Reports

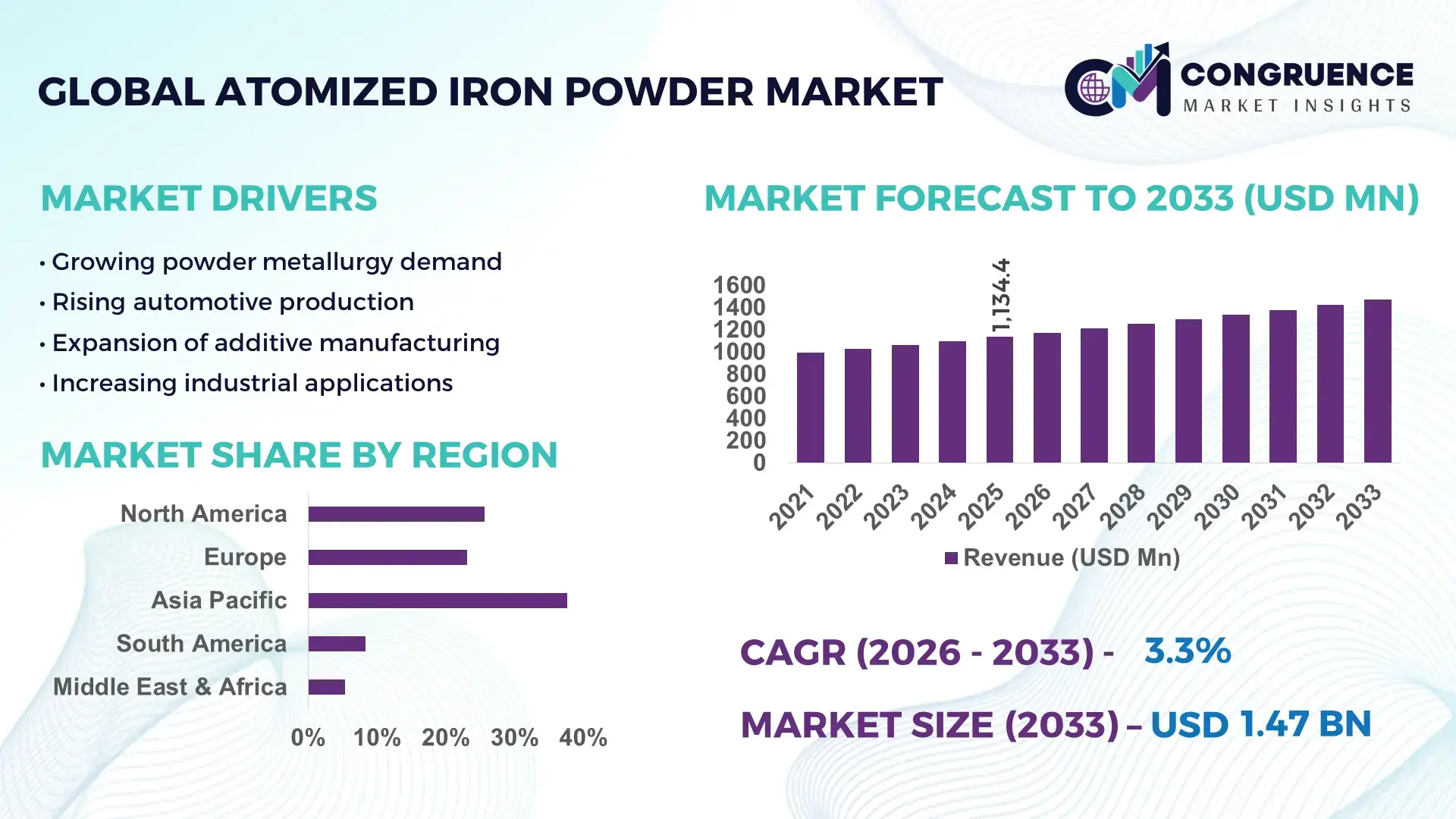

The Global Atomized Iron Powder Market was valued at USD 1134.42 Million in 2025 and is anticipated to reach a value of USD 1470.88 Million by 2033 expanding at a CAGR of 3.3% between 2026 and 2033. This growth is primarily driven by the increasing demand for powder metallurgy components in automotive and industrial manufacturing sectors, supported by advancements in additive manufacturing technologies.

China continues to play a central role in the global atomized iron powder industry, supported by an annual production capacity exceeding 700,000 metric tons across multiple state-owned and private manufacturing facilities. The country has witnessed industrial investments surpassing USD 500 million in recent years to modernize atomization technologies, including water and gas atomization systems. Atomized iron powder is extensively utilized in automotive components, contributing to over 40% of domestic powder metallurgy applications, followed by machinery and electronics sectors. Additionally, China’s growing adoption of high-density iron powder for electric vehicle components and magnetic materials has expanded its industrial utilization footprint. Technological upgrades, including automated sieving and particle size distribution control systems, have improved yield efficiency by nearly 20%, strengthening production scalability and quality standards.

Market Size & Growth: USD 1134.42 Million in 2025, projected to reach USD 1470.88 Million by 2033 at a CAGR of 3.3%, driven by rising demand in automotive powder metallurgy and additive manufacturing.

Top Growth Drivers: Automotive component demand increased by 35%, additive manufacturing adoption by 28%, and industrial machinery applications by 22%.

Short-Term Forecast: By 2028, production efficiency is expected to improve by 18% due to automation and advanced atomization techniques.

Emerging Technologies: Gas atomization refinement, hybrid additive manufacturing integration, and nano-structured iron powder development are shaping the industry.

Regional Leaders: Asia-Pacific projected at USD 620 Million by 2033 with strong manufacturing demand; Europe at USD 410 Million driven by sustainability initiatives; North America at USD 340 Million with high adoption in aerospace.

Consumer/End-User Trends: Automotive and industrial machinery sectors account for over 60% of total consumption, with increasing uptake in 3D printing applications.

Pilot or Case Example: In 2024, a European manufacturer improved material utilization efficiency by 15% using advanced particle size control technology.

Competitive Landscape: Market leader holds approximately 18% share, followed by key players including Höganäs AB, Rio Tinto Metal Powders, and JFE Steel Corporation.

Regulatory & ESG Impact: Environmental regulations targeting emissions reduction have pushed recycling rates of iron powder to exceed 30% globally.

Investment & Funding Patterns: Recent investments exceed USD 800 million globally, focusing on production automation and sustainable manufacturing.

Innovation & Future Outlook: Integration of AI-based quality monitoring and eco-friendly atomization processes is expected to drive future competitiveness.

The atomized iron powder market is characterized by strong sectoral contributions, with automotive applications accounting for nearly 45% of total demand, followed by industrial machinery at approximately 30% and electronics at 10%. Innovations such as ultra-fine powder production, enhanced compressibility grades, and improved sintering capabilities are reshaping product performance. Environmental regulations encouraging low-emission manufacturing and recycling practices are influencing production strategies, particularly in Europe and North America. Consumption patterns indicate rapid growth in Asia-Pacific due to industrial expansion, while developed regions emphasize high-performance alloys and sustainability. Emerging trends include the integration of digital process controls and the expansion of iron powder use in additive manufacturing and magnetic applications, positioning the market for long-term technological evolution.

The atomized iron powder market holds significant strategic relevance as industries increasingly prioritize lightweight, durable, and cost-efficient materials for high-performance applications. Powder metallurgy continues to serve as a critical manufacturing route, enabling material utilization rates exceeding 95%, which substantially reduces waste compared to conventional machining processes. Advanced gas atomization technology delivers nearly 25% improvement in particle uniformity compared to traditional water atomization methods, enhancing product consistency for precision engineering applications.

Asia-Pacific dominates in volume due to large-scale manufacturing operations, while Europe leads in adoption with over 55% of enterprises integrating advanced powder metallurgy techniques for sustainable production. The increasing penetration of additive manufacturing is further strengthening the market’s importance, particularly in aerospace and automotive component fabrication. By 2028, AI-driven quality control systems are expected to improve defect detection rates by over 30%, significantly reducing production inefficiencies.

From an ESG perspective, firms are committing to measurable sustainability goals, including up to 35% reduction in carbon emissions and 40% recycling of metal powders by 2030. These commitments are shaping investment decisions and operational frameworks across the industry. In 2024, a leading Japanese manufacturer achieved a 20% reduction in energy consumption through the implementation of smart furnace systems integrated with real-time monitoring technologies, demonstrating the tangible benefits of digital transformation. Looking ahead, the atomized iron powder market is expected to evolve as a cornerstone of advanced manufacturing ecosystems, supporting resilience through material efficiency, compliance with environmental standards, and continuous innovation in high-performance material solutions.

The atomized iron powder market is influenced by a combination of industrial demand shifts, technological advancements, and regulatory developments. Increasing reliance on powder metallurgy in automotive and machinery manufacturing is driving consistent demand for high-quality iron powders with controlled particle size and enhanced compressibility. Technological progress in atomization methods, including gas and water-based processes, has improved production efficiency and material characteristics. Additionally, the expansion of additive manufacturing is opening new avenues for application, particularly in precision components and prototyping. Environmental regulations are also playing a pivotal role, pushing manufacturers to adopt sustainable practices such as recycling and energy-efficient production. Global supply chain optimization and raw material availability further shape pricing and production trends, making the market highly dynamic and responsive to industrial innovation.

The growing demand for powder metallurgy components is significantly accelerating the atomized iron powder market. Powder metallurgy enables near-net-shape manufacturing, reducing material waste by up to 97% and lowering machining requirements. Automotive manufacturers increasingly rely on sintered iron components for engines, transmissions, and structural parts, with over 70% of modern vehicles incorporating powder metallurgy parts. Additionally, industrial machinery sectors are adopting atomized iron powder for producing durable and high-strength components, improving operational efficiency by approximately 15%. The shift toward electric vehicles has further amplified demand, as iron powders are used in magnetic materials and motor components. This expanding application base, combined with the need for cost-effective and sustainable manufacturing processes, continues to drive the widespread adoption of atomized iron powder across multiple industries.

Volatility in raw material prices, particularly iron ore and scrap metal, poses a significant restraint on the atomized iron powder market. Iron ore prices have experienced fluctuations exceeding 30% within short periods, directly impacting production costs for manufacturers. Additionally, energy-intensive atomization processes require substantial electricity and fuel inputs, making production costs sensitive to energy price variations. These fluctuations create challenges in maintaining stable pricing for end-users, particularly in cost-sensitive industries such as automotive and construction. Supply chain disruptions and geopolitical factors further exacerbate price instability, affecting procurement strategies and production planning. As a result, manufacturers face difficulties in achieving consistent profit margins, which can limit investment in technological upgrades and capacity expansion.

The rapid expansion of additive manufacturing presents substantial growth opportunities for the atomized iron powder market. The global adoption of metal 3D printing technologies has increased by over 25% in recent years, driving demand for high-purity, fine particle iron powders. Atomized iron powder is increasingly used in producing complex geometries and customized components, particularly in aerospace, healthcare, and automotive sectors. Advanced powder formulations with improved flowability and density are enabling higher precision and better mechanical properties in printed parts. Furthermore, the ability to reduce material waste by up to 90% compared to traditional manufacturing enhances sustainability and cost efficiency. As industries continue to invest in digital manufacturing solutions, the demand for specialized atomized iron powders tailored for additive processes is expected to grow significantly.

Stringent environmental regulations represent a critical challenge for the atomized iron powder market, particularly in regions with strict emission standards. Atomization processes generate particulate emissions and consume significant energy, leading to regulatory scrutiny. Compliance with environmental standards often requires investment in advanced filtration systems, emission control technologies, and energy-efficient equipment, increasing operational costs by up to 20%. Additionally, waste management and recycling requirements necessitate the implementation of complex processing systems, adding to production complexity. Manufacturers must also adhere to regulations governing workplace safety and material handling, further increasing compliance costs. These regulatory pressures can slow down capacity expansion and innovation, particularly for smaller manufacturers with limited financial resources.

• Increasing adoption of additive manufacturing-grade powders: The demand for fine and ultra-fine atomized iron powders has risen by over 30% in the past three years, driven by the expansion of metal 3D printing applications. Approximately 45% of manufacturers are now integrating additive manufacturing into their production processes, with particle size precision improvements reaching up to 20%. Advanced gas atomization techniques are enabling consistent powder morphology, improving print quality and reducing material wastage by nearly 25%, which is particularly valuable in aerospace and automotive prototyping.

• Shift toward high-density and high-purity powder formulations: High-density atomized iron powders now account for nearly 38% of total industrial usage, particularly in automotive and heavy machinery applications. These powders offer compressibility improvements of up to 18% compared to conventional grades, enhancing sintered component strength and durability. Manufacturers are increasingly investing in refining purification processes, achieving impurity reductions of up to 15%, which significantly improves performance in precision-engineered components and magnetic materials.

• Growing emphasis on sustainable and recycled metal powders: Sustainability initiatives are driving the adoption of recycled iron powder, with global recycling rates exceeding 32% in 2025. Energy-efficient atomization processes have reduced energy consumption by approximately 22%, while emissions control technologies have cut particulate emissions by nearly 28%. Over 50% of European manufacturers have implemented closed-loop recycling systems, reflecting a strong shift toward circular manufacturing practices and compliance with environmental standards.

• Automation and digitalization in powder production: The integration of automation and digital monitoring systems has increased production efficiency by approximately 20%, with defect detection accuracy improving by over 35% through AI-based quality control. Smart manufacturing technologies, including real-time particle size analysis and automated sieving, are now adopted by nearly 40% of large-scale producers. These advancements are reducing downtime by up to 18% and ensuring consistent product quality, particularly in high-volume industrial applications.

The atomized iron powder market is segmented based on type, application, and end-user industries, each contributing uniquely to overall demand patterns. By type, water-atomized and gas-atomized powders dominate production, with variations in particle size and purity influencing application suitability. In terms of application, powder metallurgy accounts for the majority of usage due to its efficiency in producing complex components with minimal waste. Additive manufacturing is rapidly gaining traction as industries seek precision and customization. From an end-user perspective, automotive manufacturing leads consumption, followed by industrial machinery and emerging sectors such as electronics and energy. Approximately 60% of total demand is concentrated in heavy industrial applications, while high-precision sectors are steadily increasing their share due to technological advancements and evolving material requirements.

Water-atomized iron powder remains the leading segment, accounting for approximately 62% of total market adoption due to its cost efficiency and suitability for large-scale powder metallurgy applications. Its irregular particle structure enhances compressibility, making it ideal for automotive and industrial components. In comparison, gas-atomized powders hold around 28% share, offering superior spherical particle morphology and higher purity levels, which are critical for additive manufacturing and high-performance applications. However, gas-atomized powders represent the fastest-growing segment, expanding at an estimated CAGR of 6.8% due to increasing demand for precision-engineered components and 3D printing materials.

Reduced iron powder and electrolytic iron powder collectively contribute nearly 10% of the market, serving niche applications such as magnetic materials and specialty coatings. These types are valued for their high purity and controlled chemical composition, although their higher production costs limit widespread adoption.

Powder metallurgy dominates the application landscape, accounting for approximately 68% of total usage due to its efficiency in producing complex and durable components. Automotive parts such as gears, bearings, and structural components represent a significant portion of this segment, benefiting from material utilization rates exceeding 90%. Additive manufacturing holds around 20% of the market, driven by increasing adoption in aerospace and medical sectors where precision and customization are critical. This segment is also the fastest-growing, with an estimated CAGR of 7.5%, supported by advancements in metal 3D printing technologies.

Other applications, including magnetic materials, welding electrodes, and chemical processing, collectively contribute about 12% of the market. These applications rely on specialized powder characteristics such as high purity and controlled particle size.

The automotive sector leads the atomized iron powder market, accounting for nearly 52% of total consumption, driven by extensive use in powder metallurgy components such as engine parts, transmission systems, and structural elements. Industrial machinery follows with approximately 25% share, leveraging iron powders for durable and wear-resistant components. In contrast, the aerospace and electronics sectors, while currently holding around 15% combined share, represent the fastest-growing end-user segment with an estimated CAGR of 7.2%, fueled by the increasing need for high-precision and lightweight components.

Other end-users, including energy and construction industries, contribute roughly 8% of total demand, with growing adoption in magnetic materials and specialized coatings. Adoption rates in advanced manufacturing industries have increased by nearly 20% over recent years, reflecting a broader shift toward efficient material utilization.

Region Asia-Pacific accounted for the largest market share at 46% in 2025 however, Europe is expected to register the fastest growth, expanding at a CAGR of 4.1% between 2026 and 2033.

Asia-Pacific dominates due to its large-scale manufacturing ecosystem, producing over 750,000 metric tons of atomized iron powder annually, with China alone contributing more than 60% of the regional output. North America holds approximately 24% share, supported by advanced automotive and aerospace industries, while Europe accounts for nearly 22%, driven by sustainability-focused manufacturing. South America and the Middle East & Africa collectively contribute around 8%, with growing industrialization and infrastructure development. Consumption patterns indicate that over 65% of demand is concentrated in automotive and industrial applications globally, while additive manufacturing adoption has increased by 27% across developed regions. Regional investment in advanced atomization technologies has exceeded USD 1 billion globally, with Asia-Pacific leading in capacity expansion and Europe focusing on energy-efficient production systems.

How are advanced manufacturing technologies transforming industrial material demand patterns?

North America represents approximately 24% of the global atomized iron powder market, with strong demand driven by automotive, aerospace, and industrial machinery sectors. The region consumes over 300,000 metric tons annually, with the United States accounting for nearly 75% of regional demand. Government initiatives promoting domestic manufacturing and supply chain resilience have led to increased investments in powder metallurgy facilities. Regulatory frameworks focusing on emissions reduction and workplace safety have encouraged the adoption of cleaner production technologies, improving energy efficiency by up to 18%. Digital transformation is a key trend, with nearly 42% of manufacturers implementing AI-driven quality control systems to enhance precision and reduce defects. A notable regional player, Rio Tinto Metal Powders, has expanded its production capabilities by integrating automated atomization processes, improving output consistency by approximately 20%. Consumer behavior reflects higher enterprise adoption in automotive and aerospace industries, where demand for lightweight and durable components continues to grow.

What role does sustainability-driven innovation play in shaping industrial material adoption?

Europe holds around 22% of the global atomized iron powder market, with key markets including Germany, the United Kingdom, and France collectively contributing over 65% of regional demand. The region emphasizes sustainable manufacturing practices, with more than 50% of producers adopting low-emission production technologies. Regulatory bodies have introduced strict environmental standards, leading to a 30% increase in recycling rates for metal powders. Advanced technologies such as high-purity gas atomization and digital process monitoring are widely implemented, improving production efficiency by up to 15%. Höganäs AB, a leading regional player, has invested in carbon-neutral production initiatives, reducing emissions intensity by approximately 25%. Consumer behavior in the region is strongly influenced by regulatory pressure, driving demand for environmentally compliant and high-performance materials. The automotive sector accounts for nearly 48% of regional consumption, while additive manufacturing adoption has increased by 20% in recent years.

Why is industrial expansion accelerating material demand across manufacturing ecosystems?

Asia-Pacific leads the atomized iron powder market in both production and consumption, with a total market volume exceeding 750,000 metric tons annually. China, India, and Japan are the top consuming countries, collectively accounting for over 70% of regional demand. Rapid industrialization and infrastructure development have increased demand for powder metallurgy components by approximately 35% in the past five years. The region has seen significant investment in manufacturing capacity, with over 120 new production facilities established since 2020. Technological innovation hubs in China and Japan are focusing on advanced atomization methods and nano-structured powders, improving material performance by up to 18%. JFE Steel Corporation has implemented high-efficiency production systems, enhancing output quality and reducing waste by nearly 15%. Consumer behavior reflects strong demand from automotive and electronics industries, with increasing adoption of advanced materials for electric vehicles and high-precision components.

How are industrial and infrastructure developments influencing material demand trends?

South America accounts for approximately 5% of the global atomized iron powder market, with Brazil and Argentina serving as key contributors. The region produces and consumes over 80,000 metric tons annually, with demand largely driven by automotive and construction sectors. Infrastructure development projects have increased material consumption by nearly 20% over recent years. Government incentives promoting local manufacturing and import substitution have supported the growth of domestic production facilities. Trade policies encouraging regional industrial development have also contributed to market expansion. A regional manufacturer in Brazil has adopted automated production technologies, improving efficiency by approximately 12% and reducing operational costs. Consumer behavior in the region is closely tied to industrial growth cycles, with demand fluctuations influenced by economic conditions and infrastructure investments.

What factors are shaping industrial material demand in emerging economies?

The Middle East & Africa region contributes around 3% of the global atomized iron powder market, with demand concentrated in oil & gas, construction, and emerging manufacturing sectors. Key growth countries include the United Arab Emirates and South Africa, which collectively account for over 60% of regional consumption. Infrastructure development and energy sector investments have increased demand for durable and corrosion-resistant materials by approximately 18%. Technological modernization initiatives have led to the adoption of advanced production systems, improving efficiency by nearly 10%. Trade partnerships and industrial diversification policies are supporting the expansion of local manufacturing capabilities. A regional producer in the UAE has invested in modern atomization facilities, enhancing production capacity and quality standards. Consumer behavior reflects a growing preference for cost-effective and durable materials, particularly in construction and energy-related applications.

China – 38% market share in the Atomized Iron Powder market, driven by high production capacity and extensive use in automotive and industrial manufacturing.

United States – 21% market share in the Atomized Iron Powder market, supported by strong demand from aerospace, automotive, and advanced manufacturing sectors.

The atomized iron powder market is moderately fragmented, with over 35 active global and regional competitors operating across various segments. The top five companies collectively account for approximately 52% of the total market share, indicating a balanced competitive environment with opportunities for both established players and emerging entrants. Leading companies are focusing on capacity expansion, product innovation, and strategic partnerships to strengthen their market position. Recent years have witnessed more than 20 strategic collaborations and joint ventures aimed at enhancing production efficiency and expanding geographic reach.

Technological innovation is a key competitive factor, with companies investing heavily in advanced atomization processes, including gas and hybrid techniques, to improve product quality and consistency. Automation and digitalization initiatives have enabled leading players to achieve production efficiency gains of up to 20% and reduce defect rates by nearly 30%. Additionally, sustainability has become a critical differentiator, with over 40% of major manufacturers implementing eco-friendly production methods and recycling systems.

Mergers and acquisitions activity has also increased, with at least 10 notable transactions recorded in the past three years, focusing on strengthening supply chains and expanding product portfolios. Competitive intensity is further heightened by the entry of new players leveraging innovative technologies and cost-effective production methods, creating a dynamic and evolving market landscape.

Höganäs AB

Rio Tinto Metal Powders

JFE Steel Corporation

Kobe Steel Ltd.

GKN Powder Metallurgy

Hoganas India Pvt. Ltd.

Industrial Metal Powders (India) Pvt. Ltd.

Laiwu Iron & Steel Group Powder Metallurgy Co., Ltd.

CNPC Powder Material Co., Ltd.

Pomini Tenova S.p.A.

Technological advancements in atomized iron powder production are significantly enhancing product quality, operational efficiency, and application versatility. Water atomization remains widely used, accounting for nearly 60% of global production, due to its cost efficiency and scalability. However, gas atomization is gaining traction, particularly in high-performance applications, delivering up to 25% improvement in particle sphericity and enabling tighter particle size distribution within ±10 microns. This precision is critical for additive manufacturing and advanced powder metallurgy applications.

Automation and digital process control are transforming production environments, with over 40% of large-scale manufacturers integrating AI-driven monitoring systems. These systems improve defect detection rates by approximately 35% and reduce production downtime by nearly 18%. Real-time particle size analysis and automated sieving technologies have enhanced yield efficiency by up to 20%, ensuring consistent product quality across large production batches.

Emerging technologies such as plasma atomization and ultrasonic atomization are being explored for ultra-fine powder production, achieving particle sizes below 20 microns with improved uniformity. These technologies are particularly relevant for aerospace and medical-grade components, where precision is critical. Additionally, hybrid atomization techniques combining water and gas processes are improving energy efficiency by nearly 15% while maintaining high-quality output.

Sustainability-focused innovations are also shaping the market, with energy-efficient furnaces reducing energy consumption by up to 22% and advanced filtration systems cutting emissions by approximately 28%. Recycling technologies now enable the reuse of over 30% of metal powder waste, supporting circular manufacturing practices. Digital twin technology is another emerging trend, allowing manufacturers to simulate production processes and optimize parameters, resulting in up to 12% improvement in operational efficiency and reduced material wastage.

• In March 2025, Höganäs AB announced the expansion of its production facility in Sweden, integrating advanced gas atomization technology to enhance powder quality and consistency. The upgrade is expected to improve production efficiency by 15% and support growing demand from additive manufacturing and automotive sectors. Source: www.hoganas.com

• In September 2024, Rio Tinto Metal Powders introduced a new high-purity atomized iron powder grade designed for additive manufacturing applications. The product demonstrated a 20% improvement in flowability and enhanced mechanical properties, enabling more precise component fabrication in aerospace and industrial sectors. Source: www.riotinto.com

• In May 2025, JFE Steel Corporation implemented a digital quality control system across its powder production facilities in Japan, utilizing AI-based monitoring to improve defect detection rates by 30% and reduce production inconsistencies in high-performance iron powders. Source: www.jfe-steel.co.jp

• In November 2024, GKN Powder Metallurgy launched a sustainability initiative focused on increasing the use of recycled metal powders, achieving a 25% increase in recycled material usage while reducing carbon emissions associated with production processes. Source: www.gknpm.com

The Atomized Iron Powder Market Report provides a comprehensive analysis of industry structure, covering multiple dimensions including product types, applications, end-user industries, and regional dynamics. The report evaluates key product categories such as water-atomized, gas-atomized, and specialty iron powders, which collectively account for over 90% of global production. It further examines application segments including powder metallurgy, additive manufacturing, magnetic materials, and welding consumables, with powder metallurgy alone representing nearly 65% of total usage.

Geographically, the report encompasses five major regions, analyzing production volumes, consumption patterns, and industrial trends across Asia-Pacific, North America, Europe, South America, and the Middle East & Africa. Asia-Pacific is highlighted for its large-scale manufacturing capacity exceeding 700,000 metric tons annually, while developed regions are assessed for their focus on advanced technologies and sustainability initiatives.

The scope also includes an in-depth evaluation of technological advancements such as gas atomization, hybrid atomization, and digital manufacturing integration, which are improving efficiency and product performance by up to 25%. Emerging niche segments, including ultra-fine powders for additive manufacturing and high-purity powders for electronics and medical applications, are examined for their growing industrial relevance.

Additionally, the report analyzes industry-specific demand patterns across automotive, aerospace, industrial machinery, and energy sectors, which together account for more than 80% of total consumption. It also considers regulatory frameworks, environmental compliance requirements, and sustainability initiatives influencing production and adoption. This structured approach ensures a holistic understanding of market dynamics, enabling informed decision-making for stakeholders across the value chain.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

3.3% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Höganäs AB, Rio Tinto Metal Powders, JFE Steel Corporation, Kobe Steel Ltd., GKN Powder Metallurgy, Hoganas India Pvt. Ltd., Industrial Metal Powders (India) Pvt. Ltd., Laiwu Iron & Steel Group Powder Metallurgy Co., Ltd., CNPC Powder Material Co., Ltd., Pomini Tenova S.p.A. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |