Reports

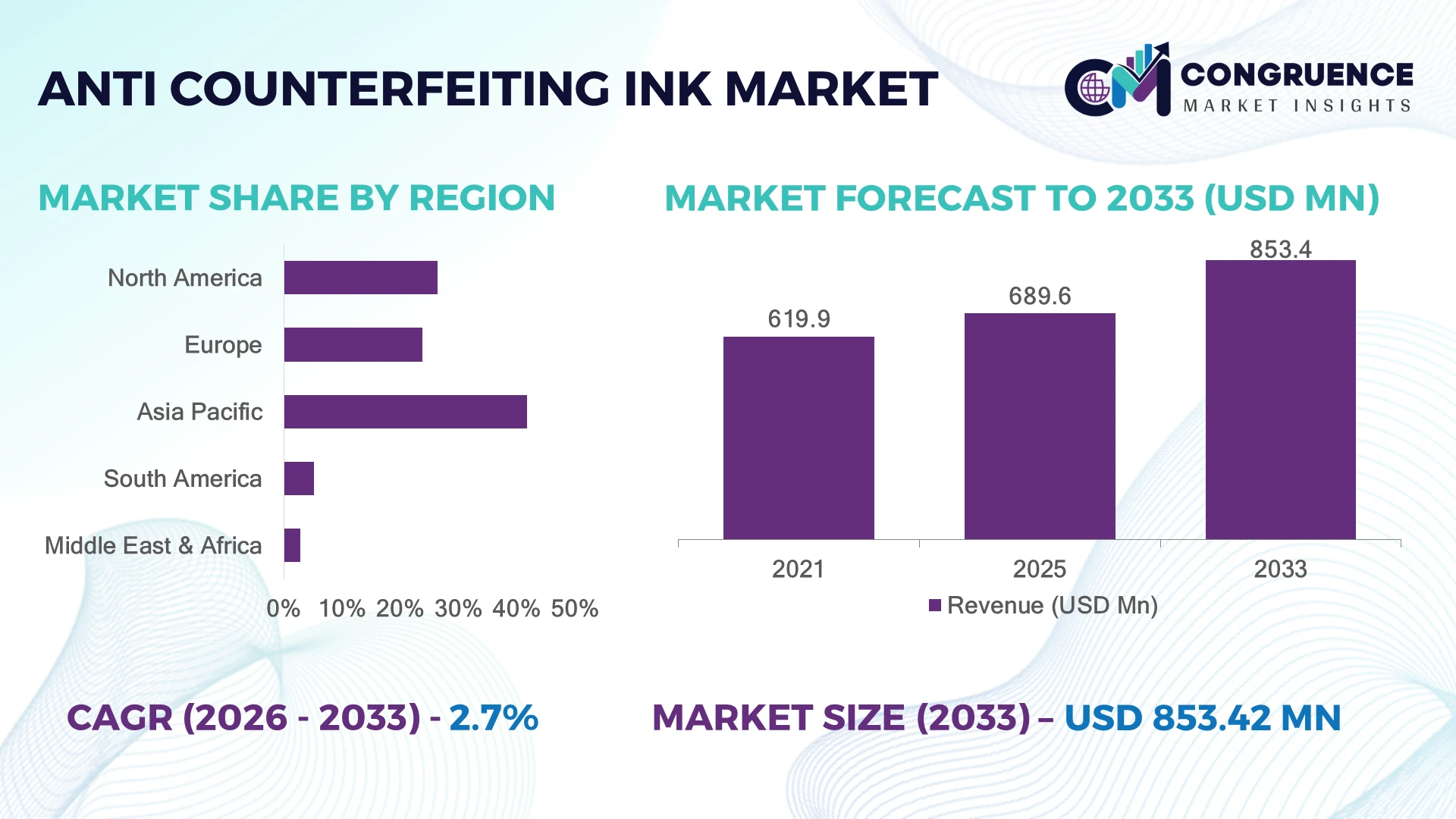

The Global Anti-Counterfeiting Ink Market was valued at USD 689.6 Million in 2025 and is anticipated to reach a value of USD 853.4 Million by 2033 expanding at a CAGR of 2.7% between 2026 and 2033. Growth is driven by stricter product authentication regulations, rising counterfeit pharmaceutical and currency incidents, and wider deployment of security printing technologies across government-issued documents and premium consumer packaging.

China commands nearly 31% of global security printing capacity, supported by expanding banknote production, pharmaceutical packaging, and government document authentication programs, while the United States accounts for approximately 24% through advanced security ink innovation and high-value brand protection initiatives. Growing compliance following tighter anti-counterfeiting frameworks and cross-border trade monitoring continues to accelerate advanced ink adoption across strategic industries.

This competitive landscape reinforces investment priorities toward secure, traceable, and technology-enabled authentication solutions across global supply chains.

Market Size & Growth: USD 689.6 Million in 2025, reaching USD 853.4 Million by 2033 at 2.7% CAGR, supported by advanced security printing and authentication technologies.

Top Growth Drivers: Pharmaceutical authentication (41%), secure packaging (34%), and government document protection (25%) lead demand expansion.

Short-Term Forecast: By 2028, authentication verification efficiency improves by nearly 20% through digital traceability integration.

Emerging Technologies: AI-assisted inspection, fluorescent and UV-reactive inks, and nano-pigment formulations strengthen high-security printing performance.

Regional Leaders: Asia Pacific (~USD 310 Million), North America (~USD 215 Million), and Europe (~USD 185 Million) benefit from manufacturing expansion, brand protection, and regulatory adoption.

Consumer/End-User Trends: More than 58% of premium brands integrate advanced anti-counterfeiting labels with security inks across high-value products.

Pilot/Case Example: In 2024, upgraded pharmaceutical serialization projects reduced counterfeit detection time by approximately 30% through integrated security printing.

Competitive Landscape: SICPA leads with roughly 22% market share alongside Sun Chemical, Kao Collins, Gleitsmann Security Inks, and CTI.

Regulatory & ESG Impact: Digital product authentication programs improved compliance rates by nearly 18% while reducing document fraud across regulated sectors.

Investment & Funding: Over USD 420 Million has supported security printing expansion, strategic partnerships, and advanced ink manufacturing upgrades.

Innovation & Future Outlook: Smart authentication inks, hybrid physical-digital security features, and blockchain-enabled verification are reshaping next-generation brand protection.

Increasing demand from pharmaceuticals, currency printing, luxury goods, electronics, and government documentation continues to reshape the Anti-Counterfeiting Ink Market. Recent innovations in UV-reactive, infrared, and nano-engineered security inks improve authentication accuracy by nearly 25%, while stricter product traceability regulations and evolving cross-border supply-chain security requirements encourage wider deployment of multi-layer authentication technologies, setting the stage for broader strategic market development.

The Anti-Counterfeiting Ink Market has become strategically important as governments, manufacturers, and brand owners strengthen product authentication to combat counterfeit trade and protect consumer confidence. Expanding pharmaceutical serialization requirements, secure identity documentation, and premium brand protection are reshaping procurement priorities. At the same time, supply-chain restructuring and stricter customs enforcement are encouraging wider adoption of sophisticated security printing technologies across international trade networks.

Modern security inks incorporating UV, infrared, and machine-readable markers deliver authentication processes that are approximately 35% faster than conventional visual verification methods while reducing manual inspection requirements. Asia-Pacific leads large-scale deployment through expanding manufacturing and government security printing programs, whereas North America emphasizes advanced innovation, digital authentication integration, and premium intellectual property protection. Over the next two to three years, enterprise adoption of hybrid physical-digital authentication platforms is expected to increase by more than 20% across regulated industries.

A practical example is pharmaceutical packaging, where multi-layer security inks combined with digital serialization strengthen product traceability and accelerate verification throughout distribution channels. Companies are expanding production capabilities, forming technology partnerships, and investing in intelligent authentication platforms to strengthen competitive positioning. Organizations capable of delivering scalable, regulation-ready, and highly secure printing solutions will establish lasting operational advantages across global authentication ecosystems.

Stringent authentication requirements across pharmaceuticals, banknotes, tax stamps, and premium consumer goods continue to strengthen demand for advanced anti-counterfeiting inks. More than 60% of newly introduced pharmaceutical packaging programs now incorporate multi-layer security features, while nearly 45% of premium brand owners have expanded covert authentication technologies to reduce illicit trade. China's stronger intellectual property enforcement and implementation of digital product traceability standards have accelerated adoption across manufacturing ecosystems. This regulatory shift improves supply-chain transparency while increasing demand for specialized security formulations. In response, leading manufacturers are investing in UV-reactive pigments, machine-readable inks, and digital verification partnerships to deliver integrated authentication platforms. Companies combining customized formulations with serialization technologies gain stronger customer retention, faster regulatory compliance, and higher-value contracts in security-sensitive industries.

Production of high-security inks relies on specialized fluorescent pigments, rare-earth compounds, and proprietary chemical formulations, exposing manufacturers to raw material availability and pricing fluctuations. Approximately 35% of critical security pigment inputs originate from concentrated supplier networks, while specialty material costs have increased by nearly 18% over recent procurement cycles. Export controls on strategic chemicals and longer qualification requirements for regulated industries further complicate sourcing strategies, particularly for European security printers. These constraints extend production lead times, compress operating margins, and slow customer deliveries. To reduce exposure, manufacturers are localizing procurement, signing long-term supply agreements, and qualifying alternative specialty materials. Diversified sourcing strategies increasingly determine operational resilience and competitive stability within high-security printing markets.

The convergence of advanced security inks with digital authentication platforms is creating high-value opportunities beyond conventional printing applications. Nearly 52% of global brand protection initiatives now evaluate physical-digital authentication solutions, while AI-enabled inspection systems improve counterfeit detection accuracy by approximately 30% compared with traditional manual verification. Japan and South Korea are expanding intelligent packaging programs that integrate QR-based traceability with invisible security inks for regulated industries. Companies are responding through R&D investments, software partnerships, and ecosystem development linking authentication, serialization, and blockchain verification. A significant emerging opportunity lies in reusable authentication architectures that enable continuous product verification throughout distribution, reducing inspection costs while strengthening consumer trust and regulatory compliance.

Deploying sophisticated anti-counterfeiting ink systems consistently across multinational supply chains remains operationally challenging due to equipment compatibility, workforce expertise, and evolving counterfeit techniques. Nearly 40% of printing facilities require production-line upgrades before implementing advanced security formulations, while operator training requirements increase implementation timelines by roughly 20%. India and other manufacturing-intensive economies continue expanding security printing capacity, yet inconsistent technology standards complicate cross-border authentication interoperability. These execution challenges affect deployment consistency, long-term competitiveness, and quality assurance across regulated industries. Companies must invest in standardized printing platforms, digital verification infrastructure, workforce development, and collaborative technology partnerships to maintain authentication integrity while adapting rapidly to increasingly sophisticated counterfeiting methods.

AI-Enabled Authentication Expansion: Brand owners are integrating AI-based inspection with security inks to strengthen authentication across packaging and regulated products. More than 48% of new verification systems now combine machine vision with UV or infrared security features, while automated inspection reduces verification time by nearly 30%. Stricter pharmaceutical traceability regulations and rising counterfeit activity are accelerating deployment. Companies are expanding software partnerships and embedding intelligent verification into production workflows to improve operational accuracy and reduce manual inspection costs.

Migration Toward Hybrid Security Features: Manufacturers are increasingly combining optically variable, magnetic, and invisible inks with QR codes and digital serialization instead of relying on standalone physical security. Around 55% of premium packaging programs now deploy layered authentication, while counterfeit detection accuracy improves by approximately 25% through hybrid verification. China and Germany continue expanding secure packaging standards, encouraging ink suppliers to redesign formulations that integrate seamlessly with digital tracking ecosystems and enterprise authentication platforms.

Localization of Security Ink Supply: Supply-chain resilience has become a strategic priority as specialty pigment sourcing remains concentrated among limited suppliers. Nearly 38% of manufacturers have diversified procurement networks since 2023, while localized production has shortened lead times by about 18%. Security ink producers are establishing regional manufacturing partnerships and qualifying multiple raw-material suppliers to maintain uninterrupted deliveries for banknote printing, tax stamps, and pharmaceutical packaging applications.

Sustainable High-Security Formulations: Environmental compliance is reshaping formulation strategies without compromising security performance. More than 42% of newly introduced security ink products feature lower-VOC compositions, while energy-efficient curing technologies reduce processing energy by nearly 15%. Regulatory pressure on chemical usage is encouraging manufacturers to modernize production processes, automate quality control, and accelerate commercialization of environmentally compliant authentication solutions for long-term industrial adoption.

UV Inks represent the largest segment, accounting for approximately 36% of total demand due to their broad compatibility with commercial printing equipment, pharmaceutical packaging, banknotes, and government documents. Their invisible security characteristics, rapid curing, and relatively lower implementation costs make them highly scalable across high-volume printing environments. Magnetic Inks maintain strong adoption in financial document processing, while Infrared (IR) Inks continue gaining traction for machine-readable authentication in logistics and customs verification. Optically Variable Inks (OVI) are the fastest-growing segment as governments and premium consumer brands increasingly deploy visually dynamic security features that are difficult to replicate. OVI adoption has expanded by nearly 22% across high-security printing programs, while Thermochromic Inks are strengthening their presence in premium packaging and promotional authentication. Companies are investing in advanced pigment technologies, hybrid ink formulations, and collaborative product development to enhance durability, counterfeit resistance, and digital compatibility. The remaining Others category continues serving niche industrial and customized authentication applications requiring specialized security characteristics.

Packaging & Labels remain the dominant application, contributing nearly 34% of market demand as manufacturers strengthen brand protection against counterfeit consumer products, pharmaceuticals, and food packaging. Increasing product serialization, retail authentication, and export compliance have made security inks operationally essential throughout packaging workflows. Banknotes & Currency continue representing a mature, high-value segment supported by central bank modernization initiatives and continuous security feature upgrades. Brand Protection & Product Authentication is the fastest-growing application, with enterprise deployment increasing by approximately 24% as luxury brands, electronics manufacturers, and industrial suppliers implement layered authentication strategies. Official Identity Documents maintain consistent demand through passport, visa, and national identity modernization projects, while Tax Stamps & Revenue Stamps remain strategically important for excise compliance and anti-smuggling enforcement. Ink manufacturers are expanding customized product portfolios, integrating digital verification capabilities, and strengthening partnerships with security printers to meet evolving authentication requirements across regulated industries.

Government & Banking constitute the largest end-user segment with an estimated 39% share owing to continuous demand for secure banknotes, passports, visas, tax stamps, and official certificates. National security requirements, central bank currency upgrades, and document authentication programs sustain stable procurement across developed and emerging economies. Pharmaceuticals represent another major customer group as serialization and anti-counterfeiting regulations become increasingly integrated into packaging operations. Pharmaceuticals are the fastest-growing end-user segment, with authentication deployments expanding by nearly 26% through stronger medicine traceability requirements and stricter regulatory oversight. Consumer Goods and Luxury Goods continue accelerating investments to protect premium brands against illicit trade, while Electronics manufacturers increasingly deploy covert authentication to secure components and aftermarket supply chains. Companies are responding through sector-specific formulations, collaborative development with packaging providers, and customized authentication platforms designed to address diverse operational requirements across each industry vertical. The Others segment continues supporting specialized industrial and institutional security applications.

Asia-Pacific accounted for the largest market share at 41.8% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 3.2% between 2026 and 2033.

North America represents approximately 26.4% of the global Anti-Counterfeiting Ink Market, supported by strong demand from pharmaceutical packaging, currency printing, secure government documentation, and premium consumer goods. Regulatory emphasis on product traceability and intellectual property protection continues to accelerate deployment of UV, infrared, and machine-readable security inks across high-value industries. Pharmaceutical serialization programs and digital authentication platforms are increasingly integrated with security printing operations, improving supply-chain visibility and verification efficiency. More than 60% of large security printing projects in the region now incorporate multi-layer authentication technologies. Security ink manufacturers are expanding strategic partnerships with packaging companies and technology providers to deliver interoperable authentication ecosystems while strengthening domestic production capabilities for regulated applications.

United States Market Outlook: The United States leads regional demand through its advanced pharmaceutical manufacturing, sophisticated currency printing infrastructure, and strong intellectual property enforcement framework. Federal authentication requirements and enterprise investments in secure packaging continue driving technology deployment across healthcare, electronics, and luxury goods industries. More than 65% of large pharmaceutical packaging facilities have implemented advanced serialization alongside security printing technologies, encouraging ink manufacturers to introduce customized formulations that support automated inspection, digital verification, and regulatory compliance across nationwide supply chains.

Europe accounts for approximately 23.8% of global market activity, supported by established security printing capabilities, advanced packaging technologies, and harmonized regulatory frameworks. Continuous modernization of banknotes, passports, tax stamps, and pharmaceutical packaging reinforces demand for high-security ink formulations. Environmental compliance is also encouraging wider adoption of lower-VOC specialty inks and energy-efficient curing technologies across commercial printing operations. Nearly 44% of newly commissioned security printing projects incorporate multiple authentication technologies within integrated production workflows. Companies continue strengthening research collaborations, expanding specialty pigment production, and modernizing manufacturing facilities to improve authentication performance while meeting increasingly stringent regulatory expectations.

Germany Market Outlook: Germany remains Europe's strategic manufacturing hub for security printing technologies due to its advanced chemical industry, precision engineering expertise, and strong packaging sector. High-value exports and industrial brand protection initiatives continue supporting enterprise investment in next-generation authentication solutions. Around 40% of regional industrial security printing equipment deployments involve German manufacturing facilities, enabling ink suppliers to collaborate closely with equipment manufacturers and packaging specialists on customized high-security printing technologies.

Asia-Pacific holds the largest regional position with approximately 41.8% of global demand, supported by extensive manufacturing capacity, expanding pharmaceutical production, government security printing programs, and rapidly growing consumer goods industries. Strong export activity and rising anti-counterfeiting enforcement have accelerated deployment of UV, magnetic, and optically variable security inks throughout industrial supply chains. More than 55% of newly installed secure packaging production lines across major manufacturing economies now integrate advanced authentication technologies. Companies continue expanding regional production facilities, establishing localized research centers, and strengthening partnerships with security printers to improve manufacturing flexibility while reducing supply-chain dependence on imported specialty materials.

China Market Outlook: China dominates regional demand through its extensive packaging industry, government document printing programs, pharmaceutical manufacturing base, and export-oriented industrial economy. Strong intellectual property enforcement and expanding digital traceability initiatives continue accelerating enterprise adoption of advanced authentication technologies. Nearly 31% of global high-security printing capacity is concentrated in China, encouraging manufacturers to invest in domestic specialty pigment production, intelligent inspection systems, and integrated authentication platforms supporting both domestic and international supply chains.

South America contributes approximately 5.2% of global market demand as governments strengthen tax stamp programs, pharmaceutical authentication, and secure packaging initiatives. Consumer goods manufacturers are increasingly deploying security inks to reduce illicit trade and improve product traceability throughout regional distribution networks. Around 28% of premium consumer packaging projects now include covert authentication features, reflecting growing enterprise awareness of brand protection requirements. Infrastructure limitations and dependence on imported specialty materials continue affecting production efficiency, yet strategic partnerships with international security printing companies are improving technology availability and operational capabilities across regulated industries.

Brazil Market Outlook: Brazil represents the region's largest opportunity owing to its extensive pharmaceutical manufacturing, food processing, and consumer goods sectors. Regulatory focus on product traceability and anti-counterfeiting initiatives continues encouraging adoption of advanced authentication technologies across domestic industries. More than 45% of regional pharmaceutical security printing demand originates from Brazil, prompting suppliers to strengthen local distribution networks, technical support capabilities, and customized security ink solutions for regulated manufacturers.

The Middle East & Africa account for approximately 2.8% of global demand, supported by national identity modernization programs, secure currency printing, and expanding pharmaceutical authentication requirements. Government investments in digital identity infrastructure and border security continue increasing deployment of sophisticated security inks across official documents and financial instruments. Nearly 35% of newly implemented government security printing initiatives now combine physical and digital authentication technologies to strengthen document integrity. Security solution providers are expanding regional partnerships, technical service networks, and localized support capabilities to address increasing public-sector procurement while improving operational resilience.

United Arab Emirates Market Outlook: The United Arab Emirates has established itself as the region's technology leader through extensive investment in secure government documentation, customs modernization, and digital identity infrastructure. National smart government initiatives continue driving adoption of advanced authentication solutions across public administration and high-value trade sectors. More than 50% of major government document modernization projects incorporate integrated security printing technologies, encouraging global manufacturers to strengthen regional partnerships and technical support operations within the country.

The competitive landscape is led by SICPA, Sun Chemical, Gleitsmann Security Inks, Kao Collins, and CTI, competing against specialized regional security ink manufacturers and cost-focused local suppliers. The top five companies collectively control approximately 58% of the global market, with competition centered on proprietary formulations, authentication performance, customization capability, and secure supply-chain control rather than price alone. Premium technology providers achieve counterfeit detection improvements of nearly 30%, while automated UV and IR-compatible formulations reduce production downtime by around 18% for industrial users. Regional suppliers compete through shorter delivery cycles and application-specific customization, whereas global leaders strengthen market position through capacity expansion, strategic partnerships with security printers, vertically integrated pigment production, and digital authentication platforms. Competition is increasingly shifting toward hybrid physical-digital security ecosystems and intelligent verification solutions. Proprietary chemistry, regulatory qualification, and customer validation remain major entry barriers. Winning requires continuous innovation, trusted authentication performance, resilient supply chains, and integrated security solutions.

Sun Chemical

Gleitsmann Security Inks GmbH

Kao Collins Inc.

Chromatic Technologies Inc. (CTI)

Flint Group

Siegwerk Druckfarben AG & Co. KGaA

Toyo Ink SC Holdings Co., Ltd.

DIC Corporation

InkTec Co., Ltd.

Microtrace LLC

Fujifilm Corporation

Advanced authentication technologies are transforming security inks beyond conventional fluorescent formulations. UV, infrared, optically variable, magnetic, and thermochromic inks are increasingly integrated into multilayer authentication systems supporting pharmaceuticals, banknotes, and premium consumer products. Nearly 62% of newly deployed security printing programs now combine at least two authentication technologies, improving verification reliability while reducing counterfeit acceptance rates. Integration with automated inspection systems strengthens manufacturing consistency and accelerates quality assurance throughout production workflows.

Disruptive innovation is shifting toward AI-assisted verification, digital serialization, blockchain-enabled traceability, and machine-readable covert markers. Compared with traditional visual inspection, AI-supported authentication improves inspection efficiency by approximately 35% while reducing manual verification costs by nearly 20%. Around 48% of enterprise authentication deployments now incorporate digital verification alongside physical security features. Global technology leaders and specialty ink innovators benefit most by delivering integrated authentication ecosystems that combine secure chemistry with intelligent software platforms.

Between 2026 and 2028, intelligent hybrid authentication platforms, nano-engineered pigments, and environmentally compliant specialty formulations will reshape competitive positioning. Wider adoption of cloud-connected verification systems, digital product passports, and smart packaging will strengthen supply-chain transparency and regulatory compliance. Companies investing today in interoperable security technologies, automated inspection infrastructure, and scalable authentication platforms will establish stronger operational resilience, higher customer retention, and sustainable differentiation as counterfeit methods become increasingly sophisticated.

October 2024 – Kao Collins introduced SIGMA+ and Pitch Black industrial ink formulations for HP printing systems, delivering PFAS-free, REACH-compliant performance and expanding sustainable industrial printing capabilities. The products support 100% regulatory-compliant formulations for targeted applications. Source: www.kaocollins.com

June 2025 – SICPA launched a year-long World Anti-Counterfeiting Day awareness initiative focused on security inks, authentication, and illicit trade prevention, reinforcing deployment of visible, machine-readable, and forensic security technologies across multiple industries. Business impact strengthened global brand-protection engagement. Source: www.sicpa.com

June 2025 – SICPA highlighted expanded deployment of advanced security inks supporting banknote authentication through visible, covert, and forensic protection layers, strengthening resilience against evolving counterfeit techniques while improving trust across secure payment ecosystems. Source: www.linkedin.com

April 2025 – SNS Insider identified increasing commercialization of AI-enabled authentication, UV security inks, and digital printing innovations, highlighting stronger enterprise adoption across packaging and secure document applications with expanding participation from leading specialty ink manufacturers.

This report provides comprehensive coverage of the Anti-Counterfeiting Ink Market across six ink types, six application segments, and six end-user categories, evaluating operational trends, technology adoption, authentication strategies, and competitive positioning. Regional assessment spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with detailed country-level analysis of major industrial hubs. The study examines advanced technologies including UV, infrared, optically variable, magnetic, thermochromic, AI-enabled verification, and digital authentication platforms while assessing deployment patterns across pharmaceuticals, banknotes, packaging, and secure government documentation.

The report also evaluates competitive dynamics, innovation strategies, supply-chain developments, manufacturing capabilities, and enterprise partnerships influencing market evolution between 2026 and 2033. More than 60% of the analysis focuses on high-value regulated industries and advanced authentication technologies, helping stakeholders identify investment priorities, expansion opportunities, emerging application areas, technology transitions, and competitive differentiation strategies for sustainable long-term business positioning.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 689.6 Million |

| Market Revenue (2033) | USD 853.4 Million |

| CAGR (2026–2033) | 2.7% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Companies Profiled | SICPA; Sun Chemical; Gleitsmann Security Inks GmbH; Kao Collins Inc.; Chromatic Technologies Inc. (CTI); Flint Group; Siegwerk Druckfarben AG & Co. KGaA; Toyo Ink SC Holdings Co., Ltd.; DIC Corporation; InkTec Co., Ltd.; Microtrace LLC; Fujifilm Corporation |

| Customization & Pricing | Available on Request (10% Customization Free) |