Reports

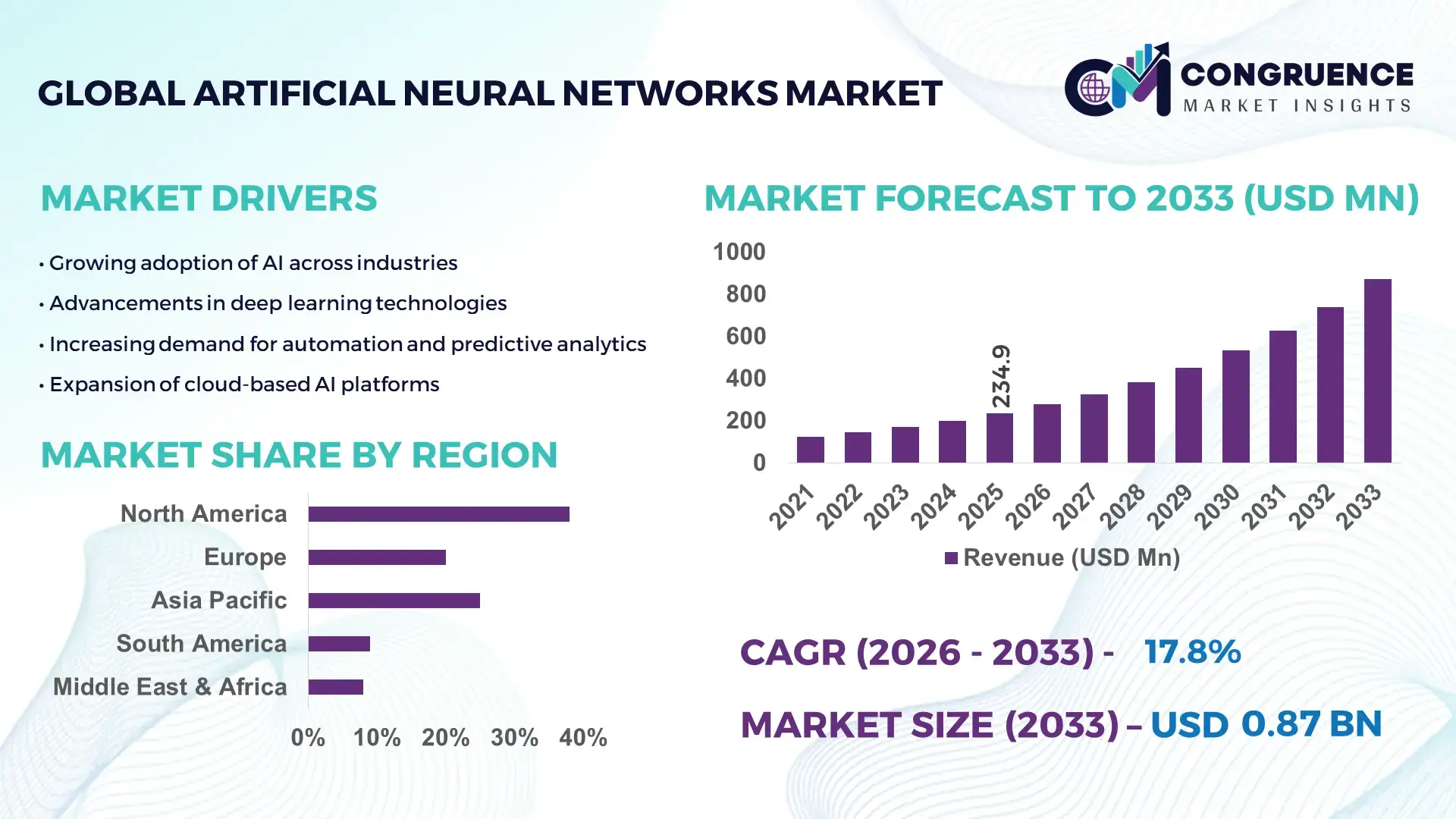

The Global Artificial Neural Networks Market was valued at USD 234.93 Million in 2025 and is anticipated to reach a value of USD 871.18 Million by 2033 expanding at a CAGR of 17.8% between 2026 and 2033. This accelerated expansion is primarily driven by rising enterprise adoption of advanced AI-driven analytics, automated decision intelligence, and scalable deep learning infrastructure across multiple high-growth industries.

The United States continues to command significant technological depth in the Artificial Neural Networks market, supported by extensive R&D expenditure exceeding USD 700 billion annually across public and private sectors. Over 65% of large enterprises in the country have deployed AI-based neural network solutions in at least one core business function, particularly in financial services, healthcare diagnostics, cybersecurity, and autonomous mobility. More than 40% of global AI startups are headquartered in the U.S., reflecting strong innovation density and venture capital inflows exceeding USD 60 billion in AI-focused investments in recent years. High-performance computing infrastructure, hyperscale cloud deployments, and widespread enterprise digital transformation initiatives have enabled scalable neural network training environments, with over 70% of Fortune 500 firms integrating machine learning-driven predictive models into operations.

Market Size & Growth: Valued at USD 234.93 Million in 2025, projected to reach USD 871.18 Million by 2033 at a CAGR of 17.8%, driven by enterprise-scale AI automation and real-time data analytics adoption.

Top Growth Drivers: 62% enterprise AI adoption growth, 48% operational efficiency improvement, 35% reduction in manual data processing through neural network deployment.

Short-Term Forecast: By 2028, organizations are expected to achieve up to 30% predictive accuracy improvement and 25% infrastructure cost optimization through advanced neural network architectures.

Emerging Technologies: Edge AI-enabled neural networks, neuromorphic computing chips, federated learning frameworks, and transformer-based deep learning models.

Regional Leaders: North America projected at USD 320 Million by 2033 with strong cloud AI penetration; Asia-Pacific at USD 290 Million driven by smart manufacturing; Europe at USD 180 Million supported by regulated AI adoption frameworks.

Consumer/End-User Trends: BFSI, healthcare, retail, and automotive sectors collectively account for over 55% of deployment demand, with predictive analytics and fraud detection leading use cases.

Pilot or Case Example: In 2024, a large financial institution deployed ANN-driven fraud detection models, achieving 28% reduction in false positives and 22% faster transaction verification cycles.

Competitive Landscape: IBM holds approximately 14% share, followed by Microsoft, Google, Amazon Web Services, and NVIDIA as key technology providers.

Regulatory & ESG Impact: AI governance regulations, data localization mandates, and ESG-focused digital transformation strategies are accelerating responsible ANN deployment.

Investment & Funding Patterns: Over USD 85 Billion invested globally in AI and neural network-focused startups and infrastructure, with increasing venture capital participation and corporate strategic funding.

Innovation & Future Outlook: Integration of generative AI, explainable neural networks, hybrid cloud AI frameworks, and domain-specific AI accelerators is shaping next-generation ANN ecosystems.

The Artificial Neural Networks market demonstrates diversified sectoral contribution, with BFSI accounting for approximately 22% of deployments, healthcare at 18%, retail and e-commerce at 15%, manufacturing at 14%, and automotive and mobility solutions contributing nearly 12%. Recent advancements in transformer-based deep neural networks, low-latency inference chips, and scalable AI model orchestration platforms are redefining performance benchmarks. Regulatory emphasis on transparent AI, data security compliance, and ethical machine learning practices is influencing product development strategies. Asia-Pacific markets are witnessing rapid consumption growth through smart city initiatives and Industry 4.0 adoption, while Europe emphasizes regulated AI frameworks. The evolving integration of hybrid cloud environments, edge-based neural processing, and domain-specific AI solutions continues to reshape long-term enterprise AI investment strategies.

The Artificial Neural Networks Market holds critical strategic relevance as enterprises transition toward intelligent automation, predictive analytics, and real-time decision optimization. Neural network architectures are increasingly embedded within mission-critical systems across finance, healthcare, manufacturing, and mobility ecosystems. Transformer-based neural networks deliver 35% improvement in contextual accuracy compared to traditional recurrent neural network models, enabling higher-performance language processing and predictive modeling. North America dominates in deployment volume, while Asia-Pacific leads in adoption intensity with over 58% of large enterprises integrating AI-driven neural models into at least one operational function.

From a forward strategy perspective, organizations are prioritizing scalable AI infrastructure, hybrid cloud orchestration, and domain-specific neural accelerators to enhance processing efficiency. By 2028, edge-deployed neural network solutions are expected to reduce latency-related operational inefficiencies by 27%, significantly improving real-time analytics performance in manufacturing and smart mobility. ESG alignment is also reshaping investment strategies, with firms committing to 30% reduction in AI data center energy intensity by 2030 through optimized model training and carbon-aware computing frameworks.

In 2024, a leading U.S.-based financial technology company achieved a 31% reduction in fraud detection processing time through advanced deep neural network integration, demonstrating measurable operational efficiency gains. As digital transformation accelerates, the Artificial Neural Networks Market is positioned as a core enabler of resilient infrastructure, regulatory compliance, and sustainable enterprise growth across global industries.

Enterprise-scale AI automation is a primary catalyst driving the Artificial Neural Networks Market. Over 65% of large organizations have integrated AI-powered automation tools to streamline operational workflows, customer analytics, and predictive maintenance. Neural network-based fraud detection systems have reduced financial transaction errors by nearly 25%, while AI-driven quality inspection in manufacturing environments has improved defect detection rates by more than 30%. In healthcare, deep learning models enhance diagnostic imaging accuracy by up to 20% compared to traditional image analysis tools. The growing adoption of AI-enabled chatbots and recommendation engines in retail and e-commerce platforms has improved customer engagement metrics by over 18%. These quantifiable operational improvements underscore how enterprise automation strategies are directly expanding demand for scalable and high-performance neural network frameworks.

Data privacy regulations and high computational infrastructure costs present notable restraints for the Artificial Neural Networks Market. Stringent data protection frameworks require enterprises to implement advanced encryption, localization, and compliance monitoring mechanisms, increasing operational complexity. Training large-scale neural networks often demands high-performance GPUs and specialized AI hardware, with infrastructure investments rising by up to 35% for advanced deep learning environments. Small and medium enterprises face resource limitations in deploying robust AI architectures, slowing adoption rates. Additionally, concerns around algorithmic bias and explainability requirements necessitate additional validation layers, increasing development timelines. These regulatory and infrastructure burdens create entry barriers and necessitate strategic capital allocation for sustainable neural network deployment.

Edge AI integration represents a transformative opportunity for the Artificial Neural Networks Market. With over 75 billion connected devices projected globally within the decade, real-time data processing at the edge is becoming critical. Edge-based neural network models can reduce latency by up to 40% compared to centralized cloud processing, enhancing performance in autonomous vehicles, industrial robotics, and smart healthcare monitoring systems. Manufacturing facilities deploying edge neural networks report up to 22% improvement in predictive maintenance accuracy. Telecommunications operators are also leveraging distributed AI inference to optimize 5G network performance and reduce downtime by approximately 18%. These developments create scalable growth avenues for lightweight, energy-efficient neural architectures tailored for decentralized computing environments.

Increasing model complexity and skilled workforce shortages pose structural challenges for the Artificial Neural Networks Market. Advanced deep neural networks require extensive training datasets and sophisticated hyperparameter optimization, increasing development cycles by nearly 25%. The global shortage of AI specialists, estimated at hundreds of thousands of skilled professionals, constrains large-scale implementation projects. Furthermore, maintaining model transparency and explainability in regulated sectors such as banking and healthcare adds technical intricacy. High computational energy consumption associated with large-scale model training also raises sustainability concerns. These operational, technical, and talent-related constraints require long-term workforce development, optimized model architectures, and strategic partnerships to ensure scalable and responsible neural network deployment.

• Rapid Expansion of Edge-Deployed Neural Networks Reducing Latency by 40%:

Edge-based Artificial Neural Networks are gaining strong traction as enterprises prioritize real-time analytics and decentralized intelligence. More than 48% of industrial IoT deployments now incorporate embedded neural inference models to process data locally. This shift has reduced latency by up to 40% compared to centralized cloud-based processing. In manufacturing environments, on-device neural inspection systems have improved defect detection accuracy by 28%, while autonomous mobility platforms report 22% faster response cycles. Asia-Pacific accounts for over 35% of new edge AI installations, reflecting accelerated smart infrastructure development and Industry 4.0 investments.

• Transformer and Large-Scale Neural Architectures Improving Model Accuracy by 35%:

Advanced transformer-based Artificial Neural Networks are replacing traditional recurrent architectures across natural language processing and predictive analytics use cases. Enterprises report up to 35% higher contextual accuracy and 30% improved pattern recognition capabilities compared to legacy machine learning models. Over 60% of AI-driven enterprise applications deployed in 2024 incorporated transformer-based architectures. Financial institutions leveraging deep neural fraud analytics observed 26% reduction in false positives, while healthcare imaging systems achieved 18% improvement in diagnostic precision, strengthening cross-sector adoption momentum.

• AI Hardware Acceleration Cutting Training Time by 45%:

Specialized AI accelerators, including high-performance GPUs and custom neural processing units, are significantly enhancing training efficiency. Training cycles for complex neural networks have declined by approximately 45% compared to CPU-based environments. More than 52% of enterprise AI workloads are now executed on dedicated AI hardware platforms, enabling scalable deep learning deployments. Cloud-based neural infrastructure adoption increased by 33% year-over-year, supporting large-scale model orchestration. North America leads in AI hardware utilization, while Europe reports 29% growth in on-premise accelerator integration for regulated industries.

• ESG-Driven Energy Optimization Reducing AI Power Consumption by 30%:

Sustainability-focused optimization is emerging as a critical trend in the Artificial Neural Networks market. Enterprises are redesigning training pipelines to reduce computational energy intensity by up to 30% through model pruning, quantization, and efficient architecture design. Approximately 41% of large organizations have implemented carbon-aware AI scheduling strategies to lower data center emissions. Neural compression techniques have reduced model size by 25% without compromising inference accuracy. These environmentally aligned innovations are reshaping procurement strategies, particularly in regions where digital sustainability compliance frameworks mandate measurable reductions in energy consumption.

The Artificial Neural Networks Market is segmented by type, application, and end-user vertical, reflecting diverse deployment strategies across intelligent automation ecosystems. From a technology standpoint, feedforward networks, convolutional neural networks (CNNs), recurrent neural networks (RNNs), and transformer-based architectures form the core structural categories. CNNs dominate image-intensive workloads, while transformers are increasingly adopted for large-scale language and multimodal tasks. Application segmentation highlights strong concentration in predictive analytics, image and speech recognition, cybersecurity modeling, and autonomous systems. End-user insights show significant penetration across BFSI, healthcare, retail, manufacturing, automotive, and telecommunications sectors. More than 65% of large enterprises globally utilize neural networks in at least one mission-critical function, with sector-specific customization driving performance differentiation. The segmentation landscape reflects a strategic transition toward scalable, domain-specific AI deployments that optimize operational efficiency and decision intelligence.

The Artificial Neural Networks Market by type includes Feedforward Neural Networks, Convolutional Neural Networks (CNNs), Recurrent Neural Networks (RNNs), Transformer Networks, and Generative Adversarial Networks (GANs). Convolutional Neural Networks currently account for approximately 34% of adoption due to their dominance in computer vision, medical imaging, and industrial inspection systems. Transformer Networks hold nearly 29% of deployments, primarily in natural language processing and generative AI use cases. However, transformer-based architectures represent the fastest-growing segment, expanding at an estimated 24% CAGR as enterprises integrate large language and multimodal models into customer service and analytics platforms. Recurrent Neural Networks maintain around 18% share, particularly in time-series forecasting and speech processing, while Feedforward Neural Networks contribute nearly 11% in structured data classification tasks. GANs and other specialized neural architectures collectively represent about 8%, serving niche applications such as synthetic data generation and simulation modeling.

Application segmentation of the Artificial Neural Networks Market demonstrates concentrated deployment in Predictive Analytics, Image & Pattern Recognition, Natural Language Processing, Fraud Detection, and Autonomous Systems. Predictive Analytics leads with nearly 26% share, driven by demand for real-time forecasting in finance, supply chain optimization, and demand planning. Image & Pattern Recognition follows at 23%, heavily utilized in healthcare diagnostics and manufacturing quality inspection. Natural Language Processing accounts for 21%, while Fraud Detection systems represent approximately 14% of adoption. Autonomous Systems, including robotics and intelligent mobility platforms, are the fastest-growing application segment, expanding at an estimated 22% CAGR due to advancements in sensor integration and edge AI inference. Collectively, other applications such as cybersecurity analytics and recommendation engines contribute roughly 16% of overall deployments.

By end-user, the Artificial Neural Networks Market is led by BFSI, accounting for approximately 24% of total deployments, supported by extensive fraud detection, algorithmic trading, and risk modeling integration. Healthcare represents nearly 19%, leveraging neural networks for medical imaging, patient monitoring, and clinical decision support. Retail and E-commerce hold around 17% share through recommendation engines and dynamic pricing algorithms. Manufacturing contributes approximately 15%, integrating AI-driven predictive maintenance and quality analytics. The Automotive and Mobility sector is the fastest-growing end-user, expanding at an estimated 23% CAGR due to rapid deployment of neural perception systems in advanced driver-assistance systems and autonomous platforms. Telecommunications, energy, and public sector entities collectively account for about 25% of the remaining market share, reflecting diversified enterprise adoption.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 21% between 2026 and 2033.

North America’s leadership is supported by over 65% enterprise AI integration across large corporations and more than 70% cloud-based neural workload penetration. Europe holds approximately 27% of the global Artificial Neural Networks Market, driven by regulated AI frameworks and industrial automation investments exceeding 30% digitalization penetration in manufacturing. Asia-Pacific accounts for nearly 24% of deployments, with China, India, and Japan collectively representing over 60% of regional consumption. South America contributes around 6%, while the Middle East & Africa holds close to 5%, with increasing adoption in oil & gas, telecom, and public sector modernization programs. More than 55% of neural network installations globally are concentrated in BFSI, healthcare, and manufacturing sectors, reflecting geographically differentiated industrial priorities and digital transformation maturity levels.

How is enterprise-scale AI deployment reshaping competitive intelligence ecosystems?

North America represents approximately 38% of the global Artificial Neural Networks Market share, supported by widespread enterprise AI maturity. Over 72% of Fortune 500 companies have deployed neural network-driven analytics in cybersecurity, fraud detection, and predictive maintenance. Healthcare and BFSI collectively account for nearly 46% of regional deployments, reflecting strong adoption in medical imaging diagnostics and algorithmic trading systems. Federal AI research initiatives exceeding USD 50 billion in combined public-private investments have accelerated high-performance computing infrastructure upgrades. The region also benefits from progressive AI governance frameworks emphasizing data protection and responsible AI. A leading technology provider, NVIDIA, continues expanding AI accelerator production, with its latest neural processing units reducing model training time by 40%. Regional consumer behavior shows higher enterprise adoption in healthcare analytics and digital banking platforms, where over 60% of financial institutions integrate AI-driven risk modeling tools.

Why is regulatory-led innovation accelerating explainable AI adoption?

Europe holds nearly 27% of the global Artificial Neural Networks Market share, led by Germany, the United Kingdom, and France, which collectively represent over 65% of regional deployment volume. Industrial automation and smart manufacturing initiatives contribute to approximately 34% of neural adoption in the region. Regulatory oversight under comprehensive AI compliance frameworks has prompted over 58% of enterprises to prioritize explainable and transparent neural architectures. Sustainability mandates targeting 30% digital energy efficiency improvements by 2030 are also influencing AI infrastructure optimization. SAP, headquartered in Germany, has integrated neural network-based analytics across enterprise resource planning systems, enhancing forecasting accuracy by 25% for industrial clients. Consumer behavior across Europe reflects heightened sensitivity to data privacy and algorithmic transparency, increasing demand for interpretable Artificial Neural Networks in finance, healthcare, and public administration systems.

How are digital infrastructure investments transforming intelligent automation ecosystems?

Asia-Pacific accounts for approximately 24% of the Artificial Neural Networks Market and ranks as the fastest-growing region by deployment expansion. China represents nearly 45% of regional consumption, followed by Japan at 18% and India at 16%. Manufacturing and e-commerce sectors collectively drive over 40% of regional demand, with neural-powered recommendation engines influencing more than 55% of online purchasing decisions. Infrastructure modernization initiatives have resulted in over 5,000 AI-enabled smart factory deployments across the region. Baidu has strengthened its neural-based autonomous driving platforms, achieving 20% improvement in real-time object detection accuracy. Consumer adoption patterns indicate strong demand for mobile AI applications, with more than 70% of digital service users interacting with neural-powered personalization engines in retail and fintech ecosystems.

How are digital banking and media localization accelerating intelligent adoption?

South America contributes around 6% of the global Artificial Neural Networks Market, with Brazil accounting for nearly 52% of regional deployments and Argentina contributing approximately 18%. Financial services represent about 33% of regional neural usage, driven by digital banking expansion and fraud analytics demand. Infrastructure digitization programs in energy and utilities sectors have increased AI integration by 22% over the past two years. Government-led digital innovation incentives encourage local AI development hubs, particularly in Brazil’s fintech ecosystem. Mercado Libre has deployed neural recommendation engines, improving customer engagement rates by 19%. Regional consumer behavior reflects strong reliance on AI-powered language localization and media content personalization, supporting broader adoption across entertainment and e-commerce platforms.

What role does industrial modernization play in accelerating AI adoption?

The Middle East & Africa region represents nearly 5% of the Artificial Neural Networks Market, with the UAE and Saudi Arabia accounting for over 60% of regional demand, followed by South Africa at 14%. Oil & gas and construction sectors collectively contribute around 38% of neural deployments, particularly in predictive maintenance and safety monitoring systems. Smart city investments exceeding USD 20 billion across Gulf nations are integrating AI-driven surveillance and traffic optimization systems. Government-backed digital transformation programs target 25% automation improvement across public services by 2030. G42, based in the UAE, has expanded neural-based cloud AI platforms to enhance public sector analytics capabilities. Regional consumer trends show growing adoption in telecom and financial inclusion services, where mobile AI tools improve customer onboarding efficiency by nearly 17%.

United States – 34% market share: Strong Artificial Neural Networks Market dominance supported by high enterprise AI integration, advanced semiconductor infrastructure, and large-scale investments in cloud-based neural computing platforms.

China – 21% market share: Rapid Artificial Neural Networks Market expansion driven by large-scale manufacturing digitization, national AI modernization initiatives, and extensive adoption across e-commerce and smart mobility ecosystems.

The Artificial Neural Networks Market is moderately consolidated, with over 120 active global competitors spanning technology providers, cloud service platforms, and AI solution integrators. The top five companies—IBM, Microsoft, Google, Amazon Web Services, and NVIDIA—collectively account for approximately 42% of market activity, reflecting strong market positioning in AI infrastructure, neural accelerator development, and enterprise deployment solutions. Competitive strategies are heavily focused on product innovation, strategic partnerships, and expansion of AI-as-a-service platforms. In 2025 alone, over 35 new transformer-based neural architectures and 27 edge-deployed neural solutions were launched by leading providers. Mergers and acquisitions continue to shape market dynamics, with 12 strategic acquisitions targeting specialized AI startups for natural language processing, computer vision, and generative AI applications. Innovation trends, including energy-efficient model compression, hybrid cloud orchestration, and domain-specific neural accelerators, are driving differentiation and influencing enterprise adoption rates. Regional competition varies, with North America leading in high-performance AI hardware and Asia-Pacific emerging as a rapid deployment hub for cloud-based and mobile neural applications. Overall, market dynamics underscore both technological intensity and strategic partnerships as critical levers for competitive advantage.

IBM

Microsoft

Amazon Web Services

NVIDIA

Intel

Baidu

SAP

Huawei

Oracle

Tencent

Salesforce

The Artificial Neural Networks Market is experiencing rapid technological evolution, driven by advances in model architectures, hardware acceleration, and deployment strategies. Transformer-based networks currently dominate large-scale natural language processing, accounting for nearly 29% of enterprise neural deployments, offering up to 35% improvement in contextual understanding compared to traditional recurrent neural networks. Convolutional Neural Networks remain the leading architecture for image recognition and computer vision tasks, representing approximately 34% of type-specific adoption, with real-time defect detection in manufacturing improving accuracy by over 28%.

Edge AI deployment is reshaping operational capabilities, with over 48% of industrial IoT projects now integrating local neural inference to reduce latency by 40% and enhance real-time decision-making. Specialized AI accelerators, including GPUs and neural processing units, have decreased model training times by nearly 45% compared to conventional CPU-based systems, enabling enterprises to scale deep learning applications efficiently. Federated learning frameworks are gaining traction in highly regulated sectors, allowing over 35% of distributed organizations to train models collaboratively while maintaining data privacy compliance.

Generative AI and multimodal neural architectures are emerging as transformative technologies, enabling enterprises to automate content creation, predictive simulation, and advanced recommendation engines, impacting more than 60 million end-users globally in 2025. In parallel, energy-efficient optimization methods, such as model pruning and quantization, have reduced neural network power consumption by up to 30%, aligning AI deployment with ESG objectives. Hybrid cloud orchestration and domain-specific AI accelerators are also shaping future innovation, enabling low-latency inference and secure, scalable deployments across BFSI, healthcare, automotive, and retail sectors. These technological advancements collectively position the Artificial Neural Networks Market as a high-performance, strategically essential pillar for enterprise intelligence and operational optimization.

• In January 2025, CoreWeave became the first cloud provider to commercially deploy Nvidia Blackwell Ultra GPUs (GB300 NVL72), expanding neural network training and inference capacity across enterprise cloud platforms and enabling enterprise-grade AI workloads with enhanced efficiency and performance. (Wikipedia)

• In May 2025, Google DeepMind unveiled “AlphaEvolve,” an evolutionary AI agent that uses advanced neural algorithms to optimize complex problem-solving, demonstrating improved algorithmic performance on 75% of tested open mathematical problems and discovering better solutions 20% of the time.

• In November 2025, Deutsche Telekom and NVIDIA launched Europe’s first Industrial AI Cloud in Berlin, a sovereign enterprise-grade platform powered by up to 10,000 advanced GPUs to accelerate AI adoption in industrial automation and manufacturing sectors ahead of full deployment in early 2026. (NVIDIA Blog)

• In March 2025, Anthropic introduced Claude 4 and expanded API capabilities, including real-time internet search integration and enhanced coding assistance, while securing multiple rounds of funding that significantly bolstered compute capacity and enterprise AI deployment potential.

The Artificial Neural Networks Market Report offers a comprehensive overview of structural and technological segments that define the global AI ecosystem. It covers detailed segmentation by model type, including convolutional neural networks, recurrent architectures, transformer and hybrid neural systems, as well as specialized models for vision, speech, and multimodal processing. The report’s application analysis spans predictive analytics, computer vision, natural language processing, fraud detection, autonomous systems, and edge AI inference solutions, reflecting diverse deployment scenarios across industries.

Geographically, the scope extends across North America, Europe, Asia-Pacific, South America, and Middle East & Africa, capturing regional infrastructure maturity, regulatory influences, and consumption trends unique to each market. Key industry focus areas include finance, healthcare, retail, manufacturing, telecommunications, and automotive sectors, with insights into adoption patterns, digital transformation initiatives, and sector-specific use cases. Technological sub-segmentation highlights hardware accelerators, cloud-native neural services, hybrid deployment models, and emerging innovations like spiking neural networks and energy-efficient model optimization.

The report also incorporates competitive landscapes and ecosystem dynamics, profiling major global players, strategic partnerships, recent technological advancements, and innovation trends shaping the market’s evolution. Additionally, it includes niche segments such as explainable AI systems, federated learning architectures, and domain-specific neural solutions tailored for regulated industries, offering decision-makers a precise and forward-looking understanding of opportunities and challenges.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

17.8% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

IBM, Microsoft, Google, Amazon Web Services, NVIDIA, Intel, Baidu, SAP, Huawei, Oracle, Tencent, Salesforce |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |