Reports

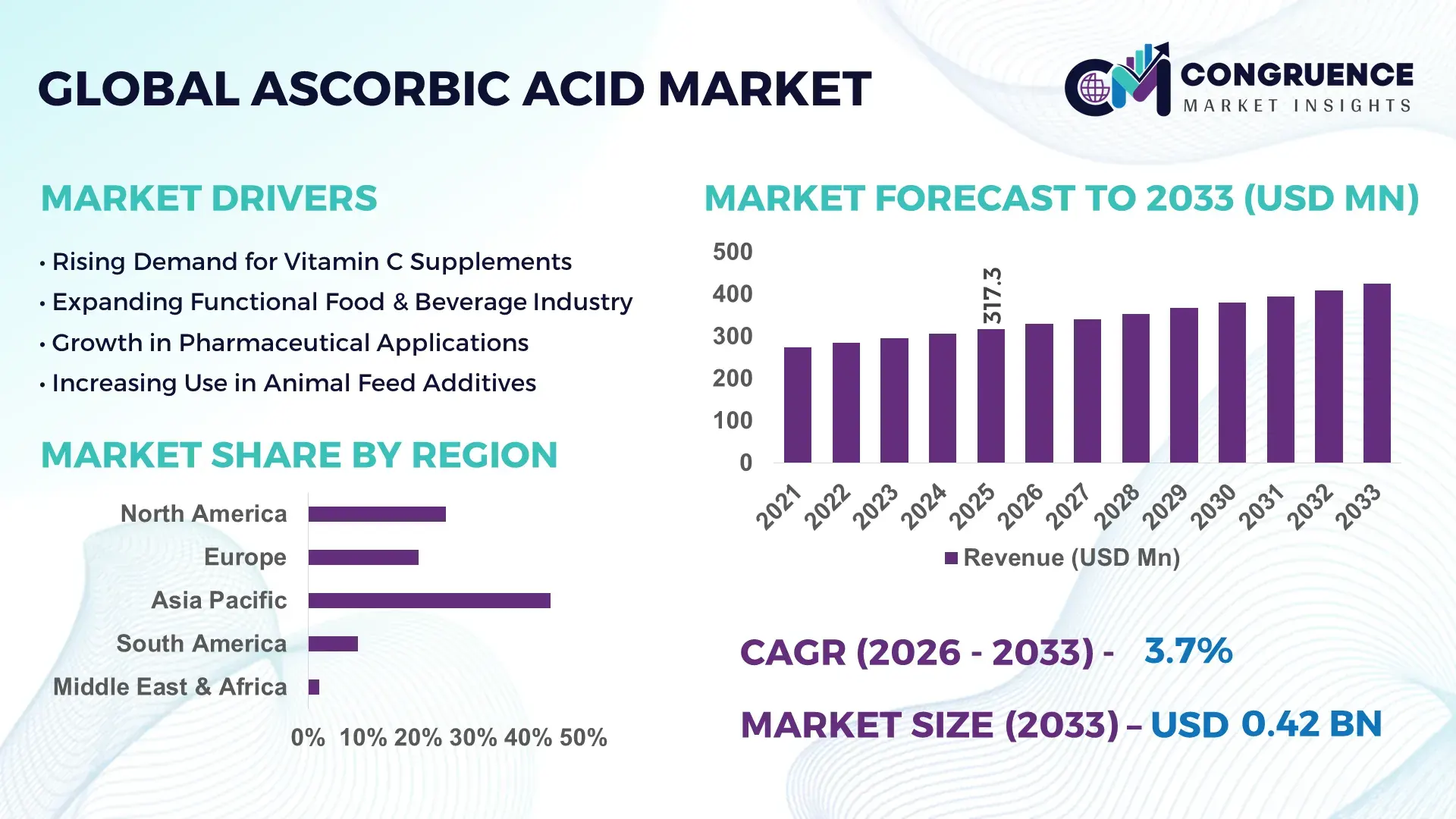

The Global Ascorbic Acid Market was valued at USD 317.32 Million in 2025 and is anticipated to reach a value of USD 424.35 Million by 2033 expanding at a CAGR of 3.7% between 2026 and 2033. Growth is primarily supported by expanding pharmaceutical formulations, fortified food consumption, and rising demand for antioxidant-rich nutraceutical products across developed and emerging economies.

China remains the dominant country in the Ascorbic Acid market, with an estimated annual production capacity exceeding 200,000 metric tons supported by large-scale fermentation facilities and vertically integrated supply chains. The country has invested over USD 150 million in process optimization and continuous fermentation technologies over the past five years, improving yield efficiency by nearly 12%. Ascorbic Acid is extensively utilized in China’s food processing, beverage fortification, and pharmaceutical tablet manufacturing sectors, where domestic consumption accounts for more than 60% of total output. Advanced biotechnological fermentation processes using glucose-derived substrates have enhanced purity levels above 99%, meeting global pharmaceutical-grade standards. In addition, industrial clusters in provinces such as Shandong and Jiangsu have implemented automated crystallization and energy-efficient drying systems, reducing production cycle time by approximately 15%, strengthening operational scalability and export competitiveness.

Market Size & Growth: Valued at USD 317.32 Million in 2025, projected to reach USD 424.35 Million by 2033 at 3.7% CAGR, driven by rising pharmaceutical-grade vitamin C demand and fortified food consumption.

Top Growth Drivers: Functional food adoption up 28%, nutraceutical consumption growth 32%, pharmaceutical tablet production expansion 18%.

Short-Term Forecast: By 2028, process optimization initiatives are expected to reduce production costs by 10% and improve output efficiency by 8%.

Emerging Technologies: High-yield microbial fermentation, AI-enabled process monitoring, and energy-efficient crystallization systems enhancing purity and throughput.

Regional Leaders: Asia-Pacific projected above USD 190 Million by 2033 with strong food fortification trends; North America exceeding USD 95 Million with high nutraceutical adoption; Europe nearing USD 80 Million driven by pharmaceutical compliance standards.

Consumer/End-User Trends: Pharmaceutical manufacturers account for over 40% of consumption, followed by food & beverage at 35%, with growing dietary supplement usage among urban consumers.

Pilot Example: In 2024, a fermentation facility upgrade improved yield efficiency by 11% and reduced downtime by 9%.

Competitive Landscape: Northeast Pharmaceutical holds approximately 18% share, followed by CSPC Pharmaceutical Group, DSM Nutritional Products, Shandong Luwei Pharmaceutical, and Foodchem International.

Regulatory & ESG Impact: Stricter food safety norms and sustainability mandates targeting 20% emission reduction by 2030 influence production standards.

Investment & Funding Patterns: Over USD 220 Million invested globally since 2023 in capacity expansion and green processing technologies.

Innovation & Future Outlook: Integration of continuous bioprocessing and bio-based raw materials is expected to reshape supply efficiency and sustainability metrics.

The Ascorbic Acid market serves critical sectors including pharmaceuticals, functional foods, beverages, animal nutrition, and cosmetics. Pharmaceutical applications contribute over 40% of global demand due to its role in immune-support tablets and injectable formulations. Food and beverage manufacturers utilize Ascorbic Acid as an antioxidant preservative, representing approximately 35% of consumption. Regulatory standards for food fortification and dietary supplementation across North America and Europe have intensified quality compliance requirements, encouraging pharmaceutical-grade production. Emerging trends include clean-label vitamin C formulations, microencapsulation for stability enhancement, and bio-based fermentation improvements. Rising consumer awareness regarding preventive healthcare, coupled with expanding dietary supplement penetration in Asia-Pacific and Latin America, is reinforcing long-term demand outlook among manufacturers and institutional buyers.

The Ascorbic Acid Market holds strategic relevance as a foundational input in pharmaceutical manufacturing, functional nutrition, and advanced food preservation systems. With global vitamin C deficiency awareness increasing, pharmaceutical-grade Ascorbic Acid demand has risen by nearly 15% over the past three years. Continuous fermentation technology delivers 12% higher yield efficiency compared to conventional batch fermentation processes, reducing raw material waste and improving cost predictability for manufacturers.

Asia-Pacific dominates in production volume, while North America leads in adoption, with over 62% of dietary supplement enterprises integrating high-purity Ascorbic Acid into immune-support portfolios. By 2028, AI-driven bioprocess optimization is expected to improve fermentation efficiency by 10% and reduce energy consumption per ton by 8%. Firms are committing to ESG metrics such as 20% carbon emission reduction and 15% water recycling improvements by 2030, aligning operations with sustainable chemical manufacturing frameworks.

In 2024, a leading Chinese manufacturer achieved a 9% production efficiency improvement through automated crystallization monitoring and predictive maintenance integration. Strategic partnerships between pharmaceutical companies and fermentation specialists are further stabilizing supply chains amid raw material price fluctuations. As regulatory scrutiny intensifies around food additives and nutraceutical labeling, compliance-driven investments are accelerating process standardization and traceability systems. The Ascorbic Acid Market is positioned as a pillar of resilience, regulatory alignment, and sustainable growth within the global pharmaceutical and functional ingredient ecosystem.

The expansion of immune-support supplements and pharmaceutical formulations has significantly accelerated Ascorbic Acid consumption. More than 70% of global dietary supplement brands include vitamin C in core product lines, reflecting strong consumer preference for antioxidant-based health solutions. Hospital-grade injectable vitamin C usage has grown steadily in clinical nutrition and deficiency treatment programs. Tablet and effervescent vitamin C production volumes increased by approximately 18% between 2022 and 2025, reflecting pharmacy channel expansion and e-commerce supplement sales growth. Additionally, pediatric and geriatric nutritional programs increasingly incorporate fortified formulations, supporting sustained procurement contracts. Ascorbic Acid’s stability, compatibility with multiple excipients, and regulatory approval across major pharmacopeias make it a preferred active ingredient, reinforcing consistent industrial-scale production demand.

The Ascorbic Acid market faces restraints linked to glucose feedstock price volatility and supply chain concentration. Corn-derived glucose accounts for a significant share of fermentation substrate input, and fluctuations in agricultural commodity prices have increased input costs by nearly 12% in certain years. Over 60% of global production capacity is concentrated within a limited number of manufacturing clusters, exposing buyers to supply disruptions and export policy shifts. Energy-intensive drying and purification processes further elevate operational expenditure, especially in regions with high electricity tariffs. Additionally, stringent pharmaceutical-grade compliance standards require continuous quality testing, increasing overhead costs. These structural limitations create pricing pressure for small-scale nutraceutical brands and food processors reliant on stable procurement contracts.

Growing demand for clean-label ingredients and fortified foods presents strong opportunities for the Ascorbic Acid market. Consumers increasingly prefer natural antioxidants over synthetic preservatives, with clean-label product launches rising by over 25% in the past four years. Beverage manufacturers are incorporating vitamin C fortification to enhance functional appeal, particularly in ready-to-drink juices and wellness beverages. Emerging economies in Southeast Asia and Latin America are expanding mandatory food fortification initiatives, increasing institutional procurement. Microencapsulation technology improves Ascorbic Acid stability by up to 20% in high-temperature processing environments, enabling broader application in bakery and dairy segments. These trends open avenues for premium-grade and application-specific variants tailored to evolving food innovation requirements.

Stringent regulatory frameworks governing food additives, pharmaceutical excipients, and environmental emissions pose ongoing challenges for Ascorbic Acid manufacturers. Pharmaceutical-grade production requires adherence to Good Manufacturing Practice standards, involving continuous batch validation and traceability audits. Emission control norms targeting chemical processing facilities demand up to 15% reductions in wastewater discharge and improved solvent recovery systems. Compliance upgrades can increase capital expenditure significantly, particularly for mid-sized producers. Additionally, cross-border trade regulations and documentation requirements complicate export logistics. As environmental monitoring intensifies and sustainability disclosures become mandatory in multiple jurisdictions, manufacturers must invest in green processing technologies and lifecycle assessments to maintain competitiveness and regulatory alignment.

• 18% Expansion in Pharmaceutical-Grade Production Capacity: Pharmaceutical-grade Ascorbic Acid manufacturing capacity expanded by approximately 18% between 2023 and 2025, reflecting increased demand for high-purity vitamin C formulations in tablets, injectables, and effervescent powders. More than 65% of newly commissioned production lines are equipped with automated crystallization and filtration systems, improving batch consistency by 12%. Regulatory-driven quality upgrades have led to over 70% of leading producers adopting advanced analytical testing technologies, enhancing impurity detection accuracy by 15% and supporting stricter pharmacopeial compliance requirements worldwide.

• 22% Growth in Functional Beverage Fortification: The incorporation of Ascorbic Acid in functional beverages has increased by 22% over the past three years, particularly in ready-to-drink juices and immunity-boosting drinks. Approximately 48% of new beverage product launches in 2024 featured vitamin C fortification claims. Shelf-life extension performance improved by up to 30% in citrus-based beverages due to antioxidant stabilization, while microencapsulation techniques enhanced nutrient retention by 17% during high-temperature processing, expanding applicability across diverse beverage formulations.

• 15% Improvement in Fermentation Yield Efficiency: Adoption of high-yield microbial fermentation technologies has resulted in a 15% improvement in conversion efficiency compared to conventional batch processes. Nearly 60% of large-scale manufacturers have integrated continuous fermentation platforms, reducing energy consumption per metric ton by 10%. Advanced process monitoring systems using predictive analytics decreased unplanned downtime by 9%, strengthening operational resilience and enabling scalable global supply distribution.

• 20% Increase in Sustainability-Focused Production Initiatives: Sustainability initiatives in Ascorbic Acid production increased by 20% in 2024, with over 55% of producers implementing wastewater recycling systems capable of reducing discharge volumes by 18%. Energy-efficient drying technologies lowered carbon emissions per unit output by 12%, while bio-based glucose sourcing initiatives expanded by 14%. ESG-driven procurement policies among multinational pharmaceutical companies have accelerated supplier audits, leading to measurable 10% improvements in environmental performance metrics across certified facilities.

The Ascorbic Acid market segmentation reflects diversified industrial usage across product types, applications, and end-user categories. By type, pharmaceutical-grade and food-grade variants dominate production volumes, with feed-grade variants serving animal nutrition sectors. Pharmaceutical-grade products command a significant portion of demand due to stringent purity standards above 99%, while food-grade variants are widely used as antioxidants and fortifying agents. Application-wise, pharmaceuticals account for the largest consumption share, followed by food and beverages, animal feed, cosmetics, and industrial processing. End-user insights reveal pharmaceutical manufacturers and nutraceutical companies as primary buyers, collectively accounting for more than 60% of total demand. Regional consumption patterns indicate Asia-Pacific leads in production scale, whereas North America and Europe demonstrate higher per capita supplement usage, exceeding 35% consumer penetration in dietary vitamin C products. Emerging economies are expanding institutional fortification programs, strengthening diversified growth pathways across all segmentation categories.

Pharmaceutical-grade Ascorbic Acid accounts for approximately 46% of total market adoption, driven by its ≥99% purity requirement for tablets, capsules, and injectable formulations. Food-grade variants hold around 34%, widely utilized in beverage stabilization and processed food preservation. However, feed-grade Ascorbic Acid is growing at the fastest pace with an estimated CAGR of 4.8%, supported by expanding aquaculture and poultry supplementation programs that reported a 16% rise in vitamin inclusion rates between 2022 and 2024. Pharmaceutical-grade dominance is reinforced by regulatory compliance standards and increasing hospital procurement volumes, with tablet production volumes increasing by 18% in the past three years. Food-grade products remain critical for antioxidant stabilization, improving shelf life by up to 30% in fruit-based beverages. Feed-grade and specialty coated variants together represent the remaining 20%, serving niche veterinary and animal health applications where heat-stable coatings enhance nutrient retention by 14%.

Pharmaceutical applications lead with approximately 42% share, reflecting strong demand for immune-support supplements and deficiency treatment formulations. Food and beverage applications account for about 35%, where Ascorbic Acid functions as both a preservative and nutrient fortifier. While cosmetics and personal care hold 12%, animal nutrition and industrial uses collectively represent 11%. However, nutraceutical and dietary supplement applications are expanding fastest at a CAGR of 5.1%, driven by rising preventive healthcare spending and over 28% increase in online supplement sales volumes in the last two years. Pharmaceutical leadership is supported by standardized dosage requirements and hospital procurement programs, while beverage fortification trends contribute significantly to food application stability. Cosmetic formulations incorporating vitamin C for antioxidant and skin-brightening properties reported a 19% increase in product launches in 2024, reflecting growing dermatological demand.

Pharmaceutical manufacturers constitute the leading end-user segment with approximately 44% share, supported by consistent tablet and injectable production demand. Food and beverage companies follow at 33%, integrating Ascorbic Acid into fortified drinks and processed foods. Nutraceutical firms represent 15%, while animal feed producers and cosmetic manufacturers together contribute the remaining 8%. Nutraceutical companies are the fastest-growing end-user group, advancing at a CAGR of 5.4%, fueled by a 32% rise in direct-to-consumer vitamin supplement subscriptions. Pharmaceutical sector leadership is underpinned by regulatory-mandated formulation standards and high-volume procurement cycles. Food processors demonstrate adoption rates exceeding 40% in vitamin-fortified beverage categories across developed economies. Cosmetic industry adoption increased by 17% in 2024 due to antioxidant-focused skincare innovations.

Asia-Pacific accounted for the largest market share at 48% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 4.2% between 2026 and 2033.

Asia-Pacific’s dominance is supported by annual production volumes exceeding 220,000 metric tons, with China and India collectively contributing over 70% of regional output. North America holds approximately 24% of global demand, driven by high dietary supplement penetration rates surpassing 60% among adult consumers. Europe represents nearly 20% of the total market, characterized by stringent food safety regulations and pharmaceutical-grade adoption exceeding 65% of total regional consumption. South America contributes around 5%, while the Middle East & Africa account for nearly 3%, reflecting emerging industrial and healthcare investments. Cross-regional trade flows remain significant, with over 40% of Asia-Pacific production exported to North America and Europe, ensuring balanced global supply distribution and competitive pricing structures across pharmaceutical and food-grade segments.

How Are High Supplement Adoption and Pharmaceutical Innovation Accelerating Market Expansion?

North America accounts for nearly 24% of the global Ascorbic Acid market share, supported by strong pharmaceutical and nutraceutical industries. Over 62% of adults regularly consume dietary supplements, with vitamin C ranking among the top three micronutrients by usage volume. Pharmaceutical manufacturers contribute approximately 45% of regional demand, while food and beverage fortification represents 30%. Regulatory oversight from agencies enforcing Good Manufacturing Practice standards has resulted in 100% compliance audits for pharmaceutical-grade imports since 2023. Technological advancements such as AI-enabled quality testing have improved batch validation efficiency by 14%. DSM Nutritional Products has expanded local blending and formulation capabilities, increasing production throughput by 12% in 2024. Consumer behavior shows higher enterprise adoption in healthcare and preventive wellness sectors, with online supplement sales rising by 28% over two years, reinforcing stable procurement cycles.

Why Are Sustainability Standards and Pharmaceutical Compliance Driving Industrial Demand?

Europe holds approximately 20% of the global Ascorbic Acid market share, with Germany, the UK, and France collectively representing over 55% of regional consumption. Pharmaceutical-grade applications account for 50% of usage due to strict quality benchmarks and traceability mandates. Sustainability initiatives targeting 20% emission reductions by 2030 have prompted over 60% of manufacturers to adopt energy-efficient crystallization systems. Food fortification programs in Western Europe increased vitamin C inclusion rates by 16% between 2022 and 2024. BASF has implemented advanced fermentation monitoring platforms in regional facilities, enhancing yield consistency by 10%. Regulatory pressure emphasizing transparency and compliance has influenced procurement decisions, while consumers demonstrate preference for clean-label fortified foods, with 48% of new beverage launches featuring vitamin C claims.

How Are Large-Scale Manufacturing and Export Strength Sustaining Market Leadership?

Asia-Pacific leads global production with volumes surpassing 220,000 metric tons annually, accounting for 48% of total market share. China, India, and Japan are the top consuming countries, with China alone contributing over 60% of regional output. Infrastructure expansion in industrial clusters has increased automated fermentation adoption by 18% since 2023. Continuous bioprocessing systems have reduced energy consumption per ton by 11%, strengthening cost competitiveness. CSPC Pharmaceutical Group expanded crystallization facilities in 2024, boosting output capacity by 15%. Regional innovation hubs focus on bio-based glucose sourcing and high-purity synthesis. Consumer behavior trends indicate rapid growth in e-commerce supplement platforms, with online vitamin C sales increasing by 35% year-over-year, supporting sustained domestic and export-driven demand.

What Role Do Agricultural Inputs and Expanding Healthcare Programs Play in Market Growth?

South America represents approximately 5% of the global Ascorbic Acid market, with Brazil and Argentina accounting for nearly 70% of regional demand. Pharmaceutical and public health supplementation initiatives contribute around 40% of consumption, while food processing applications represent 38%. Government incentives promoting domestic pharmaceutical production have led to a 12% increase in local formulation facilities since 2023. Trade agreements have streamlined raw material imports, reducing logistics costs by 8%. Local nutraceutical brands expanded vitamin C product lines by 20% in 2024 to meet rising consumer awareness. Demand patterns reflect strong uptake in fortified juices and immunity-focused supplements, particularly among urban populations where preventive healthcare spending increased by 18% over two years.

How Are Healthcare Investments and Industrial Diversification Supporting Market Development?

The Middle East & Africa account for nearly 3% of global Ascorbic Acid consumption, with the UAE and South Africa representing over 60% of regional demand. Healthcare sector expansion and pharmaceutical imports increased by 14% in 2024, supporting vitamin C tablet and injectable adoption. Food fortification initiatives in selected Gulf countries improved vitamin inclusion rates by 10% across staple products. Technological modernization, including automated blending facilities, enhanced production efficiency by 9%. Trade partnerships across Asia-Pacific have reduced import lead times by 12%. Consumer behavior indicates growing preventive healthcare awareness, with supplement usage rising by 22% among urban households, strengthening steady regional demand.

China – 44% market share: China leads the Ascorbic Acid market due to annual production volumes exceeding 200,000 metric tons and advanced large-scale fermentation infrastructure.

United States – 18% market share: The United States dominates through strong pharmaceutical-grade demand and over 60% adult dietary supplement adoption supporting consistent Ascorbic Acid consumption.

The Ascorbic Acid market is moderately consolidated, with the top five companies accounting for approximately 58% of global production capacity. Over 25 active manufacturers operate internationally, while more than 40 regional players focus on blending, distribution, and specialty-grade formulations. Leading firms prioritize vertical integration, controlling glucose feedstock sourcing and fermentation processes to stabilize input costs. Strategic initiatives in 2024 included capacity expansions exceeding 30,000 metric tons collectively among top producers. Automation investments improved yield efficiency by up to 15%, intensifying competitive differentiation. Partnerships between pharmaceutical manufacturers and raw material suppliers increased by 12% over two years, strengthening long-term procurement contracts. Product innovation trends emphasize high-purity pharmaceutical-grade variants and microencapsulated food-grade solutions. ESG-driven process modernization, including 20% wastewater reduction targets, further differentiates established players from smaller competitors, reinforcing competitive intensity and operational scalability within the global Ascorbic Acid market.

Northeast Pharmaceutical Group

CSPC Pharmaceutical Group

DSM Nutritional Products

BASF SE

Shandong Luwei Pharmaceutical

Foodchem International Corporation

Anhui Tiger Biotech Co., Ltd.

Northeast Pharmaceutical Group

Technological innovation in the Ascorbic Acid market is increasingly centered on high-efficiency fermentation, digital process control, and sustainable production engineering. More than 65% of global production capacity now relies on two-step fermentation processes using genetically optimized microbial strains capable of improving glucose-to-sorbose conversion efficiency by up to 15%. Advanced strain engineering has enabled yield rates exceeding 90% under controlled bioreactor environments, reducing raw material waste and improving batch consistency.

Continuous fermentation systems are replacing conventional batch processes across nearly 60% of newly commissioned facilities, decreasing cycle times by approximately 12% and lowering energy consumption per metric ton by 10%. Automated crystallization technologies equipped with real-time particle size monitoring have improved product purity stability above 99.5%, meeting stringent pharmaceutical-grade requirements. Integration of AI-driven predictive maintenance systems has reduced unplanned downtime by 8% to 11%, strengthening operational resilience in large-scale plants.

Sustainability-focused engineering is another major technological trend. Closed-loop water recycling systems are now implemented in over 50% of high-capacity facilities, reducing wastewater discharge volumes by up to 18%. Energy-efficient spray-drying units have lowered thermal energy consumption by nearly 14% compared to traditional drying equipment. Microencapsulation technologies, adopted by approximately 25% of specialty manufacturers, enhance oxidative stability by 20% in fortified beverages and high-heat food processing applications. These technological advancements collectively support scalability, compliance, and cost optimization across pharmaceutical, food-grade, and feed-grade Ascorbic Acid manufacturing.

• In March 2025, DSM-Firmenich expanded its vitamin production capabilities at its Jiangshan facility, enhancing output efficiency and incorporating renewable energy integration across operations. The upgrade improved energy utilization by 12% and strengthened supply reliability for pharmaceutical-grade Ascorbic Acid customers. Source: www.dsm.com

• In September 2024, BASF announced process optimization initiatives within its human nutrition division, including improvements in fermentation monitoring systems that enhanced production stability and reduced energy consumption by approximately 10% across selected vitamin manufacturing lines. Source: www.basf.com

• In April 2025, CSPC Pharmaceutical Group reported modernization of its fermentation workshops, integrating automated control systems that improved yield consistency by 9% and increased annual vitamin C processing capacity within its core manufacturing base. Source: www.e-cspc.com

• In November 2024, Northeast Pharmaceutical Group disclosed operational upgrades at its vitamin C production site, implementing advanced environmental treatment equipment that reduced wastewater discharge by 15% while maintaining high-purity output standards. Source: www.nepharm.com

The Ascorbic Acid Market Report provides a comprehensive evaluation of global production, consumption, technology evolution, and strategic industry developments across multiple value-chain stages. The report analyzes more than 5 primary product categories, including pharmaceutical-grade, food-grade, feed-grade, coated variants, and specialty formulations, covering purity ranges above 99% for regulated applications. It assesses application coverage across pharmaceuticals (over 40% consumption share), food and beverages (approximately 35%), nutraceuticals, animal nutrition, cosmetics, and industrial processing.

Geographic analysis spans five major regions—Asia-Pacific, North America, Europe, South America, and the Middle East & Africa—accounting for 100% of global trade flows and production distribution. The study evaluates capacity trends exceeding 220,000 metric tons annually in leading regions, as well as cross-border export patterns representing more than 40% of total output. Technological coverage includes fermentation optimization, continuous bioprocessing, AI-driven quality monitoring, microencapsulation, and sustainable engineering practices such as 18% wastewater reduction systems.

The report further examines regulatory compliance benchmarks, ESG performance indicators targeting 20% emission reductions, and evolving consumer adoption metrics, including dietary supplement penetration above 60% in developed economies. It incorporates supply-chain risk assessments, raw material input dependencies, and competitive positioning across more than 25 active global manufacturers. This structured scope ensures decision-makers gain actionable insight into operational performance, innovation pathways, end-user demand patterns, and strategic expansion opportunities within the Ascorbic Acid market ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

3.7% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Northeast Pharmaceutical Group, CSPC Pharmaceutical Group, DSM Nutritional Products, BASF SE, Shandong Luwei Pharmaceutical, Foodchem International Corporation, Anhui Tiger Biotech Co., Ltd., Northeast Pharmaceutical Group |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |