Reports

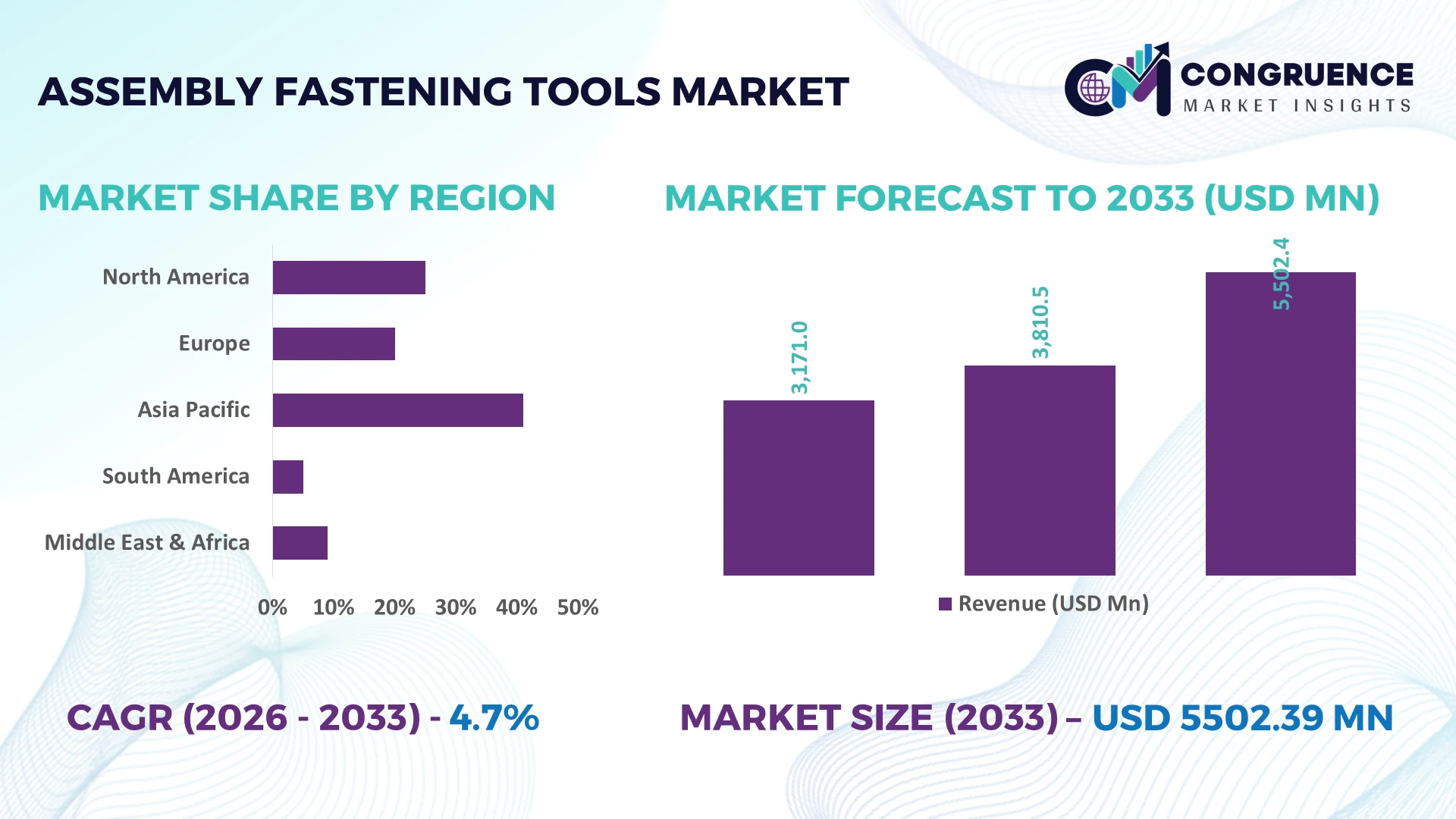

The Global Assembly Fastening Tools Market was valued at USD 3810.46 Million in 2025 and is anticipated to reach a value of USD 5502.39 Million by 2033 expanding at a CAGR of 4.7% between 2026 and 2033. Growth is supported by rising factory automation, increasing electric vehicle assembly, and wider deployment of smart torque-controlled fastening systems across high-volume manufacturing facilities.

China remains the dominant manufacturing hub, accounting for approximately 34% of global industrial production capacity for fastening equipment, supported by continued investments in automotive, electronics, and machinery sectors. Germany leads Europe through Industry 4.0 integration, with over 68% of large manufacturing plants utilizing digitally connected assembly systems, while China outpaces Germany in production scale. Ongoing supply-chain diversification following Red Sea shipping disruptions has accelerated localized tooling investments across Asia.

Manufacturers should prioritize intelligent fastening technologies and regional production strategies to strengthen supply resilience and long-term competitiveness.

Market Size & Growth: USD 3810.46 Million in 2025 reaching USD 5502.39 Million by 2033 at 4.7% CAGR, driven by automated production lines and precision assembly.

Top Growth Drivers: EV production +22%, factory automation adoption +18%, industrial robotics deployment +15% accelerate advanced fastening tool demand.

Short-Term Forecast: By 2028, smart fastening systems improve assembly efficiency by 17% while reducing rework costs by 12%.

Emerging Technologies: AI-enabled torque monitoring, cordless brushless platforms, and IoT-connected quality tracking improve fastening accuracy above 98%.

Regional Leaders: Asia-Pacific exceeds USD 2300 Million, Europe surpasses USD 1450 Million, North America crosses USD 1180 Million, supported by localized manufacturing expansion.

Consumer/End-User Trends: More than 61% of automotive manufacturers prioritize digitally calibrated fastening tools for traceability and quality assurance.

Pilot/Case Example: In 2026, an automated automotive assembly project improved fastening cycle efficiency by 19% and reduced defects by 14%.

Competitive Landscape: Top manufacturers control nearly 42% of the global market, with Atlas Copco, Stanley Black & Decker, Bosch, Makita, and Ingersoll Rand leading innovation.

Regulatory & ESG Impact: Energy-efficient production programs reduce industrial energy consumption by approximately 10% while supporting lower manufacturing emissions.

Investment & Funding: More than USD 1.3 Billion supports automation partnerships, production expansion, and digital manufacturing amid ongoing supply-chain realignment.

Innovation & Future Outlook: Advanced predictive maintenance, digital twins, and connected assembly ecosystems strengthen productivity and next-generation manufacturing strategies.

Assembly fastening tools are experiencing stronger demand across automotive, aerospace, electronics, and industrial machinery production where precision fastening directly affects product quality and throughput. Smart torque verification, battery-powered high-performance tools, and cloud-connected monitoring platforms now support over 20% faster quality validation, while regional manufacturing localization and stricter industrial compliance standards continue reshaping procurement priorities and strategic market positioning.

Assembly fastening tools have become strategically important as manufacturers compete on production accuracy, traceability, and labor efficiency rather than output volume alone. Digital manufacturing, supply-chain restructuring, and stricter quality documentation requirements are accelerating investments in intelligent fastening platforms across automotive, aerospace, electronics, and industrial equipment production. As manufacturers diversify sourcing beyond single-country dependency, localized assembly operations increasingly require standardized fastening systems capable of maintaining consistent quality across multiple production sites.

Smart fastening systems equipped with torque sensing and real-time process monitoring reduce fastening errors by nearly 30% while lowering inspection time by approximately 20% compared with conventional pneumatic tools. Japan and Germany continue to lead high-precision deployment through advanced factory automation, whereas India is expanding installations through new electronics and electric vehicle manufacturing facilities supported by industrial modernization programs. Over the next two to three years, connected fastening solutions are expected to exceed 45% adoption among newly commissioned automated production lines, reflecting stronger demand for digitally integrated manufacturing ecosystems.

A leading automotive manufacturer recently integrated AI-assisted fastening verification into an electric vehicle assembly line, reducing warranty-related fastening defects while improving production consistency. Equipment suppliers are responding through software partnerships, localized manufacturing, and modular product portfolios that simplify deployment across multiple industries. Companies that combine intelligent tooling, digital traceability, and regional manufacturing capabilities will secure stronger competitive positioning as industrial production becomes increasingly automated and quality-driven.

Accelerating industrial automation remains the strongest structural driver for the Assembly Fastening Tools Market. More than 64% of newly commissioned automotive assembly facilities now integrate digitally monitored fastening operations, while automated production cells improve fastening consistency by nearly 25% and reduce manual intervention by around 18%. China's continued investment in electric vehicle manufacturing and Germany's expansion of smart factory infrastructure are increasing demand for programmable fastening systems with integrated quality verification. In response, manufacturers are expanding regional production, strengthening automation partnerships, and introducing cordless intelligent platforms with embedded analytics. The strategic advantage extends beyond productivity, enabling manufacturers to improve product traceability, reduce warranty claims, and standardize assembly quality across geographically distributed production facilities.

Persistent fluctuations in steel, aluminum, and electronic component availability continue to constrain production planning and equipment costs. Industrial tool manufacturers have experienced component procurement lead-time increases exceeding 20% during supply disruptions, while electronic module costs remain approximately 15% above historical averages for several product categories. Dependence on specialized motor assemblies and semiconductor-based controllers exposes manufacturers to procurement uncertainty, particularly during logistics disruptions affecting Asian export routes. Companies are reducing operational risk through supplier diversification, localized component sourcing, and long-term procurement agreements. Those establishing multi-source supply strategies are improving delivery reliability while protecting manufacturing margins against continued input-cost volatility.

The next phase of market expansion lies in connected fastening ecosystems combining AI, industrial IoT, and predictive maintenance capabilities. Smart assembly platforms can reduce unplanned maintenance by nearly 22% while increasing equipment utilization by approximately 16% through continuous performance monitoring. India is rapidly expanding electronics manufacturing capacity, creating new demand for digitally integrated fastening solutions aligned with industrial modernization initiatives. Manufacturers are increasing investment in cloud-based quality management, collaborative robotics integration, and software-enabled service models that generate recurring customer value beyond hardware sales. The growing convergence of digital manufacturing and intelligent tooling creates opportunities for suppliers capable of delivering complete productivity ecosystems instead of standalone fastening equipment.

Deploying advanced fastening technologies requires synchronized investment in workforce capabilities, production software, and factory infrastructure. Nearly 38% of manufacturers report shortages of technicians qualified to manage connected assembly systems, while integration projects frequently extend commissioning schedules by approximately 15% because of compatibility and process-validation requirements. High-precision industries in the United States increasingly demand cybersecurity protection for connected production equipment, adding another layer of implementation complexity. Companies are addressing these challenges through digital training programs, technology alliances, standardized communication protocols, and scalable software architectures. Organizations that successfully integrate skilled personnel with secure intelligent manufacturing environments will establish stronger operational resilience and long-term competitive differentiation.

Smart Torque Verification Expansion Intelligent fastening platforms with integrated torque verification are becoming standard across automotive and aerospace production. More than 55% of newly installed assembly stations now incorporate digital traceability, while fastening defects decline by nearly 24% and inspection time falls by around 18%. Stricter quality compliance and recall prevention are driving deployment, prompting manufacturers to expand software partnerships and integrate fastening data directly into manufacturing execution systems.

Battery-Powered Tool Adoption Accelerates Battery-powered fastening tools are replacing pneumatic alternatives in flexible production environments, with deployment increasing by approximately 28% in high-mix manufacturing facilities. Modern lithium-ion platforms deliver nearly 20% longer operating cycles while reducing maintenance requirements by about 15%. Labor shortages and factory reconfiguration needs are encouraging manufacturers in Germany and Japan to standardize cordless platforms across multiple production lines through equipment modernization programs.

Localized Production Network Development Supply-chain diversification continues to reshape procurement strategies as manufacturers expand localized assembly capabilities. Nearly 32% of industrial firms have increased regional sourcing to reduce logistics risks, while localized tooling programs shorten equipment delivery cycles by approximately 17%. Following global shipping disruptions, equipment suppliers are restructuring production footprints, expanding local service centers, and strengthening distributor partnerships to improve operational continuity.

AI-Enabled Predictive Maintenance Integration AI-driven diagnostics are transforming maintenance workflows by identifying fastening tool wear before production failures occur. Predictive maintenance systems improve equipment availability by nearly 21% while reducing unexpected downtime by approximately 16%. Large manufacturers increasingly combine machine learning with connected sensors to optimize service intervals, leading suppliers to embed analytics, cloud monitoring, and remote support capabilities into next-generation fastening platforms.

Electric Tools represent the largest segment because they provide consistent torque control, seamless automation integration, and lower maintenance requirements than conventional alternatives. Nearly 47% of automated production facilities now prioritize electric fastening systems for quality-critical operations, while digitally controlled platforms improve fastening accuracy by approximately 22%. Pneumatic Tools remain widely deployed in high-volume manufacturing because of their durability and proven production performance. Hydraulic Tools retain strategic importance in heavy industrial applications requiring high fastening force, whereas Manual Tools continue serving maintenance, repair, and low-volume assembly environments where flexibility outweighs automation.

Battery-Powered Tools are the fastest-growing segment as manufacturers prioritize mobility, ergonomic operation, and flexible production layouts. Adoption has increased by nearly 29% across electronics and automotive assembly operations as advanced lithium-ion technology extends operating time and reduces maintenance interruptions. Manufacturers are accelerating product innovation through brushless motors, smart battery management, and connected diagnostics while expanding localized production and distribution networks to meet rising enterprise demand. Investment priorities increasingly favor intelligent cordless platforms capable of integrating with digital manufacturing ecosystems.

Automotive Assembly remains the leading application as vehicle production requires thousands of precision fastening operations supported by strict torque validation and traceability standards. More than 60% of advanced vehicle production lines now utilize digitally monitored fastening systems, reducing assembly errors by approximately 20%. Industrial Manufacturing follows as a mature application, benefiting from factory modernization and automated production cells. Construction continues using fastening tools for structural assembly and installation activities, while Aerospace Assembly depends on high-precision fastening technologies for safety-critical components.

Electronics Assembly is the fastest-growing application because miniaturized devices require highly accurate fastening with programmable torque control. Automated electronics production has increased smart fastening deployment by nearly 27%, while cycle times improve by approximately 16% through integrated robotic assembly. Companies are responding by developing compact intelligent tools, expanding automation partnerships, and tailoring fastening solutions for high-density manufacturing environments. Demand is shifting toward digitally connected platforms capable of supporting quality assurance and production flexibility across multiple industries.

Automotive remains the dominant end-user because large-scale vehicle manufacturing depends on standardized fastening quality, automated assembly, and comprehensive production traceability. Nearly 63% of vehicle manufacturers have expanded deployment of connected fastening systems to strengthen quality control and reduce rework by approximately 18%. Manufacturing enterprises broadly continue investing in fastening automation to improve productivity across machinery, industrial equipment, and consumer goods production. Construction maintains steady procurement through infrastructure development, while Aerospace & Defense emphasizes certified fastening precision for mission-critical assemblies.

Electronics is the fastest-growing end-user segment as compact product designs demand precise, repeatable fastening processes integrated with automated production equipment. Adoption of intelligent fastening technologies has increased by nearly 26% among electronics manufacturers, while digitally monitored assembly reduces quality deviations by approximately 15%. Suppliers are strengthening competitive positioning through customized product portfolios, software-enabled service offerings, and strategic partnerships with automation integrators. Future purchasing decisions increasingly favor connected fastening ecosystems that combine precision, flexibility, and production data visibility.

Asia-Pacific accounted for the largest market share at 42.8% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a 5.9% between 2026 and 2033.

Smart Manufacturing Drives Precision Assembly

North America represents a mature deployment market supported by advanced automotive, aerospace, and industrial manufacturing. The region accounts for approximately 24% of global demand, with intelligent fastening systems increasingly integrated into connected production environments. More than 62% of large manufacturers have adopted digital torque verification within automated assembly processes to improve traceability and quality compliance. Expansion of electric vehicle manufacturing and aerospace modernization programs continues to strengthen enterprise investment in programmable fastening equipment. Equipment suppliers are expanding software-enabled service portfolios and regional technical support capabilities to accelerate deployment while minimizing production interruptions.

United States Market Outlook: The United States remains the regional leader due to its extensive automotive, aerospace, and industrial equipment manufacturing base. High adoption of Industry 4.0 technologies and collaborative robotics supports increasing deployment of intelligent fastening platforms. Approximately 68% of major vehicle assembly plants utilize digitally monitored fastening systems, encouraging suppliers to strengthen domestic manufacturing, application engineering, and aftermarket support for high-value industrial customers.

Industrial Digitalization Reshapes Manufacturing Standards

Europe continues strengthening its position through advanced engineering, precision manufacturing, and factory modernization initiatives. The region contributes nearly 27% of global deployment, supported by automotive production, aerospace engineering, and industrial automation investments. More than 58% of newly upgraded manufacturing facilities now integrate connected fastening technologies aligned with digital quality management objectives. Sustainability targets and energy-efficient production systems are encouraging manufacturers to replace conventional assembly equipment with intelligent electric alternatives. Strategic collaborations between automation providers and industrial equipment manufacturers continue improving production flexibility and operational consistency.

Germany Market Outlook: Germany leads the regional market through its globally competitive automotive and machinery industries supported by advanced industrial automation. High adoption of digitally integrated production systems enables manufacturers to maintain precise fastening quality across complex assembly operations. Nearly 70% of large industrial facilities have implemented Industry 4.0-enabled manufacturing processes, encouraging continued investment in connected fastening technologies and intelligent production infrastructure.

Manufacturing Scale Accelerates Technology Deployment

Asia-Pacific remains the largest production and consumption hub because of its extensive automotive, electronics, and industrial manufacturing ecosystem. The region contributes approximately 43% of global market activity, supported by expanding factory automation and strong export-oriented manufacturing. Nearly 65% of new electronics manufacturing investments incorporate automated fastening solutions to improve consistency and production throughput. Ongoing industrial diversification and localized supply-chain strategies continue driving deployment of intelligent fastening equipment across multiple manufacturing sectors. Suppliers are expanding production capacity and regional engineering support to meet increasing enterprise demand.

China Market Outlook: China dominates the regional landscape through its large-scale automotive, electronics, and industrial equipment manufacturing capabilities. Rapid factory automation and continuing investment in intelligent production technologies support widespread deployment of connected fastening systems. More than 34% of global industrial manufacturing capacity is concentrated in China, encouraging leading equipment manufacturers to expand localized production, technology partnerships, and smart manufacturing solutions.

Industrial Modernization Supports Stable Demand

South America is experiencing steady demand driven by automotive assembly, industrial manufacturing, and infrastructure development projects. The region accounts for approximately 4.8% of global market activity while manufacturers increasingly modernize production facilities with automated assembly technologies. Industrial equipment upgrades have improved production efficiency by nearly 14% in several manufacturing sectors. Although logistics limitations and capital investment constraints continue affecting deployment speed, companies are strengthening regional distribution networks and localized technical services to improve equipment availability and operational reliability.

Brazil Market Outlook: Brazil represents the largest market in South America due to its diversified automotive manufacturing base and expanding industrial production. National manufacturers continue investing in production modernization and automated assembly processes to improve competitiveness. More than half of the region's vehicle manufacturing capacity is concentrated in Brazil, encouraging fastening equipment suppliers to expand partnerships, technical support capabilities, and localized product offerings.

Industrial Investment Expands Manufacturing Capabilities

The Middle East & Africa market is advancing through industrial diversification, infrastructure expansion, and manufacturing localization initiatives. The region contributes approximately 3.6% of global demand while increasing investment in industrial production zones and advanced manufacturing facilities. More than 20% of newly announced industrial projects include automated assembly technologies to improve operational productivity. Growth in energy equipment manufacturing, transportation infrastructure, and industrial processing is encouraging suppliers to establish stronger regional partnerships and technical service capabilities supporting long-term deployment.

Saudi Arabia Market Outlook: Saudi Arabia leads regional investment through industrial diversification initiatives, manufacturing expansion, and infrastructure modernization programs. New industrial cities and advanced production facilities are increasing demand for automated fastening equipment across machinery, transportation, and construction industries. Industrial localization programs continue attracting international manufacturers, while ongoing factory modernization strengthens opportunities for intelligent assembly technologies and long-term equipment deployment.

The Assembly Fastening Tools Market is led by global manufacturers including Atlas Copco, Stanley Black & Decker, Bosch, Makita, and Ingersoll Rand, competing directly against regional industrial tool specialists and low-cost Asian manufacturers. The top five players collectively account for approximately 42% of the market, creating intense competition between technology leaders emphasizing connected solutions and price-focused suppliers targeting standard industrial applications. Competition increasingly depends on digital torque accuracy, service responsiveness, and production flexibility, with intelligent fastening systems improving assembly precision by nearly 25% and predictive maintenance reducing downtime by around 20%. Companies are strengthening market positions through localized manufacturing, automation partnerships, software integration, and selective vertical integration of critical components to improve delivery reliability. Competitive momentum is shifting toward AI-enabled, traceable fastening platforms rather than standalone hardware, driving consolidation around digital manufacturing ecosystems. High certification requirements, industrial software integration, and established distribution networks remain significant entry barriers. Winning requires intelligent products, localized support, rapid deployment capability, and continuous innovation beyond price competition.

Atlas Copco

Stanley Black & Decker

Robert Bosch GmbH

Makita Corporation

Ingersoll Rand

Apex Tool Group

Hilti AG

Techtronic Industries (TTI)

Panasonic Connect

ESTIC Corporation

Desoutter Industrial Tools

AIMCO (Assembly Tools)

Digital transformation is redefining assembly fastening through AI-enabled torque control, industrial IoT connectivity, and real-time quality verification. More than 57% of newly automated production lines now deploy connected fastening platforms that improve assembly consistency by approximately 24% while reducing manual inspection effort by nearly 18%. Cloud-based production analytics are increasingly integrated with manufacturing execution systems, allowing manufacturers to identify fastening deviations immediately and maintain full process traceability across high-volume production environments. Automotive and aerospace manufacturers benefit most because precision and compliance directly influence operational efficiency and warranty performance.

Battery-powered intelligent fastening tools are rapidly replacing conventional pneumatic systems in flexible manufacturing environments. Compared with legacy pneumatic equipment, advanced brushless cordless platforms improve operator mobility by approximately 30% while reducing maintenance requirements by nearly 20%. Around 46% of new electronics assembly facilities now prioritize programmable electric fastening systems supporting robotic automation and digital quality management. Equipment suppliers are combining embedded sensors, wireless diagnostics, and predictive maintenance software to differentiate products through operational intelligence rather than mechanical performance alone.

Between 2026 and 2028, digital twin integration, edge AI analytics, and collaborative robot compatibility will become defining competitive technologies. Manufacturers investing in interoperable fastening ecosystems will achieve faster production changeovers, stronger traceability, and lower lifecycle operating costs. Technology leaders with integrated hardware, software, and lifecycle service capabilities will outperform suppliers focused solely on conventional fastening equipment as intelligent manufacturing becomes the industry standard.

March 2025 – Desoutter Industrial Tools introduced the AXON controller for corded assembly solutions, delivering a unified control architecture that supports multiple fastening applications and improves production flexibility by up to 20% through simplified integration. This strengthens digital manufacturing capabilities across industrial assembly operations. Source: desouttertools.com

July 2025 – Atlas Copco Group received the Red Dot Design Award for its MTRwrench industrial assembly tool featuring integrated error-proofing, rapid battery replacement, and enhanced communication capabilities that minimize production downtime. The tool incorporates recycled plastic in its construction, reinforcing sustainable product innovation. Source: atlascopcogroup.com

October 2025 – Desoutter Industrial Tools launched Connect-D, a digital industrial smart hub enabling centralized connectivity for assembly equipment and production data. The platform supports 100% digital workflow integration, improving traceability and enabling faster operational decision-making for smart factory environments. Source: desouttertools.com

March 2026 – Desoutter Industrial Tools introduced the EIDS next-generation low-torque transducerized screwdriver platform for industrial assembly, enhancing precision fastening while supporting connected manufacturing environments. The system delivers 100% transducerized torque measurement, improving process accuracy and quality assurance in electronics and precision manufacturing.

This report delivers comprehensive analysis of the Assembly Fastening Tools Market across major product types, applications, end-users, and key geographic regions. It evaluates Pneumatic Tools, Electric Tools, Battery-Powered Tools, Hydraulic Tools, and Manual Tools while assessing demand across automotive assembly, electronics manufacturing, aerospace, industrial production, and construction. The study further benchmarks competitive positioning of leading manufacturers and analyzes adoption patterns, with intelligent fastening technologies now deployed in more than 55% of newly automated production environments.

The report provides strategic insights supporting investment planning, product development, manufacturing expansion, and market-entry decisions between 2026 and 2033. It examines regional deployment trends, enterprise purchasing behavior, technology integration, digital manufacturing adoption, and emerging opportunities in connected fastening ecosystems. Coverage also includes automation-driven productivity improvements, evolving supply-chain strategies, sustainability initiatives, and competitive differentiation through software-enabled assembly systems, enabling decision-makers to identify high-priority growth segments and strengthen long-term operational positioning across mature and emerging industrial markets.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 3810.46 Million |

Market Revenue in 2033 | USD 5502.39 Million |

CAGR (2026 - 2033) | 4.7% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Atlas Copco, Stanley Black & Decker, Robert Bosch GmbH, Makita Corporation, Ingersoll Rand, Apex Tool Group, Hilti AG, Techtronic Industries (TTI), Panasonic Connect, ESTIC Corporation, Desoutter Industrial Tools, AIMCO (Assembly Tools) |

Customization & Pricing | Available on Request (10% Customization is Free) |