Reports

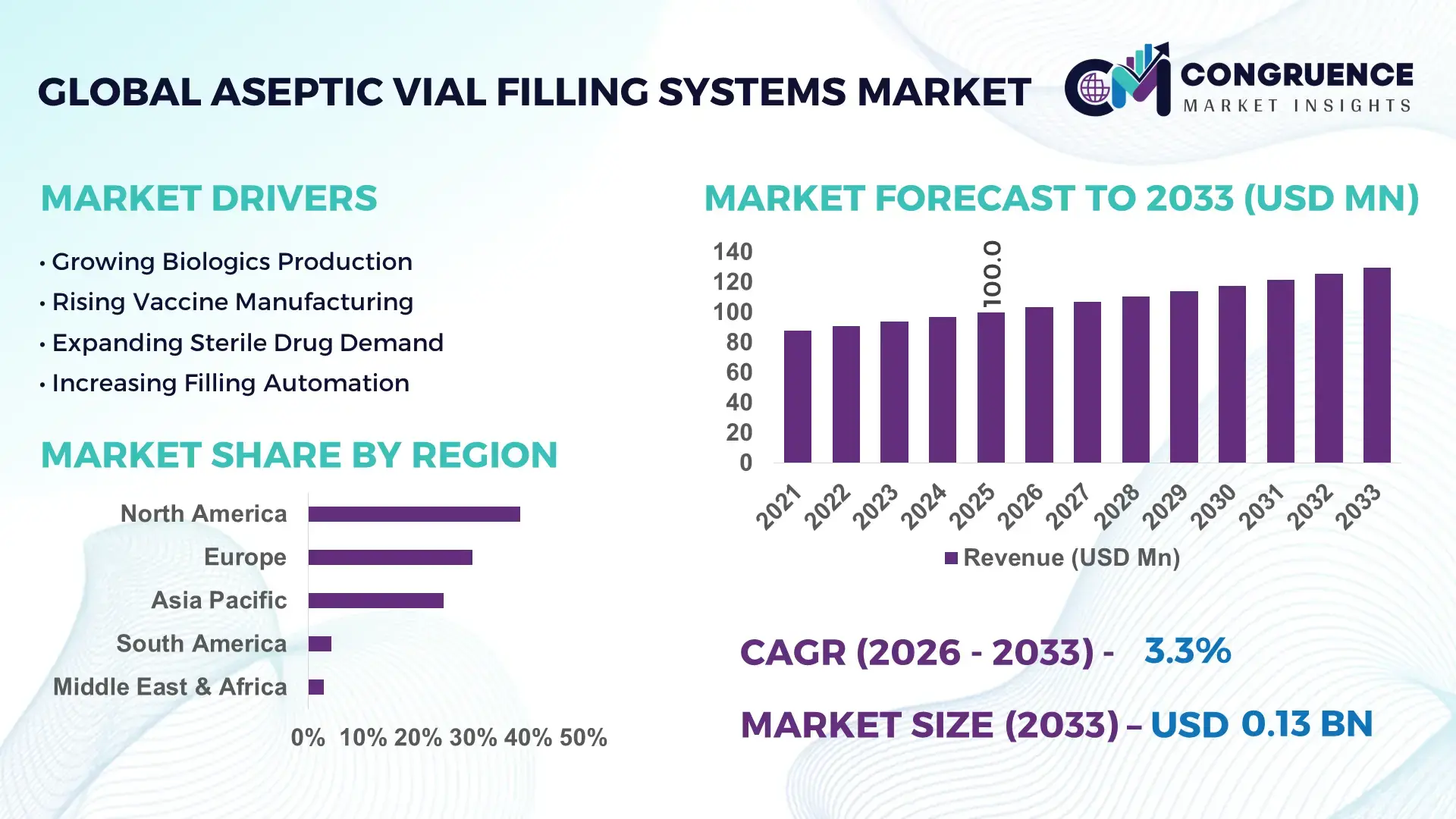

The Global Aseptic Vial Filling Systems Market was valued at USD 100.0 Million in 2025 and is anticipated to reach a value of USD 129.7 Million by 2033 expanding at a CAGR of 3.3% between 2026 and 2033. Growth is being accelerated by rising deployment of high-speed robotic fill-finish lines for injectable biologics, vaccines, and sterile oncology drugs under increasingly stringent aseptic manufacturing requirements.

The United States remains the dominant country, accounting for approximately 31% of global sterile injectable manufacturing capacity, supported by more than USD 2 billion in recent pharmaceutical fill-finish investments and widespread adoption of isolator-based systems exceeding 70% among new facilities. In comparison, Germany commands a stronger concentration of advanced pharmaceutical engineering expertise, while U.S. facilities operate larger-scale commercial biologics production lines. Ongoing pharmaceutical supply-chain reshoring initiatives following COVID-19 disruptions continue to strengthen domestic aseptic infrastructure.

Strategically, manufacturers prioritizing automated, contamination-controlled filling environments are positioned to secure higher-value contracts and improve long-term production resilience.

Market Size & Growth: Valued at USD 100.0 Million in 2025 and projected to reach USD 129.7 Million by 2033 at 3.3% CAGR, supported by expanding biologics fill-finish capacity and advanced sterile manufacturing investments.

Top Growth Drivers: Biologics production expansion (+24%), isolator adoption (+18%), and injectable drug pipeline growth (+21%) are reshaping global demand patterns.

Short-Term Forecast: By 2028, automated filling operations are expected to improve line efficiency by 15% while reducing manual intervention requirements by 20%.

Emerging Technologies: AI-enabled process monitoring, robotic aseptic handling, and digital twin validation platforms are improving sterility assurance and operational consistency.

Regional Leaders: North America (~USD 42 Million), Europe (~USD 33 Million), and Asia-Pacific (~USD 20 Million) lead deployment, driven by biologics expansion, contract manufacturing, and pharmaceutical localization initiatives.

Consumer/End-User Trends: More than 65% of new injectable drug projects now specify advanced aseptic fill-finish capabilities during commercial manufacturing planning.

Pilot/Case Example: In 2024, multiple pharmaceutical facilities integrating robotic isolators reported contamination-risk reductions exceeding 30% and batch release improvements of 18%.

Competitive Landscape: The leading supplier controls approximately 16% market share, with key participants including Syntegon, Bausch+Ströbel, IMA Group, OPTIMA, and Groninger.

Regulatory & ESG Impact: Advanced closed-system filling technologies reduce cleanroom energy consumption by nearly 12% while supporting evolving sterile manufacturing compliance standards.

Investment & Funding: More than USD 4 billion has been committed globally to sterile injectable and fill-finish infrastructure expansion amid pharmaceutical supply-chain diversification.

Innovation & Future Outlook: Next-generation modular filling platforms, real-time contamination analytics, and flexible multi-product lines are strengthening high-growth pharmaceutical manufacturing strategies.

The Aseptic Vial Filling Systems Market is witnessing strong demand from biologics, vaccines, cell therapies, and high-potency injectable pharmaceuticals. Recent innovations include robotic isolators, automated environmental monitoring, and modular fill-finish platforms that shorten changeover times by nearly 25%. Pharmaceutical manufacturers are increasingly localizing sterile production networks to reduce supply-chain exposure while meeting evolving regulatory expectations, creating a favorable environment for advanced aseptic processing investments and strategic capacity expansion.

Aseptic vial filling systems have become strategically important as pharmaceutical manufacturers compete to secure reliable sterile production capacity for biologics, vaccines, and specialized injectable therapies. The industry is undergoing a significant transformation driven by supply-chain restructuring, pharmaceutical reshoring programs, and stricter sterile manufacturing requirements. Manufacturers increasingly view advanced fill-finish infrastructure as a competitive asset that improves production flexibility, regulatory readiness, and contract manufacturing attractiveness.

Technology modernization is accelerating deployment decisions. Modern isolator-based filling systems can reduce contamination risks by more than 30% compared with conventional open cleanroom operations while lowering manual interventions by approximately 40%. The United States and Germany continue to lead large-scale commercial deployments, whereas India and China are rapidly expanding capacity through pharmaceutical infrastructure investments and contract manufacturing growth. Over the next two to three years, automated aseptic production lines are expected to account for a substantially larger share of newly commissioned facilities.

Operational examples include pharmaceutical manufacturers integrating robotics, automated inspection, and digital batch-record platforms to improve throughput consistency and compliance efficiency. Companies are strengthening partnerships with equipment suppliers, expanding sterile manufacturing footprints, and prioritizing modular production architectures. Organizations that establish scalable, highly automated aseptic filling capabilities will secure stronger competitive positioning, faster commercialization pathways, and greater long-term operational resilience.

Biologics now represent more than 35% of late-stage pharmaceutical pipelines, while injectable medicines account for over 60% of newly approved specialty therapies in several advanced pharmaceutical markets. This shift is increasing demand for contamination-controlled fill-finish operations capable of supporting complex formulations. Regulatory agencies have intensified scrutiny of sterile manufacturing processes, encouraging wider adoption of isolator technology and automated aseptic handling systems. The result is a direct increase in investments toward high-speed filling lines, robotics, and digital monitoring platforms. Pharmaceutical companies are responding through capacity expansions, strategic equipment upgrades, and long-term technology partnerships. A notable operational insight is that facilities implementing advanced automation report significantly lower deviation rates, strengthening production reliability and supporting premium contract manufacturing opportunities.

Aseptic vial filling infrastructure requires substantial upfront investment, with equipment, cleanroom integration, and qualification activities representing a significant share of project costs. Validation programs can extend implementation timelines by 20–30%, creating deployment bottlenecks for smaller manufacturers. Supply dependency on specialized components, sterile barriers, and precision filling technologies further increases operational complexity. Recent pharmaceutical equipment lead times have remained elevated in several industrial markets due to component sourcing constraints and engineering capacity limitations. To reduce risk, manufacturers are diversifying supplier networks, localizing procurement strategies, and negotiating long-term equipment agreements. A key strategic limitation remains the ability to balance regulatory compliance requirements with cost-effective capacity expansion without compromising operational efficiency.

Emerging pharmaceutical manufacturing hubs in India, Saudi Arabia, and Southeast Asia are creating significant opportunities for modular aseptic filling technologies. Automated systems can reduce manual interventions by more than 40% while improving line utilization rates by approximately 15–20%. The growing adoption of digital validation, AI-assisted process monitoring, and predictive maintenance platforms is further enhancing equipment productivity. Governments are supporting domestic pharmaceutical manufacturing through localization incentives, infrastructure programs, and strategic healthcare investments. Companies are positioning themselves through R&D partnerships, regional manufacturing expansions, and integrated service ecosystems. A less obvious opportunity lies in flexible multi-product filling platforms that enable rapid adaptation to smaller biologics batches and personalized medicine production requirements.

The transition toward highly automated aseptic manufacturing environments is increasing integration complexity across robotics, software platforms, environmental monitoring systems, and regulatory documentation frameworks. Industry surveys indicate that skilled pharmaceutical automation specialists remain in limited supply, while advanced digital manufacturing competencies are becoming critical operational requirements. Facilities implementing multiple connected systems often experience integration periods extending 15–25% beyond initial project estimates. Cybersecurity considerations and data integrity requirements add further complexity as manufacturing environments become increasingly digitized. Companies must address these challenges through workforce development programs, specialized technology partnerships, and infrastructure modernization initiatives. Organizations that successfully integrate automation, compliance, and digital operations will establish stronger long-term competitiveness and more sustainable production scalability.

Robotic Isolator Integration Accelerates Advanced robotic isolators are being deployed across new sterile manufacturing facilities, reducing operator intervention by nearly 40% and lowering contamination events by more than 30%. Regulatory scrutiny around aseptic processing and workforce availability challenges are driving adoption. Pharmaceutical manufacturers in the United States and Germany are prioritizing closed-system architectures, while equipment suppliers are expanding automation partnerships to improve batch consistency, line utilization, and compliance performance.

Modular Fill-Finish Deployment Expands Pharmaceutical companies are increasingly adopting modular filling platforms that reduce installation timelines by 25–35% and improve facility flexibility by approximately 20%. The shift is being driven by faster biologics commercialization cycles and changing production volumes. Instead of building large dedicated lines, manufacturers are deploying scalable modules capable of supporting multiple vial formats. Equipment providers are responding through standardized platform designs, integrated digital controls, and faster commissioning programs that improve operational agility.

Digital Process Validation Gains Ground Automated environmental monitoring, electronic batch records, and AI-assisted process analytics are transforming aseptic operations. Facilities implementing digital validation frameworks report documentation efficiency improvements exceeding 30% and deviation investigation times reduced by nearly 25%. Labor shortages and increasingly complex compliance requirements are accelerating adoption. Companies are investing in connected manufacturing ecosystems that strengthen traceability, accelerate quality reviews, and improve production decision-making across multiple facilities.

Regionalized Sterile Manufacturing Strategies Pharmaceutical supply-chain restructuring continues to influence aseptic filling investments, with localized sterile production capacity expanding by approximately 18% across several strategic manufacturing hubs. A notable shift involves contract manufacturers securing dedicated fill-finish capabilities closer to end markets to reduce logistics risk and improve delivery reliability. Companies are pursuing regional partnerships, targeted facility expansions, and technology transfer agreements to strengthen operational resilience while maintaining product availability during global supply disruptions.

Automated aseptic vial filling systems represent the leading segment, accounting for an estimated 62% of installations due to superior throughput, contamination control, and operational consistency. Pharmaceutical manufacturers increasingly favor fully automated platforms because they reduce manual interventions by more than 40% while improving batch reproducibility and regulatory compliance. Their scalability supports high-volume biologics and vaccine production, making them the preferred choice for commercial manufacturing facilities. Semi-automated systems continue to maintain relevance among mid-sized pharmaceutical companies seeking balanced investment costs and operational flexibility. The fastest-growing segment is robotic-integrated automated filling systems, driven by increasing adoption of isolator technology and digital process controls. Deployment activity has increased by approximately 22% over the past two years as manufacturers prioritize workforce efficiency and sterility assurance. Meanwhile, conventional semi-automated configurations remain important for specialized production runs and lower-volume injectable therapies. Equipment suppliers are responding through modular automation upgrades, strategic technology partnerships, and expanded service offerings. Investment priorities are increasingly shifting toward flexible, data-enabled filling environments capable of supporting multiple product formats and evolving compliance requirements.

Biologics manufacturing remains the dominant application segment, representing approximately 45% of aseptic vial filling system utilization due to the growing complexity of monoclonal antibodies, recombinant therapies, and specialty injectables. Sterility requirements, product sensitivity, and large-scale production needs continue to concentrate demand within this category. Vaccine manufacturing also maintains a significant position, supported by long-term immunization programs and national preparedness initiatives. Pharmaceutical companies are expanding dedicated biologics fill-finish infrastructure to improve production reliability and shorten commercialization timelines. Cell and gene therapy applications are emerging as the fastest-growing segment, with deployment activity increasing by nearly 25% as personalized medicine programs expand. These therapies require flexible batch sizes, enhanced contamination controls, and advanced process monitoring. Oncology injectables and specialty pharmaceuticals continue to strengthen demand for precision filling technologies, while contract manufacturing organizations increasingly support diversified application requirements. Companies are investing in adaptable production platforms, integrated quality systems, and specialized filling capabilities to address evolving therapeutic portfolios and changing production requirements.

Pharmaceutical and biopharmaceutical manufacturers constitute the largest end-user segment, accounting for roughly 58% of total demand due to extensive sterile production requirements, large-scale infrastructure investments, and ongoing biologics expansion programs. These organizations depend on advanced aseptic filling systems to maintain production continuity, compliance standards, and product quality. Their purchasing decisions are increasingly influenced by automation capabilities, digital integration, and long-term operational efficiency. Large pharmaceutical enterprises continue to modernize legacy facilities through phased equipment upgrades and advanced fill-finish technologies. Contract Manufacturing Organizations (CMOs) represent the fastest-growing end-user segment, supported by increasing outsourcing activity and demand for flexible production capacity. CMO utilization has expanded by approximately 20% as pharmaceutical companies seek to optimize capital allocation and accelerate product launches. Research-focused manufacturers and specialized injectable producers remain strategically relevant, particularly in emerging therapeutic categories. Equipment providers are tailoring offerings through customized platform configurations, long-term service agreements, and collaborative development programs. Competitive positioning is increasingly determined by the ability to provide scalable, multi-client manufacturing solutions with rapid deployment capabilities.

North America accounted for the largest market share at 38.5% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 4.1% between 2026 and 2033.

North America maintains its leadership position through a dense concentration of biologics manufacturers, contract development and manufacturing organizations (CDMOs), and advanced sterile injectable facilities. The region accounts for approximately 38.5% of global market activity, supported by widespread deployment of isolator-based filling systems and digital manufacturing platforms. More than 70% of newly commissioned sterile facilities in the United States now incorporate automated aseptic handling technologies, improving contamination control and operational consistency. Pharmaceutical supply-chain reshoring initiatives continue to drive facility upgrades, while strategic partnerships between equipment suppliers and drug manufacturers accelerate deployment timelines. Investments remain focused on flexible multi-product lines capable of supporting biologics, vaccines, and specialty injectable therapies.

United States Market Outlook: The United States serves as the region’s primary innovation and deployment hub, supported by its extensive biologics manufacturing ecosystem and strong pharmaceutical investment pipeline. The country hosts approximately one-third of global sterile injectable production capacity and continues expanding advanced fill-finish infrastructure. Large pharmaceutical companies are integrating robotics, AI-enabled process monitoring, and digital batch management systems to improve productivity and compliance. Increased domestic pharmaceutical manufacturing initiatives have also strengthened demand for modular aseptic filling technologies capable of supporting diversified therapeutic portfolios.

Europe represents approximately 29.8% of global market participation, supported by strong pharmaceutical engineering capabilities and stringent sterile manufacturing standards. Regulatory emphasis on contamination control and data integrity continues to accelerate adoption of advanced aseptic filling technologies. Pharmaceutical manufacturers across Germany, Switzerland, and Italy are upgrading legacy fill-finish operations with robotic isolators and automated environmental monitoring systems. Recent facility modernization projects have improved production efficiency by nearly 15% in several high-volume sterile manufacturing sites. The region also benefits from strong collaboration between equipment manufacturers and pharmaceutical producers, fostering innovation in flexible and high-precision vial filling platforms.

Germany Market Outlook: Germany remains Europe’s most strategically significant market due to its advanced pharmaceutical machinery sector and high concentration of sterile drug production facilities. The country plays a critical role in equipment design, engineering innovation, and aseptic processing technology development. More than 60% of newly installed pharmaceutical filling lines in major manufacturing clusters now incorporate advanced automation capabilities. German manufacturers continue investing in digital validation technologies and precision filling systems, strengthening their position as global suppliers of high-performance aseptic processing solutions.

Asia-Pacific accounts for approximately 24.6% of global market activity and is rapidly strengthening its position through pharmaceutical manufacturing expansion and infrastructure development. Large-scale investments in sterile injectable production, vaccine manufacturing, and biologics processing are increasing demand for advanced vial filling technologies. Several countries have expanded domestic pharmaceutical production programs, resulting in a nearly 20% increase in sterile manufacturing capacity additions over recent years. Manufacturers are adopting modular filling systems and automation technologies to support export-oriented production and regulatory compliance. The region’s combination of cost competitiveness, industrial scale, and growing technical expertise continues to attract global pharmaceutical partnerships.

China Market Outlook: China leads regional deployment activity through extensive pharmaceutical manufacturing capacity, large biologics investments, and expanding sterile production infrastructure. Government-supported pharmaceutical modernization initiatives have accelerated adoption of automated fill-finish systems across major industrial clusters. More than 50 new sterile manufacturing projects have entered various stages of development and validation in recent years. Domestic manufacturers are increasingly collaborating with international equipment providers to improve production quality, strengthen export readiness, and support high-value injectable drug manufacturing programs.

South America contributes approximately 4.2% of global market activity, with growth supported by expanding domestic pharmaceutical manufacturing and increasing healthcare infrastructure investment. Regional demand is concentrated around sterile injectable production, vaccine filling operations, and contract manufacturing activities. Several pharmaceutical companies are upgrading legacy production facilities to comply with evolving quality standards and improve operational efficiency. Recent infrastructure investments have expanded sterile manufacturing capabilities by nearly 12% across selected pharmaceutical hubs. While technology adoption continues to advance, equipment import dependency and specialized workforce availability remain important operational considerations influencing deployment timelines.

Brazil Market Outlook: Brazil represents the largest and most influential market in South America due to its sizable pharmaceutical industry and expanding biologics production activities. The country continues investing in sterile manufacturing modernization programs aimed at reducing import dependence and strengthening healthcare supply security. Leading pharmaceutical manufacturers are integrating advanced filling and inspection technologies into existing facilities to improve throughput and quality performance. Growing collaboration between local manufacturers and international technology providers is accelerating access to modern aseptic processing solutions and supporting long-term industrial development.

The Middle East & Africa region accounts for approximately 2.9% of global market activity and is increasingly influenced by pharmaceutical localization strategies and healthcare infrastructure modernization. Governments are prioritizing domestic drug manufacturing capabilities to improve supply security and reduce reliance on imported sterile medicines. Multiple pharmaceutical industrial projects have been launched across key markets, with several facilities incorporating advanced aseptic filling technologies from inception. Regional investments in pharmaceutical manufacturing infrastructure have increased by more than 15% over recent years. Market participants are focusing on technology transfer partnerships, workforce development, and regulatory capability enhancement to strengthen long-term competitiveness.

Saudi Arabia Market Outlook: Saudi Arabia stands out as the region’s leading market due to large-scale pharmaceutical investment programs, industrial diversification initiatives, and healthcare manufacturing priorities. The country is actively expanding sterile injectable production capacity through public-private partnerships and advanced pharmaceutical infrastructure projects. Several new pharmaceutical facilities are being designed around automated aseptic processing environments, supporting higher-quality domestic production. Continued investment in manufacturing ecosystems, technical training, and international technology collaboration is positioning Saudi Arabia as a strategic hub for sterile pharmaceutical production within the broader region.

The competitive landscape is led by global technology providers such as Syntegon, IMA Group, OPTIMA, Bausch+Ströbel, and Groninger, which compete directly against regional equipment suppliers and lower-cost system integrators. The top five players collectively control approximately 52% of global market activity, reflecting a moderately consolidated structure centered on technology leadership rather than price alone.

Competition increasingly revolves around automation performance, contamination control, deployment speed, and lifecycle service capabilities. Advanced robotic filling platforms deliver up to 30% lower operator intervention and nearly 20% faster line changeovers, creating a measurable competitive advantage. Companies are expanding manufacturing footprints, forming pharmaceutical partnerships, integrating digital validation tools, and strengthening end-to-end fill-finish portfolios.

The current competitive shift favors highly automated, Annex 1-compliant solutions. Validation expertise, regulatory credibility, and installed-base support remain major entry barriers. Winning requires proven sterility performance, scalable automation, and strong pharmaceutical customer integration.

IMA Group

OPTIMA

Bausch+Ströbel

Groninger

Vanrx Pharmasystems

Cozzoli Machine Company

Watson-Marlow Fluid Technology Solutions

Steriline

Tofflon Science and Technology Group

Dara Pharmaceutical Packaging

AST Inc. (Automated Systems of Tacoma)

Aseptic vial filling technology is rapidly transitioning from conventional cleanroom-dependent operations toward fully enclosed robotic and isolator-based platforms. Automated isolator systems now reduce operator interventions by more than 40% while improving contamination control performance by approximately 30%. Adoption rates continue to rise, with over 70% of newly commissioned sterile manufacturing projects incorporating advanced automation capabilities. Pharmaceutical manufacturers benefit through lower deviation rates, faster batch release cycles, and stronger regulatory compliance outcomes.

Emerging technologies include AI-enabled process analytics, digital batch records, machine vision inspection, and predictive maintenance platforms. Facilities deploying integrated digital manufacturing tools report documentation efficiency improvements exceeding 30% and quality review cycle reductions near 25%. Compared with legacy filling environments, next-generation robotic systems support up to 20% faster product changeovers and significantly improved production flexibility. Global pharmaceutical companies and large CDMOs are benefiting most due to their need for scalable, multi-product manufacturing capabilities.

Between 2026 and 2028, disruptive innovations will focus on gloveless isolators, autonomous material handling, and digital twin validation environments. Companies investing early in connected fill-finish ecosystems will strengthen operational resilience, accelerate technology transfer activities, and gain a competitive advantage through faster deployment, improved sterility assurance, and enhanced manufacturing scalability.

May 2025 – Syntegon unveiled the SynTiso gloveless aseptic filling platform developed with pharmaceutical partners. The system processes up to 600 containers per minute while reducing contamination exposure through full automation. The launch strengthens next-generation fill-finish productivity and Annex 1 compliance readiness. Source: www.syntegon.com

September 2025 – Syntegon reported strong growth in its pharma segment, supported by rising demand for isolator-equipped fill-finish solutions. The company achieved 11% sales growth in the first half of 2025, reinforcing investment momentum in advanced aseptic manufacturing technologies.

March 2026 – BioTechnique expanded aseptic fill-finish and lyophilization capabilities at its Pennsylvania facility. The site includes 268,000 square feet of manufacturing space and advanced filling infrastructure, enhancing support for clinical and commercial sterile drug programs.

April 2026 – PCI Pharma Services announced sterile fill-finish expansion initiatives backed by investments exceeding USD 1 billion across U.S. and European operations. The program strengthens high-speed vial filling and drug-device manufacturing capabilities while supporting pharmaceutical supply-chain resilience.

The report provides comprehensive analysis of the aseptic vial filling systems industry across automated and semi-automated technologies, major pharmaceutical applications, and key end-user categories including pharmaceutical manufacturers, biopharmaceutical companies, and contract manufacturing organizations. It evaluates deployment trends across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, while assessing technology adoption patterns, facility modernization initiatives, and evolving sterile manufacturing requirements. More than 60% of new installations are concentrated within highly automated production environments, highlighting the industry's ongoing digital transformation.

The study further examines robotics integration, isolator technologies, AI-enabled process monitoring, machine vision inspection, and digital validation platforms. Competitive benchmarking covers leading equipment suppliers, innovation strategies, partnership activity, and manufacturing expansion programs. Strategic insights support investment prioritization, capacity planning, technology selection, geographic expansion decisions, and operational optimization initiatives. The report also evaluates emerging opportunities in biologics manufacturing, cell and gene therapy production, modular fill-finish platforms, and next-generation sterile processing ecosystems expected to influence market direction between 2026 and 2033.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 100.0 Million |

| Market Revenue (2033) | USD 129.7 Million |

| CAGR (2026–2033) | 3.3% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Syntegon; IMA Group; OPTIMA; Bausch+Ströbel; Groninger; Vanrx Pharmasystems; Cozzoli Machine Company; Watson-Marlow Fluid Technology Solutions; Steriline; Tofflon Science and Technology Group; Dara Pharmaceutical Packaging; AST Inc. |

| Customization & Pricing | Available on Request (10% Customization Free) |