Reports

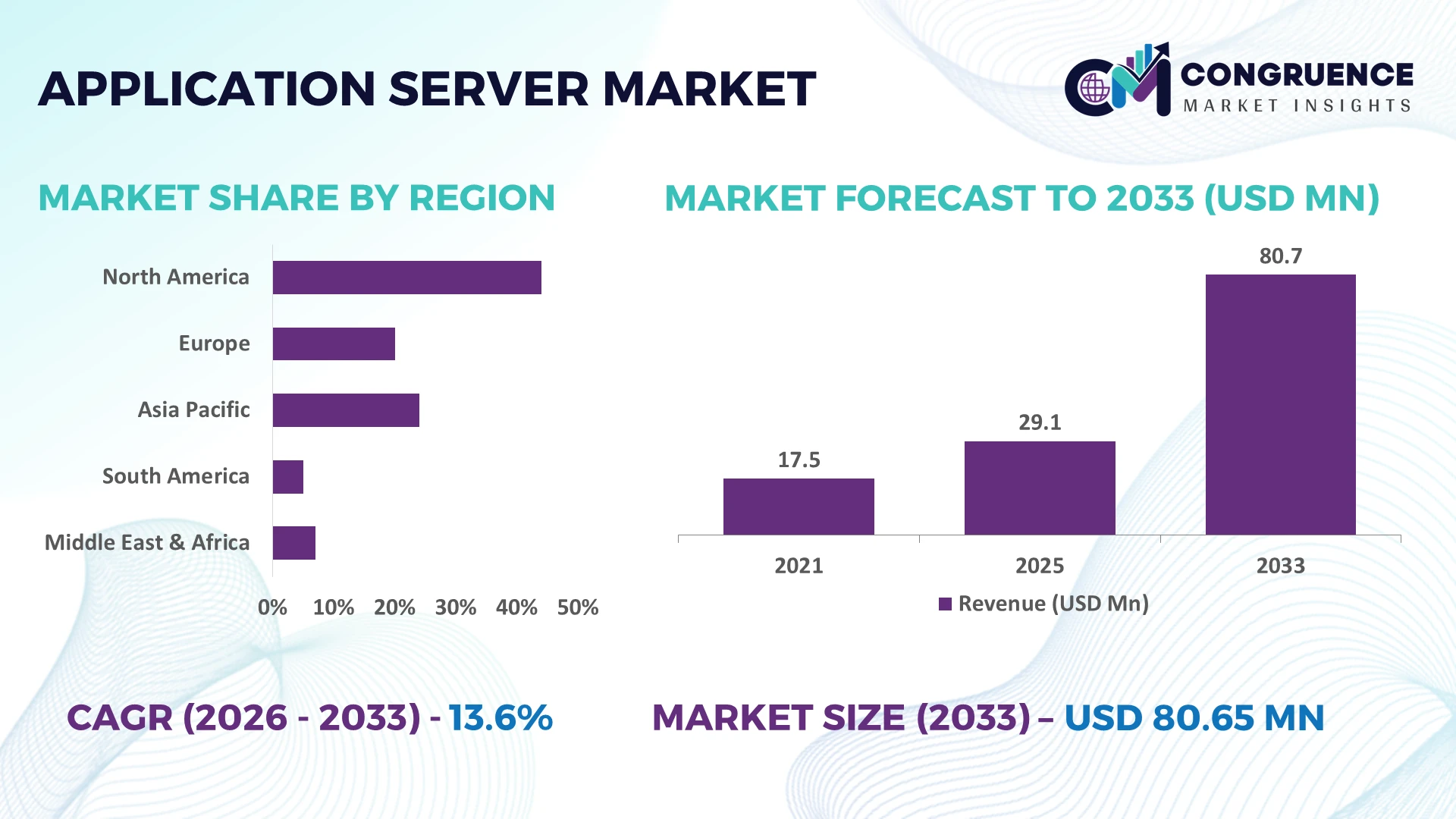

The Global Application Server Market was valued at USD 29.08 Million in 2025 and is anticipated to reach a value of USD 80.65 Million by 2033 expanding at a CAGR of 13.6% between 2026 and 2033. Growth is primarily driven by enterprise migration toward cloud-native application architectures, AI-enabled workload orchestration, containerized deployments, and hybrid infrastructure modernization across banking, manufacturing, healthcare, and public-sector digital platforms.

The United States accounts for approximately 34% of global enterprise application server deployments, supported by hyperscale cloud investments, large financial institutions, and advanced software ecosystems, while China represents nearly 22% through accelerated industrial digitalization and domestic cloud expansion. Ongoing semiconductor supply-chain diversification across Asia since recent geopolitical trade realignments has strengthened deployment resilience, enabling faster enterprise infrastructure upgrades and wider adoption of high-performance middleware platforms.

Organizations prioritizing scalable, secure, and cloud-ready application server environments are positioned to accelerate digital transformation while improving long-term infrastructure efficiency.

Market Size & Growth: USD 29.08 Million in 2025, reaching USD 80.65 Million by 2033 at 13.6% CAGR, driven by enterprise cloud-native modernization and AI-enabled application management.

Top Growth Drivers: Hybrid cloud adoption exceeds 61%, container deployment rises 48%, and enterprise automation initiatives expand 42%, strengthening application server utilization.

Short-Term Forecast: By 2028, automated workload management improves infrastructure efficiency by 28% while reducing application deployment time by 35%.

Emerging Technologies: AI operations, Kubernetes orchestration, and serverless integration improve application availability by over 30% across advanced enterprise environments.

Regional Leaders: North America approaches USD 29 Million, Asia-Pacific exceeds USD 24 Million, and Europe surpasses USD 18 Million, supported by enterprise cloud expansion and digital transformation programs.

Consumer/End-User Trends: More than 67% of large enterprises prioritize hybrid application platforms supporting secure multi-cloud operations and continuous deployment.

Pilot/Case Example: In 2026, an enterprise modernization program reduced application response latency by 31% through AI-assisted workload balancing and container optimization.

Competitive Landscape: Leading vendors collectively hold approximately 46% market share, supported by IBM, Oracle, Red Hat, Microsoft, and Fujitsu through enterprise platform innovation.

Regulatory & ESG Impact: Energy-efficient infrastructure initiatives reduce server power consumption by nearly 18% while strengthening compliance with evolving data governance frameworks.

Investment & Funding: More than USD 6 billion in enterprise cloud infrastructure investment supports platform expansion, regional data center growth, and strategic technology partnerships.

Innovation & Future Outlook: Edge-native application services, AI-driven middleware, and zero-trust architectures accelerate next-generation enterprise platform strategies amid global infrastructure diversification.

Application Server Market demand is expanding across financial services, healthcare, telecommunications, manufacturing, and public-sector digital platforms that require secure, high-availability application processing. AI-assisted workload optimization and cloud-native middleware continue improving operational efficiency, with containerized deployments increasing by nearly 45%. Enterprise infrastructure localization and resilient technology supply-chain strategies are further accelerating platform modernization, creating a stronger foundation for the strategic market analysis that follows.

Application servers have become a strategic foundation for enterprise competitiveness as organizations modernize legacy IT environments and deploy cloud-native business applications at scale. Infrastructure modernization, stricter data governance requirements, and digital service expansion are reshaping enterprise software strategies across banking, healthcare, manufacturing, and telecommunications. The ongoing restructuring of global technology supply chains is also encouraging localized data infrastructure and resilient application deployment models, strengthening enterprise demand for secure, scalable middleware platforms.

Modern container-based application server environments reduce deployment time by nearly 40% and lower infrastructure management costs by approximately 25% compared with traditional monolithic architectures. The United States leads large-scale enterprise implementation through hyperscale cloud ecosystems, while India records faster enterprise application deployment growth driven by expanding digital public infrastructure and software development capacity. Over the next two to three years, more than 60% of large organizations are expected to standardize hybrid application platforms supporting automated workload orchestration and AI-assisted operations.

Financial institutions are deploying modern application servers to process high-volume digital transactions while maintaining regulatory compliance and service continuity. Vendors are expanding investments in Kubernetes integration, security automation, and strategic cloud partnerships to strengthen enterprise ecosystems. Organizations that prioritize resilient application infrastructure, operational flexibility, and intelligent platform management will establish stronger competitive positioning as enterprise software architectures continue evolving.

Enterprise migration toward cloud-native architectures remains the strongest structural driver for the Application Server Market. More than 68% of large enterprises now operate hybrid cloud environments, while container adoption has increased by approximately 46%, accelerating demand for scalable application servers. India's digital infrastructure expansion and the United States' enterprise AI investments continue increasing enterprise application workloads. These developments enable faster software delivery, lower operational complexity, and improved platform resilience. In response, technology providers are expanding managed application server portfolios, investing in AI-driven performance optimization, and forming cloud ecosystem partnerships. The strategic outcome is a shift from infrastructure ownership toward intelligent application lifecycle management with higher operational efficiency.

Integration with legacy enterprise systems remains a major structural limitation despite rapid modernization initiatives. Around 43% of enterprise IT environments continue operating mixed legacy and cloud workloads, while application migration projects experience implementation delays exceeding 20% because of compatibility constraints. Strict data residency regulations in countries such as Germany increase deployment complexity for multinational organizations managing distributed applications. These factors raise operational costs and extend modernization timelines. Companies are reducing exposure by adopting modular middleware, diversifying infrastructure providers, and localizing data processing environments. Organizations with standardized integration frameworks achieve smoother deployment cycles and stronger long-term operational consistency.

AI-enabled workload orchestration, edge computing, and platform automation are creating new value beyond conventional application hosting. Automated resource allocation improves server utilization by approximately 30%, while predictive performance analytics reduce unplanned downtime by nearly 25%. Japan's investment in industrial digitalization and intelligent manufacturing is accelerating enterprise demand for low-latency application infrastructure. Vendors are strengthening research programs, expanding AI-integrated middleware capabilities, and building strategic partnerships with cloud and cybersecurity providers. An emerging opportunity lies in industry-specific application server platforms optimized for healthcare, finance, and industrial operations, enabling differentiated enterprise services with measurable efficiency improvements.

Maintaining secure, high-performance hybrid environments at enterprise scale presents a long-term execution challenge. More than 52% of organizations identify cybersecurity integration as the primary obstacle during application modernization, while multi-cloud management increases administrative workloads by nearly 27%. Rising AI-generated application traffic further pressures infrastructure optimization and operational visibility. Companies must strengthen observability platforms, workforce capabilities, and zero-trust security architectures to sustain consistent application performance across distributed environments. Strategic investment in automation, unified management frameworks, and cybersecurity partnerships will determine long-term competitiveness as enterprise application ecosystems become increasingly complex and interconnected.

AI-Driven Operations Expansion: Enterprises are integrating AI-based monitoring and automation into application server environments, with adoption rising nearly 38% among large organizations and workload optimization improving resource efficiency by around 30%. Companies are scaling intelligent management tools to reduce downtime, accelerate deployment cycles, and improve application performance amid growing software complexity.

Hybrid Deployment Acceleration: Hybrid application server models are gaining traction as more than 65% of enterprises combine private and public infrastructure, while cloud workload migration increases by approximately 45%. Data sovereignty requirements and supply-chain restructuring are encouraging companies in Germany, Japan, and India to adopt flexible deployment strategies with localized infrastructure planning.

Container Integration Growth: Containerized application server deployments are expanding as Kubernetes-based environments increase operational flexibility by nearly 35% and reduce application release cycles by over 40%. Technology providers are strengthening partnerships around orchestration platforms, enabling enterprises to modernize workflows without fully replacing existing application ecosystems.

Security Architecture Modernization: Zero-trust integration and automated compliance controls are becoming critical as cybersecurity investments increase across enterprise platforms. Around 55% of organizations prioritize stronger application-layer protection, while regulatory changes in financial and healthcare sectors are driving vendors to embed security automation, identity controls, and continuous monitoring capabilities into application server solutions.

Cloud-Based Servers represent the leading segment as enterprises prioritize scalable infrastructure, faster deployment, and flexible resource management. Adoption has expanded as more than 60% of large organizations transition critical applications toward cloud-enabled environments, reducing infrastructure dependency and improving operational agility. Java Application Servers remain highly established due to their enterprise compatibility, mature ecosystem, and strong integration capabilities across banking and government applications. Open-Source Servers are gaining momentum with approximately 35% adoption growth among development-focused organizations seeking customization and lower licensing expenses.

.NET Application Servers continue supporting enterprises operating Microsoft-centric technology environments, while On-Premise Servers maintain relevance in highly regulated industries requiring direct infrastructure control. Companies are increasingly adopting hybrid strategies that combine cloud flexibility with on-premise security, shifting investment toward modular platforms and integrated application management solutions.

Enterprise Applications dominate the Application Server Market due to their role in managing complex business processes, internal workflows, and integrated digital operations. Large organizations allocate significant infrastructure resources toward enterprise platforms, with adoption exceeding 65% among global corporations seeking improved application reliability and automation. Banking Systems remain a highly demanding use case because transaction processing requires continuous availability, while Healthcare Systems are expanding rapidly through digital records, patient platforms, and secure data exchange.

E-commerce represents one of the fastest-growing application areas as businesses increase real-time processing, personalization, and automated customer services. Web Applications continue supporting broad digital access, but companies are shifting investment toward advanced application architectures capable of handling AI-driven workloads and high-volume transactions. Vendors are responding through specialized solutions, integration capabilities, and performance optimization partnerships.

IT & Telecom remains the leading end-user segment due to extensive infrastructure requirements, high application traffic volumes, and continuous platform modernization initiatives. More than 70% of telecom enterprises rely on advanced application environments to support digital services, network management, and customer-facing platforms. BFSI represents another major adoption area, driven by secure transaction processing, regulatory compliance, and demand for real-time financial services.

Healthcare is emerging as the fastest-growing end-user segment as hospitals and healthcare providers expand digital platforms, analytics systems, and connected care solutions. Retail organizations are increasing adoption through e-commerce integration and automated customer engagement, while Government entities focus on secure digital service delivery and infrastructure modernization. Companies are targeting these segments through customized platforms, strategic partnerships, and industry-specific application server capabilities.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 15.2% between 2026 and 2033.

Cloud-Native Enterprise Infrastructure Reshapes Deployment Strategies

North America maintains leadership in the Application Server Market due to strong enterprise cloud adoption, advanced software ecosystems, and large-scale digital infrastructure investments. The region contributes approximately 38% of global deployments, supported by financial services, technology companies, healthcare providers, and government modernization programs. More than 72% of large enterprises in the United States operate hybrid application environments, increasing demand for scalable server platforms. Companies are expanding AI integration, automation capabilities, and managed application services to improve operational efficiency. Strategic partnerships between cloud providers and enterprise software vendors are accelerating modernization across industries, particularly where application reliability and cybersecurity requirements are critical.

United States Market Outlook: The United States remains the primary regional contributor due to its concentration of technology enterprises, hyperscale data centers, and advanced software development capabilities. Nearly 75% of large organizations prioritize application modernization initiatives, with businesses investing in cloud-native platforms, automation tools, and secure application server architectures to support high-volume digital operations.

Regulatory Compliance Drives Secure Platform Modernization

Europe’s Application Server Market is shaped by strict data governance requirements, enterprise modernization programs, and demand for secure digital infrastructure. Countries such as Germany, the United Kingdom, and France are increasing adoption across manufacturing, banking, and public-sector applications. The region represents nearly 27% of global deployments, supported by industrial automation and digital transformation initiatives. More than 60% of European enterprises are upgrading application environments to improve compliance, interoperability, and operational efficiency. Companies are focusing on energy-efficient infrastructure, secure hybrid deployment models, and partnerships with technology providers to meet evolving regulatory expectations while maintaining competitive digital capabilities.

Germany Market Outlook: Germany leads European adoption through its industrial automation ecosystem, manufacturing strength, and enterprise software demand. Approximately 65% of large industrial companies are investing in digital infrastructure upgrades, creating opportunities for application server providers supporting smart manufacturing, enterprise resource planning, and secure industrial data management.

Enterprise Digital Expansion Accelerates Large-Scale Deployment

Asia-Pacific represents the fastest-transforming market due to rapid enterprise digitization, expanding cloud infrastructure, and increasing software development activity. China, India, Japan, and South Korea are driving deployment growth through financial technology, manufacturing automation, telecommunications expansion, and public digital platforms. The region contributes nearly 25% of global application server installations, with cloud adoption among enterprises increasing by over 50% in major economies. Companies are expanding local data infrastructure, forming technology partnerships, and investing in scalable application platforms to support rising digital workloads. Supply-chain diversification and regional technology investments are further strengthening application infrastructure development.

China Market Outlook: China remains a major contributor through large-scale cloud infrastructure, industrial digitalization, and domestic technology ecosystems. More than 70% of large enterprises are adopting advanced digital platforms, supported by investments in smart manufacturing, e-commerce systems, and high-performance application environments requiring reliable server infrastructure.

Digital Infrastructure Investment Expands Enterprise Adoption

South America is experiencing gradual application server adoption as enterprises modernize IT infrastructure and expand digital services across banking, retail, telecommunications, and government sectors. Brazil and Argentina represent key markets due to increasing cloud deployment and enterprise software demand. The region accounts for nearly 6% of global deployments, with cloud-based application adoption growing by approximately 35% among medium and large organizations. Infrastructure limitations, cybersecurity requirements, and investment constraints continue influencing deployment strategies. Companies are responding through managed services, localized partnerships, and flexible infrastructure models that reduce implementation complexity while improving access to advanced application technologies.

Brazil Market Outlook: Brazil represents the largest South American market due to its financial services sector, expanding digital economy, and enterprise technology investments. More than 50% of major businesses are increasing cloud infrastructure usage, creating demand for application servers supporting online banking, commerce platforms, and business automation systems.

Digital Transformation Programs Accelerate Infrastructure Development

Middle East & Africa is gaining momentum through government digital initiatives, data center expansion, and enterprise modernization projects. Countries including the United Arab Emirates, Saudi Arabia, and South Africa are increasing application server adoption across financial services, healthcare, government platforms, and telecommunications. The region contributes around 4% of global deployments, while enterprise cloud adoption has increased by nearly 40% through infrastructure modernization programs. Companies are investing in localized data facilities, cybersecurity capabilities, and strategic technology partnerships to support digital transformation objectives. Public-sector modernization and smart city initiatives are creating new demand for secure, scalable application platforms.

United Arab Emirates Market Outlook: The United Arab Emirates leads regional adoption through advanced digital infrastructure, smart government programs, and technology investment initiatives. More than 60% of government services operate through digital platforms, increasing demand for secure application servers that support high-availability services, data management, and automated enterprise workflows.

The Application Server Market features intense competition between global platform leaders such as Oracle, IBM, Microsoft, and Red Hat, alongside open-source specialists and regional technology providers. Global vendors compete through enterprise-grade platforms, while regional players focus on customization, cost efficiency, and localized support. The top five companies collectively control approximately 48% of the market, creating a moderately concentrated competitive structure. Competition is driven by technology capability, integration speed, security performance, and deployment flexibility, with AI automation improving operational efficiency by nearly 30% and cloud-native adoption increasing platform scalability by over 40%. Players are expanding through cloud partnerships, Kubernetes integration, cybersecurity enhancements, and industry-specific solutions. The market is shifting toward AI-enabled middleware and hybrid infrastructure leadership, creating pressure on traditional vendors. High technical expertise, ecosystem maturity, and enterprise trust remain major entry barriers. Winning requires continuous innovation, strong partnerships, and the ability to deliver secure, adaptable application platforms.

Oracle Corporation

IBM Corporation

Microsoft Corporation

Red Hat, Inc.

SAP SE

Fujitsu Limited

NEC Corporation

VMware, Inc.

TIBCO Software Inc.

Apache Software Foundation

Payara Services Ltd.

TmaxSoft Inc.

Application server technology is shifting from traditional middleware platforms toward cloud-native, AI-enabled, and container-based architectures. Kubernetes integration, microservices frameworks, and automated workload management are becoming core capabilities, with container adoption improving deployment speed by nearly 40% and reducing infrastructure management complexity by approximately 25%. Enterprises are replacing rigid application environments with flexible platforms that support continuous delivery and scalable digital services.

AI-driven application monitoring and predictive automation are transforming operational performance by reducing incident response times by around 35% and improving resource utilization by nearly 30%. Compared with legacy manual administration models, intelligent application management platforms provide faster optimization, stronger reliability, and improved cost control. Large technology providers and cloud-focused innovators benefit most by combining automation, security, and advanced analytics into unified application server ecosystems.

Between 2026 and 2028, edge computing integration, zero-trust security, and serverless application capabilities will influence enterprise deployment strategies. Organizations adopting these technologies earlier gain advantages through faster application delivery, improved resilience, and reduced operational overhead. The competitive focus is moving toward platforms that combine automation, interoperability, and intelligent infrastructure management rather than traditional server hosting capabilities.

March 2025 IBM enhanced WebSphere Application Server Liberty with continuous delivery updates, improving enterprise application lifecycle management through frequent releases. The platform introduced multiple quarterly updates supporting faster modernization and operational stability for cloud-native workloads.

October 2024 Oracle expanded its cloud application ecosystem with new generative AI capabilities integrated across enterprise applications, supporting more than 50 AI use cases. The innovation strengthened application platform competitiveness by improving automation, decision support, and enterprise workflow efficiency.

June 2025 Red Hat advanced its application platform strategy by strengthening cloud-native development capabilities through OpenShift ecosystem integration. The platform supported broader containerized application deployment, enabling enterprises to improve scalability and accelerate modernization across hybrid environments.

April 2025 Kubernetes ecosystem research highlighted increasing enterprise adoption of container orchestration for application deployment optimization. Organizations using Kubernetes-based environments improved workload scalability and operational control, accelerating application server modernization strategies across cloud and hybrid infrastructure models.

The Application Server Market Report covers comprehensive analysis across major types, including Java Application Servers, .NET Application Servers, Cloud-Based Servers, On-Premise Servers, and Open-Source Servers. The study evaluates applications such as enterprise applications, web applications, e-commerce platforms, banking systems, and healthcare systems, along with end-user adoption across IT & Telecom, BFSI, healthcare, retail, and government sectors.

The report provides regional insights across North America, Europe, Asia-Pacific, South America, and Middle East & Africa while examining key technologies including cloud-native platforms, AI-enabled management, containerization, automation, and cybersecurity integration. With analysis of more than 10 major industry participants and evolving deployment models, the report supports investment planning, competitive positioning, expansion decisions, and strategic technology alignment through 2033.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 29.08 Million |

Market Revenue in 2033 | USD 80.65 Million |

CAGR (2026 - 2033) | 13.6% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Oracle Corporation, IBM Corporation, Microsoft Corporation, Red Hat, Inc., SAP SE, Fujitsu Limited, NEC Corporation, VMware, Inc., TIBCO Software Inc., Apache Software Foundation, Payara Services Ltd., TmaxSoft Inc. |

Customization & Pricing | Available on Request (10% Customization is Free) |