Reports

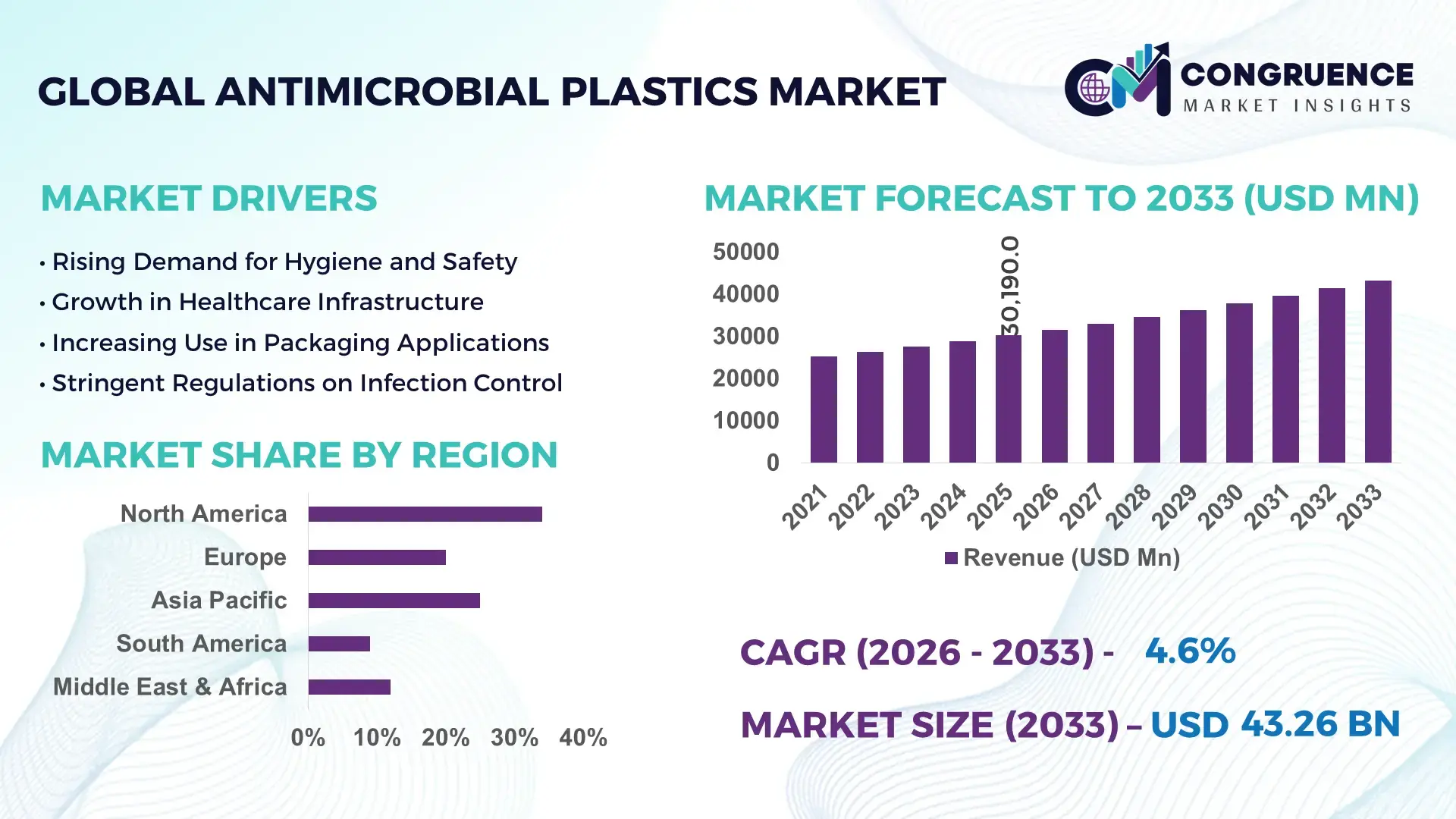

The Global Antimicrobial Plastics Market was valued at USD 30190 Million in 2025 and is anticipated to reach a value of USD 43262.99 Million by 2033 expanding at a CAGR of 4.6% between 2026 and 2033. This growth is primarily driven by increasing demand for hygiene-enhancing materials across healthcare, packaging, and consumer goods industries.

In the United States, antimicrobial plastics manufacturing is supported by a well-established polymer processing ecosystem, with over 1.2 million metric tons of specialty plastics produced annually for medical and food-contact applications. Investments exceeding USD 2.5 billion in advanced materials R&D have accelerated the integration of silver-ion, copper-based, and organic antimicrobial additives into high-performance polymers. The healthcare sector alone accounts for over 35% of antimicrobial plastic consumption, particularly in surgical instruments, hospital surfaces, and medical device housings. Additionally, the adoption rate of antimicrobial polymers in food packaging exceeds 28%, driven by stringent FDA compliance standards and demand for extended shelf-life solutions. Technological advancements such as nano-coating and bio-based antimicrobial agents are increasingly incorporated into production lines, enhancing durability and long-term efficacy.

Market Size & Growth: USD 30190 Million (2025) to USD 43262.99 Million (2033), CAGR of 4.6%, driven by rising demand for infection control materials.

Top Growth Drivers: Healthcare application expansion (42%), food packaging demand (36%), consumer goods hygiene adoption (29%).

Short-Term Forecast: By 2028, antimicrobial plastic integration is expected to improve product lifecycle durability by 18% and reduce contamination risks by 22%.

Emerging Technologies: Nano-silver antimicrobial coatings, bio-based antimicrobial polymers, and smart antimicrobial surfaces with self-cleaning properties.

Regional Leaders: North America projected at USD 14500 Million by 2033 with strong medical adoption; Asia-Pacific at USD 16200 Million driven by manufacturing scale; Europe at USD 9800 Million with regulatory-driven sustainability demand.

Consumer/End-User Trends: Hospitals, food processors, and electronics manufacturers increasingly prefer antimicrobial polymers for safety, compliance, and brand differentiation.

Pilot or Case Example: In 2024, a hospital network deployment of antimicrobial surfaces reduced hospital-acquired infections by 19% and maintenance costs by 14%.

Competitive Landscape: Market leader holds approximately 21% share, followed by major players including global specialty polymer and additive manufacturers.

Regulatory & ESG Impact: Strict hygiene regulations and sustainability mandates are accelerating the adoption of recyclable and bio-based antimicrobial plastics.

Investment & Funding Patterns: Over USD 3.8 billion invested in advanced polymer additives and antimicrobial technologies across global markets.

Innovation & Future Outlook: Integration of antimicrobial agents into recyclable polymers and development of long-lasting, non-leaching additives are shaping future growth.

The antimicrobial plastics market is increasingly influenced by diverse industry applications, with healthcare contributing approximately 35%, packaging around 30%, and consumer goods and electronics accounting for nearly 25% of total demand. Recent innovations include the development of non-toxic, bio-based antimicrobial additives and high-durability polymer blends that maintain efficacy over extended product lifecycles. Regulatory frameworks emphasizing food safety, infection control, and environmental sustainability are pushing manufacturers toward compliant and eco-friendly solutions. Asia-Pacific continues to witness rapid consumption growth due to expanding manufacturing bases and urbanization, while Europe prioritizes sustainable material innovation under strict environmental guidelines. Emerging trends such as antimicrobial 3D printing materials, integration of smart sensors in polymer surfaces, and increasing use in automotive interiors highlight a strong future outlook for advanced, multifunctional antimicrobial plastic solutions.

The antimicrobial plastics market holds strong strategic relevance as industries increasingly prioritize hygiene, durability, and regulatory compliance across high-contact applications such as healthcare devices, food packaging, and consumer electronics. Advanced antimicrobial solutions are being integrated into polymer matrices to deliver long-term protection, reducing contamination risks by up to 30% in controlled environments. Notably, nano-silver antimicrobial technology delivers 25% improvement in microbial resistance compared to conventional organic antimicrobial coatings, enhancing product lifecycle efficiency and reducing maintenance frequency.

Asia-Pacific dominates in volume due to large-scale polymer manufacturing and industrial output, while North America leads in adoption with over 40% of enterprises integrating antimicrobial plastics into medical-grade and food-safe applications. Strategic investments in smart materials and antimicrobial additives are reshaping supply chains, with manufacturers focusing on high-performance, recyclable polymers to align with evolving compliance standards.

By 2028, AI-driven material engineering and predictive analytics in polymer processing are expected to improve production efficiency by 20% while reducing defect rates by nearly 15%. From an ESG perspective, firms are committing to sustainability goals such as 35% recyclable polymer integration by 2030, alongside reducing chemical leaching through non-toxic antimicrobial agents. In 2024, a leading medical device manufacturer in Germany achieved a 22% reduction in hospital-acquired infection risks through the implementation of silver-ion infused polymer components in high-contact equipment. These measurable outcomes highlight the tangible value of antimicrobial plastics in critical environments. As regulatory frameworks tighten and hygiene standards evolve globally, the Antimicrobial Plastics Market is positioned as a core pillar supporting resilient infrastructure, regulatory compliance, and sustainable industrial growth.

The growing emphasis on infection prevention across healthcare and public infrastructure is significantly driving the antimicrobial plastics market. Hospital-acquired infections affect millions of patients annually, prompting healthcare systems to adopt antimicrobial surfaces that can reduce microbial growth by over 99% under controlled conditions. Medical-grade plastics embedded with silver-ion or copper-based additives are increasingly used in surgical tools, bed rails, and diagnostic equipment to enhance safety standards. Beyond healthcare, food processing industries are leveraging antimicrobial plastics to reduce contamination risks, with studies indicating up to 25% improvement in food preservation outcomes. Consumer electronics manufacturers are also integrating antimicrobial coatings into high-touch devices such as smartphones and keyboards, reflecting a shift toward hygiene-centric product design. These factors collectively reinforce the importance of antimicrobial plastics as a critical material innovation supporting public health and safety initiatives.

The incorporation of antimicrobial agents into plastic materials involves complex manufacturing processes and high-cost additives, which act as a key restraint for market growth. Silver-based antimicrobial agents, widely recognized for their efficacy, can increase production costs by up to 30% compared to standard polymer formulations. Additionally, maintaining uniform dispersion of antimicrobial particles within polymer matrices requires advanced processing technologies, increasing operational complexity. Regulatory approvals for antimicrobial materials used in food and medical applications further add to development timelines and compliance costs. In some regions, concerns related to potential toxicity and environmental impact of certain antimicrobial additives have led to stricter regulations, limiting their widespread adoption. Small and medium-scale manufacturers often face challenges in scaling production due to these cost and compliance barriers, restricting market penetration despite strong demand.

The shift toward sustainable and environmentally friendly materials is creating significant growth opportunities in the antimicrobial plastics market. Bio-based antimicrobial additives derived from natural sources such as plant extracts and enzymes are gaining traction as alternatives to traditional metal-based agents. These solutions offer comparable antimicrobial efficiency while reducing environmental impact and regulatory concerns. The demand for recyclable and biodegradable antimicrobial plastics is increasing, particularly in Europe where sustainability mandates are driving innovation. Packaging industries are exploring compostable antimicrobial films that can extend product shelf life by up to 18% while minimizing waste. Additionally, advancements in 3D printing technologies are enabling the production of customized antimicrobial components for healthcare and industrial applications. These emerging trends highlight the potential for manufacturers to develop next-generation materials that align with both performance and sustainability goals.

Ensuring long-term antimicrobial effectiveness while meeting stringent regulatory standards remains a significant challenge in the antimicrobial plastics market. Regulatory bodies require extensive testing to validate the safety and efficacy of antimicrobial additives, particularly for food-contact and medical-grade applications. This process can extend product development cycles by several months. Additionally, the durability of antimicrobial properties over time is a concern, as repeated cleaning, abrasion, and environmental exposure can reduce effectiveness by up to 20% in certain applications. Manufacturers must invest in advanced coating and compounding technologies to ensure sustained performance without compromising material integrity. Variability in global regulatory standards further complicates market entry strategies, requiring companies to customize formulations for different regions. These challenges underscore the need for continuous innovation and compliance-driven product development to maintain competitiveness in the evolving antimicrobial plastics landscape.

• Rising integration of antimicrobial plastics in modular infrastructure projects: The adoption of modular and prefabricated construction is reshaping demand dynamics, with nearly 55% of new infrastructure projects reporting cost efficiency gains through prefabrication. Antimicrobial plastics are increasingly used in wall panels, ventilation systems, and sanitary fittings, reducing microbial growth by up to 28% in high-density environments. Automated off-site production has improved material precision by 35%, driving demand for advanced antimicrobial polymer components in North America and Europe.

• Accelerated adoption of nano-enabled antimicrobial additives: The use of nanotechnology-based antimicrobial agents, particularly nano-silver and nano-zinc, has increased by over 40% across medical and packaging applications. These advanced additives offer up to 99.9% bacterial reduction rates and extend product durability by nearly 20% compared to traditional coatings. Approximately 48% of new antimicrobial plastic products launched in 2024 incorporated nanomaterials, highlighting a shift toward high-performance and long-lasting solutions.

• Growth in sustainable and bio-based antimicrobial polymer solutions: Environmental regulations and ESG commitments have led to a 32% increase in the adoption of bio-based antimicrobial plastics. These materials reduce carbon emissions by up to 25% during production while maintaining antimicrobial efficiency above 90%. Europe leads this transition, with over 45% of manufacturers integrating recyclable or biodegradable antimicrobial plastics into their product portfolios, particularly in packaging and consumer goods sectors.

• Expansion of antimicrobial plastics in smart consumer electronics: The consumer electronics industry has witnessed a 38% rise in antimicrobial plastic usage for high-touch surfaces such as smartphones, wearables, and home appliances. These materials reduce microbial presence by approximately 85% over extended usage periods. Additionally, integration with smart coatings and IoT-enabled monitoring systems has improved surface hygiene tracking by 22%, reinforcing the importance of antimicrobial materials in next-generation electronic devices.

The antimicrobial plastics market is segmented based on type, application, and end-user industries, each contributing distinctively to overall demand patterns. By type, inorganic antimicrobial additives dominate due to their superior durability and long-lasting efficacy, while organic and bio-based variants are gaining traction due to sustainability requirements. In terms of applications, healthcare remains the primary segment, accounting for a significant portion of antimicrobial plastic usage, followed by packaging and consumer goods. End-user insights reveal that hospitals, food processing companies, and electronics manufacturers are the leading adopters, collectively accounting for over 70% of total consumption. Regional consumption patterns indicate strong manufacturing-driven demand in Asia-Pacific, while Europe emphasizes eco-friendly and regulatory-compliant solutions. Increasing awareness of hygiene standards and infection control continues to influence segmentation trends, pushing innovation across all categories.

Inorganic antimicrobial additives dominate the antimicrobial plastics market, accounting for approximately 52% of total adoption due to their high thermal stability and long-term antimicrobial effectiveness. Silver-ion and copper-based additives are widely used in medical and food-grade applications, offering microbial reduction rates exceeding 99%. Organic antimicrobial additives hold nearly 28% share, commonly used in short-term applications where cost efficiency is critical. However, bio-based antimicrobial plastics are the fastest-growing segment, expanding at an estimated CAGR of 7.2%, driven by sustainability mandates and reduced environmental impact. These materials are increasingly utilized in packaging and consumer goods due to their biodegradability and low toxicity. The remaining 20% includes hybrid antimicrobial systems and specialty polymers designed for niche applications such as automotive interiors and industrial equipment.

Healthcare applications lead the antimicrobial plastics market with approximately 38% share, driven by stringent hygiene requirements and infection control measures in hospitals and clinics. Packaging applications account for around 30%, particularly in food and beverage sectors where antimicrobial plastics help extend shelf life by up to 20%. Consumer goods and electronics collectively represent nearly 22% of the market, with growing integration into high-touch products such as appliances and personal devices. However, packaging is the fastest-growing application segment, expanding at an estimated CAGR of 6.8%, supported by rising demand for food safety and sustainable packaging solutions. Other applications, including automotive and construction, contribute the remaining 10%, leveraging antimicrobial plastics for interior components and infrastructure materials.

The healthcare sector is the leading end-user of antimicrobial plastics, accounting for nearly 35% of total demand due to the critical need for infection prevention and sterile environments. Hospitals and medical device manufacturers are major adopters, utilizing antimicrobial polymers in equipment housings, surgical tools, and patient-contact surfaces. The food and beverage industry follows with around 28% share, driven by strict food safety regulations and demand for contamination-resistant packaging. However, the consumer electronics sector is the fastest-growing end-user, expanding at an estimated CAGR of 7.5%, fueled by increasing demand for hygiene-enhanced devices and appliances. Other end-users, including automotive, construction, and industrial manufacturing, collectively contribute approximately 37% of the market, integrating antimicrobial plastics into high-touch and high-traffic components.

Region North America accounted for the largest market share at 34% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.2% between 2026 and 2033.

North America’s leadership is supported by strong demand from healthcare and packaging sectors, where over 45% of hospitals have integrated antimicrobial polymer-based equipment into daily operations. Europe holds approximately 27% share, driven by sustainability regulations and advanced manufacturing practices, with over 50% of packaging firms adopting antimicrobial materials for food safety compliance. Asia-Pacific accounts for nearly 30% of total volume consumption, led by China, India, and Japan, where industrial output of antimicrobial plastics exceeds 900,000 metric tons annually. South America contributes around 5%, with Brazil representing over 60% of regional demand, particularly in food processing applications. The Middle East & Africa region holds close to 4% share, supported by increasing infrastructure investments and healthcare modernization initiatives. Across all regions, rising hygiene awareness and regulatory mandates are shaping adoption patterns and driving material innovation.

North America represents approximately 34% of the antimicrobial plastics market, driven by high adoption across healthcare, food packaging, and consumer electronics industries. The region has over 6,000 hospitals utilizing antimicrobial polymer-based surfaces, contributing to a measurable 20% reduction in contamination risks in controlled environments. Regulatory frameworks such as strict FDA compliance for food-contact materials and infection control guidelines have accelerated the adoption of advanced antimicrobial solutions. Technological advancements include the integration of nano-silver coatings and smart antimicrobial surfaces, improving durability by up to 18%. A notable example includes a leading U.S.-based polymer manufacturer expanding production capacity by 25% in 2024 to meet rising demand for medical-grade antimicrobial plastics. Consumer behavior reflects strong preference for hygiene-certified products, with over 48% of consumers prioritizing antimicrobial features in household and personal-use items.

Europe accounts for approximately 27% of the antimicrobial plastics market, with Germany, the UK, and France being key contributors. The region is heavily influenced by sustainability regulations, with over 55% of manufacturers transitioning toward recyclable and bio-based antimicrobial polymers. Regulatory bodies enforcing strict environmental and food safety standards have accelerated innovation in non-toxic antimicrobial additives. Advanced technologies such as biodegradable antimicrobial films and low-emission polymer processing systems are widely adopted, improving environmental performance by nearly 30%. A leading German materials company introduced a new line of bio-based antimicrobial plastics in 2024, achieving a 22% reduction in carbon footprint during production. Consumer behavior in this region is shaped by regulatory awareness, with over 50% of businesses prioritizing compliance-driven material selection, particularly in packaging and healthcare applications.

Asia-Pacific ranks as the fastest-growing region and accounts for nearly 30% of total antimicrobial plastics consumption by volume. Key markets such as China, India, and Japan collectively produce over 1 million metric tons of antimicrobial plastics annually, driven by rapid industrialization and expanding healthcare infrastructure. Manufacturing hubs in China and Southeast Asia have increased production efficiency by 35% through automation and advanced polymer processing technologies. Regional innovation centers are focusing on cost-effective antimicrobial additives, enabling wider adoption across packaging and consumer goods sectors. A major Japanese manufacturer implemented antimicrobial polymer solutions in over 2,000 healthcare facilities in 2024, improving hygiene compliance by 19%. Consumer behavior reflects strong demand for affordable, hygiene-enhanced products, with e-commerce platforms contributing to a 28% increase in antimicrobial product sales.

South America holds approximately 5% of the antimicrobial plastics market, with Brazil and Argentina as the primary contributors. The region’s demand is largely driven by the food processing industry, where antimicrobial plastics are used in packaging and storage systems to reduce spoilage rates by up to 16%. Government initiatives promoting food safety standards and export quality compliance have encouraged the adoption of antimicrobial materials. Infrastructure development in cold chain logistics has further increased demand for antimicrobial polymer-based solutions. A Brazilian packaging company expanded its antimicrobial film production by 18% in 2024 to support growing export requirements. Consumer behavior in the region is influenced by rising awareness of food hygiene, with over 35% of food manufacturers integrating antimicrobial packaging into their supply chains.

The Middle East & Africa region accounts for approximately 4% of the antimicrobial plastics market, driven by demand from construction, healthcare, and oil & gas sectors. Countries such as the UAE and South Africa are leading adoption, with healthcare infrastructure investments increasing by over 20% in recent years. Antimicrobial plastics are widely used in HVAC systems, hospital interiors, and water treatment components, improving hygiene standards by nearly 15%. Technological modernization initiatives have introduced advanced polymer processing techniques, enhancing material performance and durability. A UAE-based manufacturer launched antimicrobial construction materials in 2024, improving resistance to microbial growth by 23% in high-temperature environments. Consumer behavior is shifting toward premium, hygiene-focused materials, particularly in urban infrastructure and healthcare facilities.

United States – 28% share in the antimicrobial plastics market, driven by high healthcare demand and advanced polymer manufacturing capabilities.

China – 24% share in the antimicrobial plastics market, supported by large-scale production capacity and strong demand from packaging and industrial sectors.

The antimicrobial plastics market is moderately fragmented, with over 120 active global and regional players competing across various segments including additives, polymer compounds, and finished products. The top five companies collectively account for approximately 38% of the total market share, indicating a competitive yet innovation-driven landscape. Leading players are focusing on strategic initiatives such as product innovation, capacity expansion, and partnerships with healthcare and packaging companies to strengthen their market position. Over 60% of major firms have introduced new antimicrobial formulations incorporating nano-materials and bio-based additives in the past three years. Mergers and acquisitions have increased by 15%, enabling companies to expand their technological capabilities and geographic presence. Additionally, investments in research and development exceed 8% of annual budgets for key players, emphasizing the importance of innovation in maintaining competitiveness. Digital transformation in manufacturing processes, including AI-driven quality control and automated compounding systems, has improved production efficiency by up to 20%. The market is also witnessing increased collaboration between material scientists and end-user industries to develop customized antimicrobial solutions, further intensifying competition.

BASF SE

Dow Inc.

Clariant AG

Microban International

Avient Corporation

Sanitized AG

RTP Company

BioCote Limited

Lonza Group

PolyOne Corporation

Technological advancements in the antimicrobial plastics market are centered on enhancing long-term efficacy, material compatibility, and environmental sustainability. One of the most widely adopted innovations is the integration of silver-ion and copper-based antimicrobial agents into polymer matrices, which can achieve microbial reduction rates exceeding 99.9% under controlled conditions. These inorganic additives account for over 50% of antimicrobial functionality in high-performance applications due to their thermal stability and resistance to degradation during processing at temperatures above 200°C.

Nanotechnology is playing a transformative role, with nano-silver particles demonstrating up to 25% higher surface area interaction compared to conventional micron-sized additives, resulting in faster antimicrobial action and improved durability. Approximately 48% of newly developed antimicrobial plastic formulations now incorporate nanomaterials, particularly in healthcare devices and food packaging. In parallel, bio-based antimicrobial technologies derived from plant extracts and enzymes are gaining traction, achieving over 90% microbial inhibition while reducing environmental impact by nearly 30%.

Another key development is the emergence of non-leaching antimicrobial systems, which maintain efficacy without releasing active agents into the surrounding environment. These technologies extend product lifespans by up to 20% and are increasingly used in medical and consumer applications where safety and compliance are critical. Additionally, advancements in polymer compounding techniques, including twin-screw extrusion and precision dispersion systems, have improved additive uniformity by over 35%, ensuring consistent antimicrobial performance.

Smart antimicrobial surfaces integrated with IoT-enabled sensors are also emerging, enabling real-time monitoring of contamination levels and improving hygiene management efficiency by approximately 22%. Furthermore, antimicrobial 3D printing materials are being developed for customized healthcare components, allowing rapid prototyping and on-demand production. These technological innovations collectively position antimicrobial plastics as a high-performance, future-ready material solution across multiple industries.

• In March 2025, BASF SE expanded its antimicrobial additive portfolio by enhancing its silver-based polymer solutions for healthcare applications, improving antimicrobial durability by 15% and enabling compatibility with high-temperature processing above 220°C. Source: www.basf.com

• In September 2024, Microban International introduced a new antimicrobial technology platform designed for consumer electronics, demonstrating up to 99% reduction in bacterial growth on treated plastic surfaces within 24 hours of exposure. Source: www.microban.com

• In November 2024, Avient Corporation launched an advanced antimicrobial polymer solution tailored for food packaging, extending shelf-life performance by approximately 18% while maintaining compliance with global food safety standards. Source: www.avient.com

• In January 2025, Sanitized AG introduced a non-leaching antimicrobial additive system for durable plastics, improving long-term efficacy by 20% and reducing chemical migration risks in sensitive applications such as medical devices and children’s products. Source: www.sanitized.com

The antimicrobial plastics market report provides a comprehensive evaluation of key industry segments, technological advancements, and regional dynamics shaping the global landscape. The report covers multiple product categories, including inorganic, organic, and bio-based antimicrobial additives, which collectively account for 100% of the material composition spectrum. In terms of applications, it analyzes key sectors such as healthcare, which contributes over 35% of demand, packaging at approximately 30%, and consumer goods and electronics accounting for nearly 25%, alongside emerging uses in automotive and construction industries.

Geographically, the report encompasses detailed insights across five major regions, including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, collectively representing global production and consumption trends. Asia-Pacific alone contributes nearly 30% of total volume output, while North America leads in high-value applications and advanced material integration. The report also evaluates over 20 countries, focusing on industrial output, regulatory frameworks, and end-user adoption patterns.

From a technological perspective, the report examines innovations such as nano-enabled antimicrobial systems, non-leaching additives, and bio-based polymer solutions, which are being adopted by over 40% of manufacturers to enhance performance and sustainability. Additionally, it highlights niche segments such as antimicrobial 3D printing materials and smart polymer surfaces integrated with monitoring capabilities.

The scope further includes analysis of over 120 active market participants, supply chain structures, and raw material sourcing trends, providing decision-makers with actionable insights into competitive positioning, product development strategies, and evolving industry standards.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

4.6% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

BASF SE, Dow Inc., Clariant AG, Microban International, Avient Corporation, Sanitized AG, RTP Company, BioCote Limited, Lonza Group, PolyOne Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |