Reports

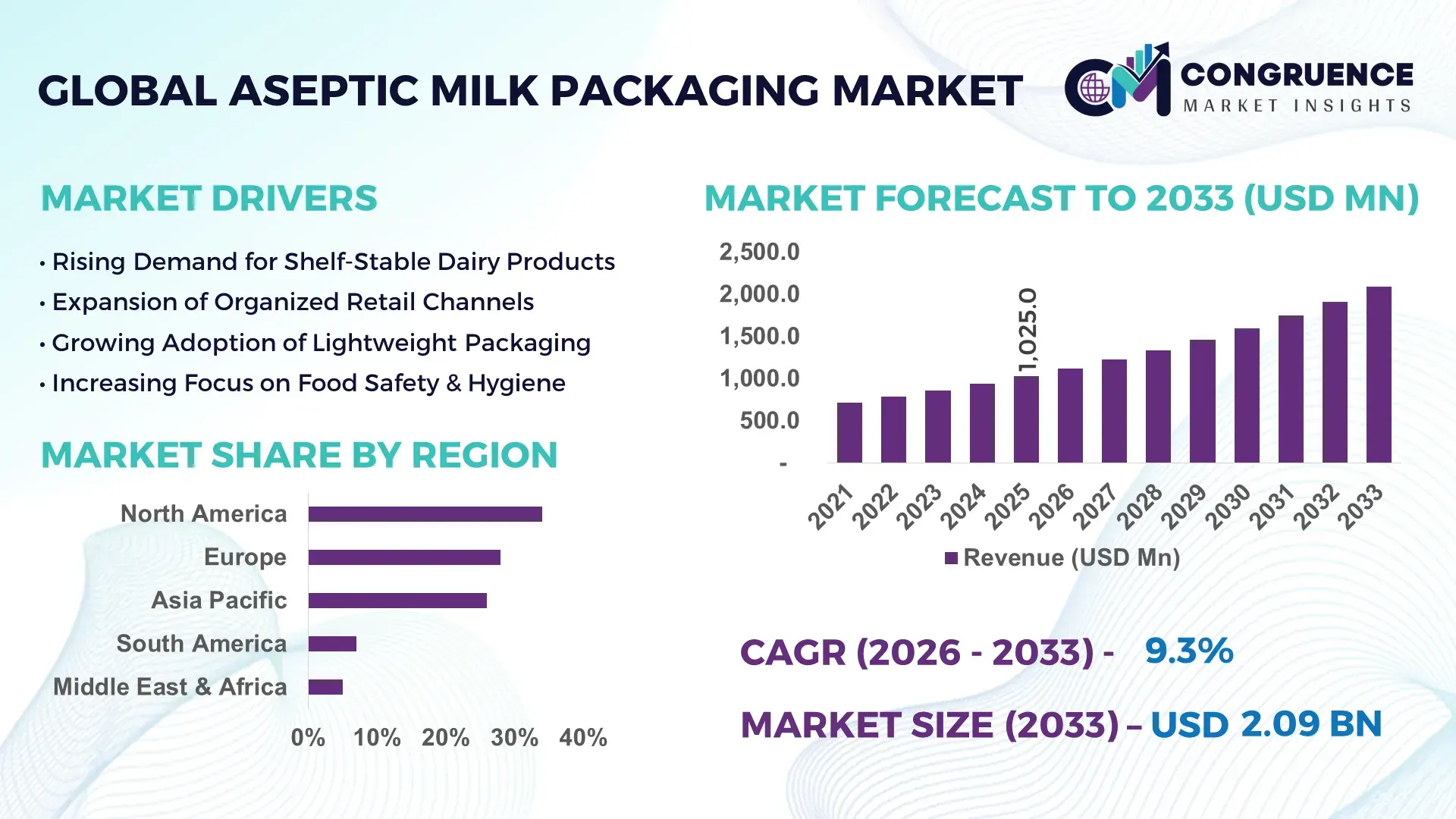

The Global Aseptic Milk Packaging Market was valued at USD 1,025.0 Million in 2025 and is anticipated to reach a value of USD 2,087.8 Million by 2033 expanding at a CAGR of 9.3% between 2026 and 2033, according to an analysis by Congruence Market Insights. The market growth is primarily driven by increasing demand for extended shelf-life dairy products, rising urban consumption, and growing adoption of carton-based aseptic solutions in emerging economies.

The United States represents the dominant country in the Aseptic Milk Packaging Market, supported by high dairy production volumes exceeding 102 billion pounds of milk annually and advanced packaging automation infrastructure. Over 65% of large-scale dairy processors in the U.S. utilize aseptic carton or PET-based systems for long shelf-life milk variants. Capital investments in automated filling lines have increased by approximately 18% over the last three years, with robotics-enabled aseptic filling improving operational efficiency by nearly 22%. Additionally, shelf-stable milk penetration in institutional supply chains (schools, military, emergency food programs) accounts for over 30% of total aseptic milk consumption.

Market Size & Growth: USD 1,025.0 Million in 2025, projected to reach USD 2,087.8 Million by 2033 at 9.3% CAGR, driven by 40% higher shelf-life efficiency compared to conventional packaging.

Top Growth Drivers: 48% growth in shelf-stable dairy demand, 35% increase in urban on-the-go consumption, 28% improvement in cold-chain cost efficiency.

Short-Term Forecast: By 2028, automated aseptic filling lines are expected to reduce packaging waste by 20% and improve throughput efficiency by 18%.

Emerging Technologies: AI-enabled quality inspection, recyclable multi-layer barrier films, and high-speed robotic aseptic filling systems.

Regional Leaders: North America projected at USD 640 Million by 2033 with institutional demand strength; Europe at USD 520 Million with 60% recyclable carton penetration; Asia-Pacific at USD 710 Million driven by 45% growth in urban dairy consumption.

Consumer/End-User Trends: Over 55% of urban consumers prefer shelf-stable milk for convenience; institutional buyers account for nearly 30% of bulk procurement.

Pilot or Case Example: In 2024, a U.S.-based dairy processor achieved 23% downtime reduction after deploying AI-powered aseptic inspection systems.

Competitive Landscape: Tetra Pak holds approximately 32% share, followed by SIG Combibloc, Elopak, Amcor, and Sealed Air.

Regulatory & ESG Impact: 70% of manufacturers are transitioning toward recyclable cartons aligned with 2030 plastic reduction targets.

Investment & Funding Patterns: Over USD 450 Million invested globally in aseptic filling line upgrades during 2023–2025, emphasizing automation and sustainability.

Innovation & Future Outlook: Bio-based polymer barriers and digital traceability integration are expected to enhance packaging recyclability by 35% by 2030.

Foodservice and retail sectors contribute over 60% of total aseptic milk packaging demand, while institutional procurement accounts for nearly 30%. Carton-based solutions represent approximately 68% of packaging formats due to lightweight and recyclability advantages. Adoption of bio-based polyethylene layers has increased by 25% in the past three years. Regulatory pressure for 50% recyclable content by 2030 in several developed economies is accelerating innovation in barrier coatings and mono-material structures.

The Aseptic Milk Packaging Market holds strategic relevance within the global dairy value chain by enabling shelf-stable distribution models, reducing cold-chain dependence, and expanding rural-to-urban supply networks. With nearly 40% of global milk output processed into long-life or value-added dairy products, aseptic systems are becoming integral to operational efficiency. Advanced aseptic carton filling delivers up to 30% reduction in logistics costs compared to refrigerated distribution models, positioning it as a resilience tool amid energy price volatility.

Technological benchmarking indicates that AI-powered visual inspection systems deliver 25% defect detection improvement compared to traditional manual inspection standards. North America dominates in production volume, while Asia-Pacific leads in adoption with nearly 45% of urban dairy enterprises integrating automated aseptic filling technologies. By 2028, smart packaging integration with QR-based traceability is expected to improve supply chain transparency metrics by 20%.

From an ESG perspective, firms are committing to packaging sustainability improvements such as 50% recycled content integration by 2030. In 2024, a leading U.S. dairy processor achieved a 21% material reduction through lightweight aseptic carton redesign supported by digital twin simulation. Looking ahead, the Aseptic Milk Packaging Market will remain a pillar of resilience, regulatory compliance, and sustainable growth as dairy processors prioritize shelf stability, cost optimization, and environmental stewardship.

The Aseptic Milk Packaging Market dynamics are shaped by evolving dairy consumption patterns, sustainability mandates, automation trends, and distribution modernization. Increasing preference for long shelf-life milk products in urban centers has driven carton-based aseptic packaging penetration beyond 60% in developed markets. Meanwhile, emerging economies are investing heavily in non-refrigerated dairy logistics to overcome infrastructure constraints. Automation in aseptic filling lines has improved production throughput by approximately 20%, while digital quality inspection tools have reduced contamination risks by nearly 30%. Environmental regulations targeting plastic waste reduction are encouraging a shift toward recyclable multilayer cartons and bio-based polymers. Additionally, institutional demand from education, defense, and disaster-relief supply chains provides consistent bulk procurement volumes. Competitive intensity remains high as manufacturers compete on sustainability, material efficiency, and line speed optimization.

Rising urbanization and changing consumption habits have significantly increased demand for shelf-stable milk variants. Over 55% of urban households in developed markets purchase long-life milk at least once per month, reflecting strong preference for convenience and reduced refrigeration dependency. Aseptic packaging enables milk shelf life of up to 6–9 months without preservatives, supporting retail distribution efficiency. Institutional programs, including school nutrition schemes, account for nearly 30% of bulk aseptic milk procurement due to extended storage capabilities. Additionally, transportation cost savings of up to 25% compared to chilled supply chains strengthen economic incentives for processors adopting aseptic formats.

Aseptic filling and sterilization lines require significant upfront capital expenditure, often exceeding USD 8–12 million per high-speed production line. Installation complexity, cleanroom requirements, and skilled labor training increase operational costs. Smaller dairy processors face barriers due to limited financing access, resulting in lower adoption rates in rural regions. Maintenance costs for advanced robotic filling systems can account for nearly 15% of annual operational budgets. Furthermore, multilayer packaging materials pose recycling challenges, limiting adoption in regions with underdeveloped waste management infrastructure.

Emerging economies in Asia and Africa are witnessing dairy consumption growth exceeding 6% annually, creating demand for shelf-stable milk products in regions with limited cold-chain infrastructure. Urban middle-class expansion has increased packaged milk consumption by nearly 40% over the past decade. Government-backed school nutrition initiatives in developing countries are expanding institutional milk distribution programs by approximately 18% annually. Technological innovation in lightweight bio-based cartons presents an opportunity to reduce material usage by 20%, supporting both cost efficiency and sustainability objectives.

Fluctuations in polymer resin and aluminum foil prices directly impact multilayer aseptic carton production costs. Raw material price variations have reached 15–20% annually in recent years, affecting procurement planning. Supply chain disruptions and geopolitical tensions further complicate sourcing of barrier materials. Additionally, compliance with increasingly stringent packaging waste directives requires redesign investments, adding to operational burdens. Recycling infrastructure gaps in emerging markets limit the circular economy potential of multilayer cartons, creating reputational and regulatory risks for manufacturers.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Aseptic Milk Packaging Market. Approximately 55% of newly installed aseptic production facilities report cost benefits through prefabricated processing units. Pre-assembled sterile modules reduce installation timelines by nearly 30% and lower on-site labor requirements by 25%. Europe and North America are leading adopters, where automated prefabrication improves facility commissioning speed by 20%.

Growth in Bio-Based and Recyclable Materials: Around 70% of leading dairy processors have integrated recyclable carton layers, while bio-based polyethylene usage has grown by 25% since 2022. Lightweight material innovation has reduced average package weight by 18%, lowering carbon emissions during transport by approximately 12%.

Automation and AI-Driven Quality Control: AI-enabled inspection systems improve contamination detection rates by 28% and reduce product recalls by nearly 15%. Robotic filling lines now operate at speeds exceeding 24,000 packs per hour, improving throughput efficiency by 22%.

Expansion of Shelf-Stable Dairy in Emerging Markets: Urban dairy consumption in Asia-Pacific has increased by 45% over five years, with nearly 50% of new milk launches introduced in aseptic formats. Institutional demand growth of 18% annually supports long-term packaging expansion.

The Aseptic Milk Packaging Market is segmented by type, application, and end-user, each reflecting distinct operational priorities and investment patterns. From a type perspective, carton-based multilayer packaging remains dominant due to its barrier efficiency, lightweight structure, and recyclability compliance. Bottle-based aseptic formats are gaining traction in premium and flavored milk categories, while pouch and bag-in-box systems serve institutional and bulk distribution channels. By application, liquid white milk accounts for the largest utilization share, followed by flavored milk and fortified dairy beverages. Increasing diversification into lactose-free and protein-enriched variants is influencing packaging customization requirements. From an end-user standpoint, dairy processing companies represent the core demand base, while foodservice operators and institutional procurement programs significantly contribute to bulk adoption. Retail chains increasingly prioritize shelf-stable SKUs, with over 50% of supermarket long-life milk inventory now relying on aseptic packaging formats. This segmentation underscores a shift toward efficiency-driven, sustainability-aligned, and automation-supported packaging strategies across the dairy value chain.

Carton-based aseptic packaging currently accounts for approximately 68% of total adoption, owing to its multi-layer barrier technology that combines paperboard, polyethylene, and aluminum layers to extend shelf life up to 9 months without refrigeration. Bottle-based aseptic packaging holds nearly 20%, primarily used for premium, organic, and flavored milk variants where transparency and brand visibility influence purchasing behavior. However, adoption in aseptic PET bottles is rising fastest, projected to grow at approximately 11.5% annually through 2033, supported by improved oxygen barrier coatings and lightweight resin technologies. Pouch and bag-in-box systems collectively contribute around 12% of the market, mainly serving institutional catering, school milk programs, and HoReCa bulk supply chains. These formats offer up to 25% logistics efficiency improvement in large-volume distribution. Technological improvements in carton sterilization and high-speed filling (exceeding 24,000 packs per hour) reinforce carton leadership, while recyclable mono-material bottle innovations accelerate PET-based growth.

In 2024, the U.S. Department of Agriculture reported that over 70% of federally supported school milk programs distributed shelf-stable milk in aseptic carton formats, enhancing storage flexibility and reducing spoilage in non-refrigerated facilities.

Liquid white milk represents the leading application, accounting for nearly 60% of aseptic packaging utilization due to its consistent household consumption and institutional procurement demand. Flavored milk variants hold approximately 25%, driven by rising youth consumption and product diversification strategies. However, fortified and functional dairy beverages are expanding fastest, projected to grow at about 12.2% annually through 2033, supported by increasing consumer demand for protein-enriched and lactose-free formulations. Retail distribution dominates application channels, with more than 55% of shelf-stable dairy SKUs positioned in supermarket chains. Institutional and school nutrition programs account for nearly 20%, leveraging extended shelf-life benefits. In 2025, approximately 42% of dairy processors globally reported expanding their flavored and functional milk portfolios in aseptic formats to meet evolving consumer preferences. Additionally, nearly 48% of urban consumers indicate preference for shelf-stable milk due to convenience and reduced refrigeration dependency.

In 2024, the Food and Agriculture Organization noted expanded deployment of shelf-stable milk solutions across over 30 national school feeding programs, improving dairy access in temperature-sensitive regions.

Dairy processing companies constitute the leading end-user segment, representing approximately 65% of total aseptic milk packaging adoption, supported by vertically integrated production and automated filling infrastructure. Large-scale processors have increased investment in robotic aseptic filling lines by nearly 18% over the past three years to improve throughput and contamination control. Foodservice and HoReCa operators account for around 20%, utilizing bulk aseptic formats to reduce cold storage costs by up to 25%. However, institutional procurement programs—including education and defense sectors—are the fastest-growing end-user group, expanding at approximately 10.8% annually through 2033 due to non-refrigerated distribution advantages. Retail chains collectively contribute about 15%, prioritizing long shelf-life SKUs to optimize inventory turnover. In 2025, nearly 50% of large supermarket chains reported increasing shelf allocation for aseptic dairy products. Additionally, around 46% of dairy enterprises globally indicated upgrading packaging lines to meet sustainability compliance targets.

In 2024, the U.S. Department of Defense expanded procurement of shelf-stable dairy products for overseas logistics operations, reporting a 19% reduction in cold-chain transport dependency through aseptic packaging adoption.

North America accounted for the largest market share at 34% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 10.8% between 2026 and 2033.

North America’s leadership is supported by annual milk production exceeding 110 billion pounds and over 65% penetration of aseptic cartons in institutional dairy supply chains. Europe follows with approximately 28% market share, driven by strong sustainability mandates and more than 60% recyclable carton usage in dairy packaging. Asia-Pacific holds nearly 26% share, fueled by rising urban dairy consumption that has increased by over 45% in the past five years. South America contributes around 7%, supported by export-oriented dairy processing in Brazil and Argentina, while the Middle East & Africa collectively account for 5%, with shelf-stable milk imports representing over 35% of packaged dairy sales in Gulf countries. Regional infrastructure modernization, automation penetration exceeding 50% in developed markets, and government-backed nutrition programs across 40+ countries continue shaping competitive positioning.

North America holds approximately 34% share of the global Aseptic Milk Packaging Market, driven by large-scale dairy processing industries and institutional demand. The United States and Canada together process over 115 billion pounds of milk annually, with nearly 60% of long-life milk distributed in aseptic carton formats. Regulatory frameworks promoting food safety modernization and sustainable packaging targets—such as 50% recyclable content goals by 2030—are accelerating material innovation. Automation penetration in aseptic filling lines exceeds 55%, with robotic inspection systems improving defect detection by 25%. Digital traceability adoption across dairy supply chains has expanded by nearly 30% over the past three years. A key industry participant, Tetra Pak’s U.S. operations, has expanded high-speed filling solutions capable of exceeding 24,000 packs per hour to meet institutional demand. Regional consumer behavior reflects preference for bulk retail purchasing, with over 52% of households buying shelf-stable milk for emergency storage and convenience.

Europe represents roughly 28% of the Aseptic Milk Packaging Market, led by Germany, France, and the United Kingdom. Germany alone processes over 33 million metric tons of milk annually, with more than 65% of long-life milk packaged in recyclable carton formats. Stringent circular economy directives require 50–55% recycling rates for packaging materials by 2030, influencing design innovation in mono-material barriers. Emerging technologies such as bio-based polyethylene layers have seen adoption growth of 25% since 2022. Smart labeling and QR-enabled traceability systems are integrated into nearly 35% of new aseptic product launches. SIG Combibloc has expanded recyclable carton solutions across Central Europe, reducing material weight by 18% while maintaining barrier integrity. Consumer behavior in this region strongly favors environmentally compliant products, with over 60% of shoppers indicating preference for recyclable packaging in dairy purchases.

Asia-Pacific accounts for nearly 26% of the global Aseptic Milk Packaging Market and ranks as the fastest-growing region. China, India, and Japan are the top consuming countries, collectively representing over 70% of regional packaged milk demand. Urban dairy consumption has increased by approximately 45% over five years, with shelf-stable milk penetration exceeding 50% in metropolitan areas. Manufacturing capacity expansion in China and India has led to over 20 new aseptic filling facilities commissioned since 2022. Automation integration in advanced plants has improved throughput efficiency by 22%. Innovation hubs in Shanghai and Mumbai are piloting lightweight carton solutions reducing packaging material use by 15%. Yili Group in China has expanded aseptic packaging capacity to serve both domestic and export markets. Regional consumers show high adoption of e-commerce grocery platforms, with nearly 38% of urban households purchasing long-life milk online.

South America contributes around 7% to the global Aseptic Milk Packaging Market, led by Brazil and Argentina. Brazil produces over 34 billion liters of milk annually, with approximately 40% processed into long-life formats for domestic and export markets. Infrastructure improvements in cold-chain alternatives have increased aseptic adoption by 18% over the past three years. Government trade agreements facilitating dairy exports to over 50 countries support packaging standardization. Energy cost volatility has encouraged processors to shift toward shelf-stable solutions that reduce refrigeration dependency by up to 30%. Tetra Pak’s operations in Brazil have expanded high-speed carton filling lines to serve regional dairy exporters. Consumers increasingly prefer affordable, long-life milk, with nearly 47% of packaged milk sales in urban supermarkets comprising aseptic formats.

The Middle East & Africa region accounts for approximately 5% of the global Aseptic Milk Packaging Market, with demand concentrated in the UAE, Saudi Arabia, and South Africa. In Gulf countries, over 35% of packaged milk consumption relies on imported or reconstituted dairy products, favoring aseptic formats due to extended shelf stability in high-temperature climates. Technological modernization in UAE-based dairy plants has improved packaging line efficiency by nearly 20%. Regional trade partnerships within the Gulf Cooperation Council support duty-free dairy imports and packaging material sourcing. Almarai has expanded aseptic carton production capacity to serve both local and export demand. Consumer purchasing behavior emphasizes bulk buying and long storage capability, with nearly 50% of households opting for shelf-stable milk to mitigate supply chain disruptions.

United States – 29% Market Share: It is driven by over 100 billion pounds of annual milk production and high automation penetration in dairy processing facilities.

China – 21% Market Share: It is supported by rapid urban dairy consumption growth exceeding 40% over five years and large-scale expansion of automated aseptic filling infrastructure.

The Aseptic Milk Packaging Market exhibits a moderately consolidated structure, with the top five companies collectively accounting for approximately 68% of global market share. The competitive landscape includes over 35 active international and regional players specializing in carton systems, PET bottle solutions, multilayer barrier materials, and high-speed aseptic filling equipment. Market leaders compete primarily on technological capability, sustainability performance, production line speed, and global service network coverage.

Tetra Pak, SIG Group, Elopak, Amcor, and Sealed Air dominate through vertically integrated offerings that combine packaging materials, filling machinery, and lifecycle service contracts. High-speed filling lines exceeding 24,000 packs per hour and AI-enabled inspection systems delivering up to 28% defect reduction have become key competitive differentiators. Strategic initiatives include long-term dairy processor partnerships, recyclable mono-material launches, and capacity expansions in Asia-Pacific and Latin America.

Sustainability is a major competitive driver, with nearly 70% of leading players committing to 50% recycled or renewable material integration by 2030. Over the past two years, at least 12 new product launches have focused on bio-based polymers and lightweight carton structures reducing packaging weight by 15–20%. Mergers and joint ventures in emerging markets have increased regional manufacturing footprints by nearly 18%, intensifying competition for institutional and export-oriented dairy contracts.

Amcor

Sealed Air

Mondi Group

DS Smith

Stora Enso

UFlex Limited

Greatview Aseptic Packaging

IPI S.r.l.

Billerud

Ecolean

Refresco

Technological advancement in the Aseptic Milk Packaging Market is centered on sterilization efficiency, barrier enhancement, automation integration, and sustainable material innovation. Modern aseptic systems use ultra-high temperature (UHT) processing at 135–150°C for 2–5 seconds, eliminating microbial contamination while preserving nutritional value. Advanced hydrogen peroxide sterilization and sterile air filtration systems now achieve up to 99.999% microbial reduction rates.

Automation integration exceeds 55% in developed markets, with robotic arms and AI-driven vision systems improving inspection accuracy by 25–30%. High-speed filling systems operate at more than 24,000 cartons per hour, increasing production throughput by 20% compared to legacy lines. Digital twin simulations reduce commissioning time by nearly 18% and optimize material usage by 12%.

Barrier technology innovation includes aluminum-layer reduction by 15% while maintaining oxygen transmission rates below 0.1 cc/m²/day. Bio-based polyethylene derived from sugarcane now accounts for approximately 25% of renewable material usage in premium cartons. Smart packaging technologies, including QR-enabled traceability and NFC tags, are embedded in nearly 35% of new product launches to enhance supply chain transparency. Additionally, mono-material PET bottles with enhanced oxygen scavengers improve shelf life by up to 20%, supporting premium dairy expansion. These technologies collectively enhance operational efficiency, compliance readiness, and sustainability positioning for dairy processors globally.

• In February 2025, Tetra Pak International S.A. introduced aseptic packaging material with 5% certified recycled polymers for use in India, making it the first company in the food and beverage packaging industry there to comply with new regulatory recycled content mandates and enhance material circularity. Source: www.business-standard.com

• In December 2025, Tetra Pak launched the world’s first paper-based barrier technology for aseptic cartons with García Carrión, debuting the Tetra Brik® Aseptic 200 ml Slim Leaf carton made with up to 80% paper and achieving 92% renewable content, reinforcing sustainability and recyclability performance. Source: www.tetralaval.com

• In February 2026, Tetra Pak expanded its paper-based barrier technology to high-speed aseptic filling lines in Asia, with Maeil Dairies in South Korea becoming the first producer to adopt this at industrial scale, achieving 87% renewable content and a 26% reduction in package carbon footprint on soy milk lines. Source: www.news.europawire.eu

• In December 2025, SIG Group AG announced that its first aseptic carton plant in India (Ahmedabad, Gujarat) is fully operational, enhancing regional production capacity for aseptic cartons to meet growing dairy and beverage market demand. Source: www.sig.biz

The Aseptic Milk Packaging Market Report provides comprehensive coverage across packaging types, applications, end-users, technologies, and regional markets. The scope includes carton-based, PET bottle, pouch, and bag-in-box systems, collectively representing 100% of shelf-stable dairy packaging formats. It analyzes liquid white milk, flavored milk, lactose-free, and fortified dairy beverages, which together account for over 90% of aseptic milk consumption globally.

Geographic coverage spans North America (34% share), Europe (28%), Asia-Pacific (26%), South America (7%), and Middle East & Africa (5%), incorporating country-level insights for major dairy-producing and importing nations. The report evaluates technological frameworks such as UHT sterilization, hydrogen peroxide-based aseptic filling, AI-driven inspection systems, and recyclable barrier material innovations, reflecting automation penetration levels exceeding 50% in developed economies.

Industry focus areas include sustainability compliance targets (50% recyclable content benchmarks), institutional procurement programs covering more than 40 countries, and digital traceability integration adopted in 35% of new product launches. The report further assesses competitive positioning among over 35 global and regional players, innovation pipelines, material efficiency strategies, and regulatory impacts shaping packaging modernization. It delivers actionable insights for dairy processors, packaging manufacturers, institutional buyers, and investors evaluating long-term resilience and supply chain optimization within the Aseptic Milk Packaging Market.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 1,025.0 Million |

| Market Revenue (2033) | USD 2,087.8 Million |

| CAGR (2026–2033) | 9.3% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Tetra Pak; SIG Group; Elopak; Amcor; Sealed Air; Mondi Group; DS Smith; Stora Enso; UFlex Limited; Greatview Aseptic Packaging; IPI S.r.l.; Billerud; Ecolean; Refresco |

| Customization & Pricing | Available on Request (10% Customization Free) |