Reports

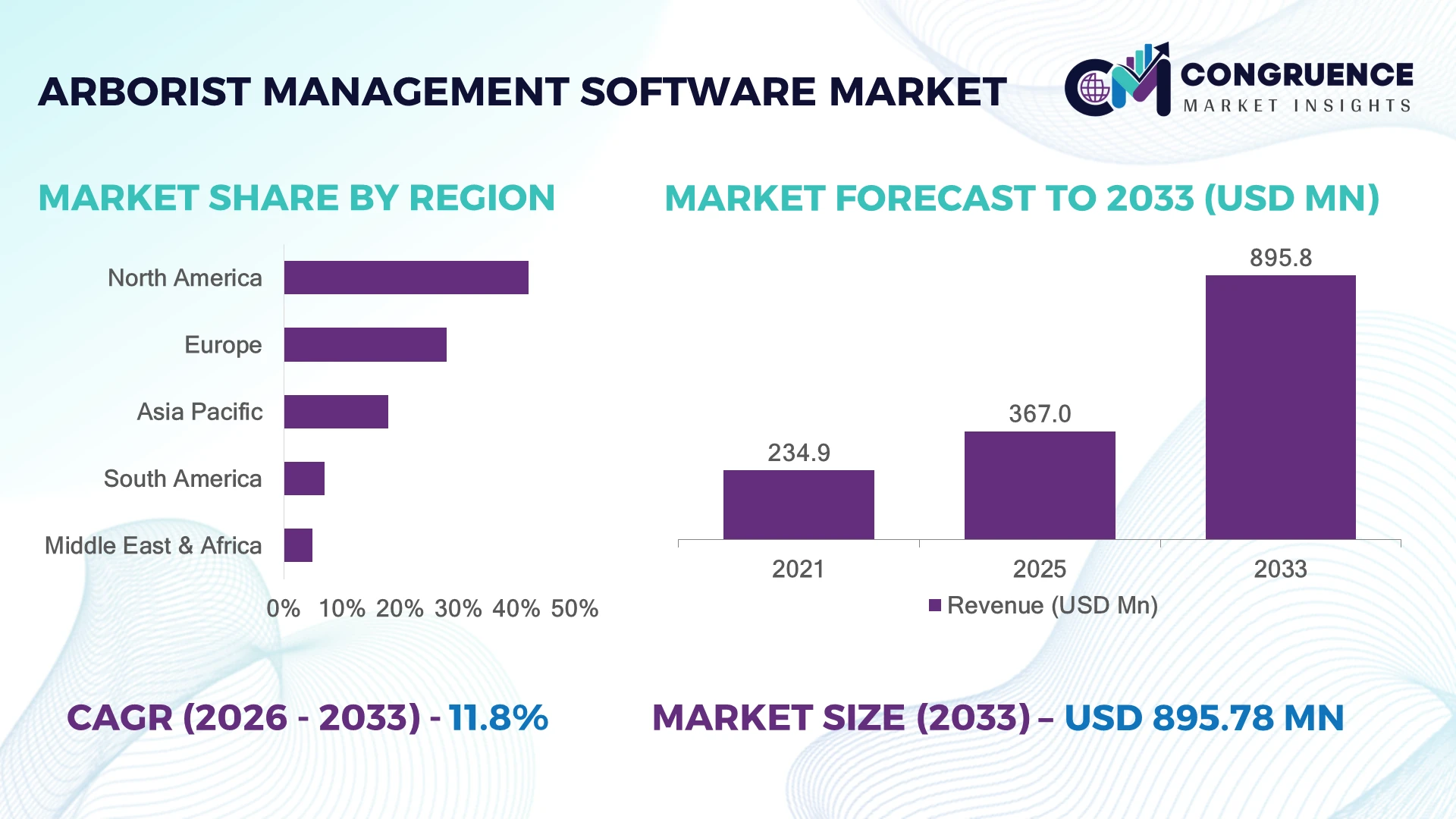

The Global Arborist Management Software Market was valued at USD 367.0 Million in 2025 and is anticipated to reach a value of USD 895.8 Million by 2033 expanding at a CAGR of 11.8% between 2026 and 2033. Growth is driven by AI-enabled tree inventory management, cloud-based field operations, GPS mapping, and increasing adoption of digital platforms for vegetation maintenance and urban forestry management.

The United States dominates the global arborist management software landscape, accounting for approximately 42% market adoption, supported by extensive municipal tree-care programs, utility vegetation management investments, and advanced landscaping service networks. North American companies are integrating cloud platforms across more than 60% of professional arborist operations, while European markets emphasize compliance-driven digital monitoring under urban sustainability initiatives.

Strategic adoption in developed markets indicates that software providers focusing on automation, analytics, and regulatory compliance will gain stronger competitive positioning.

Market Size & Growth: USD 367.0 Million market value in 2025 reaching USD 895.8 Million by 2033 at 11.8% CAGR, driven by cloud adoption and digital transformation in tree-care operations.

Top Growth Drivers: Cloud platforms (65% adoption), AI analytics (45% implementation growth), and GPS-based asset tracking (50% usage expansion) are accelerating market development.

Short-Term Forecast: By 2028, arborist businesses using digital management tools achieve 25% faster scheduling and 20% lower administrative workload.

Emerging Technologies: AI-based risk assessment, automated work-order systems, IoT-enabled monitoring, and predictive tree health analytics are reshaping operations.

Regional Leaders: North America reaches USD 380 Million with advanced municipal adoption; Europe reaches USD 260 Million with compliance-focused platforms; Asia Pacific reaches USD 170 Million through smart-city expansion.

Consumer/End-User Trends: More than 55% of professional arborist companies prioritize mobile-enabled software for field workforce coordination and reporting.

Pilot/Case Example: In 2024, digital urban forestry management programs improved inspection efficiency by 30% through automated mapping and reporting workflows.

Competitive Landscape: Leading providers hold approximately 35% combined market influence, with key players including ArborNote, SingleOps, Jobber, Arborgold, and TreeKeeper.

Regulatory & ESG Impact: Urban sustainability regulations increase digital tree inventory adoption by over 40% among municipalities implementing environmental monitoring programs.

Investment & Funding: More than USD 100 Million has been directed toward landscaping technology platforms, partnerships, and software expansion initiatives.

Innovation & Future Outlook: Next-generation platforms combine AI forecasting, automation, and real-time field intelligence, creating a shift toward data-driven arborist management ecosystems.

The Arborist Management Software Market is gaining traction as tree-care companies increasingly prioritize operational visibility, workforce optimization, and compliance management. Demand is rising for cloud-based scheduling, digital inspections, and automated reporting tools, with more than 50% of service providers adopting mobile workflows to improve field productivity. Recent innovations include AI-assisted risk evaluation, integrated customer management systems, and real-time asset tracking. The transition toward smart-city infrastructure and stricter vegetation management standards is accelerating software adoption across commercial and municipal applications.

The Arborist Management Software Market is becoming strategically important as tree-care companies, municipalities, and utility operators move from manual recordkeeping toward connected digital ecosystems. Rising urban forestry investments, infrastructure modernization programs, and regulatory requirements for vegetation monitoring are accelerating adoption of specialized management platforms.

Modern cloud-based arborist software improves operational efficiency by reducing manual scheduling and reporting tasks by nearly 30% compared with traditional spreadsheet-based systems. AI-powered platforms provide predictive maintenance insights, while legacy systems rely primarily on reactive workflows. North America leads in deployment scale due to established landscaping networks and utility vegetation programs, whereas Asia Pacific is advancing through smart-city initiatives and digital infrastructure expansion.

Companies are increasingly deploying mobile workforce applications, automated customer management tools, and GIS-based tree inventory systems to improve service delivery. Utility providers are partnering with technology vendors to enhance vegetation risk monitoring and compliance reporting. Over the next few years, adoption will accelerate as businesses prioritize automation, data visibility, and operational resilience. Organizations investing in integrated software ecosystems will strengthen competitive positioning through improved productivity, faster decision-making, and scalable service capabilities.

The shift from manual tree-care management to cloud-based platforms is accelerating adoption among arborist firms, municipalities, and utility contractors. More than 60% of professional arborist businesses are integrating digital scheduling, GPS mapping, and mobile workforce tools to improve field visibility. In the United States, increasing urban forestry programs and utility vegetation management requirements are driving demand for automated asset tracking systems. Companies are responding through software upgrades, AI-based risk assessment features, and partnerships with landscaping service providers. The key operational advantage is improved crew utilization and faster decision-making through centralized data management.

High implementation costs and fragmented technology infrastructure remain major limitations for smaller arborist businesses. Around 35% of small operators continue relying on spreadsheets or basic tools due to budget constraints and limited technical resources. In markets such as Canada and Australia, integration challenges between GIS platforms, customer management systems, and existing field applications affect deployment efficiency. Companies face slower scalability and higher onboarding expenses when migrating legacy workflows. Software providers are reducing these barriers through modular subscription models, simplified integrations, and localized support services to improve accessibility across diverse business sizes.

The integration of artificial intelligence, predictive analytics, and IoT-based monitoring is creating new opportunities for advanced arborist management solutions. AI-driven inspection tools can improve tree-risk identification accuracy by more than 40% compared with manual assessments, while automated workflows reduce administrative workloads by nearly 25%. Countries including the United States and Germany are investing in smart urban forestry initiatives that require real-time environmental data management. Companies are expanding R&D efforts, forming technology partnerships, and developing ecosystem-based platforms combining GIS, sensors, and analytics. The emerging opportunity lies in transforming arborist software from operational tools into predictive environmental management systems.

Increasing dependence on connected software platforms introduces cybersecurity concerns and workforce adaptation challenges. Approximately 45% of organizations using cloud-based field management systems identify data protection and system integration as critical operational priorities. In the United Kingdom and United States, expanding digital infrastructure requires stronger cybersecurity controls for municipal and utility-linked vegetation databases. Limited availability of digitally skilled arborists also slows consistent platform adoption across smaller companies. Software providers must invest in secure cloud architecture, workforce training programs, and interoperability standards to maintain long-term competitiveness. Addressing these execution challenges will determine the reliability and scalability of future arborist technology ecosystems.

AI-Powered Tree Analytics Growth Arborist companies are increasingly adopting AI-based inspection and predictive analytics tools, with digital assessment usage expanding by nearly 35% among professional service providers. Automated risk scoring and image-based tree diagnostics are reducing manual evaluation time by approximately 25%. Companies are integrating AI features into existing platforms to improve safety planning, optimize crew allocation, and support data-driven maintenance decisions.

Mobile Workforce Optimization Shift Field mobility is becoming a core operational priority, with more than 60% of arborist firms deploying mobile applications for scheduling, work orders, and real-time reporting. GPS-enabled workflows are improving route efficiency by around 20% while reducing communication delays between field teams and managers. Software providers are responding through mobile-first platforms, enterprise integrations, and expanded cloud capabilities to support distributed operations.

Smart Urban Forestry Adoption Municipal tree-management programs are transitioning toward digital inventories as cities increase sustainability monitoring requirements. More than 45% of urban forestry departments are prioritizing digital asset tracking, driven by climate resilience initiatives and infrastructure planning needs. Companies are developing GIS-integrated solutions that combine tree databases, maintenance records, and compliance reporting to support smarter city management.

Integrated Business Platform Expansion Arborist software providers are moving beyond basic scheduling tools toward integrated business ecosystems combining customer management, billing, inventory, and analytics. Nearly 50% of growing arborist businesses prefer unified platforms to improve operational visibility. Partnerships between software developers and landscaping service networks are increasing as companies seek scalable solutions that reduce administrative workload and strengthen service efficiency.

Cloud-based arborist management software represents the leading type due to scalability, remote accessibility, and lower infrastructure requirements for small and large service providers. Cloud platforms account for nearly 65% of deployments as companies prioritize centralized data access, automated updates, and mobile workforce coordination. Traditional desktop-based systems remain relevant among established businesses requiring customized workflows but are gradually losing adoption momentum due to limited flexibility and integration constraints. Mobile-enabled cloud solutions are emerging as the fastest-growing type, supported by increasing demand for real-time field operations and GPS-based asset management. Adoption of mobile workflows has increased by approximately 40% as arborist companies seek faster inspections, digital reporting, and improved crew productivity. Software providers are investing in modular platforms, API integrations, and AI-enabled features to strengthen competitiveness. The market shift indicates that future investment priorities are moving toward connected, data-driven arborist ecosystems rather than standalone management tools.

Tree care management is the dominant application segment as arborist companies rely on software platforms for scheduling, inspections, work tracking, and customer coordination. This application represents more than 55% of total usage among professional arborist service providers due to its direct impact on daily operational efficiency. Emergency response planning, pruning management, and tree health monitoring are becoming increasingly digitized as companies improve service reliability. Urban forestry management is the fastest-growing application area, supported by smart-city initiatives, environmental compliance programs, and increasing municipal investment in digital tree inventories. Adoption in this segment is rising by nearly 35% as cities require accurate asset records and predictive maintenance capabilities. Utility vegetation management and commercial landscaping applications are also expanding through automated reporting and workforce optimization tools. Companies are adapting by developing specialized modules for municipalities, utilities, and large landscaping enterprises to address diverse operational requirements.

Commercial arborist companies represent the leading end-user segment due to higher service volumes, frequent field operations, and stronger demand for scheduling and customer management solutions. More than 60% of professional tree-care businesses utilize digital platforms to manage workforce activities, customer records, and operational reporting. Large landscaping firms are increasingly adopting integrated systems to improve resource planning and maintain service consistency across multiple locations. Municipal authorities and utility providers are emerging as the fastest-growing end-user groups as public infrastructure management becomes more data-driven. Adoption among government and utility organizations is increasing by approximately 40% due to requirements for vegetation monitoring, safety compliance, and infrastructure protection. Residential arborist services continue expanding through simplified cloud tools that improve customer engagement and booking efficiency. Software companies are targeting these segments through customized dashboards, enterprise partnerships, and flexible subscription models. Future demand is shifting toward organizations requiring scalable platforms capable of combining field operations, environmental data, and regulatory reporting.

North America accounted for the largest market share at 42% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of13.2% between 2026 and 2033.

North America held the dominant position in the arborist management software market with approximately 42% market share in 2025, supported by strong adoption among commercial arborists, utility vegetation management companies, and municipal forestry departments. The United States represents the largest deployment base, with more than 60% of professional arborist firms using digital scheduling, GIS mapping, or mobile workforce solutions. Increasing urban tree management initiatives and utility safety requirements are accelerating enterprise software adoption. Companies are expanding through cloud integrations, AI-based inspection tools, and partnerships with landscaping networks to improve operational efficiency and workforce coordination.

United States Market Outlook: The United States remains the primary technology hub for arborist software adoption due to its large landscaping industry, utility vegetation programs, and municipal forestry investments. More than 65% of large arborist service providers are prioritizing cloud-enabled platforms for field coordination, customer management, and compliance reporting. Technology providers are focusing on AI analytics and enterprise integrations to address complex multi-location operations.

Europe accounted for approximately 28% of the global arborist management software market in 2025, driven by urban sustainability programs, environmental monitoring requirements, and increasing digital transformation among municipal forestry organizations. Countries such as Germany, the United Kingdom, and France are adopting GIS-based tree inventory systems to improve urban planning and maintenance efficiency. More than 45% of European municipalities with structured tree management programs are moving toward digital asset tracking solutions. Companies are strengthening regional presence through partnerships with environmental technology providers and customized compliance-focused platforms supporting climate resilience initiatives.

Germany Market Outlook: Germany represents the leading European market due to strong environmental governance, advanced municipal infrastructure, and technology adoption across public services. Approximately 50% of larger urban forestry operations are incorporating digital monitoring tools to improve planning accuracy and documentation. Software providers are targeting German municipalities with integrated GIS, analytics, and sustainability reporting capabilities.

Asia-Pacific represented around 18% of the global arborist management software market in 2025 and is emerging as the fastest-expanding market due to smart-city development, urban landscaping projects, and increasing digital adoption among service providers. Countries including China, Japan, Australia, and India are investing in technology-enabled urban infrastructure management. Digital workflow adoption among growing landscaping enterprises has increased by nearly 40%, driven by mobile workforce tools and automated reporting requirements. Companies are expanding through localized platforms, cloud deployment models, and partnerships with urban development organizations to address rising demand for efficient vegetation management.

China Market Outlook: China is becoming a strategically important market through smart-city programs, large-scale urban greening initiatives, and digital infrastructure development. More than 30% of major metropolitan landscaping projects are incorporating technology-based monitoring and management practices. Software companies are focusing on scalable platforms that support large municipal networks and automated maintenance planning.

South America accounted for nearly 7% of the global arborist management software market in 2025, supported by growing commercial landscaping services, urban beautification projects, and increasing adoption of digital business management tools. Brazil and Argentina represent key demand centers where arborist companies are transitioning from manual scheduling systems toward cloud-based platforms. Approximately 35% of medium and large landscaping businesses are adopting digital tools for customer management and field operations. Companies are improving market penetration through affordable subscription models, mobile applications, and partnerships with local service providers to overcome infrastructure limitations.

Brazil Market Outlook: Brazil leads the South American market due to its large landscaping sector, expanding urban infrastructure projects, and increasing professional arborist services. Around 40% of established landscaping companies are adopting digital scheduling and customer management solutions. Technology providers are targeting Brazil through flexible cloud platforms designed for diverse operational environments.

Middle East & Africa represented approximately 5% of the global arborist management software market in 2025, with demand concentrated in Gulf countries, South Africa, and major urban development projects. Large-scale landscaping initiatives, smart-city investments, and water-efficient green infrastructure programs are encouraging adoption of digital vegetation management systems. The United Arab Emirates and Saudi Arabia are increasing technology integration within urban maintenance operations, with more than 30% of large landscaping contractors adopting digital workflow solutions. Companies are entering the market through government partnerships, localized support services, and platforms designed for large-scale landscape management.

United Arab Emirates Market Outlook: The United Arab Emirates is the most advanced market in the region due to smart-city initiatives, high-value landscaping projects, and technology-focused urban planning. More than 50% of major landscaping contractors in Dubai and Abu Dhabi utilize digital project management tools to improve operational coordination. Software providers are positioning solutions around automation, asset tracking, and sustainable landscape management.

The Arborist Management Software Market features competition between global field-service platforms and specialized arboriculture technology providers. Leading players such as SingleOps, Arborgold, Jobber, ArborNote, and ArboStar compete through automation depth, industry customization, integrations, and pricing flexibility. The top five players collectively account for approximately 45% of market influence, with competition concentrated around cloud capability, mobile workflows, GIS mapping, and customer management features. Technology-focused providers differentiate through AI analytics and ecosystem integrations, while cost-focused platforms target small and medium arborist businesses. Around 60% of buyers prioritize workflow automation, while nearly 50% seek advanced reporting and integration capabilities. Companies are expanding through partnerships, product upgrades, and vertical-specific solutions. The competitive shift is moving toward AI-enabled tree intelligence, real-time data management, and connected field operations. High entry barriers include specialized industry knowledge, customer retention, and integration complexity. Winning requires superior automation, scalable platforms, and deep arborist workflow understanding.

Arborgold

Jobber

ArborNote

ArboStar

Treezi

ServiceTitan

LMN

Aspire Software

WorkWave

FieldRoutes

GoCanvas

Cloud computing, mobile workforce applications, and GIS-based mapping are becoming foundational technologies in arborist management software. Cloud platforms enable centralized data access, automated updates, and remote collaboration, with adoption among professional arborist businesses exceeding 60%. Compared with legacy desktop systems, cloud solutions improve workflow accessibility by nearly 30% and reduce administrative delays through real-time synchronization. Companies benefiting most are multi-location service providers requiring scalable operations.

Artificial intelligence and predictive analytics are introducing advanced tree-risk assessment, automated scheduling, and maintenance forecasting capabilities. AI-assisted inspections improve evaluation speed by approximately 35% compared with manual assessments, helping companies optimize workforce deployment and reduce operational inefficiencies. Integration with IoT sensors and digital tree inventories is expanding as municipalities and utilities demand more accurate asset monitoring.

Between 2026 and 2028, competitive advantage will increasingly depend on intelligent automation, API connectivity, and ecosystem integration. Providers investing in AI-driven recommendations, mobile-first platforms, and automated compliance reporting will strengthen market positioning. The transition from basic scheduling software to predictive arborist intelligence platforms is reshaping how companies manage resources, improve service quality, and differentiate offerings.

April 2025 SingleOps expanded its Tree Inventory functionality with enhanced tree mapping and proposal workflows, enabling arborists to document individual trees directly from field locations. The update improved inventory visibility and strengthened customer management capabilities for tree-care businesses. Source: www.docs.singleops.com

July 2025 SingleOps introduced client-facing Tree Map capabilities, allowing customers to view mapped tree information within proposals. The enhancement improved transparency in service communication and expanded digital engagement between arborists and property owners. Source: www.docs.singleops.com

2025 ArborNote strengthened its technology ecosystem through expanded integrations with QuickBooks, HubSpot, Zapier, and open API connectivity. The platform improved workflow automation by connecting financial, customer relationship, and operational systems. Source: www.arbornote.com

October 2025 SingleOps enhanced Tree Inventory capabilities by adding individual tree photo management, improving documentation accuracy for field teams. The update supported better tracking of tree health conditions and strengthened operational record management.

The Arborist Management Software Market Report covers comprehensive analysis across software types, applications, and end-user categories, including cloud-based platforms, mobile solutions, tree inventory management, scheduling systems, commercial arborists, municipalities, utilities, and landscaping enterprises. The report evaluates adoption patterns across North America, Europe, Asia-Pacific, South America, and Middle East & Africa with emphasis on digital transformation trends.

The study analyzes emerging technologies such as AI-based tree assessment, GIS mapping, automation tools, mobile workforce platforms, and integrated business management systems. It highlights competitive positioning, deployment strategies, partnership opportunities, and evolving customer requirements. The report supports investment planning, expansion decisions, product development strategies, and competitive benchmarking by identifying high-potential application areas and technology-driven market shifts between 2026 and 2033.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 367.0 Million |

| Market Revenue (2033) | USD 895.8 Million |

| CAGR (2026–2033) | 11.8% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Companies Profiled | SingleOps; Arborgold; Jobber; ArborNote; ArboStar; Treezi; ServiceTitan; LMN; Aspire Software; WorkWave; FieldRoutes; GoCanvas |

| Customization & Pricing | Available on Request (10% Customization Free) |