Reports

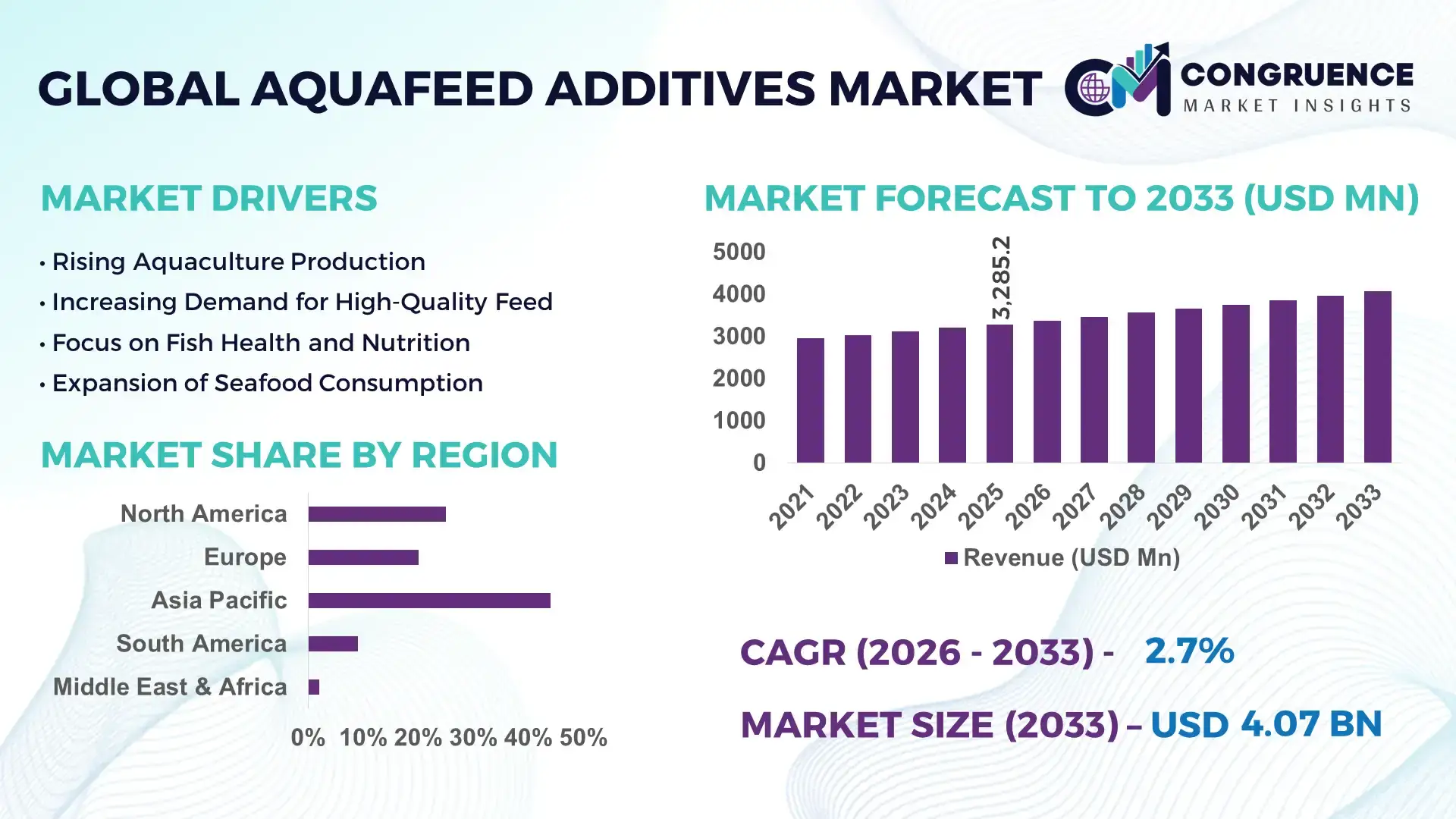

The Global Aquafeed Additives Market was valued at USD 3285.16 Million in 2025 and is anticipated to reach a value of USD 4065.56 Million by 2033 expanding at a CAGR of 2.7% between 2026 and 2033. The steady expansion is primarily driven by increasing demand for high-quality aquaculture production and improved feed efficiency.

China continues to exhibit strong dominance in aquafeed additives production, supported by an aquaculture output exceeding 70 million metric tons annually. The country has invested over USD 1.5 billion in aquaculture modernization projects between 2022 and 2025, focusing on precision feeding systems and enzyme-based additives. More than 65% of commercial fish farms in coastal provinces have adopted functional feed additives such as probiotics and amino acids to enhance yield and disease resistance. Additionally, China’s feed mills have achieved production capacities exceeding 200 million metric tons per year, integrating advanced micro-encapsulation technologies to improve nutrient delivery efficiency and reduce feed waste in intensive aquaculture systems.

Market Size & Growth: Valued at USD 3285.16 Million in 2025 and projected to reach USD 4065.56 Million by 2033 at a CAGR of 2.7%, driven by rising aquaculture intensification and feed optimization demand.

Top Growth Drivers: Feed conversion efficiency improvement (30%), disease resistance enhancement (25%), and protein utilization optimization (20%).

Short-Term Forecast: By 2028, feed efficiency is expected to improve by 18% through advanced additive integration and precision feeding systems.

Emerging Technologies: Micro-encapsulation technology, enzyme-based nutrient enhancers, and AI-driven feed formulation platforms.

Regional Leaders: Asia-Pacific projected at USD 1800 Million by 2033 with high aquaculture density; Europe at USD 900 Million driven by sustainability compliance; North America at USD 750 Million with advanced feed innovation adoption.

Consumer/End-User Trends: Commercial aquaculture farms account for over 70% of additive usage, with increased demand for antibiotic-free feed solutions.

Pilot or Case Example: In 2024, a Norway-based aquaculture project achieved 22% feed conversion improvement using enzyme-enriched feed additives.

Competitive Landscape: Market leader holds approximately 18% share, followed by key players including Cargill, ADM, DSM-Firmenich, Nutreco, and Alltech.

Regulatory & ESG Impact: Regulations targeting 15–20% reduction in antibiotic usage are accelerating adoption of natural and probiotic additives.

Investment & Funding Patterns: Over USD 2 billion invested globally in aquafeed innovation and sustainable aquaculture systems between 2022 and 2025.

Innovation & Future Outlook: Increasing integration of bioactive compounds, precision nutrition, and sustainable feed additives is shaping long-term market growth.

Aquafeed additives are widely utilized across finfish, crustaceans, and mollusks, with finfish accounting for nearly 55% of total consumption due to large-scale farming operations. Innovations such as phytogenic additives and functional lipids are enhancing growth performance while reducing environmental impact. Regulatory emphasis on antibiotic-free aquaculture and sustainable sourcing is influencing product development strategies. Asia-Pacific dominates consumption due to high seafood demand, while Europe emphasizes eco-friendly additives. Emerging trends include biosecurity-focused feed solutions, digital feed management systems, and increased adoption of organic aquaculture practices, positioning the market for stable, technology-driven expansion.

The aquafeed additives market holds strategic importance as global aquaculture production surpasses 120 million metric tons annually, necessitating efficient, sustainable, and high-performance feed solutions. Advanced feed technologies such as enzyme-enhanced formulations deliver up to 25% improvement in nutrient absorption compared to conventional feed additives, significantly reducing feed wastage and operational costs. Precision aquaculture systems integrated with AI-driven feed optimization are enabling farms to achieve measurable productivity gains while minimizing environmental impact.

Asia-Pacific dominates in volume due to extensive aquaculture infrastructure, while Europe leads in adoption with over 60% of enterprises implementing sustainable and antibiotic-free feed additives. By 2028, AI-powered feed management systems are expected to improve feed conversion ratios by 20%, enhancing overall production efficiency. Firms are committing to ESG targets, including a 30% reduction in antibiotic usage and a 25% decrease in feed-related emissions by 2030, aligning with global sustainability mandates.

In 2024, a Chile-based salmon farming initiative achieved a 19% reduction in feed waste through the deployment of smart feeding systems combined with probiotic additives, demonstrating measurable operational benefits. The integration of biotechnology, data analytics, and sustainable feed inputs is reshaping industry standards. As regulatory frameworks tighten and consumer demand for responsibly sourced seafood increases, the Aquafeed Additives Market is emerging as a critical pillar supporting resilient supply chains, compliance-driven production, and long-term sustainable growth.

The aquafeed additives market is characterized by evolving production practices, increasing regulatory scrutiny, and technological advancements in feed formulation. Rising global seafood consumption, which has grown at over 3% annually, is driving demand for efficient aquaculture systems. Feed additives such as amino acids, enzymes, vitamins, and probiotics are playing a crucial role in improving feed conversion ratios and animal health. Industry participants are focusing on reducing environmental impact through low-emission feed solutions and sustainable ingredient sourcing. Additionally, digitalization in aquaculture operations is influencing additive usage patterns, enabling precise nutrient delivery and improved farm productivity. Market dynamics are further shaped by regional consumption disparities, raw material availability, and innovation in functional feed ingredients.

The rapid intensification of aquaculture systems is significantly increasing the demand for high-performance aquafeed additives. Intensive fish farming systems now account for over 60% of global aquaculture output, requiring optimized feed solutions to maintain productivity and health standards. Feed additives such as enzymes and probiotics can improve feed conversion efficiency by up to 25%, reducing overall feed consumption and operational costs. Additionally, the use of functional additives enhances disease resistance, lowering mortality rates by approximately 15–20% in high-density farming environments. The expansion of commercial aquaculture farms, particularly in Asia-Pacific, has led to higher adoption of advanced feed formulations, supporting consistent growth in additive demand.

Volatility in raw material prices, particularly for key ingredients such as fishmeal, soybean derivatives, and specialty chemicals, poses a significant challenge for aquafeed additive manufacturers. Fishmeal prices have shown fluctuations of up to 30% over recent years due to supply constraints and environmental factors affecting fish stocks. Similarly, plant-based protein sources are subject to agricultural variability and global trade disruptions. These cost fluctuations impact production planning and profit margins, forcing manufacturers to adjust pricing strategies. Smaller producers, in particular, face difficulties in maintaining consistent supply chains, which limits market expansion and adoption of premium additive solutions.

The global shift toward sustainable aquaculture practices presents substantial growth opportunities for aquafeed additives. Increasing regulatory restrictions on antibiotic use have accelerated demand for natural alternatives such as probiotics, prebiotics, and phytogenic additives. These solutions can enhance immunity and growth rates while reducing environmental impact. Sustainable aquaculture certifications now cover over 25% of global seafood production, encouraging producers to adopt eco-friendly feed inputs. Additionally, innovations in algae-based additives and insect protein supplements are gaining traction, offering alternative nutrient sources with lower carbon footprints. This transition toward green aquaculture is opening new avenues for product development and market expansion.

Strict regulatory frameworks governing feed safety, environmental impact, and animal health present ongoing challenges for the aquafeed additives market. Compliance with international standards requires extensive testing, certification, and quality assurance processes, increasing operational complexity and costs. For instance, European regulations mandate rigorous evaluation of feed additives, including toxicity and environmental impact assessments, which can extend product approval timelines by 12–24 months. Additionally, maintaining consistency in additive quality across large-scale production is technically demanding. These factors create barriers for new entrants and slow down innovation cycles, impacting overall market growth and competitiveness.

• Rapid Shift Toward Functional and Probiotic Feed Additives: Functional aquafeed additives, particularly probiotics and prebiotics, are witnessing accelerated adoption, with over 48% of aquaculture producers integrating these solutions into feed formulations. These additives have demonstrated the ability to improve survival rates by 18–22% in shrimp and fish farming operations. Additionally, probiotic-enhanced feeds have reduced disease outbreaks by approximately 20%, supporting antibiotic-free aquaculture practices. The trend is particularly strong in Asia-Pacific, where more than 60% of large-scale farms are transitioning toward gut-health-focused feed strategies to enhance productivity and meet export compliance standards.

• Increased Adoption of Precision Nutrition and AI-Driven Feed Optimization: Precision nutrition technologies are gaining traction, with nearly 35% of commercial aquaculture farms adopting data-driven feed management systems. AI-based feed optimization tools have improved feed conversion ratios by up to 20%, while reducing feed waste by 15%. Smart feeding systems integrated with sensors and analytics platforms are enabling real-time adjustments in nutrient delivery. In advanced markets, over 40% of salmon farming operations have implemented automated feeding systems, resulting in measurable improvements in growth rates and operational efficiency.

• Expansion of Sustainable and Alternative Protein Additives: Sustainable aquafeed additives derived from algae, insect protein, and plant-based sources now account for nearly 28% of new product development initiatives. These alternatives have shown a 25% reduction in environmental impact compared to conventional fishmeal-based additives. In Europe, over 50% of new aquafeed formulations include at least one sustainable additive component, aligning with strict environmental regulations. Additionally, algae-based omega-3 additives have improved fish growth performance by 12–15%, while reducing dependency on marine resources.

• Growing Demand for Micro-Encapsulation and Advanced Delivery Technologies: Micro-encapsulation technologies are being adopted in over 30% of high-value aquafeed products to enhance nutrient stability and bioavailability. These technologies have improved nutrient absorption efficiency by up to 18% and reduced leaching losses in water by 10–12%. Feed manufacturers are increasingly investing in advanced coating and encapsulation systems to ensure targeted nutrient delivery. In North America and Europe, nearly 45% of premium aquafeed products now utilize encapsulated additives, supporting consistent performance in intensive aquaculture environments.

The aquafeed additives market is segmented based on type, application, and end-user, reflecting diverse operational requirements across global aquaculture systems. By type, amino acids, vitamins, enzymes, and probiotics dominate due to their essential role in improving feed efficiency and animal health. Applications are largely concentrated in finfish, crustaceans, and mollusks, with finfish accounting for the highest consumption due to large-scale farming operations. End-user segmentation highlights commercial aquaculture farms as the primary consumers, followed by integrated feed manufacturers and research institutions. Approximately 70% of additive demand originates from intensive aquaculture operations, where productivity and disease management are critical. The segmentation structure reflects a growing emphasis on performance optimization, sustainability, and regulatory compliance across the aquaculture value chain.

Amino acids represent the leading segment in the aquafeed additives market, accounting for approximately 34% of total adoption due to their critical role in enhancing protein synthesis and feed conversion efficiency. Lysine and methionine are widely used, improving growth rates by up to 20% in high-density aquaculture systems. In comparison, vitamins account for nearly 22% of adoption, while enzymes hold around 18%. However, probiotics are emerging as the fastest-growing segment, expanding at an estimated CAGR of 5.1%, driven by increasing demand for antibiotic-free feed solutions and improved gut health management. Enzymes such as phytase and protease are gaining traction due to their ability to increase nutrient digestibility by 15–18%, while vitamins remain essential for maintaining metabolic functions and immunity. Other types, including antioxidants, binders, and acidifiers, collectively contribute approximately 26% of the market, serving niche but critical roles in feed stability and preservation.

Finfish applications dominate the aquafeed additives market, accounting for nearly 55% of total usage due to the large-scale farming of species such as salmon, tilapia, and carp. Crustaceans, including shrimp and prawns, represent approximately 30% of the market, driven by export-oriented aquaculture practices. However, mollusks are emerging as the fastest-growing application segment, with an estimated CAGR of 4.8%, supported by increasing demand for sustainable seafood and low-input farming systems. Additives used in finfish farming improve feed conversion efficiency by up to 22%, while in crustacean farming, they enhance disease resistance and survival rates by 18–20%. Mollusk farming benefits from specialized additives that improve shell formation and nutrient uptake. Other applications, including ornamental fish and emerging aquaculture species, contribute around 15% of the market, reflecting niche but growing demand segments.

Commercial aquaculture farms are the leading end-user segment, accounting for approximately 68% of total aquafeed additive consumption due to the scale and intensity of production systems. Integrated feed manufacturers follow with around 20% share, focusing on developing customized feed solutions for diverse aquaculture species. Research institutions and small-scale farms collectively account for the remaining 12%, contributing to innovation and localized adoption.

While commercial farms dominate, integrated aquaculture companies are the fastest-growing end-user segment, expanding at an estimated CAGR of 4.9%, driven by vertical integration strategies and increased investment in feed optimization technologies. These companies are adopting advanced additives to achieve consistent production outcomes and regulatory compliance. Adoption rates among large-scale aquaculture enterprises exceed 75%, compared to 45–50% among small and medium farms, reflecting disparities in access to technology and capital.

Region Asia-Pacific accounted for the largest market share at 52% in 2025 however, Region Europe is expected to register the fastest growth, expanding at a CAGR of 3.4% between 2026 and 2033.

Asia-Pacific’s dominance is supported by aquaculture production exceeding 90 million metric tons, with China alone contributing over 60% of regional output. North America holds approximately 16% share, driven by advanced feed technologies and high-value aquaculture species such as salmon. Europe accounts for nearly 18% of the market, supported by stringent sustainability regulations and widespread adoption of functional additives. South America contributes around 9%, led by Brazil and Chile with combined aquaculture production surpassing 5 million metric tons annually. The Middle East & Africa region holds close to 5%, with increasing investments in aquaculture infrastructure and feed manufacturing. Across regions, over 65% of large-scale farms are integrating additives such as enzymes and probiotics to improve feed efficiency, while more than 40% of feed mills globally have adopted automated production systems to enhance consistency and reduce waste.

How are advanced feed technologies reshaping aquaculture efficiency and sustainability?

North America accounts for approximately 16% of the global aquafeed additives market, driven by high-value aquaculture operations and technological innovation. The United States and Canada lead regional demand, with salmon, trout, and shrimp farming contributing significantly to additive consumption. Over 70% of large aquaculture enterprises in this region utilize precision feeding systems, improving feed conversion ratios by up to 18%. Regulatory frameworks promoting antibiotic-free aquaculture have accelerated the adoption of probiotics and enzyme-based additives, with nearly 60% of feed formulations now incorporating functional ingredients. Digital transformation is evident, as more than 45% of aquaculture farms have implemented AI-driven monitoring systems. A leading regional player, Cargill, has expanded its aqua nutrition portfolio with customized feed solutions, improving nutrient efficiency by 12% in commercial trials. Consumer behavior reflects strong demand for sustainably sourced seafood, with over 65% of buyers preferring products certified for environmental compliance.

What role do sustainability regulations and innovation play in shaping feed additive demand?

Europe holds approximately 18% of the aquafeed additives market, with key countries including Norway, Germany, France, and the UK leading adoption. The region is characterized by strict regulatory oversight, with more than 75% of aquaculture operations complying with sustainability certifications. Regulatory initiatives targeting a 20% reduction in antibiotic use have accelerated the shift toward natural additives such as phytogenics and probiotics. Technological advancements are prominent, with over 50% of feed manufacturers adopting micro-encapsulation techniques to improve nutrient stability. Norway remains a major hub, producing over 1.5 million metric tons of farmed salmon annually, driving high demand for specialized additives. A regional leader, Nutreco, has introduced advanced feed solutions that enhance growth performance by 15% while reducing environmental impact. Consumer behavior in this region is strongly influenced by sustainability, with over 70% of seafood buyers prioritizing eco-labeled and responsibly farmed products.

Why is aquaculture expansion and feed innovation accelerating demand at scale?

Asia-Pacific leads the global aquafeed additives market in volume, contributing over 52% of total consumption. China, India, Vietnam, and Indonesia are the top consuming countries, with China alone producing more than 70 million metric tons of aquaculture output annually. The region’s feed manufacturing capacity exceeds 250 million metric tons, supported by continuous infrastructure expansion and modernization. More than 60% of commercial farms have adopted functional additives to improve productivity and disease resistance. Technological innovation is advancing rapidly, with over 35% of feed mills integrating automated systems and precision formulation technologies. A key regional player, Tongwei Group, has expanded production capacity by over 20% in recent years to meet rising demand. Consumer behavior reflects strong seafood consumption trends, with per capita intake exceeding 30 kg annually in several countries, driving consistent growth in aquafeed additive adoption.

How are export-driven aquaculture industries influencing feed innovation and adoption?

South America accounts for approximately 9% of the global aquafeed additives market, led by Brazil, Chile, and Ecuador. Chile’s salmon industry alone produces over 1 million metric tons annually, requiring high-performance feed additives to maintain export quality standards. Brazil has expanded its aquaculture output by more than 10% annually in recent years, increasing demand for feed optimization solutions. Government initiatives supporting aquaculture development have resulted in over 25% growth in feed production capacity across the region. Infrastructure improvements, including modern feed mills and cold chain systems, are enhancing supply efficiency. A regional company, BioMar Chile, has introduced sustainable feed solutions that reduce feed waste by 14% in commercial operations. Consumer behavior is influenced by export markets, with over 60% of production targeting international demand, driving the need for high-quality, compliant feed additives.

What factors are driving aquaculture modernization and feed additive adoption?

The Middle East & Africa region represents approximately 5% of the aquafeed additives market, with growing demand driven by food security initiatives and aquaculture expansion. Countries such as the UAE, Saudi Arabia, Egypt, and South Africa are investing heavily in aquaculture infrastructure, with Egypt producing over 2 million metric tons of fish annually. Regional governments are promoting local feed production, resulting in a 20% increase in feed manufacturing facilities over the past five years. Technological modernization includes the adoption of automated feeding systems in nearly 30% of large farms. Regulatory frameworks are evolving to ensure feed quality and sustainability, encouraging the use of advanced additives. A regional player, Skretting Middle East, has developed specialized feed solutions tailored to local species, improving growth rates by 13%. Consumer behavior reflects increasing demand for locally produced seafood, with urban consumption rising by over 25% in key markets.

China Aquafeed Additives Market – 38% share: Dominates due to extensive aquaculture production capacity exceeding 70 million metric tons and strong feed manufacturing infrastructure.

United States Aquafeed Additives Market – 14% share: Leads with advanced feed technologies, high adoption of precision nutrition systems, and strong demand for sustainable aquaculture solutions.

The aquafeed additives market is moderately fragmented, with over 120 active global and regional competitors operating across feed production, biotechnology, and specialty ingredient segments. The top five companies collectively account for approximately 45% of the total market share, indicating a balanced competitive environment with opportunities for both established players and emerging entrants. Leading companies are focusing on strategic partnerships, product innovation, and geographic expansion to strengthen their market positions.

More than 35% of major players have invested in research and development initiatives targeting enzyme-based additives, probiotics, and sustainable feed solutions. Mergers and acquisitions have increased by nearly 20% over the past three years, reflecting consolidation efforts aimed at enhancing technological capabilities and supply chain efficiency. Additionally, over 40% of companies are integrating digital technologies such as AI-driven feed formulation and real-time monitoring systems to improve product performance and customer engagement.

Innovation remains a key competitive factor, with more than 50 new additive formulations introduced globally between 2023 and 2025. Companies are also focusing on sustainability, with over 60% of leading firms committing to reducing environmental impact through eco-friendly feed ingredients and production processes. This dynamic competitive landscape is characterized by continuous innovation, strategic collaborations, and increasing emphasis on sustainable aquaculture solutions.

Cargill

Archer Daniels Midland (ADM)

DSM-Firmenich

Nutreco

Alltech

Evonik Industries

Kemin Industries

Adisseo

Novozymes

BASF

BioMar Group

Technological advancements in the aquafeed additives market are transforming feed efficiency, sustainability, and aquaculture productivity. One of the most impactful innovations is enzyme technology, where additives such as phytase and protease improve nutrient digestibility by 15–20%, enabling better phosphorus and protein utilization. These enzymes are increasingly integrated into over 40% of commercial feed formulations, particularly in high-density aquaculture systems. Micro-encapsulation technology is another critical advancement, used in nearly 30–35% of premium aquafeed products. This technology enhances nutrient stability and reduces leaching losses in water by up to 12%, ensuring targeted delivery of vitamins, amino acids, and probiotics. Additionally, encapsulated additives can improve bioavailability by approximately 18%, supporting consistent growth rates across species.

Digitalization and AI-driven feed optimization are gaining significant traction, with over 35% of large-scale aquaculture farms adopting smart feeding systems. These systems use real-time data analytics and sensor-based monitoring to adjust feeding patterns, resulting in feed conversion improvements of up to 20% and waste reduction of nearly 15%. Precision nutrition platforms are enabling tailored feed formulations based on species-specific requirements and environmental conditions. Biotechnology innovations, including fermentation-based production of amino acids and probiotics, are expanding rapidly, with more than 25% of new additive products utilizing bio-based processes. Sustainable feed technologies such as algae-derived omega-3 additives and insect protein enhancers are reducing reliance on fishmeal, lowering environmental impact by up to 25%. These technological advancements collectively position the aquafeed additives market as a key enabler of efficient, sustainable, and scalable aquaculture production systems.

• In March 2025, DSM-Firmenich expanded its Veramaris algal omega-3 production capacity to supply aquaculture feed producers with EPA and DHA-rich additives, enabling fish farmers to reduce fish oil dependency by over 60% while maintaining nutritional value. Source: www.dsm-firmenich.com

• In September 2024, Cargill launched an advanced digital aqua nutrition platform integrating AI-driven feed management tools, helping aquaculture farms improve feed conversion efficiency by up to 15% and reduce feed waste through real-time monitoring systems. Source: www.cargill.com

• In May 2024, Nutreco introduced a new range of functional aquafeed additives under its Skretting brand, focusing on gut health and immunity enhancement, demonstrating up to 18% improvement in fish survival rates during commercial aquaculture trials. Source: www.nutreco.com

• In January 2025, Evonik Industries expanded its amino acid production facility to support aquaculture feed demand, increasing output capacity by 12% and enabling improved protein utilization efficiency in fish diets through optimized methionine supplementation. Source: www.evonik.com

The aquafeed additives market report provides a comprehensive analysis of industry structure, segmentation, technological advancements, and regional performance across the global aquaculture ecosystem. The report covers key product categories including amino acids, enzymes, vitamins, probiotics, antioxidants, and binders, which collectively account for over 90% of additive usage in commercial aquafeed formulations. It evaluates application segments such as finfish, crustaceans, and mollusks, with finfish alone representing more than 50% of global consumption due to large-scale aquaculture operations.

Geographically, the report encompasses detailed insights across five major regions, including Asia-Pacific, North America, Europe, South America, and the Middle East & Africa, collectively representing 100% of global production and consumption patterns. It highlights regional variations in feed manufacturing capacity, with Asia-Pacific exceeding 250 million metric tons annually, while Europe and North America focus on high-value, technology-driven aquaculture systems.

The scope further includes analysis of advanced technologies such as micro-encapsulation, enzyme engineering, and AI-based feed optimization platforms, which are currently adopted by over 30–40% of large-scale aquaculture enterprises. Additionally, the report addresses regulatory frameworks influencing additive adoption, including restrictions on antibiotic usage and sustainability mandates impacting more than 70% of commercial aquaculture operations.

Emerging segments such as algae-based additives, insect protein enhancers, and bioactive compounds are also examined, reflecting growing industry focus on sustainable and alternative feed solutions. The report is designed to support strategic decision-making by providing actionable insights into product innovation, end-user demand patterns, competitive positioning, and future industry developments.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

2.7% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Cargill, Archer Daniels Midland (ADM), DSM-Firmenich, Nutreco, Alltech, Evonik Industries, Kemin Industries, Adisseo, Novozymes, BASF, BioMar Group |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |