sound technology for broadcasting and live performance environments. Consumer behavior reflects strong preference for high-quality sound systems and environmentally sustainable electronics, with demand particularly strong in home theater systems and professional audio equipment.

How Are Large-Scale Electronics Manufacturing and Mobile Technology Adoption Driving Market Leadership?

The Audio Devices and Component market in this region ranks as the largest production hub globally, contributing more than 38% of worldwide audio device manufacturing output. China, Japan, and India represent the largest consuming markets due to massive smartphone production and rapidly growing consumer electronics industries. China alone manufactures over 500 million headphones and wireless audio devices annually, while Japan leads innovation in high-precision acoustic components and audio semiconductor technologies. Infrastructure investments in semiconductor fabrication, electronics assembly plants, and AI research centers are strengthening the region’s leadership in audio technology innovation. Companies such as Sony continue to expand high-resolution audio product lines and immersive audio technologies for gaming and entertainment ecosystems. Consumer behavior is strongly influenced by e-commerce and mobile technology usage, with over 70% of young consumers purchasing wireless audio devices through digital retail platforms and mobile applications.

How Is Expanding Digital Entertainment Consumption Creating Opportunities for Audio Technology Adoption?

South America accounts for approximately 7% of the global Audio Devices and Component market, with Brazil and Argentina representing the largest national markets. Increasing smartphone penetration and digital media consumption are key factors stimulating demand for headphones, wireless speakers, and portable audio equipment. Brazil alone has more than 160 million active internet users, and nearly 65% of them regularly stream music or video content requiring personal audio devices. Governments across the region are introducing trade policies and tax incentives to support electronics manufacturing and technology imports. Infrastructure improvements in telecommunications networks are also expanding digital entertainment ecosystems. A notable regional electronics brand, Multilaser in Brazil, has expanded its portfolio of affordable wireless headphones and portable speakers targeting mass-market consumers. Consumer behavior in the region shows strong demand for budget-friendly audio devices, with usage closely tied to social media, mobile streaming platforms, and localized digital entertainment services.

How Are Digital Infrastructure Expansion and Smart Entertainment Adoption Supporting Industry Growth?

The Middle East & Africa Audio Devices and Component market accounts for nearly 5% of global demand and continues to expand as smartphone adoption and digital infrastructure investments accelerate. Countries such as the United Arab Emirates and South Africa represent major technology adoption hubs within the region. Rapid growth in digital entertainment, gaming communities, and online streaming services has increased demand for wireless headphones, smart speakers, and professional audio systems. Governments are investing heavily in smart city initiatives and high-speed communication networks, supporting the adoption of voice-enabled devices and connected home technologies. Retail electronics markets in the UAE report more than 50% year-on-year growth in premium wireless audio products. Regional companies such as Axiom Telecom are expanding consumer electronics distribution networks to increase device accessibility. Consumer behavior indicates rising demand for high-performance audio equipment, particularly among younger urban populations using mobile gaming and digital streaming services.

United States – 27% market share: The United States leads the Audio Devices and Component market due to strong consumer electronics demand, advanced R&D investment exceeding 5 billion annually, and high adoption of smart audio devices across households and enterprises.

China – 23% market share: China dominates global manufacturing of audio devices and components, producing over 500 million wireless audio products annually while supporting large-scale smartphone and electronics assembly industries.

The Audio Devices and Component market features a moderately fragmented competitive environment with more than 120 global and regional manufacturers actively competing across consumer electronics, professional audio systems, and automotive infotainment technologies. The top five companies collectively account for approximately 38% of the global market, reflecting strong competition among established brands and emerging electronics innovators. Companies are prioritizing research and development investments exceeding USD 8 billion annually to develop advanced acoustic processors, MEMS microphones, and spatial audio technologies. Strategic initiatives include partnerships with automotive manufacturers, expansion of smart speaker ecosystems, and integration of AI-driven sound optimization software. Product innovation cycles have shortened to approximately 18 months due to intense competition in wireless headphones and smart home audio segments. Mergers, acquisitions, and technology licensing agreements are also shaping the competitive landscape, enabling companies to expand global distribution networks and accelerate innovation in immersive audio systems.

Apple

Samsung Electronics

Sony Corporation

Bose Corporation

Harman International

Panasonic Corporation

Sennheiser Electronic

Yamaha Corporation

LG Electronics

Qualcomm Incorporated

Texas Instruments

Cirrus Logic

STMicroelectronics

Knowles Corporation

Dolby Laboratories

Technological advancement in the Audio Devices and Component market is increasingly centered on AI-driven sound processing, miniaturized acoustic hardware, and high-efficiency wireless transmission protocols. Modern digital signal processors can now analyze and adjust sound frequencies in real time, improving audio clarity by nearly 30% compared with traditional fixed equalizer systems. MEMS microphones have become the dominant acoustic sensor technology, representing nearly 70% of microphones integrated into smartphones, wearables, and smart home devices due to their compact size of less than 4 mm and signal-to-noise ratios above 65 dB.

Wireless audio technology is also evolving rapidly with Bluetooth Low Energy Audio and LC3 codecs, which reduce power consumption by approximately 50% while maintaining high-resolution sound quality. These improvements enable wireless headphones to deliver over 30 hours of playback in many modern devices. Spatial audio and immersive sound processing technologies are expanding across gaming, streaming media, and automotive infotainment systems, supporting up to 12 independent sound channels for 360-degree audio experiences.

In addition, semiconductor manufacturers are introducing specialized audio chips integrating AI noise suppression and adaptive voice recognition. These chips can filter up to 40 dB of background noise in real time, enabling clearer voice communication for conferencing systems, smart assistants, and connected vehicle platforms.

• In January 2025, Samsung Electronics introduced the Galaxy Buds3 Pro wireless earbuds featuring advanced AI-powered adaptive noise control and real-time sound optimization. The device incorporates dual-amplifier architecture and enhanced spatial audio capabilities designed to improve audio clarity and reduce distortion in immersive listening environments. Source: www.samsung.com

• In April 2024, Bose Corporation launched the Ultra Open Earbuds featuring an open-ear design with proprietary OpenAudio technology. The device allows users to hear environmental sounds while delivering high-fidelity audio, targeting fitness and outdoor users. The product integrates advanced Bluetooth connectivity and adaptive sound processing. Source: www.bose.com

• In September 2024, Sony Corporation expanded its ULT Power Sound product lineup with new wireless speakers and headphones engineered for enhanced bass performance. The devices incorporate Sony’s proprietary audio processing technology and improved battery systems supporting more than 25 hours of playback for portable listening. Source: www.sony.com

• In August 2024, Dolby Laboratories announced the expansion of Dolby Atmos FlexConnect technology for smart televisions, enabling wireless pairing between TV speakers and external audio devices. The system dynamically optimizes sound positioning across multiple speakers, delivering immersive audio performance without requiring complex wired configurations.

The Audio Devices and Component Market Report provides a comprehensive evaluation of global industry performance across multiple technology segments, product categories, and end-user industries. The report examines key product types including speakers, headphones and earphones, microphones, amplifiers, digital signal processors, and audio integrated circuits. These categories collectively represent billions of units produced annually across consumer electronics, automotive infotainment systems, professional broadcasting equipment, and enterprise communication devices.

Geographically, the report analyzes industry activity across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, covering more than 30 major national markets and global manufacturing hubs. The study highlights regional production capacities, technology adoption levels, and consumer behavior patterns influencing demand for wireless audio devices, smart speakers, and immersive entertainment systems.

The scope further includes emerging technologies such as spatial audio processing, MEMS acoustic sensors, AI-based noise suppression chips, and Bluetooth Low Energy Audio protocols. It also evaluates adoption trends across major application sectors including smartphones, gaming equipment, smart homes, streaming platforms, and connected vehicles, where advanced multi-speaker systems and voice-enabled audio interfaces are increasingly integrated into modern digital ecosystems.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

3.1% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Apple, Samsung Electronics, Sony Corporation, Bose Corporation, Harman International, Panasonic Corporation, Sennheiser Electronic, Yamaha Corporation, LG Electronics, Qualcomm Incorporated, Texas Instruments, Cirrus Logic, STMicroelectronics, Knowles Corporation, Dolby Laboratories |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |