Reports

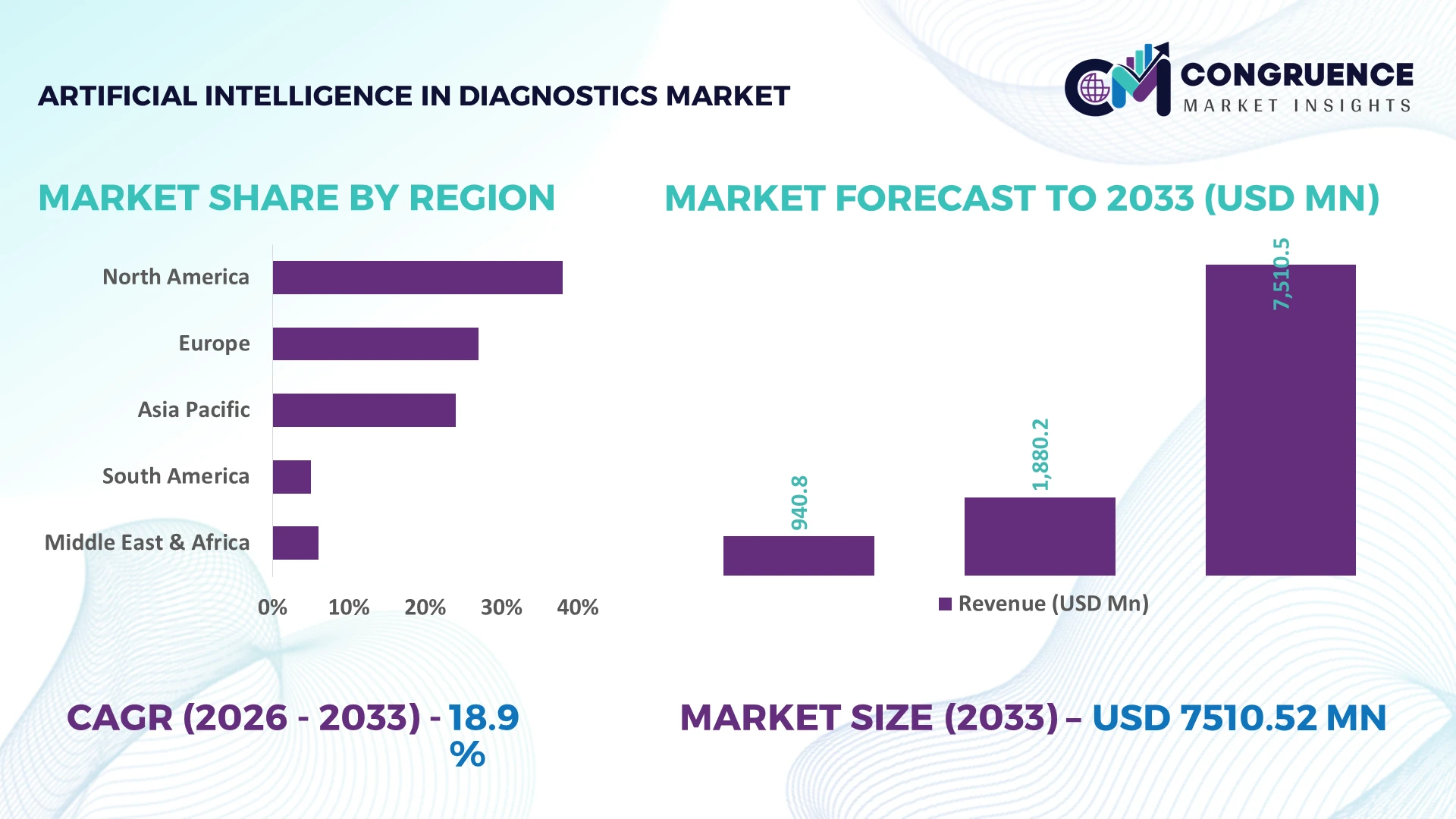

The Global Artificial Intelligence in Diagnostics Market was valued at USD 1880.24 Million in 2025 and is anticipated to reach a value of USD 7510.52 Million by 2033 expanding at a CAGR of 18.9% between 2026 and 2033. Growth is being accelerated by rapid clinical AI integration into radiology, pathology, genomics, and laboratory diagnostics, supported by expanding regulatory approvals and hospital-wide digital imaging infrastructure.

The United States dominates the global Artificial Intelligence in Diagnostics Market with approximately 41% market share, supported by multi-billion-dollar healthcare AI investments, over 6,000 hospital networks adopting digital diagnostics, and strong medical imaging innovation. Compared with Germany, where AI deployment is expanding through public healthcare digitization, the U.S. benefits from faster commercialization despite evolving global AI governance discussions and healthcare cybersecurity priorities in 2026. Organizations investing in validated AI-enabled diagnostic ecosystems and interoperable clinical platforms are positioned to secure long-term competitive advantages.

Market Size & Growth: USD 1880.24 Million (2025) to USD 7510.52 Million (2033) at 18.9% CAGR, driven by enterprise AI diagnostics, cloud imaging platforms, and clinical workflow automation.

Top Growth Drivers: AI-assisted imaging adoption exceeds 55%, digital pathology deployment grows above 40%, and cloud-based diagnostic workflows improve efficiency by 35%.

Short-Term Forecast: By 2028, diagnostic reporting time declines by nearly 30% while laboratory workflow efficiency improves over 25%.

Emerging Technologies: Generative AI, multimodal imaging analytics, and federated learning accelerate advanced diagnostic accuracy across healthcare systems.

Regional Leaders: North America exceeds USD 3.1 Billion, Europe reaches USD 2.0 Billion, and Asia-Pacific surpasses USD 1.8 Billion through expanding hospital digitization.

Consumer/End-User Trends: More than 60% of large healthcare providers integrate AI-assisted diagnostic decision support into routine clinical workflows.

Pilot/Case Example: 2026 hospital imaging deployment improved radiology interpretation productivity by 32% while reducing reporting turnaround time.

Competitive Landscape: Leading vendors collectively control nearly 48% of the market alongside Siemens Healthineers, GE HealthCare, Philips, Roche, and Fujifilm.

Regulatory & ESG Impact: AI governance frameworks reduce algorithm validation timelines by approximately 20% while strengthening clinical transparency and compliance.

Investment & Funding: Global investments exceed USD 5 Billion through strategic partnerships, healthcare innovation funds, and regional AI expansion initiatives.

Innovation & Future Outlook: Next-generation foundation models, predictive diagnostics, and edge AI strengthen precision medicine amid expanding regional healthcare infrastructure.

Artificial Intelligence in Diagnostics Market expansion is increasingly driven by radiology, oncology, pathology, cardiology, and precision medicine applications requiring faster, data-driven clinical decisions. AI-enabled multimodal diagnostic platforms and foundation models continue to enhance workflow performance, with diagnostic accuracy improvements exceeding 20% in selected clinical environments. Growing regulatory standardization and resilient healthcare technology supply chains are strengthening commercial deployment, setting the stage for deeper strategic market analysis.

Artificial Intelligence in Diagnostics has become a strategic priority as healthcare providers compete to improve diagnostic accuracy, reduce clinical workloads, and optimize resource utilization. Infrastructure modernization, stricter AI governance, and digital health integration are accelerating enterprise adoption across imaging centers, pathology laboratories, and hospital networks. More than 65% of large healthcare systems are expanding AI-enabled diagnostic workflows, while standardized clinical validation frameworks introduced during 2025–2026 are strengthening procurement confidence and encouraging long-term investment decisions.

Compared with conventional rule-based diagnostic software, advanced deep-learning platforms reduce image interpretation time by nearly 40% while improving diagnostic sensitivity by approximately 18% in selected radiology applications. The United States leads large-scale commercial deployment through mature healthcare IT infrastructure, whereas Japan is advancing precision diagnostics by integrating AI into aging-care pathways and national screening programs. Over the next two to three years, enterprise AI deployment across high-volume diagnostic departments is expected to exceed 70%, supported by interoperable cloud platforms and automated clinical decision support.

Healthcare technology providers are expanding partnerships with imaging manufacturers, cloud infrastructure companies, and hospital systems to deliver scalable diagnostic ecosystems. A practical example includes AI-assisted chest imaging platforms that prioritize critical cases within minutes, improving emergency department throughput and clinician productivity. Companies are increasing investments in explainable AI, cybersecurity, and multimodal diagnostic platforms to strengthen competitive positioning, improve operational resilience, and secure long-term differentiation in precision healthcare.

Healthcare providers are rapidly integrating AI into radiology, pathology, cardiology, and laboratory diagnostics to improve clinical productivity and diagnostic consistency. More than 60% of tertiary hospitals now evaluate AI-assisted imaging solutions, while automated workflow platforms reduce reporting turnaround by nearly 30% and improve resource utilization by approximately 25%. The United States continues expanding regulatory clearances for clinical AI applications, encouraging faster commercial deployment. In response, technology companies are strengthening partnerships with imaging equipment manufacturers, electronic health record providers, and research institutions while expanding multimodal AI portfolios. A notable strategic shift is the movement from standalone algorithms toward enterprise-wide diagnostic platforms that deliver measurable operational efficiencies across multiple clinical departments.

Fragmented healthcare IT infrastructure and limited interoperability remain significant barriers to large-scale AI deployment. Nearly 45% of hospitals continue operating legacy information systems that complicate seamless AI integration, while implementation costs increase by approximately 20% when multiple proprietary platforms require customization. Germany and several emerging healthcare markets continue addressing fragmented digital infrastructure through modernization initiatives, yet procurement cycles remain lengthy. These constraints affect deployment consistency, operational scalability, and return on technology investments. Companies are reducing implementation risks by developing vendor-neutral software architectures, expanding localized integration partnerships, and offering modular deployment models that simplify compatibility with existing imaging equipment and clinical information systems.

The convergence of multimodal AI, genomics, digital pathology, and cloud-native analytics is creating high-value opportunities beyond traditional medical imaging. More than 50% of enterprise healthcare organizations are prioritizing integrated diagnostic platforms, while AI-assisted pathology workflows improve case prioritization efficiency by nearly 35%. India is strengthening digital health infrastructure and expanding diagnostic access, creating favorable conditions for scalable AI deployments. Companies are increasing R&D investment in foundation models, federated learning, and explainable AI while establishing ecosystem partnerships with pharmaceutical, biotechnology, and diagnostics providers. An emerging strategic advantage lies in unified diagnostic platforms capable of combining imaging, laboratory, and genomic data within a single clinical decision environment.

Long-term market success depends on overcoming deployment complexity, cybersecurity exposure, workforce readiness, and continuous algorithm validation. Approximately 38% of healthcare organizations report shortages of AI-skilled clinical personnel, while cybersecurity incidents targeting healthcare systems have increased by more than 25%, intensifying operational risks. The United Kingdom and other digitally advanced healthcare markets are strengthening governance requirements for clinical AI transparency and lifecycle monitoring. Companies must invest in secure cloud infrastructure, explainable AI frameworks, workforce training, and continuous performance validation to maintain deployment consistency. Organizations that successfully integrate security, compliance, and scalable clinical operations will establish stronger competitive advantages as enterprise AI adoption becomes increasingly standardized.

Multimodal AI Platforms Expand: Healthcare providers are integrating imaging, pathology, and genomic datasets into unified AI platforms, reducing diagnostic workflow duplication by nearly 28% and improving multidisciplinary decision accuracy by approximately 20%. Regulatory expectations for clinically validated AI models are accelerating enterprise deployments, while vendors respond through platform consolidation, cloud integration, and strategic partnerships that simplify hospital-wide implementation and lower operational complexity.

Edge Deployment Gains Momentum: Hospitals are moving AI inference closer to imaging equipment, reducing image processing latency by around 35% and decreasing cloud data transfer requirements by nearly 25%. Data privacy regulations and cybersecurity priorities are driving localized computing adoption, particularly across the United States and Japan. Technology providers are restructuring product portfolios to include embedded AI hardware, enabling faster emergency diagnostics and more resilient clinical operations.

Workflow Automation Reshapes Laboratories: AI-driven automation now supports specimen prioritization, quality assurance, and reporting, increasing laboratory throughput by approximately 30% while reducing manual verification workloads by nearly 22%. Persistent shortages of skilled diagnostic professionals are encouraging laboratories to redesign operating models. Companies are expanding automation partnerships and integrating intelligent orchestration software that balances workload distribution across multiple diagnostic sites.

Explainable AI Becomes Standard: Healthcare organizations increasingly require transparent AI outputs, with more than 60% of enterprise procurement programs evaluating explainability before deployment. Clinical governance reforms and evolving regulatory frameworks are shifting procurement priorities beyond algorithm accuracy alone. Companies are investing in interpretable AI, continuous model monitoring, and validation frameworks, strengthening physician confidence while creating differentiation through measurable compliance, accountability, and long-term deployment reliability.

Imaging Diagnostics remains the leading segment because of its extensive integration with radiology infrastructure, high examination volumes, and proven workflow efficiency. More than 58% of enterprise AI diagnostic deployments focus on imaging applications, where automated image interpretation shortens reporting time by approximately 30%. Diagnostic Software continues supporting interoperability and workflow orchestration, while Clinical Decision Support strengthens physician confidence through evidence-based recommendations. Companies are expanding imaging portfolios through strategic acquisitions, cloud-native platforms, and direct integration with picture archiving and communication systems to improve scalability across hospital networks.

Predictive Diagnostics represents the fastest-growing segment as healthcare providers increasingly prioritize early disease detection and risk stratification. AI-enabled predictive models improve patient prioritization accuracy by nearly 24%, while In Vitro Diagnostics benefits from automation that enhances laboratory efficiency by around 20%. Vendors are investing in multimodal analytics, integrated software ecosystems, and specialized diagnostic algorithms, shifting investment priorities toward platforms capable of combining imaging, laboratory, and clinical datasets into unified decision environments.

Radiology remains the dominant application due to standardized imaging workflows, extensive digital infrastructure, and high examination volumes. More than 60% of AI-assisted diagnostic implementations are concentrated within radiology departments, where automated image analysis reduces interpretation time by approximately 35%. Cardiology continues strengthening adoption through AI-assisted echocardiography and ECG interpretation, while Pathology expands digital slide analysis to improve diagnostic consistency. Healthcare technology companies are enhancing interoperability and workflow automation to support enterprise-scale deployment across imaging departments.

Oncology is the fastest-growing application as precision medicine and biomarker-driven treatment planning become operational priorities. AI-assisted oncology workflows improve lesion detection accuracy by nearly 22%, while Neurology benefits from rapid stroke assessment and neuroimaging analysis that accelerate emergency decision-making. Vendors are expanding partnerships with hospital systems, integrating multimodal analytics, and developing disease-specific AI models that address specialized clinical workflows while improving operational efficiency and diagnostic confidence.

Hospitals represent the largest end-user segment because they operate integrated diagnostic ecosystems, advanced imaging infrastructure, and multidisciplinary clinical teams. Approximately 62% of enterprise AI diagnostic deployments occur within hospitals, where workflow automation improves reporting efficiency by nearly 30% and supports higher patient throughput. Diagnostic Laboratories remain strategically important through increasing laboratory automation, while Imaging Centers continue adopting AI to improve examination turnaround and optimize equipment utilization. Technology providers are prioritizing enterprise licensing, integrated implementation services, and long-term support agreements to strengthen customer retention.

Specialty Clinics are emerging as the fastest-growing end-user group as AI becomes more accessible through cloud-based platforms and subscription deployment models. Research Institutes continue driving algorithm validation and clinical innovation, supporting new product commercialization. Companies are tailoring pricing structures, forming partnerships with specialty healthcare providers, and developing modular AI platforms that reduce deployment barriers while expanding addressable markets. This competitive shift reflects growing demand for flexible, scalable diagnostic solutions beyond traditional hospital environments.

North America accounted for the largest market share at 39.8% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a 20.8% CAGR between 2026 and 2033.

Digital Clinical Infrastructure Accelerates Enterprise AI Deployment

North America maintains the strongest position through advanced healthcare IT infrastructure, extensive diagnostic imaging networks, and early commercialization of clinical AI platforms. The region contributes nearly 40% of global deployment activity, supported by enterprise hospitals integrating AI across radiology, pathology, and laboratory operations. More than 68% of large healthcare systems have adopted at least one AI-enabled diagnostic workflow, while strategic collaborations between software developers, imaging manufacturers, and cloud providers continue expanding enterprise implementation. Investment in interoperable clinical platforms and explainable AI is strengthening operational efficiency, accelerating deployment consistency, and supporting standardized diagnostic decision-making across integrated healthcare networks.

United States Market Outlook: The United States remains the largest national market because of mature digital healthcare infrastructure, strong regulatory momentum, and extensive enterprise investment in AI-enabled diagnostics. More than 70% of leading academic medical centers have expanded AI-assisted imaging or clinical decision support deployments, while healthcare providers continue integrating multimodal diagnostic platforms with electronic health records. Technology companies are strengthening partnerships with hospitals and medical device manufacturers to commercialize scalable AI ecosystems that improve workflow efficiency and diagnostic precision.

Regulatory Alignment Strengthens Clinical AI Adoption

Europe continues expanding AI-enabled diagnostics through healthcare modernization, harmonized digital health policies, and strong medical technology capabilities. The region accounts for approximately 28% of global market activity, with increasing deployment across public hospital networks and university healthcare systems. More than 55% of newly procured diagnostic imaging platforms now support embedded AI functionality, improving workflow standardization and clinical productivity. Medical device companies are investing in interoperable software, cybersecurity compliance, and cloud-enabled diagnostic ecosystems, enabling healthcare providers to accelerate enterprise implementation while maintaining stringent clinical governance standards.

Germany Market Outlook: Germany leads the European market through its advanced medical technology industry, hospital digitization programs, and engineering expertise. AI integration continues expanding across radiology and pathology departments supported by nationwide digital health initiatives. More than 60% of large university hospitals have introduced AI-assisted diagnostic applications within specialized clinical departments. Domestic technology providers and global manufacturers are strengthening collaborative research, software validation, and enterprise deployment programs to improve healthcare productivity and long-term operational resilience.

Healthcare Digitalization Drives High-Scale Deployment

Asia-Pacific is emerging as the fastest-expanding regional market through rapid healthcare digitization, expanding diagnostic infrastructure, and increasing AI investment across major economies. The region represents approximately 24% of global deployment activity, with governments accelerating digital healthcare transformation and hospital modernization. More than 35% of newly established tertiary hospitals are incorporating AI-ready imaging infrastructure during construction or expansion. Technology firms are scaling cloud-based diagnostic platforms, forming healthcare partnerships, and localizing AI development to address growing clinical workloads while improving diagnostic accessibility across diverse healthcare systems.

China Market Outlook: China dominates the regional landscape through extensive hospital infrastructure, strong artificial intelligence capabilities, and large-scale medical imaging deployment. National digital healthcare initiatives continue supporting AI adoption across tertiary hospitals and provincial healthcare systems. More than 65% of top-tier hospitals have incorporated AI-assisted imaging into selected diagnostic workflows. Domestic technology companies are investing heavily in algorithm development, cloud infrastructure, and medical device integration, strengthening enterprise competitiveness while supporting nationwide healthcare modernization objectives.

Hospital Modernization Expands AI Utilization

South America is experiencing steady adoption as healthcare providers modernize diagnostic capabilities and expand digital infrastructure despite budgetary constraints. The region contributes approximately 5% of global market activity, with enterprise hospitals leading implementation across radiology and laboratory services. AI-assisted workflow deployment has increased by nearly 22% among large private healthcare organizations, supported by partnerships between healthcare providers and technology vendors. Operational progress remains uneven because of infrastructure disparities, yet investments in cloud-based diagnostic platforms and scalable software solutions are improving accessibility and reducing implementation complexity.

Brazil Market Outlook: Brazil represents the region's largest market through its extensive hospital network, expanding private healthcare sector, and growing digital transformation initiatives. Large diagnostic providers continue integrating AI into imaging interpretation and laboratory management to improve operational efficiency. Healthcare organizations are strengthening partnerships with international technology companies while expanding cloud-enabled diagnostic infrastructure. Enterprise adoption continues increasing across metropolitan healthcare systems where digital imaging capacity and specialist demand remain highest.

Strategic Healthcare Investment Supports AI Transformation

The Middle East & Africa market is advancing through government-backed healthcare modernization, smart hospital initiatives, and increased investment in digital diagnostics. The region accounts for roughly 3% of global market activity, with AI deployment concentrated in advanced healthcare hubs. More than 30% of newly commissioned flagship hospitals are incorporating AI-enabled diagnostic capabilities during infrastructure development. Healthcare organizations are prioritizing cloud connectivity, enterprise imaging platforms, and specialized technology partnerships to improve clinical capacity while supporting long-term healthcare transformation strategies.

Saudi Arabia Market Outlook: Saudi Arabia leads regional development through ambitious healthcare modernization programs, digital transformation policies, and significant investment in advanced medical infrastructure. National initiatives continue encouraging AI integration across public hospitals, imaging centers, and specialist healthcare facilities. Large healthcare providers are expanding enterprise diagnostic platforms and collaborating with international technology companies to strengthen clinical efficiency, improve diagnostic quality, and establish scalable AI-enabled healthcare ecosystems aligned with long-term national development priorities.

The Artificial Intelligence in Diagnostics Market is led by Siemens Healthineers, GE HealthCare, Philips, Roche, and Fujifilm, competing directly with specialized AI innovators such as Aidoc, Viz.ai, and Gleamer. Global imaging leaders leverage installed equipment ecosystems, while software-focused innovators compete through algorithm performance, workflow integration, and rapid deployment. The top five participants collectively control approximately 47% of the market. Competition increasingly centers on diagnostic accuracy improvements exceeding 20%, workflow automation reducing reporting time by nearly 30%, and cloud-enabled implementation lowering deployment complexity by around 25%. Established manufacturers are strengthening positions through acquisitions, enterprise partnerships, and vertical integration across imaging hardware and AI software, while emerging companies emphasize disease-specific algorithms and subscription delivery models. The competitive landscape is shifting toward integrated diagnostic ecosystems rather than standalone applications, increasing pressure on vendors lacking interoperability and clinical validation. Regulatory compliance, enterprise integration capability, and scalable deployment remain the primary entry barriers. Winning requires clinically validated AI platforms, seamless hospital integration, continuous innovation, and trusted long-term healthcare partnerships.

Siemens Healthineers

GE HealthCare

Philips

Roche

Fujifilm

Canon Medical Systems

Aidoc

Viz.ai

Gleamer

Qure.ai

Tempus AI

PathAI

Arterys

Lunit

Current technology development is centered on deep learning, computer vision, and multimodal AI capable of analyzing medical images, pathology slides, laboratory results, and clinical records within unified diagnostic workflows. More than 60% of enterprise healthcare organizations are deploying AI-assisted imaging platforms, while workflow automation reduces reporting time by approximately 30%. Cloud-native architectures increasingly replace isolated on-premise deployments, improving collaboration, scalability, and software update cycles across multi-hospital networks.

Emerging technologies include foundation models, federated learning, explainable AI, and edge computing integrated directly into diagnostic equipment. Compared with traditional rule-based software, foundation model-based diagnostic systems improve complex pattern recognition by nearly 22% while reducing manual data preparation by approximately 18%. Imaging manufacturers, enterprise hospitals, and specialized AI software providers gain the strongest competitive advantage through integrated platforms combining imaging, genomics, and laboratory intelligence. Explainable AI is also becoming a procurement requirement, strengthening physician confidence and regulatory readiness.

Between 2026 and 2028, autonomous workflow orchestration, multimodal clinical reasoning, and predictive diagnostics will reshape enterprise healthcare operations. AI deployment across advanced diagnostic departments is expected to exceed 70%, enabling faster triage, resource optimization, and personalized treatment planning. Organizations investing now in interoperable AI ecosystems, cybersecurity, and continuous model validation will establish durable operational advantages, while delayed adopters risk integration complexity, slower clinical productivity, and reduced competitiveness in precision diagnostics.

November 2025: Philips expanded its AI diagnostics portfolio through a partnership with Cortechs.ai by integrating NeuroQuant into Philips Smart Reading, enabling automated quantitative brain MRI analysis and streamlining neurological assessments across enterprise imaging workflows. Source: Philips

January 2026: Aidoc received U.S. FDA clearance for its CARE foundation model-powered multi-triage CT solution, combining 11 newly cleared indications with 3 existing indications into a single workflow, significantly expanding enterprise clinical AI deployment across emergency imaging services. Source: Aidoc

March 2026: Viz.ai partnered with Alnylam Pharmaceuticals to launch an AI-enabled cardiac amyloidosis care pathway, strengthening coordinated diagnosis and treatment workflows while expanding enterprise adoption of disease-specific clinical AI solutions across cardiovascular care networks. Source: Viz.ai

May 2026: Siemens Healthineers received FDA clearance for six new Artis interventional imaging systems featuring the Optiq AI Imaging Chain, enhancing real-time image quality across 6 platforms and strengthening AI-enabled precision imaging for complex interventional procedures. Source: Siemens Healthineers

The report delivers comprehensive analysis of the Artificial Intelligence in Diagnostics Market across Imaging Diagnostics, In Vitro Diagnostics, Predictive Diagnostics, Clinical Decision Support, and Diagnostic Software, while evaluating demand across Radiology, Pathology, Cardiology, Oncology, and Neurology. It further examines adoption trends among Hospitals, Diagnostic Laboratories, Imaging Centers, Research Institutes, and Specialty Clinics across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, covering more than 25 major healthcare economies.

The study assesses competitive positioning, enterprise deployment strategies, multimodal AI, foundation models, explainable AI, cloud-based diagnostics, and edge AI integration. With enterprise AI adoption exceeding 60% among leading healthcare providers, the report provides actionable insights into technology evolution, regional deployment patterns, investment priorities, partnership strategies, and emerging precision diagnostics opportunities. It supports business expansion, product development, competitive benchmarking, and strategic decision-making for organizations operating across the global Artificial Intelligence in Diagnostics Market between 2026 and 2033.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 1880.24 Million |

Market Revenue in 2033 | USD 7510.52 Million |

CAGR (2026 - 2033) | 18.9% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Siemens Healthineers, GE HealthCare, Philips, Roche, Fujifilm, Canon Medical Systems, Aidoc, Viz.ai, Gleamer, Qure.ai, Tempus AI, PathAI, Arterys, Lunit |

Customization & Pricing | Available on Request (10% Customization is Free) |