Reports

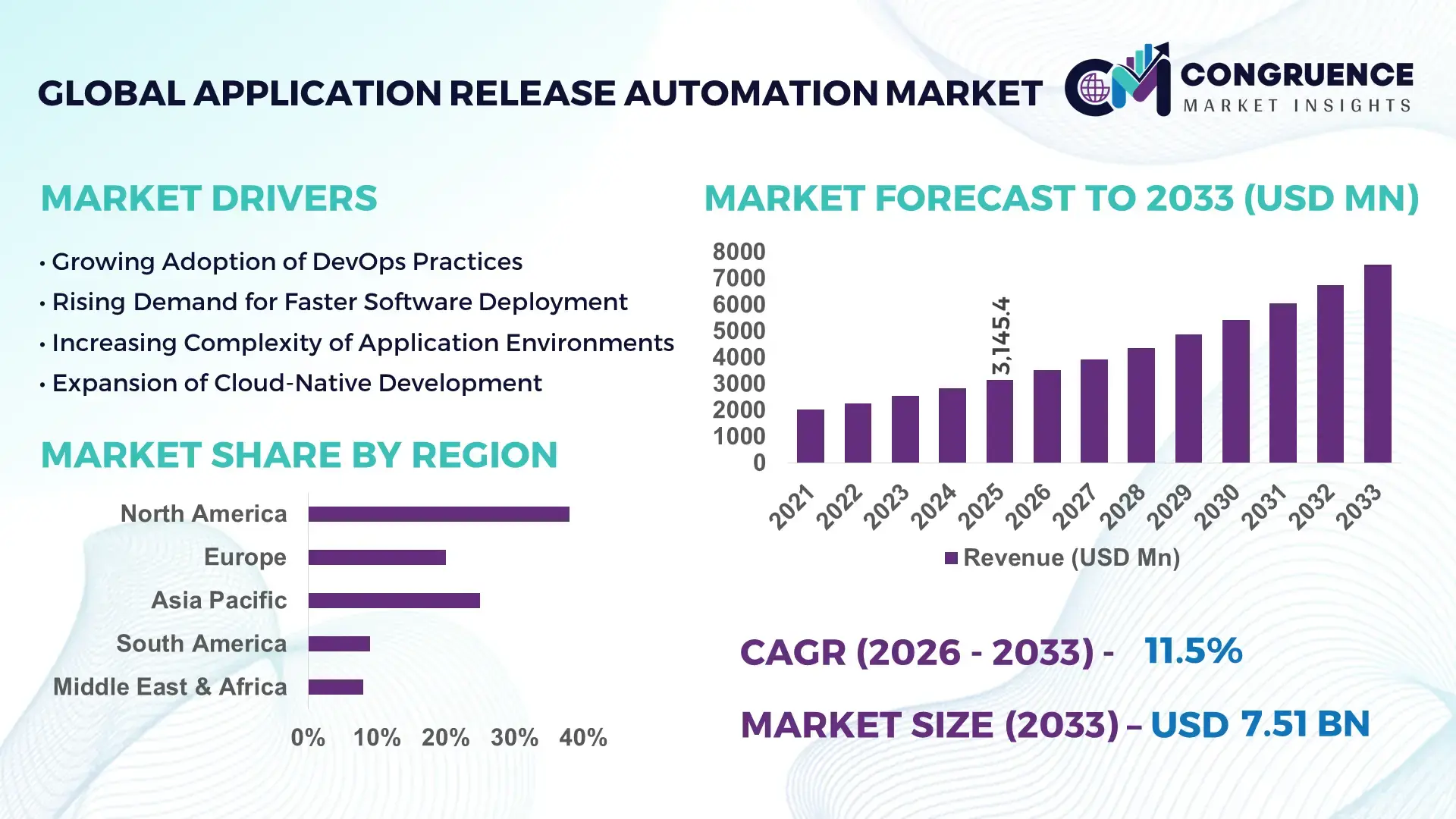

The Global Application Release Automation Market was valued at USD 3145.35 Million in 2025 and is anticipated to reach a value of USD 7513.96 Million by 2033 expanding at a CAGR of 11.5% between 2026 and 2033. The growth is primarily driven by the increasing need for faster software deployment cycles and continuous delivery capabilities across enterprise IT ecosystems.

The United States remains a major hub for Application Release Automation development and enterprise deployment, supported by large-scale cloud infrastructure, DevOps adoption, and enterprise software innovation. More than 78% of large enterprises in the U.S. have integrated DevOps pipelines that incorporate automated release management frameworks. The country hosts over 4,500 DevOps-focused technology providers and software integration firms delivering advanced release orchestration platforms. Additionally, enterprise spending on software lifecycle management tools surpassed USD 25 billion in 2024, indicating strong institutional investment in automated deployment technologies. The financial services and telecommunications sectors collectively account for nearly 42% of enterprise automation adoption in the country, while over 65% of cloud-native applications developed in the U.S. incorporate automated release pipelines for faster production deployment and operational scalability.

• Market Size & Growth: The Application Release Automation Market was valued at USD 3145.35 million in 2025 and is projected to reach USD 7513.96 million by 2033, expanding at a CAGR of 11.5%, driven by enterprise demand for accelerated DevOps pipelines and continuous software delivery frameworks.

• Top Growth Drivers: DevOps adoption expansion (68%), enterprise cloud migration initiatives (61%), and automated software deployment efficiency improvements (45%).

• Short-Term Forecast: By 2028, advanced automation platforms are expected to reduce application deployment time by 35% while lowering operational errors by nearly 28%.

• Emerging Technologies: AI-driven release orchestration, Kubernetes-based container deployment pipelines, and predictive release analytics are shaping next-generation automation platforms.

• Regional Leaders: North America projected to reach USD 2.8 billion by 2033 with strong enterprise DevOps adoption; Europe expected to reach USD 2.1 billion driven by digital transformation initiatives; Asia-Pacific forecast to reach USD 1.9 billion due to rapid software development outsourcing expansion.

• Consumer/End-User Trends: Large enterprises account for nearly 60% of deployments, with banking, telecommunications, and e-commerce sectors adopting automated release pipelines to support continuous integration and high-frequency software updates.

• Pilot or Case Example: In 2024, a major telecommunications infrastructure project deployed automated release pipelines that reduced application downtime by 32% and accelerated deployment cycles by 40%.

• Competitive Landscape: The market leader holds approximately 19% share, with major competitors including IBM, Microsoft, Broadcom, Red Hat, and Atlassian competing through cloud-native automation solutions.

• Regulatory & ESG Impact: Compliance requirements for secure DevOps pipelines and data governance standards are pushing organizations to adopt automated release validation and security scanning tools.

• Investment & Funding Patterns: Global investments exceeding USD 4.5 billion have recently been directed toward DevOps automation startups and enterprise deployment platforms.

• Innovation & Future Outlook: AI-assisted release validation, infrastructure-as-code integration, and self-healing deployment environments are expected to transform enterprise software lifecycle management in the coming decade.

The Application Release Automation Market is influenced by increasing digital transformation across banking, healthcare, telecommunications, and e-commerce sectors, which collectively account for a substantial portion of enterprise automation adoption. Financial services institutions contribute nearly 28% of platform demand due to strict release governance and high-frequency application updates. Recent innovations such as AI-assisted deployment validation, container orchestration integration, and automated rollback mechanisms have significantly improved software reliability. Regulatory requirements around data security and compliance monitoring are further driving adoption of automated testing and release management tools. Regional consumption patterns show strong adoption across North America and Europe, while Asia-Pacific is experiencing rapid expansion due to the growth of IT outsourcing, cloud computing ecosystems, and large-scale enterprise digitalization programs.

The Application Release Automation Market has become strategically important for enterprises seeking to accelerate digital transformation while maintaining operational stability across complex IT environments. Organizations deploying modern DevOps frameworks increasingly rely on automated release orchestration platforms to manage application updates, configuration management, and deployment across hybrid cloud infrastructures. Studies across enterprise software environments indicate that automated deployment pipelines reduce software release cycles by nearly 40%, enabling businesses to launch features faster and respond rapidly to changing market demands.

A comparative technology benchmark shows that AI-driven release orchestration delivers nearly 35% improvement in deployment efficiency compared to traditional manual release management processes. Modern automation frameworks integrate container orchestration, continuous integration pipelines, and infrastructure-as-code technologies to streamline application delivery while reducing operational errors. These advanced capabilities are particularly critical for industries such as financial services, telecommunications, and digital commerce, where software reliability and rapid feature updates are essential to maintaining competitiveness.

From a regional perspective, North America dominates in deployment volume due to mature DevOps ecosystems, while Europe leads in adoption intensity with nearly 72% of large enterprises integrating automated release management tools into their digital infrastructure. Meanwhile, the Asia-Pacific region is experiencing accelerated adoption driven by large technology outsourcing hubs and rapidly expanding cloud service providers.

Short-term projections indicate that by 2027, AI-enabled predictive deployment analytics will reduce software release failures by approximately 30% through automated error detection and rollback capabilities. Many organizations are also integrating ESG-aligned IT strategies by committing to a 25% reduction in data center operational waste and energy consumption through optimized automation processes by 2028.

The rapid expansion of DevOps practices across enterprise IT environments is one of the most significant drivers supporting the growth of the Application Release Automation Market. DevOps frameworks emphasize continuous integration, continuous delivery, and automated deployment pipelines to enable faster and more reliable software releases. Surveys across enterprise technology organizations reveal that nearly 74% of companies have adopted DevOps methodologies to improve application development and operational efficiency. Application Release Automation platforms play a central role in DevOps pipelines by orchestrating software deployments, managing configuration environments, and ensuring consistent releases across development, testing, and production systems. Enterprises implementing automated release management have reported deployment frequency improvements exceeding 40%, along with substantial reductions in configuration errors. Large technology firms and financial institutions frequently deploy hundreds of application updates each month, making manual release coordination impractical. Automated release management tools enable standardized workflows that integrate testing, approval processes, and deployment validation. This operational efficiency allows organizations to maintain service reliability while supporting rapid innovation. As more enterprises adopt agile development methodologies and microservices architectures, demand for sophisticated release automation platforms continues to expand globally.

Despite its advantages, the Application Release Automation Market faces constraints due to integration challenges associated with legacy IT infrastructure and complex enterprise environments. Many large organizations still operate legacy applications built on outdated architecture frameworks that are not easily compatible with modern automation platforms. Integrating these systems with automated deployment pipelines often requires extensive reconfiguration, specialized middleware, and significant implementation time. Research across enterprise IT environments shows that nearly 45% of companies report integration difficulties when introducing automation into legacy application infrastructures. These challenges can delay deployment projects and increase implementation costs, particularly in industries such as government services, healthcare, and traditional banking where older systems remain operational. Additionally, legacy systems often lack standardized APIs or containerized architecture, which limits the ability of automation platforms to perform seamless deployment orchestration. In some cases, enterprises must redesign portions of their application architecture before implementing automated release management tools. These technical limitations slow the adoption rate of advanced automation technologies and create operational barriers for organizations attempting to modernize complex software environments.

The rapid expansion of cloud-native application development presents significant opportunities for the Application Release Automation Market. Organizations increasingly build applications using microservices architectures, container technologies, and cloud infrastructure platforms, all of which require highly automated deployment pipelines to manage frequent updates and distributed computing environments. Industry statistics indicate that more than 65% of newly developed enterprise applications now utilize cloud-native architectures. These systems involve multiple interconnected services deployed across various cloud environments, requiring automated orchestration tools to manage application releases efficiently. Application Release Automation platforms enable organizations to coordinate deployment workflows across containers, virtual machines, and serverless environments. Cloud service providers and enterprise technology vendors are also integrating release automation features directly into DevOps toolchains, creating opportunities for enhanced platform interoperability. Automated deployment solutions that support Kubernetes, container orchestration, and infrastructure-as-code frameworks are gaining significant attention from technology organizations seeking to improve software scalability. As global cloud adoption continues expanding, the demand for sophisticated automation platforms capable of managing complex multi-cloud deployment environments is expected to grow substantially.

Security risks and regulatory compliance requirements present major challenges for organizations adopting Application Release Automation platforms. Automated deployment pipelines often handle sensitive application code, configuration data, and system credentials, making them potential targets for cybersecurity threats. If automation workflows are not properly secured, vulnerabilities can be introduced into production systems during the deployment process. Enterprise cybersecurity studies reveal that nearly 36% of security incidents in DevOps environments originate from misconfigured deployment pipelines or insufficient access control mechanisms. These vulnerabilities can expose organizations to data breaches, service disruptions, and regulatory penalties. Industries such as banking, healthcare, and government services face particularly strict compliance standards regarding software deployment and data protection. To address these concerns, organizations must integrate advanced security measures such as automated vulnerability scanning, encryption protocols, and identity-based access controls within their release automation frameworks. However, implementing these safeguards requires specialized expertise and additional infrastructure investment. Balancing deployment speed with strong cybersecurity protections remains one of the key operational challenges influencing the evolution of the Application Release Automation Market.

• Expansion of AI-Driven Deployment Intelligence: Artificial intelligence is increasingly embedded into Application Release Automation platforms to optimize deployment accuracy and operational monitoring. Approximately 63% of large enterprises now integrate AI-assisted release validation tools within their DevOps pipelines. These systems analyze deployment patterns, detect anomalies, and automatically trigger rollback actions when issues arise. Organizations implementing predictive deployment analytics report a 31% reduction in failed releases and a 27% improvement in system uptime. Automated root-cause analysis powered by machine learning has also reduced debugging time by nearly 40% in complex application environments. As organizations handle hundreds of deployments weekly, AI-driven automation is becoming a core component of enterprise-grade release orchestration platforms.

• Rapid Growth of Containerized Deployment Pipelines: The adoption of container technologies such as Docker and Kubernetes is significantly transforming release automation workflows. Nearly 68% of enterprise applications developed in 2024 were deployed through containerized infrastructure, requiring automated orchestration tools to manage application updates efficiently. Container-based release pipelines enable developers to deploy updates 45% faster while reducing configuration errors by approximately 30%. Enterprises operating large microservices environments report managing more than 1,000 automated deployments per month through container orchestration frameworks. This trend is particularly strong across financial services, telecommunications, and digital commerce platforms where software scalability and rapid feature releases are essential for operational competitiveness.

• Increasing Integration with DevSecOps Security Frameworks: Security-focused automation has become a defining trend in the Application Release Automation ecosystem as organizations prioritize secure software delivery. Around 57% of enterprises now integrate automated security testing and compliance checks directly into release pipelines. Automated vulnerability scanning tools can identify security flaws during deployment stages, reducing the risk of production vulnerabilities by nearly 35%. DevSecOps-enabled automation pipelines also ensure regulatory compliance through continuous monitoring and automated audit trails. Organizations operating in highly regulated sectors, including banking and healthcare, report a 28% reduction in security-related deployment incidents after integrating automated security validation processes into their release management frameworks.

• Growth of Multi-Cloud and Hybrid Infrastructure Automation: Enterprises increasingly deploy applications across hybrid and multi-cloud environments, creating demand for sophisticated release orchestration systems capable of managing complex deployment environments. Recent industry surveys indicate that 71% of large organizations operate workloads across at least two cloud platforms. Automated release orchestration platforms help coordinate deployments across private cloud, public cloud, and on-premise infrastructure while maintaining configuration consistency. Companies implementing hybrid-cloud release automation report up to 34% faster application deployment cycles and a 29% improvement in infrastructure utilization. This trend reflects the growing need for centralized automation platforms capable of managing distributed enterprise IT environments efficiently.

The Application Release Automation market is segmented based on deployment type, application areas, and end-user industries, each reflecting specific adoption patterns within enterprise software ecosystems. Deployment types generally include cloud-based automation platforms, on-premise release orchestration systems, and hybrid deployment frameworks designed for multi-cloud environments. Cloud-based platforms account for a large proportion of modern implementations due to scalability and ease of integration with DevOps pipelines. Application areas vary widely, with banking and financial services, telecommunications, retail technology, and healthcare software development representing major deployment environments. End-user segmentation highlights strong adoption among large enterprises operating complex application infrastructures, while mid-sized organizations increasingly deploy automation tools to accelerate digital transformation initiatives. Across regions, adoption patterns show strong enterprise implementation in North America and Europe, while Asia-Pacific demonstrates expanding usage due to IT outsourcing growth and rising cloud adoption among technology service providers.

Application Release Automation solutions are commonly categorized into cloud-based platforms, on-premise deployment systems, and hybrid release automation environments designed to support complex enterprise infrastructure. Cloud-based automation platforms currently dominate the segment, accounting for nearly 54% of adoption, as organizations increasingly migrate application development pipelines to scalable cloud infrastructure. These platforms allow teams to coordinate deployment workflows across distributed environments while maintaining centralized control and monitoring capabilities. Cloud deployment also supports rapid integration with container orchestration technologies and infrastructure-as-code frameworks, improving deployment efficiency by nearly 32% compared to traditional systems. On-premise release automation platforms continue to hold approximately 26% of enterprise implementations, particularly among government institutions, defense agencies, and highly regulated financial organizations that require strict data control and security governance. Although this segment is smaller, it remains critical for organizations operating legacy IT infrastructure and internal application environments. Hybrid release automation environments represent the fastest-growing segment, expanding at an estimated 14.2% CAGR due to rising enterprise adoption of multi-cloud architectures. Hybrid systems allow organizations to orchestrate deployments across private infrastructure and multiple cloud platforms simultaneously, enabling operational flexibility and redundancy. Other niche automation deployment models collectively contribute around 20% of the market, including specialized DevOps integration tools and industry-specific release orchestration platforms.

The Application Release Automation market spans multiple enterprise software environments including banking and financial services, telecommunications, retail and e-commerce platforms, healthcare systems, and IT services development operations. Among these, the banking and financial services sector accounts for approximately 34% of overall adoption, driven by the need to manage frequent updates across digital banking platforms, payment gateways, and financial data processing systems. Financial institutions deploy automated release pipelines to ensure system reliability while supporting thousands of daily transactions and real-time service updates. The telecommunications sector represents about 22% of automation deployments, as telecom operators continuously upgrade network management systems, customer service platforms, and billing applications. Automated deployment systems help telecom companies release software updates without disrupting critical network services. Retail and e-commerce platforms account for roughly 18% of applications, primarily driven by the need to deploy frequent feature updates and maintain high system performance during peak transaction periods. Healthcare software environments represent approximately 12% of deployments, where automation tools support secure release of patient data management and diagnostic software platforms. The fastest-growing application segment is IT services and cloud platform development, expanding at an estimated 15.1% CAGR due to increasing demand for continuous software delivery and cloud-native application development.

End-user segmentation within the Application Release Automation market includes large enterprises, small and medium-sized enterprises (SMEs), government institutions, and technology service providers. Large enterprises dominate the market with approximately 58% adoption, as these organizations operate extensive application portfolios requiring frequent updates across multiple IT environments. Enterprises in sectors such as banking, telecommunications, and global e-commerce platforms often manage hundreds of software releases each month, making automated deployment orchestration essential for maintaining system stability and operational efficiency. Small and medium-sized enterprises account for nearly 24% of adoption, reflecting growing interest in automation tools that support faster software development and improved operational agility. SMEs increasingly implement cloud-based automation platforms due to lower infrastructure requirements and easier integration with modern DevOps toolchains. Technology service providers represent the fastest-growing end-user segment, expanding at an estimated 16.3% CAGR as IT outsourcing firms manage large volumes of software deployments for global clients. These organizations utilize advanced release automation frameworks to coordinate deployments across multiple client environments and geographic regions. Government agencies and public sector organizations collectively contribute around 18% of the market, particularly in national digital infrastructure programs and large-scale public service software platforms.

Region North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 13.8% between 2026 and 2033.

Regional dynamics in the Application Release Automation market are strongly linked to enterprise cloud adoption, DevOps maturity, and large-scale digital transformation programs. North America leads due to advanced software ecosystems where more than 70% of large enterprises operate automated CI/CD pipelines and manage over 500 deployment cycles annually. Europe follows with approximately 27% market share, supported by strong enterprise software sectors across Germany, the United Kingdom, and France, where over 55% of organizations deploy DevOps automation tools. Asia-Pacific holds nearly 23% share, driven by rapid digital platform expansion across China, India, and Japan. Over 40% of new enterprise applications in the region are deployed through automated release pipelines integrated with cloud infrastructure. South America contributes roughly 7%, led by Brazil’s banking and telecom sectors, while the Middle East & Africa account for around 5%, supported by government-led digital infrastructure modernization and expanding enterprise cloud adoption.

How Are DevOps-Driven Enterprises Accelerating Automated Software Releases?

North America holds around 38% share of the Application Release Automation market, supported by strong enterprise technology adoption and advanced cloud infrastructure. The United States accounts for nearly 80% of regional deployments, driven by software-intensive sectors such as financial services, healthcare technology, and large-scale e-commerce platforms. Over 68% of enterprises in the region use integrated DevOps pipelines to manage frequent application updates and maintain high system availability. Government-backed digital modernization programs and cybersecurity regulations are encouraging automation adoption in federal and public sector IT systems. Technological advancements such as AI-assisted deployment monitoring and automated rollback tools have improved deployment success rates by nearly 30% across enterprise systems. A notable regional player, Digital.ai, continues expanding its release orchestration platform used by global financial institutions to manage thousands of automated deployments annually. Consumer behavior in the region reflects high enterprise reliance on automation within healthcare and financial services where uninterrupted application availability is critical.

How Are Compliance and Enterprise Cloud Strategies Transforming Automated Deployment?

Europe represents approximately 27% of the global Application Release Automation market, with strong adoption across Germany, the United Kingdom, and France. Germany alone contributes nearly 24% of regional enterprise deployments, supported by its advanced industrial software ecosystem and strong IT services sector. Across the region, more than 55% of large enterprises operate DevOps-based automation pipelines to manage complex application updates. Strict regulatory frameworks related to data protection and digital governance are encouraging organizations to adopt automated release management platforms that maintain detailed audit trails and compliance monitoring. Emerging technologies such as container orchestration and hybrid cloud deployment systems are widely integrated into release automation workflows. A notable European company, Micro Focus, continues expanding enterprise automation solutions used by banking and telecommunications firms to manage high-volume deployment environments. Regional adoption trends show strong demand for explainable and secure automation systems due to regulatory oversight and enterprise compliance requirements.

How Are Rapid Digital Economies Accelerating Automated Software Deployment?

Asia-Pacific ranks among the fastest expanding regions in the Application Release Automation market, holding nearly 23% of global adoption volume. China, India, and Japan represent the largest consuming countries, collectively accounting for over 65% of regional enterprise deployments. Rapid expansion of digital platforms, cloud computing infrastructure, and large-scale e-commerce ecosystems is fueling demand for automated release management tools. Technology innovation hubs in cities such as Shenzhen, Bengaluru, and Tokyo are driving enterprise software development activity. More than 45% of new digital applications in the region are deployed through automated CI/CD pipelines integrated with cloud-native infrastructure. Regional technology companies are investing heavily in DevOps automation platforms to support high-frequency deployment cycles. For example, Huawei Cloud continues expanding enterprise DevOps services used by large telecommunications and digital commerce companies. Consumer behavior across the region shows strong adoption driven by mobile-first digital services and large-scale e-commerce platforms.

How Is Enterprise Digital Transformation Expanding Automated Software Deployment?

South America accounts for roughly 7% of the global Application Release Automation market, with Brazil representing nearly 60% of regional adoption. Brazil and Argentina lead regional deployment activity, particularly within financial services, telecommunications, and media technology platforms. Banking institutions across Brazil manage thousands of daily digital transactions, requiring automated release orchestration tools to maintain system reliability during frequent application updates. Government initiatives supporting digital financial services and cloud adoption are contributing to enterprise software modernization across the region. Infrastructure expansion in telecommunications networks is also creating demand for automated deployment platforms capable of managing complex software updates. A regional technology company, TOTVS, is actively expanding enterprise DevOps and automation platforms to support business software deployment across Latin American enterprises. Consumer behavior trends indicate growing demand for localized digital applications and multilingual media platforms, which require frequent automated software releases.

How Are National Digital Transformation Programs Driving Software Automation?

The Middle East & Africa region contributes approximately 5% of the global Application Release Automation market, supported by large-scale digital transformation initiatives across the United Arab Emirates, Saudi Arabia, and South Africa. Government-led smart infrastructure programs and national digital economy strategies are encouraging enterprises to modernize software development environments. Industries such as oil and gas, financial services, and telecommunications are adopting automated release platforms to manage complex enterprise applications. Over 35% of enterprise software deployments in the Gulf region are now integrated with automated DevOps pipelines to improve system reliability and deployment speed. Cloud computing expansion and technology investment zones in cities like Dubai and Riyadh are accelerating innovation in enterprise software delivery. Regional technology service providers such as Injazat are expanding digital transformation services that include automated application deployment and infrastructure management. Consumer adoption across the region is strongly linked to government digital services and expanding fintech platforms.

• United States – 33% share in the Application Release Automation market due to large enterprise software ecosystems, extensive cloud infrastructure, and high DevOps adoption across finance, healthcare, and technology industries.

• China – 16% share in the Application Release Automation market supported by rapid digital platform expansion, large-scale e-commerce ecosystems, and strong government investment in cloud computing infrastructure.

The Application Release Automation market features a moderately fragmented competitive landscape with more than 40 active global technology providers offering release orchestration and DevOps automation solutions. The top five companies collectively control nearly 46% of the market, reflecting strong enterprise demand for established automation platforms integrated with cloud infrastructure and CI/CD pipelines.

Major vendors focus heavily on expanding automation capabilities through artificial intelligence, predictive deployment analytics, and hybrid cloud compatibility. Strategic partnerships between DevOps tool providers and major cloud platforms have increased significantly, with more than 120 new technology collaborations announced between 2023 and 2025 to enhance automation ecosystems. Product innovation also remains a major competitive factor, as vendors introduce advanced deployment analytics and automated compliance monitoring tools designed for highly regulated industries.

Mergers and acquisitions are shaping the competitive environment as larger software vendors acquire niche automation providers to strengthen their DevOps portfolios. Enterprise demand for scalable release management solutions has encouraged vendors to expand SaaS-based automation platforms capable of managing thousands of application deployments per day across distributed infrastructure. Continuous integration with container orchestration systems and microservices environments is becoming a key differentiator among market leaders.

IBM Corporation

Micro Focus

Digital.ai

Broadcom Inc.

BMC Software

Electric Cloud

Red Hat

Atlassian

Puppet

Chef Software

XebiaLabs

CloudBees

Technological innovation is a defining force shaping the evolution of the Application Release Automation market as enterprises increasingly prioritize rapid, secure, and reliable software delivery. Modern release automation platforms integrate deeply with continuous integration and continuous deployment (CI/CD) pipelines, enabling organizations to manage complex application deployments across cloud, hybrid, and on-premise infrastructure. More than 65% of enterprise development teams now rely on automated release orchestration tools to coordinate multi-stage deployment processes across testing, staging, and production environments.

Containerization technologies such as Kubernetes have significantly influenced automation strategies. Enterprise environments now operate hundreds to thousands of microservices-based applications, requiring sophisticated orchestration tools capable of coordinating simultaneous software updates across distributed systems. Automated container deployment frameworks have reduced application rollout times by nearly 40%, while minimizing configuration inconsistencies across environments.

Artificial intelligence is also emerging as a transformative capability within release automation platforms. AI-driven deployment monitoring systems analyze historical release data to predict potential failures before deployment occurs. Enterprises implementing predictive release analytics report a 31% reduction in failed deployments and a 28% decrease in system downtime during application upgrades. Machine learning models are also being applied to automatically optimize deployment sequences and resource allocation.

Security automation is another critical technology trend. DevSecOps frameworks now embed automated vulnerability scanning and compliance verification directly within release pipelines. Approximately 58% of enterprises integrate automated security testing before application deployment, ensuring regulatory compliance and reducing the risk of production vulnerabilities. These technologies collectively enable organizations to maintain high software reliability while supporting increasingly rapid development cycles.

• In May 2025, IBM enhanced its DevOps automation portfolio by integrating advanced deployment orchestration capabilities within the IBM Cloud Continuous Delivery platform. The update introduced AI-assisted deployment monitoring and automated rollback features designed to reduce deployment failures across large-scale enterprise application environments. Source: www.ibm.com

• In September 2024, Digital.ai released an updated version of its Release platform featuring enhanced pipeline orchestration, security compliance tracking, and hybrid-cloud deployment support. The update enables enterprises to coordinate thousands of software deployments across complex infrastructure environments through automated governance and analytics.

• In July 2024, Broadcom expanded its enterprise DevOps solutions by enhancing automation capabilities within its software delivery portfolio. The improvements introduced advanced release orchestration and automated testing integration designed to support high-frequency deployment pipelines for financial and telecommunications platforms. Source: www.broadcom.com

• In March 2025, CloudBees introduced new capabilities within its CI/CD automation platform enabling enterprise teams to manage large-scale multi-cloud deployment pipelines. The update improves release governance and operational visibility while supporting container-based deployment frameworks used in modern cloud-native application development.

The Application Release Automation Market Report provides a comprehensive analysis of the global ecosystem supporting automated software deployment and DevOps orchestration technologies. The report evaluates more than 10 major technology segments covering release orchestration tools, deployment automation frameworks, CI/CD pipeline management systems, and hybrid cloud deployment platforms. It examines adoption trends across five major geographic regions and over 20 key countries, offering a detailed perspective on enterprise digital transformation and software delivery modernization.

The scope includes segmentation based on deployment models such as cloud-based, on-premise, and hybrid automation platforms, each supporting different enterprise infrastructure environments. The report also analyzes application-level adoption across critical sectors including financial services, telecommunications, healthcare technology, retail and e-commerce, and IT services development. These industries collectively account for more than 75% of enterprise software deployment automation activity, reflecting their reliance on continuous digital service delivery.

Technology coverage extends to emerging innovations such as AI-assisted release analytics, container orchestration integration, DevSecOps security automation, and infrastructure-as-code frameworks. The report evaluates the impact of these technologies on deployment speed, operational reliability, and enterprise software lifecycle management.

Additionally, the report examines over 40 global technology vendors involved in release automation platforms, highlighting product capabilities, innovation strategies, and enterprise adoption patterns. It also reviews enterprise usage metrics including automated deployment frequency, infrastructure scalability requirements, and integration with modern cloud-native development environments. The report further explores niche market segments such as automation platforms for microservices architecture, large-scale container deployment environments, and government digital infrastructure programs supporting automated software delivery systems.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

11.5% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

IBM Corporation, Micro Focus, Digital.ai, Broadcom Inc., BMC Software, Electric Cloud, Red Hat, Atlassian, Puppet, Chef Software, XebiaLabs, CloudBees |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |