Reports

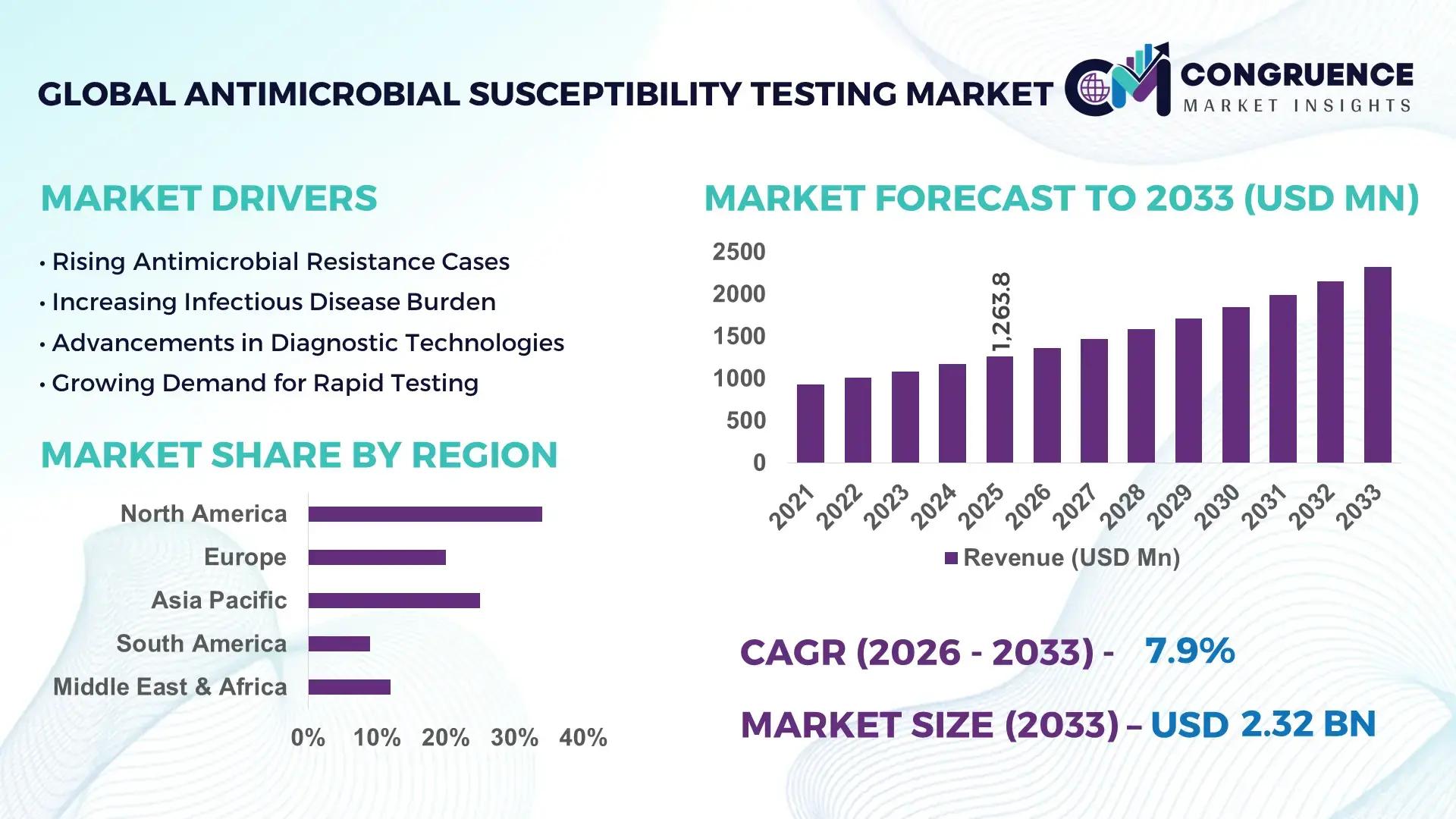

The Global Antimicrobial Susceptibility Testing Market was valued at USD 1263.78 Million in 2025 and is anticipated to reach a value of USD 2151.9 Million by 2033 expanding at a CAGR of 7.9% between 2026 and 2033. Growth is accelerating through rapid hospital adoption of automated AST platforms, rising multidrug-resistant infections, and stricter antimicrobial stewardship mandates across clinical laboratories and pharmaceutical manufacturing networks.

The United States accounted for approximately 34% of global antimicrobial susceptibility testing demand in 2025, supported by over USD 1.8 billion in infectious disease surveillance investments and advanced automation penetration exceeding 62% across tertiary laboratories. Germany maintained stronger per-capita microbiology testing density than China, while China expanded local AST instrument manufacturing capacity by nearly 18% amid regional healthcare localization initiatives linked to post-pandemic supply-chain resilience programs and WHO antimicrobial resistance containment priorities in 2026.

Market leaders are prioritizing AI-integrated diagnostic workflows, regional manufacturing expansion, and rapid-result testing portfolios to secure procurement contracts and reduce laboratory turnaround dependency.

Market Size & Growth: USD 1263.78 Million in 2025 reaching USD 2151.9 Million by 2033, driven by automated microbiology platforms and accelerated antimicrobial stewardship adoption at 7.9% CAGR.

Top Growth Drivers: Hospital-acquired infection testing demand rose 21%, automated AST deployment increased 18%, and rapid diagnostic adoption expanded 24% globally during 2025–2026.

Short-Term Forecast: By 2027, automated AST workflows are projected to reduce laboratory reporting time by 32% and improve pathogen identification efficiency by 27%.

Emerging Technologies: AI-assisted interpretation, microfluidics, and cloud-connected diagnostic systems improved testing throughput by 29% across advanced clinical laboratories.

Regional Leaders: North America surpassed USD 540 Million with strong hospital digitization, Europe exceeded USD 410 Million through stewardship mandates, and Asia-Pacific crossed USD 360 Million via local manufacturing expansion.

Consumer/End-User Trends: Nearly 58% of tertiary hospitals integrated automated susceptibility analyzers to manage multidrug-resistant bacterial outbreaks more effectively.

Pilot/Case Example: In 2026, a multi-hospital rapid AST deployment project lowered antibiotic misuse rates by 19% and reduced ICU reporting delays by 26%.

Competitive Landscape: Leading manufacturers controlled approximately 47% market share, with competition centered on automation speed, reagent compatibility, and integrated software ecosystems.

Regulatory & ESG Impact: Updated antimicrobial resistance policies improved standardized laboratory compliance by 31% while reducing repeat culture waste volumes by 14%.

Investment & Funding: Global sector investments exceeded USD 820 Million in 2025, led by diagnostic partnerships, regional production facilities, and infectious disease innovation programs.

Innovation & Future Outlook: Next-generation phenotypic AST and sequencing-linked diagnostics are shortening clinical decision timelines by nearly 40%, strengthening precision infection management strategies.

Antimicrobial susceptibility testing demand is intensifying across hospitals, pharmaceutical quality-control laboratories, and public health surveillance networks as rapid resistance detection becomes operationally critical. AI-enabled AST software and microfluidic diagnostic platforms improved reporting accuracy by nearly 28% in 2026, while localized reagent manufacturing expanded amid global supply-chain restructuring. Emerging economies are accelerating automated laboratory modernization, creating a stronger foundation for strategic capacity expansion and competitive differentiation.

Antimicrobial susceptibility testing is becoming strategically critical as healthcare systems confront rising multidrug-resistant infections, tighter antibiotic stewardship mandates, and increasing pressure to shorten clinical decision cycles. Large hospital networks and diagnostic providers are restructuring procurement toward integrated AST platforms capable of delivering standardized results across decentralized laboratories. In 2026, automated microbiology infrastructure upgrades accelerated across the United States and Japan, while localized reagent manufacturing gained traction following global diagnostic supply-chain disruptions and stricter infectious disease surveillance frameworks.

Advanced automated AST systems now deliver reporting turnaround improvements of nearly 35% compared with conventional manual disk diffusion workflows while reducing repeat testing volumes by approximately 22%. Germany maintains higher laboratory automation density and interoperability adoption than India, whereas India is scaling deployment rapidly through public-private laboratory modernization initiatives and digital pathology integration. Over the next two to three years, AI-assisted interpretation tools are expected to penetrate more than 45% of tertiary-care microbiology laboratories, improving workflow consistency and technician productivity.

A 2026 multi-hospital deployment in South Korea integrated cloud-connected AST analyzers with hospital information systems, lowering broad-spectrum antibiotic misuse by 18% within one year. Diagnostic companies are responding through regional manufacturing expansion, software partnerships, and rapid-testing portfolio diversification to secure long-term procurement agreements and strengthen competitive positioning in high-volume clinical networks.

Hospital systems are accelerating automated antimicrobial susceptibility testing deployment to reduce diagnostic delays, improve antimicrobial stewardship compliance, and manage rising resistant pathogen volumes. Automated AST penetration across tertiary laboratories increased by nearly 24% in 2025–2026, while rapid-result platforms reduced reporting times by approximately 30% compared with legacy workflows. In the United States, federal infectious disease preparedness programs and stricter stewardship protocols are pushing laboratories toward integrated microbiology automation ecosystems. This shift is directly improving laboratory throughput and reducing manual interpretation variability. Companies are expanding manufacturing capacity, investing in AI-assisted interpretation software, and forming hospital network partnerships to secure recurring consumables demand. A notable strategic shift involves bundled analyzer-reagent contracts, enabling vendors to strengthen long-term procurement control while reducing customer switching rates.

High automation costs and fragmented laboratory infrastructure continue limiting scalable antimicrobial susceptibility testing deployment across mid-tier healthcare facilities. Advanced automated AST systems require capital investments that remain nearly 38% higher than conventional microbiology setups, while imported reagent dependency increased procurement volatility by approximately 17% during recent supply-chain disruptions. In Brazil and South Africa, inconsistent cold-chain logistics and limited laboratory interoperability are extending implementation timelines and increasing operational inefficiencies. These constraints directly pressure diagnostic margins and delay modernization programs in cost-sensitive healthcare systems. Companies are mitigating risks through localized reagent production, long-term distributor agreements, and modular analyzer designs with lower maintenance intensity. A critical operational insight is that facilities prioritizing hybrid semi-automated platforms are achieving faster deployment scalability without full infrastructure replacement costs.

AI-enabled antimicrobial susceptibility testing platforms are creating high-value opportunities through faster pathogen interpretation, workflow automation, and decentralized laboratory deployment. AI-assisted systems improved result standardization accuracy by approximately 28% in 2026, while cloud-connected microbiology platforms reduced manual data entry workloads by nearly 33%. China and India are expanding smart laboratory infrastructure through digital healthcare modernization programs and domestic diagnostic manufacturing incentives. Simultaneously, next-generation phenotypic AST combined with genomic sequencing is accelerating targeted therapy optimization for critical-care environments. Companies are increasing R&D spending, building software ecosystems, and partnering with hospital IT providers to strengthen interoperability capabilities. A non-obvious strategic opportunity is emerging in outpatient diagnostic chains, where compact automated AST platforms are enabling faster same-day infection management and reducing tertiary hospital testing congestion.

Long-term market scalability is increasingly constrained by integration complexity between automated AST platforms, laboratory information systems, and hospital digital infrastructure. Nearly 31% of laboratories implementing advanced microbiology automation reported interoperability delays in 2025, while skilled microbiology workforce shortages increased system underutilization rates by approximately 19%. In the United Kingdom and Canada, cybersecurity compliance requirements for cloud-connected diagnostic systems are extending validation cycles and increasing operational oversight costs. These execution pressures affect deployment consistency, data reliability, and multi-site laboratory standardization efforts. Companies must strengthen software integration capabilities, expand workforce training programs, and invest in secure digital architecture to maintain operational continuity. A major strategic challenge involves balancing high-throughput automation with flexible laboratory customization requirements across fragmented healthcare procurement environments.

• AI-Guided Workflow Acceleration Automated antimicrobial susceptibility testing platforms integrated with AI-assisted interpretation reduced result validation time by nearly 34% in 2026, while laboratory throughput improved by approximately 27%. Large hospital systems in the United States are restructuring microbiology workflows to offset technician shortages and rising resistant pathogen loads. Vendors are scaling cloud-based analytics partnerships and embedding decision-support software directly into diagnostic platforms to improve reporting consistency and lower manual review dependency.

• Localized Reagent Manufacturing Expansion Diagnostic manufacturers in India and China increased localized AST consumable production by nearly 21% following persistent global logistics disruptions and stricter procurement localization policies. Import substitution strategies reduced average reagent lead times by approximately 18%, improving operational continuity for high-volume laboratories. Companies are expanding regional production hubs, renegotiating distributor agreements, and prioritizing dual-sourcing models to stabilize supply-chain exposure and protect recurring consumables demand.

• Rapid Phenotypic Testing Adoption Rapid phenotypic AST systems shortened bloodstream infection response timelines by approximately 30% compared with conventional culture workflows, driving stronger adoption across intensive-care networks. In Germany, tertiary hospitals expanded same-day susceptibility testing deployment to reduce unnecessary broad-spectrum antibiotic usage. Companies are responding through automated analyzer scaling, integrated sample preparation systems, and hospital alliance programs targeting high-acuity infectious disease management environments.

• Decentralized Diagnostic Network Integration Multi-site diagnostic chains are connecting AST analyzers directly with centralized laboratory information systems, improving data harmonization rates by nearly 25% and reducing duplicate reporting workflows by 16%. Regulatory pressure around antimicrobial stewardship reporting in Japan and the United Kingdom accelerated interoperability investments during 2025–2026. Vendors are prioritizing API-enabled platforms, cybersecurity-focused software upgrades, and enterprise-wide deployment contracts to strengthen long-term institutional integration capabilities.

Automated Testing remains the leading segment due to higher laboratory throughput, lower manual interpretation variability, and seamless integration with hospital information systems. Large tertiary hospitals and centralized diagnostic laboratories increased automated AST deployment by approximately 24% during 2025–2026 as infectious disease testing volumes intensified. Automated platforms also reduced reporting turnaround time by nearly 30% compared with Manual Testing workflows, strengthening operational efficiency in high-volume microbiology environments. Disk Diffusion continues to retain relevance in cost-sensitive laboratories because of lower infrastructure requirements, particularly across mid-tier facilities in Southeast Asia and Latin America. Broth Dilution remains strategically important for reference laboratories handling precision antimicrobial sensitivity analysis and pharmaceutical validation procedures.

Molecular Testing is emerging as the fastest-growing type as healthcare systems prioritize rapid pathogen identification and resistance gene detection. Adoption of molecular-integrated AST workflows increased by approximately 19% in 2026, especially across critical-care and bloodstream infection management programs. Companies are expanding AI-enabled analyzer portfolios, strengthening reagent partnerships, and investing in compact rapid-testing systems to capture decentralized laboratory demand. Manual Testing is gradually shifting toward hybrid semi-automated workflows as facilities seek lower-cost modernization without complete infrastructure replacement.

Bacterial Infections represent the dominant application segment due to consistently high clinical testing volumes, multidrug-resistant organism surveillance requirements, and expanding antimicrobial stewardship mandates. Hospitals and diagnostic laboratories increased bacterial susceptibility testing utilization by nearly 22% during 2025–2026 as healthcare systems prioritized earlier targeted therapy selection. Respiratory Infections continue generating strong demand following expanded post-pandemic infectious disease monitoring programs, while Urinary Tract Infections maintain stable testing volumes through routine outpatient and inpatient diagnostic workflows. Fungal Infections are gaining clinical attention in immunocompromised patient management, particularly across advanced oncology and transplant centers.

Bloodstream Infections are emerging as the fastest-growing application due to the operational urgency associated with sepsis management and ICU mortality reduction initiatives. Rapid AST deployment for bloodstream infection workflows improved antibiotic optimization timelines by approximately 28% in several high-acuity hospital networks. Companies are expanding integrated blood culture compatibility, automated sample processing, and rapid-result testing portfolios to strengthen critical-care positioning. Demand is increasingly shifting toward high-speed susceptibility testing capable of supporting same-day clinical intervention and reducing broad-spectrum antibiotic overuse across emergency and intensive-care environments.

Hospitals remain the dominant end-user segment due to large-scale microbiology testing requirements, continuous infectious disease monitoring, and intensive-care diagnostic dependency. More than 58% of high-capacity hospitals upgraded automated AST infrastructure during 2025–2026 to improve laboratory turnaround efficiency and strengthen antimicrobial stewardship reporting. Diagnostic Laboratories are expanding rapidly through centralized high-volume processing models and multi-site integration strategies, particularly in India and the United States. Pharmaceutical Companies continue utilizing AST platforms for antimicrobial drug development and resistance profiling, while Research Institutes and Academic Institutions maintain demand through clinical microbiology studies and resistance surveillance programs.

Diagnostic Laboratories represent the fastest-growing end-user category as healthcare systems consolidate microbiology testing operations to reduce operational duplication and improve workflow standardization. Integrated laboratory networks improved sample processing efficiency by approximately 26% through automation and digital interoperability investments. Companies are targeting these buyers through scalable analyzer configurations, subscription-based reagent contracts, and enterprise software integration services. Clinics are gradually adopting compact semi-automated AST systems to support outpatient infectious disease management, creating new decentralized deployment opportunities for vendors focused on lower-footprint diagnostic infrastructure.

North America accounted for the largest market share at 38.4% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.1% between 2026 and 2033.

Advanced Laboratory Automation Driving Clinical Standardization

North America maintains leadership through large-scale automated microbiology infrastructure, strong antimicrobial stewardship compliance, and high deployment concentration across tertiary healthcare systems. The region accounted for approximately 38% of global automated AST installations in 2025, supported by integrated laboratory information systems and expanding rapid diagnostic adoption. Hospital networks across the United States and Canada accelerated AI-assisted microbiology deployment to reduce reporting delays and improve resistant pathogen surveillance. In 2026, multiple enterprise laboratory partnerships expanded cloud-connected AST integration across multi-site hospital systems, improving workflow harmonization by nearly 24%. Diagnostic manufacturers are prioritizing reagent localization, cybersecurity-ready software platforms, and high-throughput analyzer expansion to strengthen institutional procurement positioning and operational continuity.

United States Market Outlook: The United States leads the regional market through extensive infectious disease testing infrastructure, advanced hospital digitization, and strong enterprise-level microbiology automation. More than 62% of tertiary laboratories integrated automated AST workflows by 2026, supported by federal antimicrobial resistance monitoring programs and growing ICU diagnostic demand. Domestic manufacturers are strengthening regional reagent production capacity and expanding interoperability-focused software ecosystems to support large multi-hospital procurement contracts and same-day susceptibility testing initiatives.

Regulatory Harmonization Accelerating Diagnostic Modernization

Europe is strengthening antimicrobial susceptibility testing deployment through standardized stewardship regulations, hospital laboratory modernization, and integrated infectious disease surveillance frameworks. Germany, France, and the United Kingdom collectively represented over 56% of regional AST deployment activity in 2025 due to advanced microbiology infrastructure and centralized public healthcare procurement systems. Automated susceptibility testing adoption increased by approximately 21% across major European hospital laboratories following stricter antimicrobial resistance reporting requirements. Regional diagnostic providers are prioritizing energy-efficient analyzers, digital interoperability upgrades, and rapid phenotypic testing expansion to improve operational consistency. Enterprise partnerships between laboratory networks and diagnostic technology suppliers are also accelerating standardized multi-site workflow integration across public healthcare systems.

Germany Market Outlook: Germany remains the region’s most strategically significant market due to its dense hospital laboratory network, high microbiology automation penetration, and strong industrial diagnostic manufacturing base. Nearly 68% of high-capacity clinical laboratories implemented integrated AST platforms by 2026 to strengthen antimicrobial stewardship reporting and laboratory efficiency. German healthcare systems are also investing in rapid bloodstream infection diagnostics and cloud-enabled laboratory management systems to improve cross-network infectious disease monitoring capabilities.

Localized Manufacturing and High-Volume Deployment Expansion

Asia-Pacific is emerging as the fastest-scaling antimicrobial susceptibility testing market due to expanding healthcare infrastructure, localized diagnostic manufacturing, and rising resistant infection surveillance requirements. China, India, Japan, and South Korea collectively accounted for more than 61% of regional microbiology equipment deployment activity in 2025. Local reagent and analyzer production increased by approximately 23% amid supply-chain localization initiatives and healthcare modernization programs. Hospital groups across India and Southeast Asia are rapidly deploying semi-automated and automated AST systems to manage growing infectious disease burdens while reducing diagnostic turnaround pressure. Companies are expanding regional manufacturing hubs, forming hospital technology alliances, and introducing lower-footprint automated systems optimized for decentralized laboratory environments.

China Market Outlook: China leads the regional market through large-scale diagnostic manufacturing capacity, aggressive hospital modernization programs, and expanding infectious disease monitoring infrastructure. By 2026, more than 55% of urban tertiary hospitals had integrated automated AST workflows within centralized microbiology departments. Domestic companies are scaling AI-assisted diagnostic software, increasing export-oriented reagent production, and strengthening partnerships with provincial healthcare systems to reduce imported diagnostic dependency and improve nationwide antimicrobial resistance surveillance consistency.

Public Healthcare Expansion Supporting Testing Demand

South America is experiencing steady antimicrobial susceptibility testing expansion through public healthcare modernization, increasing resistant infection monitoring, and growing centralized laboratory deployment. Brazil and Argentina accounted for nearly 64% of regional microbiology testing activity in 2025, supported by expanding hospital diagnostic infrastructure and infectious disease surveillance initiatives. Automated AST deployment improved by approximately 17% across large urban healthcare systems as laboratories prioritized faster reporting workflows and reduced manual interpretation dependency. However, imported reagent exposure and fragmented laboratory interoperability continue creating operational inefficiencies in secondary healthcare networks. Companies are responding through regional distribution partnerships, modular analyzer deployment, and localized technical support expansion to improve implementation consistency and procurement stability.

Brazil Market Outlook: Brazil remains the region’s largest operational market due to its broad hospital network, centralized public healthcare system, and growing infectious disease diagnostic demand. More than 48% of major urban laboratories upgraded microbiology automation capabilities during 2025–2026 to support antimicrobial stewardship compliance and sepsis management programs. Diagnostic suppliers are increasing local warehousing capacity, strengthening maintenance partnerships, and introducing hybrid AST platforms tailored for mid-capacity laboratories facing infrastructure and procurement constraints.

Healthcare Modernization Strengthening Diagnostic Infrastructure

The Middle East & Africa market is advancing through healthcare infrastructure investment, laboratory modernization programs, and increasing antimicrobial resistance surveillance initiatives. Gulf healthcare systems represented approximately 58% of regional automated AST deployment activity in 2025 due to strong hospital investment pipelines and centralized procurement frameworks. Saudi Arabia and the United Arab Emirates accelerated digital microbiology integration and cloud-connected laboratory deployments to strengthen infectious disease monitoring capabilities. In Africa, large urban healthcare centers are gradually expanding semi-automated susceptibility testing capacity despite workforce and infrastructure limitations. Companies are prioritizing training partnerships, regional service hubs, and scalable analyzer platforms to improve operational reliability and long-term deployment sustainability across diverse healthcare environments.

Saudi Arabia Market Outlook: Saudi Arabia leads regional deployment activity through large-scale healthcare infrastructure modernization, advanced hospital construction programs, and expanding infectious disease surveillance capabilities. By 2026, automated microbiology integration across government-supported tertiary hospitals increased by nearly 26%, supported by centralized laboratory procurement initiatives and digital health transformation programs. International diagnostic manufacturers are strengthening local partnerships, expanding technical training operations, and introducing high-throughput AST platforms aligned with national healthcare modernization objectives.

Global diagnostic leaders including bioMérieux, Thermo Fisher Scientific, Becton Dickinson, Danaher, and Bio-Rad Laboratories compete directly against regional automation specialists and low-cost reagent suppliers across hospital and laboratory procurement networks. The top five players collectively control approximately 54% of the antimicrobial susceptibility testing market, with competition centered on automation speed, reagent compatibility, software integration, and consumables retention. AI-assisted AST platforms reduced reporting turnaround by nearly 30%, while localized reagent manufacturing lowered supply lead times by approximately 18%, intensifying pressure on import-dependent suppliers. Companies are expanding through hospital partnerships, regional production facilities, cloud-based microbiology software integration, and vertically integrated consumables strategies. Competitive momentum is shifting toward rapid phenotypic testing and interoperability-ready systems capable of supporting multi-site laboratory operations. High validation requirements, regulatory compliance complexity, and installed-system switching costs remain major entry barriers. Winning increasingly depends on integrated workflow ecosystems, localized support infrastructure, and scalable automation performance.

bioMérieux

Thermo Fisher Scientific

Becton, Dickinson and Company

Danaher Corporation

Bio-Rad Laboratories

Bruker Corporation

Accelerate Diagnostics

Liofilchem

HiMedia Laboratories

Merck KGaA

Synbiosis

Hardy Diagnostics

F. Hoffmann-La Roche Ltd

Abbott Laboratories

Automated antimicrobial susceptibility testing platforms remain the dominant technology backbone, with integrated AI-assisted interpretation reducing result validation time by nearly 34% and improving laboratory throughput by approximately 27% compared with conventional manual workflows. More than 58% of tertiary microbiology laboratories adopted automated AST analyzers by 2026 to address workforce shortages and rising multidrug-resistant infections. Cloud-connected laboratory information integration is strengthening reporting consistency, lowering repeat testing volumes by 18%, and improving enterprise-wide infectious disease surveillance efficiency across multi-site hospital networks.

Emerging technologies are shifting toward rapid phenotypic testing, microfluidics, and genomic resistance profiling. Ultra-rapid AST systems now deliver susceptibility results within 2–4 hours instead of the traditional 24–72-hour culture cycle, improving sepsis intervention timelines by nearly 30%. Molecular-integrated AST adoption increased by approximately 21% across critical-care hospitals in Germany, Japan, and the United States. Diagnostic companies are expanding partnerships with sequencing firms, hospital networks, and AI software developers to secure interoperability advantages and accelerate same-day infectious disease decision-making capabilities.

Between 2026 and 2028, disruptive next-generation sequencing-linked AST and decentralized compact analyzers will intensify competition between automation leaders and low-cost conventional suppliers. Companies deploying scalable rapid-testing ecosystems, localized reagent manufacturing, and cybersecurity-ready digital microbiology platforms are expected to secure stronger procurement positioning and long-term institutional contracts.

May 2026 – iFAST Diagnostics expanded its partnership with SYNLAB UK & Ireland to deploy rapid AST workflows delivering results in under 3 hours versus traditional 72-hour processes, strengthening routine clinical adoption and antimicrobial stewardship efficiency across UK laboratory networks. Source: pathologyinpractice.com

April 2026 – Cepheid and Oxford Nanopore Technologies advanced their infectious disease collaboration into phase two, enabling rapid genomic antibiotic susceptibility prediction workflows with expanded researcher beta deployment planned by Q3 2026, accelerating bloodstream infection analysis and high-speed molecular diagnostics integration. Source: caclp.com

January 2026 – ShanX Medtech secured EUR 24 million in financing to accelerate commercialization of its ultra-rapid AST platform, strengthening clinical validation, regulatory expansion, and European deployment capacity amid rising demand for rapid antimicrobial resistance diagnostics. Source: shanxmedtech.com

September 2025 – AST Revolution LLC launched following acquisition of Accelerate Diagnostics assets, advancing the WAVE rapid AST platform capable of delivering results in approximately 4.5 hours, significantly improving sepsis-focused treatment decision speed and strengthening next-generation diagnostic commercialization efforts.

The report delivers comprehensive analysis across Automated Testing, Manual Testing, Disk Diffusion, Broth Dilution, and Molecular Testing technologies, covering deployment trends, workflow modernization, and diagnostic integration strategies between 2026 and 2033. It evaluates operational demand across Bacterial Infections, Respiratory Infections, Bloodstream Infections, Fungal Infections, and Urinary Tract Infections while assessing procurement patterns among Hospitals, Diagnostic Laboratories, Pharmaceutical Companies, Research Institutes, Academic Institutions, and Clinics. More than 58% of enterprise microbiology deployments analyzed within the study involve automated or semi-automated AST infrastructure modernization initiatives.

Regional coverage includes North America, Europe, Asia-Pacific, South America, and Middle East & Africa, with strategic emphasis on laboratory automation, localized reagent manufacturing, AI-enabled diagnostics, and rapid phenotypic testing expansion. The report also evaluates competitive positioning, interoperability readiness, decentralized testing opportunities, and emerging sequencing-linked AST technologies to support investment planning, procurement strategy, partnership evaluation, and long-term infectious disease diagnostic infrastructure decisions.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 1263.78 Million |

|

Market Revenue in 2033 |

USD 2151.9 Million |

|

CAGR (2026 - 2033) |

7.9% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

bioMérieux, Thermo Fisher Scientific, Becton, Dickinson and Company, Danaher Corporation, Bio-Rad Laboratories, Bruker Corporation, Accelerate Diagnostics, Liofilchem, HiMedia Laboratories, Merck KGaA, Synbiosis, Hardy Diagnostics, F. Hoffmann-La Roche Ltd, Abbott Laboratories |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |