Reports

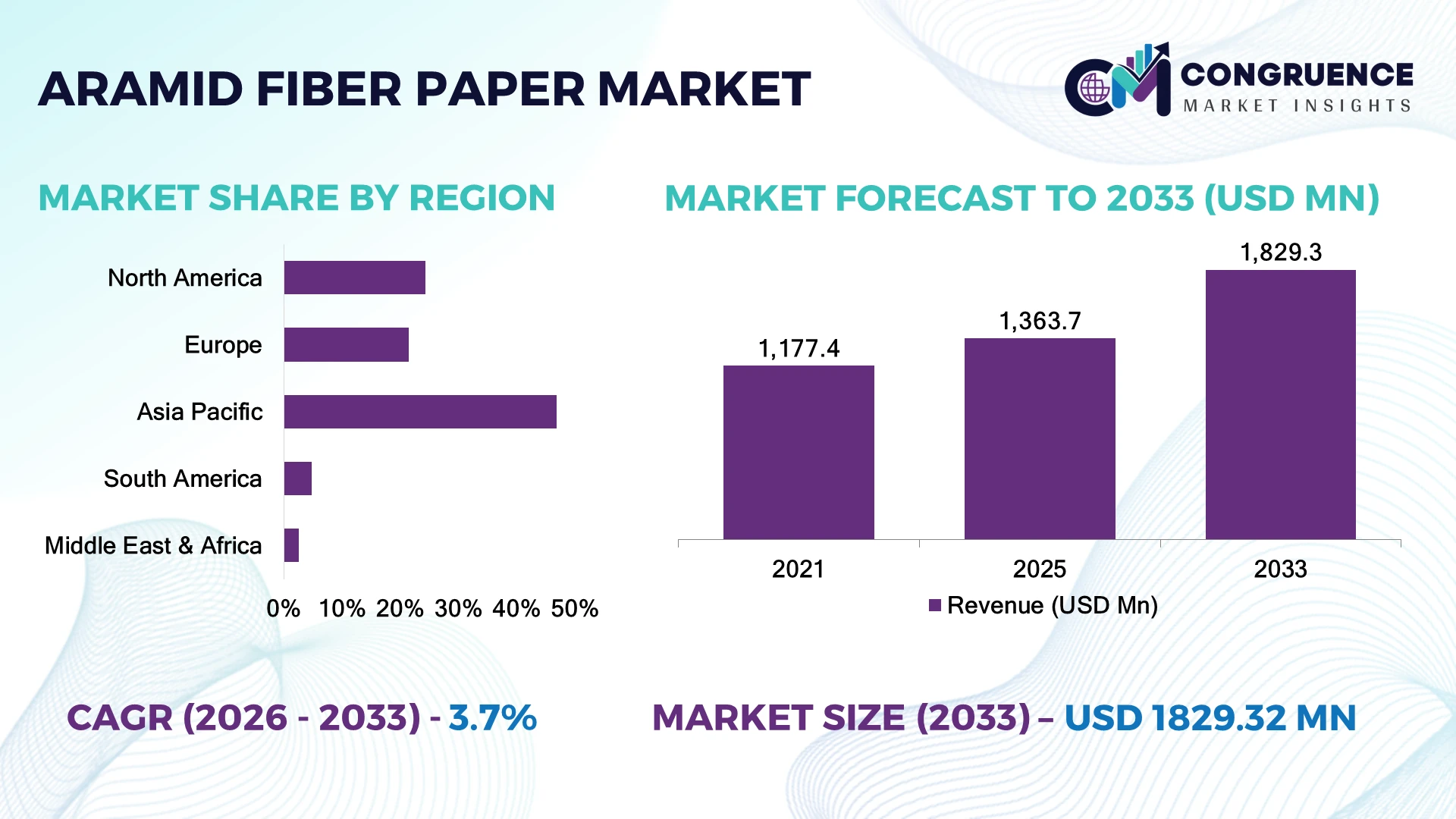

The Global Aramid Fiber Paper Market was valued at USD 1,363.7 Million in 2025 and is anticipated to reach a value of USD 1,829.3 Million by 2033 expanding at a CAGR of 3.74% between 2026 and 2033. Rising electrification across power infrastructure and aerospace insulation systems is accelerating the adoption of high-temperature, lightweight aramid fiber paper in mission-critical applications.

China leads the global market with approximately 38% production capacity, supported by expanding electrical equipment manufacturing, aerospace programs, and sustained industrial investments exceeding USD 15 billion in advanced materials. In comparison, Germany accounts for nearly 11% of high-performance insulation demand, driven by automotive electrification and precision engineering, while China's production scale remains over three times larger, reinforcing global supply leadership.

The competitive landscape increasingly favors manufacturers investing in localized production, advanced processing technologies, and resilient supply-chain partnerships.

Market Size & Growth: USD 1,363.7 Million in 2025, reaching USD 1,829.3 Million by 2033 at a CAGR of 3.74%, supported by expanding electrical insulation and aerospace applications.

Top Growth Drivers: Electrical infrastructure (+28%), EV component demand (+24%), aerospace insulation adoption (+18%) continue strengthening global market expansion.

Short-Term Forecast: By 2028, manufacturing waste is projected to decline by 12% through automated material processing and quality optimization.

Emerging Technologies: AI-assisted quality inspection, precision fiber calendaring, and advanced resin impregnation improve production consistency and operational efficiency.

Regional Leaders: Asia Pacific (~USD 790 Million), North America (~USD 360 Million), and Europe (~USD 320 Million) benefit from industrial modernization and regional supply-chain expansion.

Consumer/End-User Trends: Nearly 46% of electrical equipment manufacturers prioritize lightweight insulation materials for higher thermal reliability.

Pilot/Case Example: In 2024, an automated insulation paper production project improved material utilization by approximately 15% while reducing process defects.

Competitive Landscape: Top five manufacturers collectively control around 55% of global supply, led by DuPont, Teijin, Yantai Tayho, X-FIPER, and LongPont.

Regulatory & ESG Impact: High-performance insulation materials help improve equipment energy efficiency by nearly 10% while supporting stricter industrial sustainability standards.

Investment & Funding: More than USD 2.4 billion has been directed toward advanced material expansion, localization initiatives, and strategic manufacturing partnerships.

Innovation & Future Outlook: Nanofiber reinforcement, recyclable insulation solutions, and digitally controlled manufacturing are strengthening long-term competitive positioning.

Aramid Fiber Paper Market demand is expanding across transformers, electric motors, aerospace components, and battery insulation systems where thermal stability and dielectric performance remain essential. Manufacturers are introducing enhanced resin-treated grades and precision-engineered lightweight materials, while nearly 35% of new industrial insulation projects emphasize higher operating efficiency. Ongoing regional supply-chain diversification is also encouraging localized production and strategic procurement decisions, setting the stage for broader competitive differentiation.

Aramid fiber paper has become strategically important as industries prioritize electrical reliability, lightweight engineering, and long-life insulation materials across power transmission, aerospace, railways, and electric mobility. Infrastructure modernization and supply-chain restructuring are encouraging manufacturers to establish regional production capabilities, reducing dependence on single-country sourcing while improving delivery resilience for critical industrial sectors.

Modern automated fiber formation and precision calendaring technologies deliver approximately 18% higher production consistency and reduce material waste by nearly 14% compared with conventional manufacturing methods. Asia-Pacific continues to dominate large-scale manufacturing and downstream electrical equipment production, whereas North America and Europe emphasize innovation, premium-grade insulation materials, and aerospace-focused applications. Over the next two to three years, automated inspection systems and digital manufacturing platforms are expected to become standard across major production facilities, improving quality control and operational responsiveness.

A growing number of insulation manufacturers are expanding strategic partnerships with electrical equipment and EV component suppliers to secure long-term procurement agreements and strengthen localized manufacturing networks. The increasing focus on durable, recyclable, and high-performance insulation materials also aligns with evolving industrial sustainability objectives. Companies that combine advanced manufacturing capabilities with resilient regional supply chains will secure stronger competitive positioning and long-term operational advantages in this evolving market.

Accelerating grid modernization, electric mobility expansion, and aerospace electrification are strengthening demand for aramid fiber paper with superior dielectric and thermal resistance. Nearly 48% of newly installed high-voltage equipment now incorporates advanced insulation materials, while over 30% of electric motor manufacturers are replacing conventional cellulose insulation with aramid-based alternatives to extend service life. China's continued investment in ultra-high-voltage transmission networks and domestic electrical manufacturing is reinforcing procurement volumes for premium insulation materials. This structural transition improves equipment reliability, reduces maintenance frequency, and supports higher operating temperatures. Manufacturers are responding through capacity expansion, automated production lines, and strategic partnerships with transformer and electrical equipment producers. A key competitive advantage increasingly depends on supplying customized insulation grades designed for next-generation electrification platforms rather than standardized industrial applications.

Aramid fiber paper production remains constrained by limited availability of specialty para-aramid and meta-aramid fibers, creating persistent procurement and pricing pressure. Raw materials account for nearly 55% of manufacturing costs, while imported specialty fibers represent approximately 40% of procurement requirements for several producers outside China. Periodic logistics disruptions and energy-intensive processing further increase production complexity, limiting pricing flexibility for manufacturers serving cost-sensitive industrial sectors. These conditions reduce margin stability and slow expansion into emerging manufacturing markets. Companies are mitigating exposure through long-term supply agreements, localized sourcing strategies, and greater investment in regional conversion facilities. A growing operational priority is reducing dependence on single-source suppliers while improving inventory resilience through diversified procurement networks.

Next-generation electrical infrastructure, battery systems, and lightweight transportation platforms are creating new commercial opportunities for engineered aramid fiber paper solutions. More than 42% of advanced transformer development programs emphasize higher thermal endurance, while automated manufacturing technologies have improved production efficiency by approximately 16%. Japan and South Korea continue expanding research into ultra-thin insulation materials supporting compact electrical equipment and next-generation mobility applications. Manufacturers are increasing investment in nanofiber reinforcement, recyclable composite structures, and precision resin impregnation technologies to enhance durability without increasing material weight. An emerging strategic opportunity lies in customized insulation engineered for high-frequency power electronics, enabling suppliers to secure premium industrial contracts beyond conventional transformer applications.

Maintaining uniform product quality across expanding manufacturing capacity remains one of the industry's most significant long-term execution challenges. High-performance insulation applications require production tolerances exceeding 98% consistency, while nearly 22% of production optimization efforts focus on minimizing microscopic fiber variation that affects dielectric reliability. Germany's industrial quality standards continue raising certification expectations for electrical insulation components, increasing validation requirements for global suppliers. Scaling automated production without compromising thermal stability or mechanical strength requires continuous investment in digital inspection systems, advanced process control, and workforce expertise. Companies that successfully integrate intelligent manufacturing, predictive quality monitoring, and standardized global certification processes will strengthen operational resilience and secure long-term competitiveness in high-value industrial markets.

Advanced Manufacturing Automation Production facilities are increasingly integrating AI-enabled inspection systems and automated calendaring processes, improving dimensional consistency by nearly 18% while reducing material waste by approximately 14%. Manufacturers in China and Japan are restructuring production workflows to address labor constraints and tighter quality requirements. These upgrades shorten production cycles, improve throughput, and enable suppliers to deliver customized insulation grades for high-performance electrical equipment with greater operational efficiency.

Localized Supply Network Expansion Companies are shifting procurement and converting operations closer to major industrial hubs as global supply-chain diversification continues. Around 35% of manufacturers have expanded regional sourcing programs, while localized inventory strategies have reduced average delivery lead times by nearly 20%. Electrical equipment producers are strengthening long-term procurement partnerships to improve supply continuity, allowing manufacturers to reduce logistics exposure and maintain stable production despite changing trade conditions.

Lightweight Electrical Material Adoption Demand for thinner and lighter insulation materials continues rising across transformers, electric motors, and mobility systems. Nearly 42% of new electrical equipment designs now prioritize lightweight insulation architectures, while advanced resin-treated aramid paper improves thermal endurance by roughly 16%. Producers are expanding specialized product portfolios to meet evolving engineering specifications and strengthen long-term customer integration across premium industrial applications.

Digital Quality Assurance Integration Manufacturers are deploying predictive analytics, machine vision, and digital traceability platforms to strengthen process reliability. Automated quality monitoring has reduced inspection time by nearly 25%, while defect detection accuracy has improved by approximately 19%. Germany-based industrial customers increasingly require digital production records, encouraging suppliers to modernize manufacturing operations and enhance certification readiness for mission-critical electrical insulation applications.

Meta-Aramid Fiber Paper remains the leading segment, accounting for approximately 64% of global demand due to its superior electrical insulation, flame resistance, and cost-effective performance across transformers, motors, and industrial equipment. Its broad compatibility with high-temperature electrical systems and established manufacturing ecosystem continue supporting large-scale deployment. Para-Aramid Fiber Paper represents the fastest-growing segment as aerospace, defense, and lightweight structural applications increasingly require higher mechanical strength and improved durability. Growing investment in premium engineered insulation materials is accelerating commercial adoption of para-aramid grades across specialized industrial sectors. Manufacturers continue balancing mature demand for meta-aramid products with expanding portfolios of para-aramid solutions designed for advanced mobility and aerospace applications. Nearly 37% of new product development programs now target lightweight, high-strength insulation grades, while over 28% of premium electrical equipment specifications include enhanced-performance aramid materials. Companies are expanding production capacity, investing in material engineering, and strengthening collaborations with OEMs to address shifting industrial requirements and improve product differentiation.

Electrical Insulation remains the dominant application, representing approximately 58% of overall demand because of widespread deployment in transformers, generators, switchgear, and electric motors operating under elevated thermal conditions. High dielectric performance and long operational life continue supporting replacement of conventional insulation materials across critical infrastructure. Battery Insulation is emerging as the fastest-growing application, driven by increasing electrification programs and next-generation energy storage systems requiring lightweight and thermally stable insulation components. Honeycomb Core applications maintain strategic importance within aerospace structures by reducing component weight while preserving mechanical integrity. Aerospace applications continue expanding as manufacturers adopt advanced insulation materials capable of operating under demanding environmental conditions. Nearly 34% of newly developed electrical equipment platforms incorporate upgraded insulation technologies, while around 29% of battery system developers prioritize enhanced thermal protection. Manufacturers are responding through specialized product development, automated production processes, and collaborative engineering partnerships that align products with evolving industrial performance requirements.

Electrical & Electronics remains the largest end-user segment with approximately 52% market share, supported by extensive deployment across transformers, motors, switchgear, power distribution equipment, and industrial electrical systems. Continuous infrastructure modernization and increasing equipment replacement cycles sustain demand for premium insulation materials with superior thermal stability. Aerospace & Defense represents the fastest-growing end-user group as aircraft electrification, lightweight engineering, and high-performance insulation requirements continue expanding across advanced manufacturing programs. Automotive manufacturers are steadily increasing utilization of aramid fiber paper within electric propulsion systems and battery assemblies, while Industrial users continue adopting premium insulation materials for high-temperature processing equipment and rotating machinery. Nearly 31% of electrical equipment manufacturers have expanded procurement of advanced insulation materials during recent modernization initiatives, while over 26% of aerospace component suppliers have introduced higher-performance insulation specifications. Companies are strengthening customer-specific product development, technical partnerships, and localized manufacturing capabilities to improve responsiveness across diverse industrial applications.

Asia-Pacific accounted for the largest market share at 46.8% in 2025 however, South America is expected to register the fastest growth, expanding at a CAGR of 4.38% between 2026 and 2033.

North America accounted for approximately 24.3% of the global market in 2025, supported by modernization of aging power infrastructure, increasing transformer replacement programs, and expanding electric mobility manufacturing. Utilities and OEMs continue specifying high-temperature insulation materials capable of extending equipment service life while reducing maintenance requirements. The United States and Canada are accelerating investments in transmission reliability and industrial electrification, increasing procurement of advanced electrical insulation products. More than 32% of newly commissioned high-voltage transformer projects across the region now utilize premium insulation systems. Manufacturers are expanding local converting operations, strengthening OEM partnerships, and integrating automated quality control to improve supply responsiveness and product consistency for mission-critical electrical applications.

United States Market Outlook: The United States remains the largest national market due to its extensive electrical equipment manufacturing base, aerospace production, and ongoing transmission infrastructure upgrades. More than 60% of regional demand originates from domestic industrial and utility applications, while transformer modernization initiatives continue supporting procurement of advanced insulation materials. Manufacturers are investing in localized production, collaborative engineering programs, and automation technologies to improve delivery reliability and support increasingly stringent performance specifications.

Europe represented approximately 21.5% of the global market in 2025, driven by industrial electrification, high-performance manufacturing, and stringent equipment efficiency standards. Electrical equipment manufacturers continue replacing conventional insulation materials with advanced aramid fiber paper to improve operational durability and thermal stability. Modernization of transmission networks and expansion of rail electrification projects are reinforcing demand across industrial sectors. Nearly 29% of new premium transformer installations specify enhanced insulation systems designed for extended operating performance. Companies are strengthening regional production capabilities, investing in sustainable manufacturing practices, and expanding technical collaboration with electrical equipment suppliers to improve long-term competitiveness.

Germany Market Outlook: Germany leads the European market through its advanced electrical engineering sector, industrial automation expertise, and globally competitive machinery manufacturing ecosystem. Approximately 35% of Western Europe's premium transformer manufacturing capacity is concentrated in Germany, supporting sustained consumption of high-performance insulation materials. Domestic producers continue integrating automated production technologies and advanced quality assurance systems to strengthen export competitiveness and industrial reliability.

Asia-Pacific dominated the global market with approximately 46.8% share in 2025, supported by large-scale manufacturing, expanding electrical infrastructure, and integrated supply chains for advanced materials. China, Japan, and South Korea continue increasing production of transformers, motors, batteries, and industrial electrical equipment requiring premium insulation solutions. More than 55% of global aramid fiber paper manufacturing capacity is concentrated within the region, providing strong export competitiveness and stable industrial supply. Manufacturers are expanding production facilities, adopting intelligent manufacturing systems, and strengthening downstream partnerships to improve operational efficiency and product specialization across multiple industrial applications.

China Market Outlook: China remains the industry's largest manufacturing hub due to its integrated aramid fiber supply chain, high-voltage transmission investments, and extensive electrical equipment production. Approximately 38% of global aramid fiber paper production capacity is located in China, supported by continuous industrial modernization and domestic infrastructure development. Local manufacturers are investing in higher-value specialty grades, automation platforms, and export-oriented production strategies to strengthen international market positioning.

South America accounted for approximately 4.8% of the global market in 2025 as investments in electrical infrastructure, mining operations, and industrial modernization increased demand for durable insulation materials. Utilities continue upgrading aging transmission assets, while industrial facilities seek higher-performance insulation capable of improving equipment reliability under demanding operating conditions. More than 18% of recently approved power infrastructure projects include modernization of electrical insulation systems. Manufacturers are strengthening regional distribution partnerships and localized inventory networks to reduce delivery times despite logistical constraints. Continued industrial expansion presents attractive opportunities, although manufacturing capacity remains comparatively limited.

Brazil Market Outlook: Brazil leads regional demand through its large electricity network, expanding industrial manufacturing sector, and sustained investments in transmission infrastructure. More than half of South America's transformer manufacturing activity is concentrated in Brazil, creating consistent demand for advanced insulation materials. Companies are expanding technical service capabilities, strengthening local distribution channels, and collaborating with electrical equipment manufacturers to support infrastructure modernization initiatives.

Middle East & Africa represented approximately 2.6% of the global market in 2025, supported by expanding transmission infrastructure, industrial diversification, and modernization of energy networks. Governments and utilities continue investing in reliable electrical equipment capable of operating under demanding climatic conditions, increasing the requirement for thermally stable insulation materials. Approximately 21% of recently announced grid modernization projects across key Gulf economies incorporate advanced transformer technologies. Manufacturers are establishing regional partnerships, expanding technical support capabilities, and improving supply-chain responsiveness to meet infrastructure deployment schedules while enhancing operational reliability.

Saudi Arabia Market Outlook: Saudi Arabia represents the region's most strategically significant market due to extensive grid expansion, industrial diversification initiatives, and large-scale utility investments. National infrastructure projects continue increasing procurement of premium electrical equipment requiring advanced insulation systems. Manufacturers are strengthening local partnerships, expanding technical support operations, and aligning product offerings with utility performance standards to improve long-term participation in the country's evolving power infrastructure ecosystem.

The competitive landscape is led by DuPont, Teijin Aramid, Yantai Tayho Advanced Materials, Shenzhen LongPont, and X-FIPER New Material, with global technology leaders competing directly against cost-efficient Chinese manufacturers for transformer, aerospace, and industrial insulation contracts. The top five companies collectively account for approximately 68% of the global market, creating a moderately consolidated structure. Competition centers on material performance, thermal endurance, production scalability, and supply reliability rather than pricing alone. Nearly 42% of procurement decisions prioritize customized insulation solutions, while over 35% of OEM contracts require localized technical support and rapid delivery capabilities. Companies are expanding specialty production lines, strengthening long-term OEM partnerships, investing in automated quality inspection, and increasing vertical integration to secure raw material availability. The competitive shift increasingly favors advanced manufacturing and supply-chain control over conventional cost leadership. High qualification requirements, proprietary processing technologies, and certification standards remain significant entry barriers. Sustainable competitive advantage depends on innovation, manufacturing precision, reliable supply networks, and application-specific engineering expertise.

Teijin Aramid

Yantai Tayho Advanced Materials

Shenzhen LongPont New Materials

X-FIPER New Material

SRO Aramid (Jiangsu)

Aramid HPM

ISOVOLTA AG

Weidmann Electrical Technology

Elinar (UK)

LongPont Group

Metastar Special Paper

Manufacturers are rapidly transitioning from conventional fiber processing to digitally controlled production systems featuring AI-assisted inspection, automated calendaring, and precision resin impregnation. These technologies improve dimensional consistency by nearly 18% while reducing production waste by approximately 14%. Around 46% of premium manufacturing facilities now utilize machine-vision inspection to maintain dielectric performance and process repeatability. The result is greater manufacturing efficiency, improved product reliability, and faster qualification for electrical and aerospace applications.

Emerging technologies include nanofiber reinforcement, ultra-thin aramid paper structures, recyclable fiber processing, and digital process twins for production optimization. Compared with conventional manufacturing, next-generation fiber engineering increases thermal endurance by approximately 20% while reducing material thickness by nearly 15% without compromising mechanical strength. Companies with integrated R&D capabilities and advanced automation benefit from shorter development cycles, stronger OEM collaboration, and greater product differentiation in specialized insulation markets.

Between 2026 and 2028, intelligent manufacturing platforms, predictive quality analytics, and fiber-to-fiber recycling technologies are expected to become mainstream across leading production facilities. Deployment of connected manufacturing systems is projected to exceed 60% among premium suppliers, improving traceability, certification readiness, and operational responsiveness. Companies investing early in digital manufacturing, sustainable material technologies, and customized engineering capabilities will strengthen competitive positioning while supporting increasingly demanding industrial performance requirements.

November 2024 – Teijin Aramid announced a major organizational restructuring to improve competitiveness amid changing aramid market conditions. The company plans to reduce its workforce by approximately 15% while optimizing manufacturing, streamlining operations, and focusing investments on higher-growth specialty applications, strengthening long-term operational efficiency. Source: www.teijinaramid.com

August 2025 – DuPont signed a definitive agreement to divest its Kevlar® and Nomex® aramids business to Arclin in a transaction valued at approximately USD 1.8 billion. The move enables DuPont to streamline its portfolio while allowing the aramids business to pursue dedicated growth under specialized ownership. Source: www.dupont.com

August 2025 – Teijin Limited announced the transfer of its 50% ownership in DuPont Teijin Advanced Papers (Japan) and DuPont Teijin Advanced Papers (Asia) to DuPont following DuPont's decision to exit the aramid paper joint ventures. The transaction supports Teijin's portfolio optimization and strategic resource reallocation toward priority growth businesses. Source: www.teijin.com

June 2025 – Teijin Aramid published its 2024 Sustainability Report, confirming that its Twaron® production process achieved ISCC PLUS certification, strengthening circular manufacturing and certified sustainable raw-material sourcing across its aramid production network. The certification enhances customer confidence in environmentally responsible high-performance material supply.

This report provides comprehensive analysis of the global Aramid Fiber Paper Market across Meta-Aramid Fiber Paper and Para-Aramid Fiber Paper, covering applications including Electrical Insulation, Honeycomb Core, Aerospace, Battery Insulation, and related industrial uses. It evaluates demand across Electrical & Electronics, Aerospace & Defense, Automotive, Industrial, and other key end-user sectors while examining market performance across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. More than 65% of the assessment focuses on operational demand patterns, technology adoption, manufacturing capabilities, and competitive positioning.

The report further examines advanced manufacturing technologies, digital quality control, automation, lightweight material innovation, and sustainable production strategies shaping future industry development. It provides strategic benchmarking of leading companies, regional deployment trends, supply-chain developments, and evolving procurement priorities. The analysis supports investment evaluation, market entry planning, product portfolio optimization, competitive intelligence, partnership strategies, and long-term business expansion decisions throughout the 2026–2033 assessment period.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 1,363.7 Million |

| Market Revenue (2033) | USD 1,829.3 Million |

| CAGR (2026–2033) | 3.74% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Companies Profiled | DuPont; Teijin Aramid; Yantai Tayho Advanced Materials; Shenzhen LongPont New Materials; X-FIPER New Material; SRO Aramid (Jiangsu); Aramid HPM; ISOVOLTA AG; Weidmann Electrical Technology; Elinar (UK); LongPont Group; Metastar Special Paper |

| Customization & Pricing | Available on Request (10% Customization Free) |