Reports

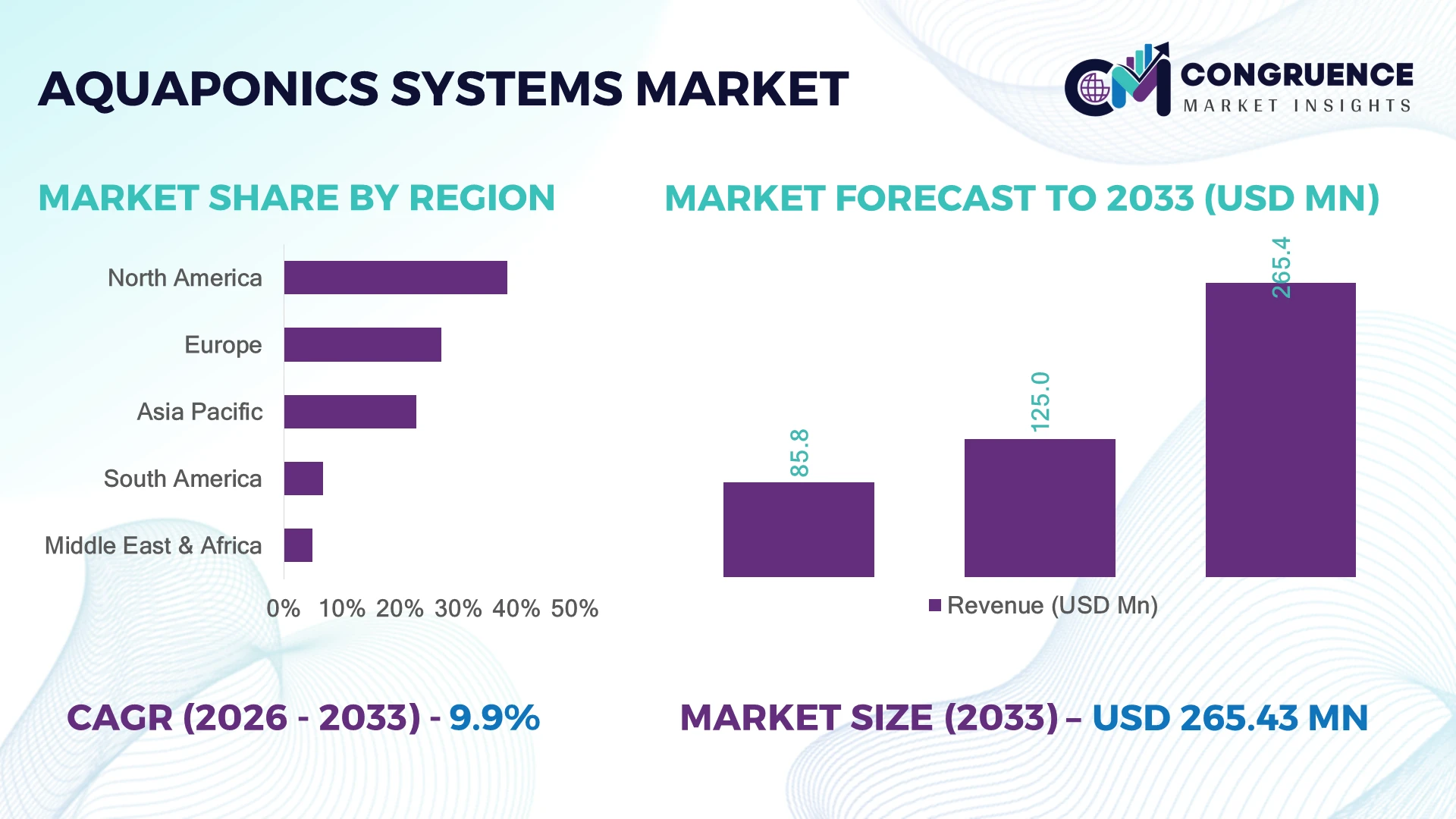

The Global Aquaponics Systems Market was valued at USD 125.0 Million in 2025 and is anticipated to reach a value of USD 265.4 Million by 2033 expanding at a CAGR of 9.87% between 2026 and 2033. Rising adoption of controlled-environment agriculture, water-efficient food production, and integrated fish-vegetable farming systems is accelerating commercial deployment across urban farming, greenhouse cultivation, and institutional agriculture.

The United States dominates the global aquaponics systems market with an estimated 34% share, supported by advanced greenhouse infrastructure, USDA-backed sustainable agriculture initiatives, and widespread adoption of precision farming technologies. More than 2,500 commercial and educational aquaponics installations operate nationwide, while Australia leads in water-constrained farming innovation through high-efficiency recirculating systems. Increasing food security investments and climate-resilient agriculture programs continue to strengthen large-scale deployment across North America.

The market's leadership concentration highlights the importance of investing in scalable automation, regional supply networks, and resource-efficient production technologies to strengthen long-term competitiveness.

Market Size & Growth: Valued at USD 125.0 Million in 2025 and projected to reach USD 265.4 Million by 2033 at a CAGR of 9.87%, supported by rapid adoption of advanced controlled-environment agriculture technologies.

Top Growth Drivers: Water consumption reduced by up to 90%, crop productivity increased by nearly 30%, and urban farming projects expanded by over 20% globally.

Short-Term Forecast: By 2028, automated nutrient monitoring is expected to improve operational efficiency by approximately 18% while reducing maintenance costs by 15%.

Emerging Technologies: AI-driven monitoring, IoT-enabled sensors, automated dosing systems, and digital farm analytics are transforming high-performance aquaponics operations.

Regional Leaders: North America (~USD 90 Million), Europe (~USD 65 Million), and Asia-Pacific (~USD 55 Million) lead through commercial greenhouse expansion, food security initiatives, and smart farming adoption.

Consumer/End-User Trends: More than 45% of premium urban food producers are integrating sustainable aquaponics systems to supply pesticide-free vegetables and fish.

Pilot/Case Example: In 2024, commercial greenhouse modernization projects reported nearly 22% higher crop output through automated environmental control systems.

Competitive Landscape: The leading supplier holds approximately 12% market share alongside Pentair Aquatic Eco-Systems, Nelson and Pade, AquaSprouts, Backyard Aquaponics, and The Aquaponic Source.

Regulatory & ESG Impact: Water-efficient farming systems lower freshwater consumption by up to 90%, aligning with sustainable agriculture policies and climate resilience strategies.

Investment & Funding: More than USD 300 Million has supported controlled-environment agriculture expansion through strategic partnerships, technology investments, and commercial greenhouse projects.

Innovation & Future Outlook: Modular commercial systems, robotics integration, and AI-enabled predictive management are strengthening global supply-chain resilience and operational scalability.

Aquaponics systems are gaining momentum across commercial greenhouses, educational institutions, hospitality, and urban food production where efficient resource utilization is becoming a competitive priority. Recent innovations integrate AI-based water quality monitoring, automated nutrient balancing, and remote farm management platforms, improving operational consistency by nearly 20%. Growing localization of fresh food production amid evolving agricultural regulations and supply-chain diversification is reinforcing long-term deployment across developed and emerging economies, setting the stage for broader strategic expansion.

Aquaponics systems are becoming strategically important as governments, agribusinesses, and food producers prioritize resilient local food production, efficient water management, and climate-adaptive agriculture. Infrastructure modernization, increasing digital farm management, and stronger food security policies are encouraging commercial investment in controlled-environment cultivation while reducing dependence on conventional agricultural supply chains.

Modern AI-enabled aquaponics platforms deliver approximately 20% higher resource efficiency and reduce water usage by as much as 90% compared with conventional soil-based cultivation. North America continues to lead in commercial-scale deployment through advanced greenhouse infrastructure, while Asia-Pacific is expanding rapidly through urban agriculture initiatives and smart farming investments. Over the next two to three years, automated environmental monitoring and predictive analytics are expected to become standard across large commercial facilities, improving operational consistency and production planning.

Commercial greenhouse operators are deploying modular recirculating systems integrated with IoT sensors to optimize fish health, nutrient balance, and crop quality while reducing manual intervention. Companies are strengthening partnerships with technology providers, expanding regional manufacturing capabilities, and investing in intelligent monitoring platforms to improve scalability. Organizations that combine automation, localized production, and sustainable resource management will establish stronger competitive positioning and long-term operational resilience within the evolving global aquaponics ecosystem.

Commercial adoption of controlled-environment agriculture is accelerating as growers seek resilient food production systems that reduce dependence on conventional irrigation and volatile weather conditions. Modern aquaponics facilities use up to 90% less water than traditional farming while improving crop productivity by nearly 30% through continuous nutrient recirculation. In the United States, USDA-supported sustainable farming initiatives and urban agriculture programs are encouraging commercial greenhouse investments, while food retailers increasingly prioritize locally produced vegetables and fish to shorten supply chains. This operational shift is prompting companies to expand modular system portfolios, integrate AI-enabled environmental monitoring, and establish partnerships with greenhouse technology providers. Businesses combining automation with scalable infrastructure gain stronger production consistency and higher resource efficiency.

Large-scale aquaponics deployment remains constrained by substantial upfront investment in recirculating water systems, greenhouse structures, environmental controls, and biological filtration. Operating expenses can account for nearly 35% of annual production costs, while energy consumption represents approximately 20–30% of facility operating expenditure in climate-controlled environments. In Germany, rising electricity costs continue to pressure commercial greenhouse economics, reducing profitability for smaller operators. Dependence on imported sensors, pumps, and control equipment also exposes projects to supply-chain disruptions and procurement delays. To reduce operational risk, companies are localizing equipment sourcing, negotiating long-term supplier agreements, and investing in energy-efficient system designs that improve lifecycle performance and cost predictability.

Artificial intelligence, IoT connectivity, and predictive water-quality analytics are creating new commercial opportunities beyond traditional greenhouse production. Automated nutrient optimization can improve operational efficiency by nearly 20%, while predictive maintenance reduces unexpected equipment downtime by approximately 25%. In Singapore, national food resilience initiatives continue to accelerate investment in high-density urban farming supported by advanced digital agriculture technologies. Companies are expanding R&D programs focused on autonomous monitoring platforms, modular production units, and cloud-based farm management ecosystems that simplify commercial deployment. An emerging strategic advantage lies in integrating aquaponics facilities with renewable energy and circular water infrastructure, enabling lower operating costs and stronger environmental performance for institutional and industrial customers.

Commercial scalability depends on maintaining biological balance across fish cultivation, plant production, and water treatment while integrating increasingly sophisticated automation platforms. Workforce shortages in aquaculture engineering and controlled-environment agriculture contribute to nearly 18% longer commissioning timelines for advanced facilities, while system integration issues can reduce production efficiency by approximately 15% during early deployment phases. In Japan, aging agricultural workforces are increasing reliance on digital monitoring and remote operational management, yet skilled technical personnel remain limited. Companies must strengthen workforce development, standardize interoperable control architectures, and invest in digital training, cybersecurity, and predictive operational analytics to achieve consistent large-scale deployment and maintain long-term competitive differentiation.

AI-Powered Farm Intelligence Commercial operators are rapidly integrating AI-driven monitoring, IoT sensors, and automated nutrient balancing to improve production consistency and reduce manual intervention. More than 48% of newly commissioned commercial facilities now incorporate remote monitoring platforms, while automated control systems reduce water-quality deviations by nearly 22%. Labor shortages in the United States are accelerating digital workflow adoption, prompting technology providers to expand cloud-based management platforms and predictive maintenance capabilities that improve operational uptime and resource efficiency.

Modular Greenhouse Expansion Modular aquaponics systems are replacing conventional fixed installations as growers seek faster deployment and operational flexibility. Prefabricated units shorten installation timelines by approximately 30% and reduce construction-related costs by nearly 18%. In Singapore, commercial operators continue scaling compact greenhouse facilities to strengthen urban food resilience. Manufacturers are responding by standardizing modular components, expanding regional assembly capacity, and partnering with greenhouse integrators to accelerate project delivery while reducing procurement complexity.

Renewable Energy Integration Operators are increasingly coupling aquaponics systems with solar generation, energy storage, and intelligent environmental controls to reduce operating expenses. Integrated renewable systems lower electricity consumption by up to 25%, while automated climate management improves energy efficiency by nearly 17%. Rising electricity prices across Germany have accelerated investment in hybrid energy solutions, encouraging equipment suppliers to develop compatible power management technologies that strengthen long-term operational resilience and production stability.

Circular Resource Optimization Commercial producers are shifting toward closed-loop resource management that maximizes water reuse, nutrient recovery, and waste valorization across integrated production systems. Advanced recirculation technologies enable up to 90% water reuse while reducing nutrient losses by approximately 20%. Food security initiatives and increasing sustainability requirements are encouraging enterprises to redesign production workflows around circular agriculture principles. Companies are expanding strategic partnerships with water treatment specialists and automation providers to improve traceability, compliance, and operational consistency while creating differentiated premium food supply chains.

Deep Water Culture (DWC) Systems represent the leading segment, accounting for approximately 42% of commercial deployments due to their scalability, stable nutrient circulation, and suitability for leafy vegetable production. Their compatibility with automated aeration and environmental control platforms makes them the preferred choice for commercial greenhouse operators seeking consistent yields and lower maintenance variability. Media-Filled Bed Systems continue to hold strong demand among educational institutions and small-scale producers because of their simple biological filtration and relatively lower installation complexity. Companies are enhancing DWC platforms through integrated monitoring technologies, modular expansion capabilities, and standardized production layouts to improve operational efficiency. Nutrient Film Technique (NFT) Systems are emerging as the fastest-growing segment, with commercial adoption increasing by nearly 19% as growers prioritize higher planting density and efficient water distribution for premium herbs and leafy greens. Hybrid and vertical aquaponics configurations are also expanding in urban agriculture projects where space optimization is becoming a strategic priority. Manufacturers are investing in lightweight structural designs, automated nutrient control, and modular product portfolios to address diverse commercial requirements while supporting rapid deployment across institutional and commercial facilities.

Commercial Food Production remains the dominant application, representing nearly 58% of total installations as retailers, restaurants, and food distributors increase procurement of locally produced vegetables and fish. Commercial facilities emphasize year-round production, quality consistency, and efficient resource utilization through automated environmental control systems. Companies continue expanding greenhouse capacity and integrating digital monitoring platforms to improve operational reliability while strengthening localized food supply chains. Home Food Production maintains steady adoption as consumers increasingly invest in compact systems supporting household food security and sustainable lifestyles. Research & Education is the fastest-growing application, expanding by approximately 17% as universities, agricultural institutes, and vocational training centers invest in practical controlled-environment agriculture laboratories. Demonstration farms are increasingly supporting technology validation, workforce development, and sustainable farming research. Other applications, including hospitality, community farming, and institutional projects, continue gaining traction through customized modular solutions. Manufacturers are strengthening collaborations with educational organizations while developing scalable platforms that accommodate both commercial production and research-focused environments.

Commercial Farms remain the dominant end-user segment, accounting for roughly 61% of total demand because they require large-scale production infrastructure, automated environmental controls, and integrated water recirculation technologies. Large operators continue investing in modular greenhouse expansion, digital monitoring, and precision nutrient management to improve productivity and reduce operating costs. Residential/Home Growers represent a stable consumer segment driven by compact, user-friendly systems that support localized food cultivation and educational engagement. Educational & Research Institutions are the fastest-growing end-user category, recording adoption growth of nearly 18% as governments and academic organizations strengthen investments in sustainable agriculture research and technical education. Government & Community Projects are also expanding through urban agriculture initiatives, food resilience programs, and public sustainability strategies. Equipment manufacturers are introducing application-specific product portfolios, flexible pricing models, and technical support partnerships to address varying operational requirements while strengthening long-term customer relationships across institutional and commercial markets.

North America accounted for the largest market share at 38.4% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 11.2% between 2026 and 2033.

North America remains the leading regional market, supported by established greenhouse infrastructure, commercial aquaculture expertise, and widespread adoption of precision agriculture technologies. The region contributes approximately 38.4% of global demand, with commercial greenhouse operators driving large-scale deployment of automated aquaponics facilities. More than 55% of newly commissioned commercial installations incorporate AI-enabled monitoring and remote environmental management systems, improving production consistency and operational efficiency. Strategic partnerships between greenhouse equipment suppliers, agricultural technology companies, and food producers continue expanding integrated farming capacity. Strong institutional research, urban farming initiatives, and localized food production strategies reinforce the region's long-term operational leadership.

United States Market Outlook: The United States represents the largest national market due to its mature controlled-environment agriculture ecosystem, advanced greenhouse manufacturing capabilities, and strong commercial investment in sustainable food production. More than 2,500 operational commercial and educational aquaponics facilities support technology validation and enterprise deployment. Companies continue expanding modular greenhouse projects, integrating digital farm management platforms, and collaborating with research institutions to improve automation, resource efficiency, and localized food supply resilience.

Europe maintains a strong market position through sustainability-focused agricultural modernization, efficient resource utilization, and strict environmental standards encouraging water-saving cultivation systems. The region accounts for approximately 27.1% of global deployment, with increasing investment in greenhouse automation and circular food production. Nearly 45% of commercial facilities are adopting advanced environmental monitoring technologies to improve operational precision and reduce energy consumption. Growing collaboration between agricultural technology providers and commercial growers is strengthening integrated production systems while supporting climate-resilient farming infrastructure and premium fresh produce supply chains.

Netherlands Market Outlook: The Netherlands leads the European market through world-class greenhouse infrastructure, precision horticulture expertise, and advanced agricultural engineering capabilities. Commercial producers continue integrating automated climate control, intelligent irrigation, and recirculating cultivation technologies into high-density greenhouse operations. More than 60% of large greenhouse facilities utilize digital environmental management systems, enabling highly efficient resource utilization while supporting year-round production for domestic and export markets.

Asia-Pacific is emerging as the fastest-growing regional market as governments strengthen food security strategies, urban farming initiatives, and controlled-environment agriculture investments. The region represents approximately 22.8% of global deployment, with commercial projects expanding rapidly across metropolitan food production hubs. Automated cultivation technologies improve operational productivity by nearly 20%, while modular greenhouse construction shortens installation periods by approximately 30%. Enterprises are increasing investment in localized manufacturing, digital agriculture platforms, and integrated aquaculture systems to improve scalability and reduce dependence on imported fresh produce.

Singapore Market Outlook: Singapore has established itself as a strategic innovation hub through strong policy support for urban agriculture and advanced food production technologies. Commercial operators continue deploying high-density vertical aquaponics facilities integrated with AI-based monitoring and automated nutrient management systems. National food resilience initiatives have accelerated enterprise investment, with controlled-environment farming becoming an important component of long-term agricultural infrastructure modernization and sustainable domestic food production.

South America is steadily expanding its aquaponics ecosystem through commercial diversification, sustainable agriculture initiatives, and increasing investment in efficient food production technologies. The region contributes approximately 6.8% of global market activity, supported by growing interest in greenhouse cultivation and integrated aquaculture. Commercial projects have improved water-use efficiency by nearly 80–90%, creating attractive opportunities in water-stressed agricultural zones. Infrastructure limitations and uneven technology availability continue affecting deployment speed, encouraging suppliers to introduce modular systems and localized technical support services that simplify implementation and improve operational reliability.

Brazil Market Outlook: Brazil dominates the regional market owing to its large agricultural economy, expanding greenhouse sector, and increasing focus on sustainable food production. Universities, commercial growers, and agritech companies continue collaborating on integrated aquaponics projects supporting premium vegetable and fish cultivation. Growing adoption of automated environmental monitoring and localized equipment manufacturing is improving commercial feasibility while strengthening domestic expertise in controlled-environment agriculture.

The Middle East & Africa market is advancing through strategic investments in water-efficient agriculture, greenhouse modernization, and food security infrastructure. The region accounts for approximately 4.9% of global market activity, with commercial operators prioritizing technologies that minimize freshwater consumption in arid environments. Modern recirculating aquaponics systems reduce water usage by up to 90%, supporting sustainable production under resource-constrained conditions. Government-backed agricultural diversification programs and partnerships with international technology providers continue strengthening deployment capacity while encouraging localized production of high-value fresh foods.

United Arab Emirates Market Outlook: The United Arab Emirates leads regional adoption through substantial investment in controlled-environment agriculture, smart greenhouse infrastructure, and advanced food security initiatives. Commercial enterprises continue integrating automated climate control, AI-enabled monitoring, and high-efficiency recirculating production systems into urban farming projects. Public-private collaborations and innovation-focused investment programs are accelerating commercial deployment while positioning the country as a regional center for sustainable agricultural technology and climate-resilient food production.

The competitive landscape is shaped by technology specialists including Pentair Aquatic Eco-Systems, Nelson and Pade, The Aquaponic Source, AquaSprouts, and ECF Farmsystems, competing against regional greenhouse integrators and custom system builders. The top five players collectively account for approximately 36% of the global market, reflecting a moderately fragmented structure. Competition centers on automation, biological system reliability, modular design, and lifecycle operating costs rather than price alone. AI-enabled monitoring platforms improve operational efficiency by nearly 20%, while modular installations reduce deployment time by approximately 30%, creating measurable differentiation. Companies are strengthening their positions through strategic partnerships, localized manufacturing, turnkey project delivery, and vertical integration across design, equipment, installation, and technical support. The market is shifting toward digitally connected controlled-environment agriculture solutions, increasing pressure on conventional equipment suppliers lacking software capabilities. High technical expertise, biological process optimization, and after-sales service remain significant entry barriers. Sustainable competitive advantage depends on delivering integrated, automated, scalable systems with proven operational performance.

Nelson and Pade, Inc.

The Aquaponic Source

AquaSprouts

ECF Farmsystems GmbH

Aquaponic Lynx LLC

UrbanFarmers AG

Green Life Aquaponics

Aquaponics USA

EcoGro

Japan Aquaponics

Aquaponics Place

My Aquaponics

Endless Food Systems

Technology innovation is transforming aquaponics from manually managed farming into intelligent controlled-environment production. AI-enabled water-quality analytics, IoT sensor networks, and cloud-based farm management platforms are becoming mainstream across commercial facilities. More than 50% of new commercial installations incorporate connected monitoring systems that improve nutrient stability and reduce manual intervention. Automated environmental controls lower operating variability by approximately 18%, enabling consistent crop quality and healthier aquaculture performance.

Emerging technologies include computer vision for fish health monitoring, predictive maintenance algorithms, autonomous nutrient dosing, and digital twin simulations for production planning. Compared with conventional manually monitored systems, AI-integrated platforms improve resource efficiency by nearly 20% while reducing maintenance costs by approximately 15%. Commercial greenhouse operators, institutional growers, and technology-driven food producers benefit most because integrated platforms simplify large-scale deployment, strengthen traceability, and improve production forecasting. Robotics integration is also reducing repetitive labor requirements while enhancing operational precision.

Between 2026 and 2028, autonomous control architectures, edge computing, and renewable-energy-integrated production systems will accelerate commercial adoption. Modular digital platforms are expected to become standard for enterprise-scale facilities seeking operational resilience and localized food production. Companies investing now in intelligent automation, interoperable software ecosystems, and predictive analytics will achieve stronger competitive positioning through lower operating costs, higher production consistency, faster scalability, and improved long-term sustainability.

December 2024 – Pentair completed the acquisition of G&F Manufacturing LLC, expanding its water treatment and filtration capabilities that support controlled-environment agriculture and aquaculture applications. The acquisition strengthens product integration and manufacturing flexibility across commercial water systems.

February 2025 – Pentair reported 17% growth in fourth-quarter operating income and continued investment in sustainable water technologies supporting advanced recirculating water management solutions applicable to aquaculture and controlled farming. The stronger financial position supports continued innovation and product development.

September 2025 – Innovasea partnered with the Andrew J. Young Foundation to deploy two integrated recirculating aquaculture and aquaponics facilities in Colorado and Georgia. The initiative expands regenerative food production infrastructure and demonstrates commercial-scale deployment of advanced land-based aquaculture technologies.

March 2026 – Aquasafra Holdings and Waterfield Farms signed a strategic agreement with Avio Smart Market Stack to evaluate aquaponics-enabled aquaculture deployment across 5,000+ villages through region-specific hatcheries, farmer training, and technology integration, significantly strengthening climate-resilient food production ecosystems. Source: www.business-standard.com

The report delivers comprehensive analysis across Deep Water Culture (DWC), Media-Filled Bed, Nutrient Film Technique (NFT), and hybrid systems, evaluating their commercial adoption, operational efficiency, deployment patterns, and technology integration. It assesses applications including commercial food production, residential cultivation, research, and institutional projects while examining demand across commercial farms, educational organizations, government initiatives, and home growers. Regional evaluation covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, supported by operational trends, deployment intensity, technology adoption, and competitive positioning.

The study also evaluates automation, AI-enabled monitoring, IoT connectivity, predictive analytics, renewable energy integration, and modular greenhouse technologies influencing future industry transformation. Competitive benchmarking includes leading technology providers, strategic partnerships, product innovation, and expansion initiatives. With analysis spanning more than 10 major industry participants and multiple end-user segments, the report supports investment prioritization, market entry assessment, product development strategies, capacity expansion decisions, and long-term competitive positioning across evolving controlled-environment agriculture markets between 2026 and 2033.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 125.0 Million |

| Market Revenue (2033) | USD 265.4 Million |

| CAGR (2026–2033) | 9.87% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Pentair Aquatic Eco-Systems; Nelson and Pade, Inc.; The Aquaponic Source; AquaSprouts; ECF Farmsystems GmbH; Aquaponic Lynx LLC; UrbanFarmers AG; Green Life Aquaponics; Aquaponics USA; EcoGro; Japan Aquaponics; Endless Food Systems |

| Customization & Pricing | Available on Request (10% Customization Free) |