Reports

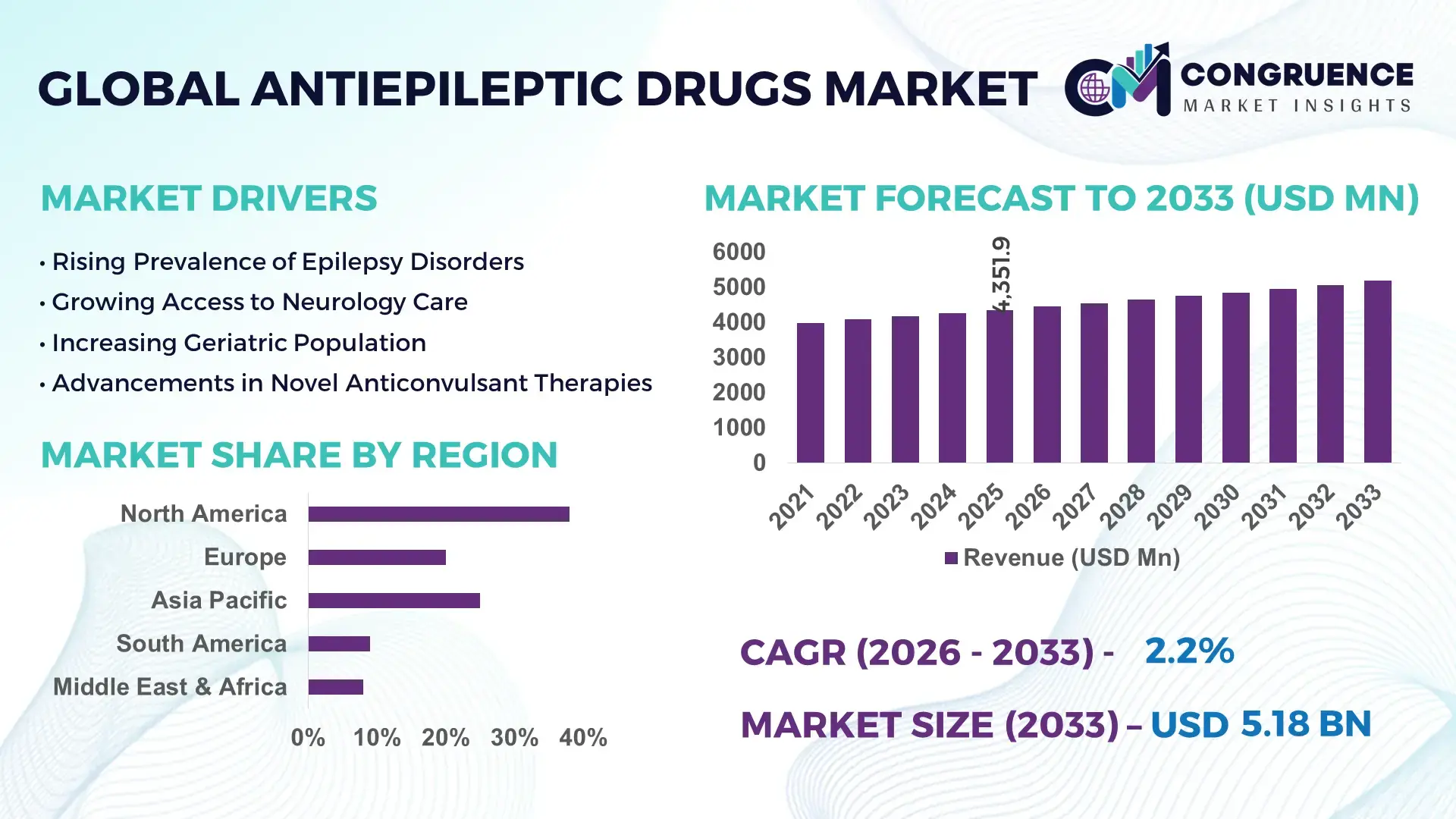

The Global Antiepileptic Drugs Market was valued at USD 4351.93 Million in 2025 and is anticipated to reach a value of USD 5179.52 Million by 2033 expanding at a CAGR of 2.2% between 2026 and 2033. The steady expansion is primarily driven by the rising global prevalence of epilepsy and neurological disorders, alongside improved diagnosis rates and long-term pharmacotherapy adherence.

The United States remains a dominant country in the Antiepileptic Drugs market, supported by advanced pharmaceutical manufacturing infrastructure and high treatment penetration. Over 3.4 million individuals in the U.S. live with epilepsy, including approximately 470,000 children, generating sustained prescription demand for first-line and adjunctive antiepileptic therapies. The country hosts more than 30 FDA-approved antiepileptic molecules across various generations, including sodium channel blockers, GABA analogs, and SV2A modulators. U.S.-based pharmaceutical manufacturers allocate over 15% of neurology drug revenues to R&D annually, accelerating innovation in extended-release formulations and precision neurology. Hospital pharmacies account for nearly 55% of dispensed antiepileptic drugs, while retail and online channels collectively contribute over 40% of volume distribution. Additionally, the integration of digital seizure-monitoring devices into treatment regimens has improved medication adherence by nearly 20% in monitored patient cohorts.

Market Size & Growth: Valued at USD 4351.93 Million in 2025, projected to reach USD 5179.52 Million by 2033 at a CAGR of 2.2%, driven by increasing epilepsy incidence and long-term chronic therapy demand.

Top Growth Drivers: 18% rise in diagnosed epilepsy cases globally, 25% improvement in treatment adherence via digital monitoring, 30% increase in pediatric neurology prescriptions.

Short-Term Forecast: By 2028, optimized extended-release formulations are expected to reduce dosing frequency by 40%, improving patient compliance metrics.

Emerging Technologies: AI-driven seizure prediction algorithms, precision neurology based on genetic biomarkers, and long-acting injectable antiepileptic formulations.

Regional Leaders: North America projected to exceed USD 1.8 Billion by 2033 with high biologic adoption; Europe expected to cross USD 1.4 Billion with strong regulatory harmonization; Asia-Pacific anticipated to surpass USD 1.2 Billion driven by expanding neurology infrastructure.

Consumer/End-User Trends: Hospitals and specialty neurology clinics represent over 60% of prescriptions, with increasing uptake of combination therapy protocols.

Pilot or Case Example: In 2024, a U.S. digital epilepsy management pilot achieved a 22% reduction in seizure-related emergency visits through AI-assisted dose optimization.

Competitive Landscape: UCB holds approximately 15% share, followed by Pfizer, GlaxoSmithKline, Sun Pharmaceutical Industries, and Eisai.

Regulatory & ESG Impact: Stricter pharmacovigilance frameworks and commitments to reduce manufacturing emissions by 25% by 2030 are influencing production models.

Investment & Funding Patterns: Over USD 800 Million invested globally in neurology drug R&D in recent years, with rising venture funding for neuro-digital therapeutics.

Innovation & Future Outlook: Growth in gene-targeted therapies, sustained-release platforms, and AI-integrated neurology care pathways will shape long-term industry transformation.

The Antiepileptic Drugs market serves key healthcare segments including hospital pharmacies, retail drug chains, specialty neurology clinics, and telehealth-enabled prescription platforms. Second- and third-generation antiepileptic drugs contribute over 65% of total prescriptions due to improved tolerability profiles. Recent product innovations include once-daily extended-release tablets and novel SV2A receptor modulators that enhance seizure control in refractory epilepsy patients. Regulatory emphasis on bioequivalence, pharmacovigilance compliance, and controlled substance monitoring continues to influence commercialization strategies. Asia-Pacific markets are experiencing faster consumption growth due to increasing public healthcare spending and broader insurance coverage. Future trends indicate rising adoption of personalized medicine approaches, combination therapy regimens, and integration of AI-based seizure analytics into standard neurology care pathways.

The Antiepileptic Drugs Market holds strategic relevance within the broader neurology therapeutics landscape, as epilepsy affects over 50 million people globally, requiring lifelong disease management. Pharmaceutical companies are prioritizing portfolio optimization through next-generation molecules and lifecycle management strategies. Precision medicine platforms leveraging pharmacogenomic testing are redefining therapy selection, with biomarker-guided treatments improving seizure control rates by up to 28% compared to conventional trial-and-error prescribing models. AI-assisted seizure prediction systems deliver 35% improvement in early intervention accuracy compared to traditional patient-reported monitoring.

North America dominates in prescription volume, while Asia-Pacific leads in adoption growth with over 40% of new neurology patients entering structured treatment programs. By 2028, AI-enabled remote monitoring solutions are expected to reduce epilepsy-related hospital admissions by 18%, improving healthcare cost efficiency. Firms are committing to ESG-aligned manufacturing practices, targeting 25% carbon emission reduction and 30% recyclable packaging integration by 2030.

In 2024, Japan achieved a 20% improvement in medication adherence through nationwide digital neurology tracking initiatives integrated with hospital networks. Strategic collaborations between pharmaceutical firms and medtech providers are accelerating long-acting injectable development and digital companion diagnostics. As healthcare systems emphasize chronic disease management efficiency and value-based reimbursement models, the Antiepileptic Drugs Market is positioned as a pillar of resilience, compliance-driven innovation, and sustainable pharmaceutical growth.

The increasing global prevalence of epilepsy directly strengthens demand for antiepileptic drugs across developed and emerging healthcare systems. Approximately 5 million new epilepsy cases are diagnosed annually worldwide, creating sustained long-term treatment demand. In low- and middle-income countries, treatment gaps historically exceeding 50% are narrowing due to improved healthcare access and public awareness programs. Pediatric epilepsy accounts for nearly 25% of total diagnosed cases, expanding prescription volumes in specialized formulations. Aging populations further contribute to rising seizure incidence linked to stroke and neurodegenerative conditions. Enhanced diagnostic imaging and EEG utilization have improved early detection rates by over 15%, accelerating timely drug initiation. As healthcare coverage expands in Asia-Pacific and Latin America, prescription volumes continue to rise steadily.

Despite stable demand, adverse drug reactions remain a notable restraint within the Antiepileptic Drugs market. Nearly 30% of patients experience dose-related side effects such as dizziness, cognitive impairment, or dermatological reactions, leading to therapy switching or discontinuation. Stringent regulatory requirements for safety surveillance increase compliance costs for manufacturers. Additionally, generic penetration exceeds 60% in multiple mature markets, intensifying pricing competition and compressing margins for branded formulations. Patent expirations of key molecules have shifted procurement strategies toward cost-efficient alternatives. Reimbursement constraints and tender-based purchasing in public healthcare systems further limit premium pricing opportunities. These combined pressures challenge innovation incentives and reduce differentiation potential in saturated therapeutic classes.

Personalized medicine and long-acting drug delivery systems represent transformative opportunities in the Antiepileptic Drugs market. Pharmacogenomic profiling can improve therapeutic response accuracy by up to 25%, reducing trial-and-error prescribing cycles. Long-acting injectable formulations and once-daily extended-release tablets enhance adherence, addressing non-compliance rates that historically reach 40% in chronic epilepsy management. Digital companion applications integrated with wearable devices allow real-time seizure tracking and dose adjustments, improving patient outcomes. Emerging markets with rising healthcare investments present untapped prescription potential, particularly where diagnosis rates are improving. Additionally, research into gene-modifying therapies and targeted receptor modulators is expanding treatment options for drug-resistant epilepsy, which affects nearly 30% of patients globally.

The Antiepileptic Drugs market faces significant challenges linked to stringent regulatory approvals and high clinical trial expenditures. Neurology trials often require multi-year evaluation periods with large patient cohorts to demonstrate seizure frequency reduction and long-term safety. Phase III trials in epilepsy can involve over 1,000 participants across multiple regions, increasing operational complexity. Post-marketing surveillance requirements demand continuous pharmacovigilance reporting, raising compliance costs. Variability in regional approval standards complicates global product launches. Furthermore, competition from established generics reduces financial returns on innovative molecules. These structural challenges necessitate strategic partnerships, adaptive trial designs, and digital monitoring integration to sustain long-term competitiveness in the evolving neurology therapeutics landscape.

• 32% Increase in Adoption of Third-Generation Antiepileptic Drugs: Prescription patterns are shifting toward third-generation antiepileptic drugs due to improved tolerability and lower drug–drug interaction profiles. These advanced formulations now account for nearly 48% of new prescriptions in developed markets, compared to 36% five years ago. Clinical studies indicate a 20% reduction in severe adverse reactions compared to first-generation molecules, strengthening physician confidence. Neurology centers in North America report that over 60% of newly diagnosed focal seizure patients are initiated on newer-generation therapies, reflecting a measurable shift in treatment standards.

• 25% Improvement in Medication Adherence Through Digital Monitoring: Integration of wearable seizure trackers and AI-enabled mobile health platforms has enhanced therapy compliance by approximately 25% among monitored patient groups. Over 40% of tertiary epilepsy centers in Europe now incorporate digital seizure diaries into routine care. These tools reduce emergency hospital visits by 18% and enable dose optimization in nearly 30% of digitally monitored cases. Pharmaceutical companies are increasingly bundling digital companion applications with drug therapy to strengthen long-term treatment outcomes.

• 28% Growth in Pediatric-Specific Formulations: Pediatric epilepsy represents nearly 25% of global epilepsy cases, prompting increased development of age-appropriate formulations such as oral suspensions and dispersible tablets. Adoption of pediatric-friendly dosage forms has grown by 28% in the past three years. Hospitals report a 15% improvement in dosing accuracy and a 12% reduction in administration-related errors when using child-specific antiepileptic formulations, reinforcing demand in specialized neurology clinics.

• 35% Expansion in Emerging Market Treatment Access: Public healthcare initiatives in Asia-Pacific and Latin America have reduced epilepsy treatment gaps by nearly 35% over the past decade. Government-supported procurement programs now supply essential antiepileptic drugs to over 70% of public hospitals in select emerging economies. Generic penetration exceeds 60% in these regions, improving affordability while maintaining stable supply chains. This expansion is significantly increasing prescription volumes and strengthening long-term market sustainability.

The Antiepileptic Drugs market is segmented by type, application, and end-user, each reflecting distinct demand drivers and prescribing behaviors. By type, second- and third-generation antiepileptic drugs dominate due to improved safety and targeted mechanisms of action, collectively accounting for over 65% of prescriptions. By application, focal seizures represent the largest treatment category, covering nearly 55% of diagnosed epilepsy cases, followed by generalized seizures and adjunctive therapy in refractory epilepsy. End-user segmentation highlights hospital pharmacies as primary distribution channels, contributing more than 50% of dispensed volumes, while retail and online pharmacies continue expanding their presence, particularly in urban regions. Growth dynamics across segments are influenced by regulatory compliance standards, pediatric formulation demand, generic penetration rates, and increasing adoption of combination therapy protocols in tertiary neurology care centers.

Second-generation antiepileptic drugs currently account for approximately 44% of total prescriptions, making them the leading product type due to their balanced efficacy and improved tolerability compared to first-generation therapies. Third-generation antiepileptic drugs represent about 32% of adoption, supported by targeted mechanisms such as SV2A modulation and enhanced pharmacokinetics. However, third-generation therapies are the fastest-growing segment, expanding at an estimated 4.8% annually, driven by rising demand for reduced cognitive side effects and compatibility with polytherapy regimens. First-generation antiepileptic drugs still contribute nearly 24% of global prescriptions, primarily in cost-sensitive markets where generic alternatives dominate procurement systems. These drugs remain clinically relevant for generalized tonic-clonic seizures but face declining adoption in high-income countries due to safety concerns.

Focal seizures represent the leading application segment, accounting for nearly 55% of total antiepileptic drug utilization, reflecting their high global prevalence. Generalized seizures account for approximately 30% of prescriptions, supported by standardized treatment protocols across hospital networks. However, adjunctive therapy for drug-resistant epilepsy is the fastest-growing application, advancing at approximately 5.2% annually as nearly 30% of epilepsy patients exhibit partial or non-response to monotherapy. Status epilepticus management and off-label psychiatric applications collectively contribute around 15% of demand, serving niche but clinically significant patient populations. Increasing awareness campaigns and improved diagnostic EEG access have raised early-stage focal seizure identification by nearly 20%, strengthening first-line treatment volumes.

Hospital pharmacies dominate the Antiepileptic Drugs market, accounting for approximately 52% of total dispensed volumes due to centralized procurement systems and specialist neurology oversight. Retail pharmacies contribute nearly 33% of prescriptions, benefiting from chronic refill demand and improved insurance coverage. However, online and specialty digital pharmacies are the fastest-growing end-user segment, expanding at an estimated 6.1% annually, supported by tele-neurology adoption and home-delivery convenience. Specialty epilepsy centers and academic medical institutions collectively represent about 15% of distribution, focusing primarily on refractory and pediatric cases. Adoption of integrated digital adherence platforms in hospital settings has improved medication compliance by nearly 20%, strengthening institutional purchasing volumes.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 4.6% between 2026 and 2033.

North America’s leadership is supported by high diagnosis rates, where nearly 70% of epilepsy patients receive continuous pharmacological therapy. Europe follows with approximately 27% share, driven by structured reimbursement frameworks and standardized neurology guidelines across more than 30 countries. Asia-Pacific currently contributes close to 24% of global volume, with over 20 million diagnosed epilepsy patients across China, India, and Japan combined. South America represents nearly 6% of the Antiepileptic Drugs market, while the Middle East & Africa collectively account for about 5%, reflecting gradual improvements in public healthcare access. Generic penetration exceeds 60% in emerging markets, compared to nearly 45% in mature markets, shaping pricing dynamics and procurement strategies. Increasing hospital-based prescription rates, which account for more than 55% of global dispensed volumes, continue to influence regional demand patterns and long-term therapy adoption.

How Are Advanced Neurology Protocols and Digital Therapeutics Reshaping Treatment Adoption?

North America holds approximately 38% share of the global Antiepileptic Drugs market, with the United States accounting for nearly 85% of the regional volume. Over 3.4 million individuals are actively treated for epilepsy, and more than 60% of prescriptions involve second- and third-generation therapies. Hospital pharmacies contribute nearly 55% of dispensed volumes, while retail and online platforms account for 40% combined. Regulatory oversight through stringent pharmacovigilance frameworks has improved post-marketing safety reporting compliance by 18% over the past five years. Digital transformation is accelerating, with over 45% of tertiary epilepsy centers integrating AI-based seizure monitoring systems. A leading regional player, UCB, continues expanding its SV2A-focused portfolio and digital companion tools, improving adherence rates by nearly 20% in monitored cohorts. Consumer behavior reflects high insurance coverage penetration exceeding 70%, supporting sustained prescription refills and premium therapy adoption.

How Do Harmonized Regulatory Standards and Public Healthcare Systems Influence Market Expansion?

Europe represents nearly 27% of the global Antiepileptic Drugs market, with Germany, the UK, and France collectively accounting for over 50% of regional demand. Public healthcare systems cover more than 75% of epilepsy-related prescriptions, ensuring stable therapy continuity. The European Medicines Agency has strengthened pharmacovigilance reporting standards, leading to a 15% improvement in adverse event documentation accuracy. Adoption of extended-release formulations has increased by 22% in Western Europe due to adherence-focused treatment guidelines. Local pharmaceutical innovator UCB, headquartered in Belgium, continues to invest over 15% of its neurology revenues into R&D, supporting next-generation molecule development. Consumer patterns indicate strong demand for evidence-backed, explainable treatment options, with over 65% of neurologists preferring therapies supported by long-term safety studies exceeding five years.

What Role Do Expanding Healthcare Infrastructure and Generic Manufacturing Play in Accelerated Adoption?

Asia-Pacific contributes around 24% of global Antiepileptic Drugs volume and ranks as the fastest-growing region. China, India, and Japan account for nearly 70% of regional prescriptions. The region hosts over 20 million epilepsy patients, with treatment access improving by 30% in urban centers over the past decade. Generic manufacturing dominates, representing over 65% of dispensed formulations. India alone operates more than 3,000 pharmaceutical manufacturing facilities, strengthening supply capacity. Japan leads in digital neurology integration, with over 40% of tertiary hospitals implementing electronic prescription monitoring systems. Sun Pharmaceutical Industries has expanded its neurology portfolio in India, increasing domestic distribution coverage by 18% in the past two years. Consumer trends indicate rising adoption of telemedicine platforms, with mobile health app usage for chronic disease management increasing by 35% across metropolitan regions.

How Are Public Health Investments and Local Production Strengthening Treatment Accessibility?

South America accounts for approximately 6% of the global Antiepileptic Drugs market, with Brazil and Argentina representing nearly 65% of regional demand. Brazil’s public healthcare system supplies essential antiepileptic medications to over 70% of registered epilepsy patients. Regional generic penetration exceeds 75%, improving affordability. Government-backed procurement programs have increased essential drug availability in public hospitals by 20% over the past five years. Local pharmaceutical manufacturers have expanded production capacity by nearly 15% to meet growing demand. Consumer behavior reflects strong reliance on public hospital distribution channels, accounting for more than 60% of prescriptions. Increased awareness campaigns have improved diagnosis rates by approximately 12%, strengthening long-term therapy adherence in urban populations.

How Are Healthcare Modernization Efforts Enhancing Chronic Neurology Treatment Delivery?

The Middle East & Africa region contributes about 5% to the global Antiepileptic Drugs market, with the UAE and South Africa emerging as key growth hubs. Over 50% of epilepsy treatments in the region are distributed through government-supported hospital networks. Healthcare modernization initiatives have increased neurology specialist availability by 18% in Gulf Cooperation Council countries. Digital prescription systems are now operational in nearly 35% of tertiary hospitals in the UAE. Trade partnerships and reduced import tariffs have improved drug availability by 22% across selected African nations. Consumer patterns show growing preference for branded generics, which account for nearly 55% of dispensed therapies. Expanding insurance penetration, particularly in urban Middle Eastern markets, is contributing to stable prescription renewal rates.

United States – 33% share in the Antiepileptic Drugs market: High diagnosis rates, strong R&D investment exceeding 15% of neurology revenues, and advanced hospital infrastructure drive sustained prescription volumes.

Germany – 9% share in the Antiepileptic Drugs market: Robust public healthcare coverage, standardized epilepsy treatment protocols, and strong regulatory compliance frameworks support consistent therapy adoption.

The Antiepileptic Drugs market demonstrates a moderately consolidated structure, with the top five companies collectively accounting for approximately 55% of global share. More than 40 active pharmaceutical companies participate in this therapeutic category, including multinational innovators and regional generic manufacturers. Market leaders focus on lifecycle management strategies, extended-release formulations, and regulatory expansion of approved indications. Over 25 new clinical trials targeting refractory epilepsy are currently underway globally, reflecting sustained innovation intensity. Strategic partnerships between pharmaceutical firms and digital health providers have increased by 30% since 2022, aiming to enhance patient adherence and real-world outcome monitoring. Patent expirations for first- and second-generation molecules have intensified generic competition, which now represents over 60% of dispensed volumes in emerging economies. Mergers and acquisitions remain selective, with companies prioritizing neurology-focused pipeline acquisitions. Competitive differentiation increasingly centers on safety profile enhancements, pediatric approvals, and digital integration, shaping a technology-driven and compliance-oriented competitive landscape.

UCB

Pfizer Inc.

GlaxoSmithKline plc

Sun Pharmaceutical Industries Ltd.

Eisai Co., Ltd.

Johnson & Johnson

Novartis AG

Sanofi

Teva Pharmaceutical Industries Ltd.

Abbott Laboratories

Technological advancement in the Antiepileptic Drugs market is increasingly centered on precision neurology, digital therapeutics integration, and novel drug delivery platforms. Pharmacogenomic testing is now influencing treatment selection in nearly 20% of complex epilepsy cases in advanced healthcare systems, enabling clinicians to predict drug metabolism profiles and reduce adverse reactions by up to 25%. This biomarker-driven approach is particularly valuable for drug-resistant epilepsy, which affects approximately 30% of patients globally. Artificial intelligence–based seizure prediction systems are gaining measurable traction, with wearable EEG-integrated devices demonstrating up to 35% improvement in early seizure detection compared to traditional patient-reported tracking. Over 40% of tertiary neurology centers in developed markets have adopted electronic seizure diaries and AI-assisted analytics to support dose optimization. These systems contribute to an 18–22% reduction in emergency hospital visits among digitally monitored patients.

On the pharmaceutical manufacturing side, continuous manufacturing technologies are improving production efficiency by nearly 15% while reducing batch variability. Extended-release and controlled-release formulations now represent over 45% of new product development pipelines, supporting once-daily dosing regimens that enhance adherence rates by approximately 30%. Lipid-based and nanoformulation drug delivery systems are also under evaluation to improve bioavailability in refractory epilepsy cases. In addition, digital companion applications linked to prescription therapies are becoming standard in neurology portfolios, with adoption rates exceeding 25% among leading pharmaceutical firms. These technologies strengthen post-marketing surveillance, improve real-world evidence collection, and enable data-driven lifecycle management strategies for high-value antiepileptic therapies.

• In March 2024, UCB received U.S. FDA approval for FINTEPLA (fenfluramine) oral solution for the treatment of seizures associated with Lennox-Gastaut syndrome in patients aged 2 years and older. This expanded indication strengthens UCB’s pediatric epilepsy portfolio and broadens access for a severe, treatment-resistant patient population. Source: www.ucb.com

• In April 2024, Eisai Co., Ltd. announced that the U.S. FDA approved FYCOMPA (perampanel) as monotherapy for focal seizures in pediatric patients aged 4 years and older. The label expansion supports simplified treatment regimens and enhances therapeutic flexibility in early-stage epilepsy management. Source: www.eisai.com

• In January 2025, UCB reported positive Phase 3 data for bepranemab, an investigational anti-tau monoclonal antibody, reinforcing its neurology R&D pipeline strategy. While primarily targeting neurodegenerative disorders, the advancement underscores UCB’s sustained investment exceeding 15% of neurology-focused revenues into central nervous system innovation. Source: www.ucb.com

• In February 2025, Pfizer Inc. announced continued expansion of its digital health collaborations to integrate remote patient monitoring solutions across selected neurology portfolios. The initiative aims to enhance real-world evidence collection and improve long-term treatment adherence metrics in chronic neurological conditions, including epilepsy. Source: www.pfizer.com

The Antiepileptic Drugs Market Report provides a comprehensive evaluation of therapeutic segments, distribution channels, technological advancements, regulatory frameworks, and regional demand dynamics across more than 30 countries. The report covers first-, second-, and third-generation antiepileptic drugs, which collectively address over 70% of diagnosed epilepsy cases requiring long-term pharmacotherapy. It assesses application areas including focal seizures, generalized seizures, Lennox-Gastaut syndrome, and drug-resistant epilepsy, the latter affecting nearly 30% of patients globally. Geographic analysis spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting regional treatment access variations and generic penetration levels exceeding 60% in emerging markets. End-user evaluation includes hospital pharmacies, retail chains, online pharmacies, and specialty neurology centers, with hospital channels accounting for more than 50% of global dispensed volumes.

The report also examines digital health integration, including AI-driven seizure prediction systems adopted by over 40% of tertiary care centers in developed economies. Manufacturing trends such as continuous production technologies improving efficiency by approximately 15% and extended-release formulations representing nearly 45% of new product pipelines are analyzed in detail. In addition, the scope addresses regulatory compliance requirements, pharmacovigilance reporting systems, pediatric formulation innovation, ESG-driven manufacturing initiatives targeting 25% emission reductions, and investment patterns in neurology R&D. The report is structured to support strategic planning, competitive benchmarking, portfolio optimization, and long-term decision-making within the evolving Antiepileptic Drugs market ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

2.2% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

|

|

Customization & Pricing |

Available on Request (10% Customization is Free) |