Reports

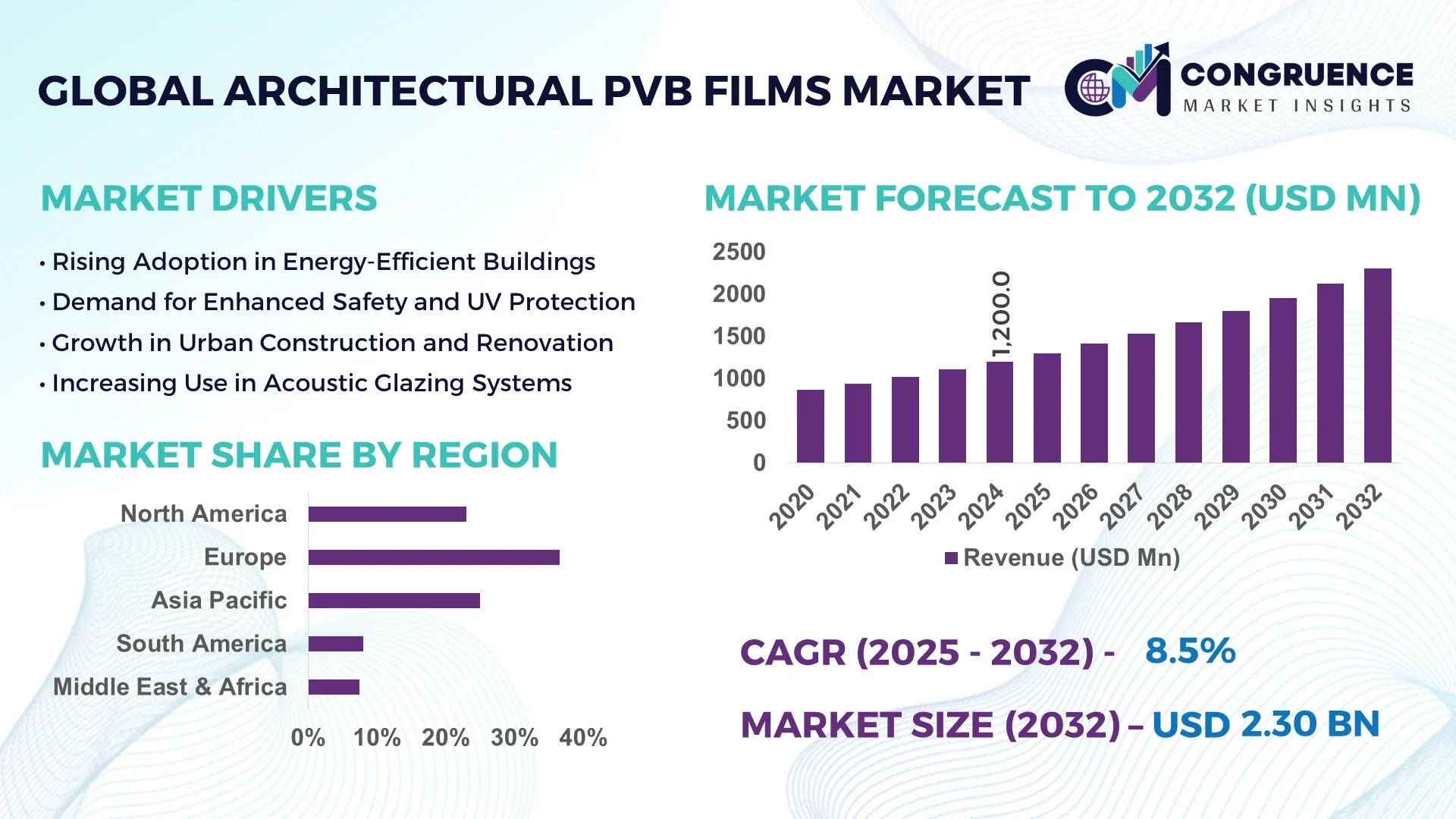

The Global Architectural PVB Films Market was valued at USD 1,200.0 Million in 2024 and is anticipated to reach a value of USD 2304.7 Million by 2032 expanding at a CAGR of 8.5% between 2025 and 2032.

Germany leads the Architectural PVB Films Market with advanced production infrastructure, including a dedicated 30,000-tonne annual capacity plant commissioned in 2023. The country has invested €75 million in modernization programs, supplying key sectors such as commercial glazing, blast-resistant façades, and high-performance sound-insulating glass systems. German manufacturers have implemented in-line UV-stabilization and acoustic layering technologies, pushing innovation in architectural safety films.

The Architectural PVB Films Market spans sectors including residential and commercial construction, automotive glazing, industrial façades, and aerospace, each contributing distinct value. Construction applications account for the majority of film usage, driven by demand for laminated safety and solar-control glazing, while automotive and aerospace sectors rely on specialized film formulations for lightweight, high-transparency glazing solutions. Recent innovations include multi-layer acoustic PVB films with staggered density profiles and solar-control variants with embedded reflective particulates. Regulatory drivers, such as stricter impact-resistance and fire-safety standards in built environments, have accelerated adoption. Sustainable construction initiatives are informing usage of formaldehyde-free and solvent-reduced PVB formulations. Consumption patterns vary regionally: mature markets in Europe prioritize safety and sustainability, while emerging markets in Asia and Latin America invest heavily in urban infrastructure projects. Going forward, demand is expected to grow through custom film blends targeting energy efficiency, digital production lines for thickness control, and localized film manufacturing hubs aligning with urbanization and green-building trends.

AI is making significant inroads into the Architectural PVB Films Market, revolutionizing both production and product quality. In manufacturing, AI-driven real-time monitoring systems now adjust extrusion parameters—like temperature and film draw rate—automatically, reducing thickness deviation to under 2%. Predictive maintenance platforms, powered by machine learning, have decreased unscheduled downtime by up to 28%, allowing manufacturers to maintain continuous film production pipelines. Quality control systems using computer vision inspect film surfaces at full production line speed, catching micro-inclusions or delamination issues with over 99% detection accuracy—far higher than traditional manual checks.

On the research and development front, AI algorithms analyze formulation datasets to optimize PVB-laminated film properties, such as acoustic dampening and solar control performance, cutting iteration cycles by half. In logistics, AI-enabled demand forecasting tools match production output to regional construction tender data, reducing overproduction risk and slashing warehouse holding time by approximately 20%. Vendors are also using AI-driven digital platforms that allow architects and specifiers to input project parameters and receive automated film product recommendations tailored to performance needs—streamlining project procurement cycles.

These AI-driven transformations are enhancing operational efficiency, quality assurance, and responsiveness within the Architectural PVB Films Market, enabling companies to deliver customized solutions more rapidly and reliably. Decision-makers benefit from enhanced predictive insights and reduced waste, while end-users gain access to film materials that meet precise acoustic, safety, and solar-performance criteria with improved supply chain reliability.

“In 2024, a German film producer introduced an AI-powered extrusion control system that reduced film thickness tolerance from ±15 µm to ±3 µm, improving uniformity and reducing material scrap by 18%.”

The Architectural PVB Films Market dynamics reflect a transition towards high-performance glazing solutions, driven by regulatory mandates, environmental standards, and design innovation. Safety and acoustic regulations in building codes now prioritize laminated glass with certified PVB films, encouraging manufacturers to enhance product portfolios. Simultaneously, sustainability trends are pushing film producers toward formaldehyde-free, solvent-reduced, and recycled-content PVB variants. Digitization is reshaping value chains: real-time extrusion control, AI-based QC, and smart logistics systems are boosting productivity and transparency. Customization is on the rise—architects increasingly specify film blends targeting solar gain control, daylight modulation, and iconic façade aesthetics. At the same time, cost pressures and raw material volatility require manufacturers to optimize supply chains and stabilize pricing. Urbanization-driven construction projects in emerging regions are expanding film consumption volumes, while retrofit demand in mature markets fuels demand for acoustic and visually controllable films. Overall, the Architectural PVB Films Market is being steered by performance innovation, sustainability integration, and operational intelligence.

Building standards now require laminated glass capable of resisting blasts, bullets, or airborne noise above 45 dB. Adoption of multi-layer PVB films with staggered densities has increased by 40% in commercial façade markets. Manufacturers have scaled production of acoustic-grade films by investing in in-line compaction rollers and ultrasonic bonding systems to meet these performance needs.

Acoustic, solar-control, and blast-resistant PVB films rely on costly additives, such as nano-silica or metallic flakes, raising unit costs by up to 25%. This restricts adoption among value-sensitive residential projects. Moreover, variable raw material pricing has forced inventory buffers and pricing volatility, affecting profitability.

An estimated 15% of global commercial buildings now use retrofit PVB films to upgrade façades for energy savings and acoustic insulation. Retrofit programs offer 5–7-year ROI, prompting film vendors to launch self-adhesive PVB retrofit kits compatible with standard laminated glass, expanding market reach into retrofit and renovation segments.

Safety and sustainability standards vary widely: the U.S. adopts ANSI Z97.1, Europe uses EN 356, Asia-Pacific has fragmented national codes. These differences require film producers to run multiple certification lines and maintain country-specific documentation, increasing costs and complicating product launches in multi-region projects.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Architectural PVB Films Market. Pre-bent and cut elements are prefabricated off-site using automated machines, reducing labor needs and speeding project timelines. Demand for high-precision machines is rising, especially in Europe and North America, where construction efficiency is critical.

Advanced Acoustic Film Layers for Urban Environments: Manufacturers now produce PVB films engineered to reduce traffic and construction noise by up to 48 dB, exceeding previous 40 dB benchmarks. Adoption in urban retrofit projects has grown by 30%, driven by stricter urban noise ordinances and tenant comfort standards in high-density cities.

Solar-Control Multilayer Films for Low‑E Glazing: High-performance PVB films embedded with micron‑scale reflective flakes are being used to reduce solar heat gain by up to 65% without compromising visible light transmittance. Such films are increasingly specified in LEED-certified buildings and low-emission façade systems.

Smart Specification Platforms for Project Teams: Digital B2B tools allow architects to input project criteria (e.g., seismic risk, solar exposure, noise levels) and receive automated PVB film recommendations within minutes. These platforms have accelerated specification cycles by around 40% and improved compliance accuracy, enhancing coordination among design, procurement, and glazing installers.

The Architectural PVB Films Market is segmented based on type, application, and end-user, offering a comprehensive view of its diverse landscape. Each segment plays a distinct role in shaping product demand, technological integration, and investment direction. In terms of type, films vary by functional performance such as safety, acoustics, solar control, and UV resistance. Application-wise, demand is driven by usage in commercial facades, residential windows, and automotive glass, with increased focus on sustainability and energy efficiency. End-user segmentation further reveals how stakeholders such as construction companies, architects, automotive OEMs, and government infrastructure agencies influence product specifications, volume consumption, and regional variation. Growth dynamics across these segments are guided by factors such as tightening regulatory frameworks, urban infrastructure upgrades, and the integration of smart film technologies in new construction and renovation projects.

Architectural PVB films are classified into several types, with standard clear PVB films leading the market due to their widespread use in safety glazing for windows and doors in residential and commercial buildings. These films offer reliable adhesion and impact resistance, making them a preferred choice in basic construction requirements.

Acoustic PVB films are the fastest-growing segment, driven by rising demand for noise insulation in urban environments. These films are engineered with specialized multilayer structures to suppress sound transmission, making them ideal for buildings near highways, airports, and industrial zones.

Other film types include solar-control PVB films, which incorporate reflective or absorptive particles to reduce heat gain and improve indoor comfort. These are gaining popularity in green buildings and energy-efficient retrofits. Colored and UV-resistant PVB films also hold niche appeal in decorative facades and sun-facing structures where aesthetics or material longevity is prioritized. The growing customization of PVB film properties to match project-specific needs is expected to further diversify the type segment.

Among various applications, building and construction remains the dominant segment in the Architectural PVB Films Market. This is largely due to stringent safety and energy performance standards for glazing in both new developments and renovation projects. These films are integral in laminated glass used for façades, curtain walls, partitions, skylights, and balconies, where safety, acoustic insulation, and solar performance are critical.

The automotive sector is emerging as the fastest-growing application area. With increasing adoption of laminated side and roof glass for enhanced passenger safety and comfort, automotive OEMs are turning to advanced PVB films for superior clarity, UV resistance, and sound dampening properties.

Other notable application areas include public infrastructure such as airports, railway stations, and hospitals, where blast-resistance and acoustic control are priorities. Additionally, interior architecture is leveraging colored and decorative PVB films for aesthetic innovation in glass partitions and staircases. Overall, applications are evolving to prioritize multifunctionality—safety, design, and performance in a single film product.

Commercial construction firms and developers represent the leading end-user group in the Architectural PVB Films Market. They drive demand for high-performance glazing solutions in commercial buildings, corporate offices, shopping complexes, and hospitality projects, where aesthetics and regulatory compliance are equally critical.

The fastest-growing end-user segment is public infrastructure authorities, propelled by increasing government investments in smart cities, transportation terminals, and educational campuses. These projects require materials with certified safety ratings and durability, making PVB films a core component of specified building materials.

Other relevant end-users include residential developers, particularly in urban centers focused on luxury and mid-rise developments with enhanced energy efficiency standards. Architectural and design firms also influence demand by specifying customized film properties in bespoke architectural projects. Additionally, automotive OEMs are increasingly integrating these films in their vehicle platforms to meet safety, noise, and sustainability expectations. Collectively, these end-users are shaping product innovation and diversification within the market.

Europe accounted for the largest market share at 36.5% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.4% between 2025 and 2032.

Europe’s leadership stems from stringent building safety regulations, early adoption of sustainable construction practices, and strong presence of global PVB film manufacturers. In contrast, Asia-Pacific’s rapid growth is being driven by large-scale urbanization, infrastructure upgrades, and rising investments in commercial real estate. Across regions, the Architectural PVB Films Market is being shaped by varying degrees of technological integration, regulatory rigor, and construction activity intensity. While North America continues to witness robust demand from commercial building retrofits and acoustically efficient glass solutions, Latin America and Middle East & Africa are slowly catching up, supported by policy reforms and energy efficiency mandates. Regional market differentiation is increasingly pronounced, requiring customized product strategies for optimal penetration and compliance.

North America holds a significant market share of 24.1%, primarily fueled by commercial and institutional construction in the United States and Canada. Demand is particularly strong in high-rise buildings and retrofitting projects aiming to meet advanced energy efficiency standards. Key sectors include hospitality, education, and corporate real estate. Recent U.S. government policies mandating laminated safety glass in public buildings are creating favorable conditions for increased adoption. Moreover, several state-level green building codes have accelerated the use of solar-control and acoustic PVB films. Technological trends such as AI-integrated film inspection systems, dynamic glazing interfaces, and prefabricated laminated panels are rapidly modernizing production lines. These innovations are helping regional manufacturers meet evolving safety and sustainability expectations with greater precision and productivity.

Europe commands the highest market share in the Architectural PVB Films Market, standing at 36.5% in 2024. Germany, the UK, and France are the key contributors due to their stringent façade safety regulations and strong investment in green infrastructure. European standards such as EN 12600 and EN 356 guide the use of laminated safety films across commercial and residential applications. Sustainability initiatives led by the European Commission, including building energy performance directives, have bolstered the market for solar-control and low-emission PVB films. Leading manufacturers are integrating recycled content and formaldehyde-free bonding technologies to comply with circular economy goals. Moreover, smart glazing technologies and acoustic-grade films have seen increased adoption in urban development projects across Northern and Western Europe.

Asia-Pacific ranks as the fastest-growing regional market with increasing consumption led by China, India, and Japan. The region is witnessing large-scale urban redevelopment, smart city programs, and modernization of public infrastructure that boost demand for laminated glass applications. China leads in terms of manufacturing capacity and domestic consumption, followed closely by India's metro city development plans and transport terminal upgrades. Japan’s focus on seismic-resilient architecture also contributes to demand for high-performance PVB interlayers. Emerging tech hubs in South Korea and Singapore are promoting use of solar-control films for energy-efficient buildings. Additionally, regional manufacturers are investing in domestic production lines to minimize dependency on imports and improve customization speed for infrastructure developers.

South America's Architectural PVB Films Market is expanding steadily, with Brazil and Argentina emerging as major contributors. The region accounted for approximately 6.2% of the global volume in 2024. Government programs aimed at improving public infrastructure and urban housing quality, particularly in Brazil, have stimulated interest in laminated safety glazing. Regulatory policies encouraging energy-efficient construction materials are also gaining traction. The hospitality and tourism sectors are key demand drivers for acoustic and decorative PVB films in hotel glazing and interior applications. Brazil has implemented trade incentives for local film producers, while Argentina is witnessing increased imports of high-specification films for premium construction projects. Despite economic volatility, structural housing needs continue to drive market relevance.

Middle East & Africa accounted for 5.7% of global market demand in 2024, with significant contributions from the UAE, Saudi Arabia, and South Africa. Regional demand is driven by large commercial and institutional construction projects supported by oil revenues and economic diversification plans. The UAE’s emphasis on high-rise development, including luxury hotels and mixed-use towers, boosts demand for high-performance laminated films. South Africa’s adoption of impact-resistant and solar-reducing glass in public infrastructure supports acoustic-grade PVB consumption. Technological modernization is visible through increased use of automated lamination equipment and digitally optimized manufacturing. Local regulations such as the UAE’s Estidama and Saudi Vision 2030 further promote use of advanced glass solutions, positioning the region for long-term structural demand.

Germany – 18.2% Market Share

Germany leads due to its advanced production infrastructure, strict safety standards, and consistent demand from high-end commercial real estate and transportation terminals.

China – 16.5% Market Share

China follows closely with large-scale urban infrastructure development, robust manufacturing capacity, and demand from domestic construction megaprojects.

The Architectural PVB Films Market is characterized by a moderately consolidated competitive landscape, with approximately 20–25 active global players and several regional manufacturers. Leading companies maintain a strong presence through vertically integrated production systems, wide product portfolios, and strategic global footprints. Competition is driven by innovation, quality certification, and alignment with green building standards. Several players are actively engaging in partnerships with construction firms and glass manufacturers to co-develop customized film solutions with advanced properties such as sound insulation, UV protection, and thermal performance.

Key industry participants are investing in R&D to develop bio-based PVB films, aiming to reduce environmental impact and meet sustainable building mandates. Mergers and acquisitions are also reshaping market dynamics, as companies seek to strengthen their geographic reach and production capabilities. Product differentiation through functional layering technologies, anti-fog and anti-glare properties, and digitally integrated inspection systems is gaining momentum. The growing trend of smart glass integration, especially in commercial and institutional buildings, is encouraging firms to innovate and maintain a competitive edge through technical enhancements and compliance leadership.

Eastman Chemical Company

Kuraray Co., Ltd.

Sekisui Chemical Co., Ltd.

Everlam

DuLite Technologies

Huakai Plastic (Chongqing) Co., Ltd.

Zhejiang Decent Plastic Co., Ltd.

Chang Chun Group

Saflex Interlayers

Kingboard Chemical Holdings Limited

The Architectural PVB Films Market is witnessing significant advancements in both material innovation and production technology. Modern PVB films now offer multifunctional performance including acoustic damping, enhanced UV protection, and solar control. Manufacturers are deploying co-extrusion technology to produce multilayer films that meet evolving performance standards across safety, energy efficiency, and aesthetics. These multilayer structures also allow the inclusion of decorative tints or patterns without compromising structural integrity.

In addition, digital lamination inspection systems powered by machine vision and AI are being widely adopted in manufacturing lines to ensure uniform adhesion and defect-free film quality. These systems improve yield rates and lower operational costs by automating quality control. Bio-based and recycled PVB materials are gaining traction in alignment with green building regulations and circular economy goals. These sustainable variants typically include renewable raw content and demonstrate comparable performance in impact resistance and clarity.

Thermo-adaptive PVB films that respond to external temperature changes to regulate light transmission are also under development. These smart films enhance building energy performance without the need for active control systems. Furthermore, advancements in UV-blocking nanoparticles and infrared-reflective coatings integrated into PVB films are pushing the boundaries of solar efficiency. The convergence of digital automation, sustainability, and smart functionality is setting the direction for future innovation in this market.

In March 2024, Kuraray Co., Ltd. launched a new generation of acoustic PVB interlayers designed specifically for commercial skyscrapers, featuring improved sound insulation ratings of up to 42 dB and enhanced optical clarity.

In December 2023, Everlam commissioned a fully automated PVB film production line in Belgium to meet growing demand across Europe, improving annual output capacity by 20% and reducing production downtime by 15%.

In July 2024, Eastman Chemical introduced a low-carbon PVB film variant made using renewable energy and incorporating 25% recycled resin content, aligning with industry sustainability benchmarks for green construction.

In February 2024, Sekisui Chemical unveiled an anti-fog architectural PVB film optimized for humid environments such as tropical commercial centers and transportation hubs, increasing market reach in Southeast Asia.

The Architectural PVB Films Market Report offers an in-depth analysis of the global market landscape covering product types, key applications, end-user sectors, regional performance, and technological advancements. The report focuses on various types of PVB films such as standard clear, acoustic, solar control, UV-resistant, and decorative interlayers, analyzing their deployment across construction and infrastructure projects. It also evaluates critical application areas including commercial glazing, residential windows, interior partitions, public infrastructure, and automotive glass.

Geographically, the report spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, offering granular insights into regional consumption patterns, investment trends, regulatory environments, and technological maturity. The report highlights strategic developments including R&D innovation, digital production techniques, and sustainability-driven material engineering.

Target audiences include construction companies, architectural consultants, PVB film manufacturers, material scientists, and government policy stakeholders. The report also examines how emerging smart technologies and bio-based materials are transforming product lifecycles and performance expectations. Additionally, it addresses niche areas such as solar façade integration and acoustic design applications, providing valuable intelligence for market entrants and established players alike.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Revenue (2024) | USD 1,200.0 Million |

| Market Revenue (2032) | USD 2304.7 Million |

| CAGR (2025–2032) | 8.5% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Eastman Chemical Company, Kuraray Co., Ltd., Sekisui Chemical Co., Ltd., Everlam, DuLite Technologies, Huakai Plastic (Chongqing) Co., Ltd., Zhejiang Decent Plastic Co., Ltd., Chang Chun Group, Saflex Interlayers, Kingboard Chemical Holdings Limited |

| Customization & Pricing | Available on Request (10% Customization is Free) |