Reports

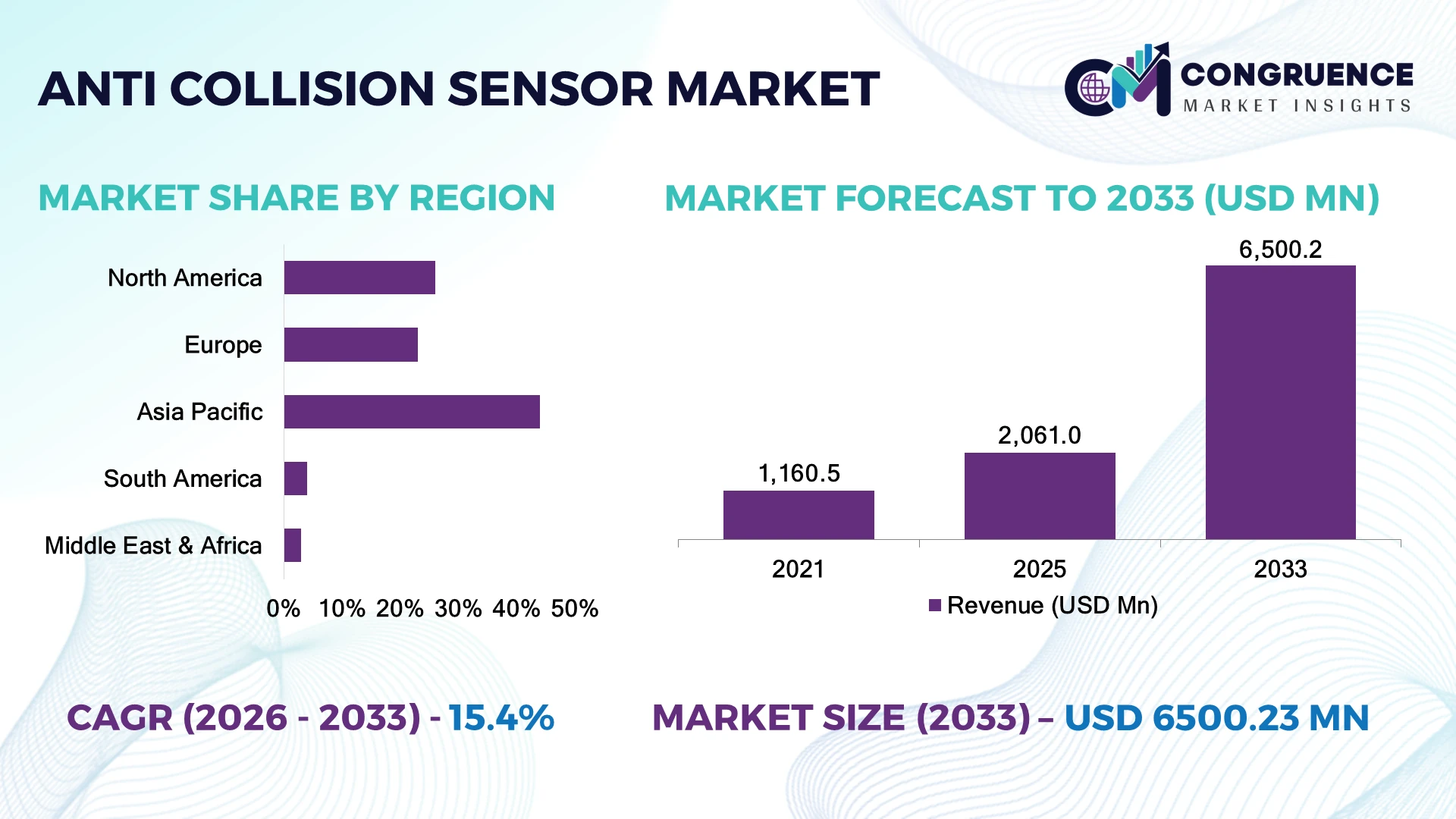

The Global Anti-collision Sensor Market was valued at USD 2,061.0 Million in 2025 and is anticipated to reach a value of USD 6,500.2 Million by 2033 expanding at a CAGR of 15.44% between 2026 and 2033. Growth is driven by accelerated ADAS integration, industrial automation, autonomous mobile equipment deployment, and stricter vehicle safety regulations across major automotive and manufacturing economies.

China accounts for approximately 34% of global anti-collision sensor manufacturing capacity, supported by large-scale EV production, smart manufacturing investments, and over 30 million annual vehicle production capacity. Germany remains a leading innovation hub with advanced automotive engineering and higher sensor integration per premium vehicle, while China's manufacturing scale exceeds Germany's output by more than 8x. Ongoing automotive supply-chain diversification across Asia further strengthens production resilience.

The market favors companies investing in AI-enabled sensing platforms, regional manufacturing expansion, and diversified supply-chain strategies.

Market Size & Growth: USD 2,061.0 Million in 2025, projected to reach USD 6,500.2 Million by 2033 at a CAGR of 15.44%, supported by rapid ADAS deployment and industrial automation.

Top Growth Drivers: ADAS adoption exceeds 22%, industrial automation expands by 18%, and warehouse robotics installations grow above 20% globally.

Short-Term Forecast: By 2028, sensor processing efficiency improves by over 25% while calibration time declines by nearly 18%.

Emerging Technologies: AI-enabled perception, sensor fusion, solid-state LiDAR, and edge computing significantly improve real-time collision detection.

Regional Leaders: Asia-Pacific exceeds USD 2,900 Million, North America surpasses USD 1,650 Million, and Europe approaches USD 1,300 Million, driven by intelligent mobility investments.

Consumer/End-User Trends: More than 65% of new premium passenger vehicles integrate advanced collision sensing technologies.

Pilot/Case Example: In 2024, automated logistics deployments improved warehouse navigation accuracy by over 30% through AI-based collision avoidance.

Competitive Landscape: Bosch leads with approximately 13% market share alongside Continental, Denso, Valeo, Aptiv, and ZF.

Regulatory & ESG Impact: Advanced vehicle safety regulations contribute to over 40% of new safety-system installations while reducing accident risks.

Investment & Funding: More than USD 4 Billion has been invested globally in intelligent sensing, strategic partnerships, and autonomous mobility expansion.

Anti-collision sensors are experiencing stronger demand across passenger vehicles, commercial fleets, warehouse robotics, mining equipment, and autonomous industrial machinery. AI-powered sensor fusion, compact radar modules, and solid-state LiDAR continue improving detection precision by over 30% under complex operating conditions. Increasing compliance with advanced vehicle safety regulations and resilient semiconductor supply-chain localization are accelerating deployment while setting the stage for broader strategic market developments.

The Anti-collision Sensor Market has become strategically important as intelligent mobility, automated manufacturing, and connected infrastructure increasingly rely on accurate real-time object detection. Vehicle safety mandates, logistics automation, and infrastructure modernization are encouraging manufacturers to strengthen production capabilities while diversifying component sourcing to improve operational resilience and reduce supply-chain disruptions.

AI-enabled sensor fusion systems provide up to 35% greater object recognition accuracy than conventional single-sensor platforms while reducing false detection events by approximately 20%. Asia-Pacific leads large-scale manufacturing and deployment through strong automotive production capacity, whereas Europe remains focused on premium vehicle innovation and high-performance sensing technologies. Over the next two to three years, integration of multi-sensor architectures is expected to become standard across a growing share of advanced vehicles and autonomous industrial equipment.

Major manufacturers are expanding partnerships with automotive OEMs, robotics companies, and semiconductor suppliers to accelerate product commercialization. For example, autonomous warehouse vehicles equipped with advanced anti-collision sensors have significantly improved navigation efficiency and workplace safety while lowering operational interruptions. Organizations that prioritize AI-driven sensing capabilities, scalable manufacturing, and diversified regional supply networks will strengthen competitive positioning and establish long-term operational advantages in this evolving market.

The accelerating adoption of advanced driver assistance systems (ADAS), autonomous equipment, and industrial automation is reshaping demand for anti-collision sensors. More than 65% of premium passenger vehicles now incorporate advanced sensing technologies, while warehouse automation installations have increased by over 20% globally. China continues expanding intelligent vehicle manufacturing through large-scale EV production, supported by stricter automotive safety standards. This shift is driving higher sensor content per vehicle and industrial machine. In response, companies are expanding semiconductor sourcing, investing in AI-enabled sensor fusion, and forming technology partnerships with automotive OEMs. A key strategic advantage lies in integrating radar, camera, and LiDAR platforms that improve operational reliability while reducing false detection events in complex environments.

High-performance anti-collision sensors remain exposed to semiconductor supply dependency, specialized component sourcing, and increasing integration costs. Advanced sensing modules can account for nearly 18% of electronic safety system costs, while semiconductor lead times have remained 15–20% above historical averages for several critical components. Germany and Japan continue facing procurement pressure for advanced automotive chips used in safety platforms. These constraints affect production planning, deployment schedules, and profit margins for manufacturers supplying intelligent mobility solutions. Companies are mitigating risks by localizing component sourcing, securing long-term semiconductor supply agreements, and redesigning platforms with standardized architectures that reduce dependence on single-source suppliers while improving manufacturing flexibility.

Artificial intelligence, software-defined vehicles, and connected infrastructure are creating new commercial opportunities beyond conventional automotive applications. AI-enabled sensor fusion improves object recognition accuracy by approximately 35%, while predictive perception algorithms reduce unnecessary braking events by nearly 20%. South Korea and the United States are accelerating smart transportation initiatives that integrate roadside sensing with connected vehicle ecosystems. Companies are increasing investment in solid-state LiDAR, edge AI processors, and cloud-connected safety platforms while collaborating with robotics and infrastructure providers. A significant strategic opportunity exists in industrial logistics, where unified sensing architectures can simultaneously improve fleet efficiency, workplace safety, and operational visibility across large automated facilities.

Deploying anti-collision sensing systems across connected vehicles and automated equipment requires seamless integration of cameras, radar, ultrasonic sensors, LiDAR, and embedded software. Sensor calibration accounts for nearly 12% of system commissioning time, while software validation requirements have increased by over 25% as safety functions become more autonomous. The United States is strengthening automotive cybersecurity expectations for connected vehicle platforms, increasing engineering complexity for manufacturers. Companies must address software interoperability, functional safety validation, and secure over-the-air updates through sustained R&D investment and cross-industry collaboration. Organizations that successfully standardize hardware-software integration and cybersecurity frameworks will achieve stronger long-term competitiveness and more consistent large-scale deployment.

AI Sensor Fusion Expansion Advanced sensor fusion platforms combining radar, cameras, and LiDAR are replacing single-sensor architectures, with integrated deployments increasing by nearly 30% and object recognition accuracy improving by over 35%. Automotive manufacturers in Germany and China are standardizing multi-sensor platforms to simplify vehicle software development. Companies are scaling AI software partnerships and unified electronic architectures, reducing validation cycles while improving real-time driving performance.

Software-Defined Safety Platforms Software-defined vehicle adoption is accelerating, with more than 40% of new premium vehicle programs supporting over-the-air safety updates and diagnostic functions. Regulatory emphasis on functional safety and connected mobility is encouraging manufacturers to separate hardware from software development. Companies are restructuring engineering workflows, expanding cloud-enabled validation, and shortening feature deployment timelines by approximately 20%, improving lifecycle efficiency without major hardware redesigns.

Industrial Automation Deployment Automated factories and logistics centers are increasing intelligent collision avoidance implementation, with autonomous mobile robot installations growing above 22% and operational downtime declining by nearly 18%. Labor shortages and productivity targets are accelerating automation across Japan and South Korea. Sensor manufacturers are expanding industrial partnerships and modular product portfolios, enabling faster integration into robotics, material handling, and smart manufacturing environments.

Localized Component Manufacturing Supply-chain resilience is becoming a competitive priority as localized electronic component sourcing expands by approximately 25% among leading automotive suppliers. India and Mexico are strengthening electronics manufacturing ecosystems to reduce procurement risk and transportation delays. Companies are diversifying supplier networks, increasing regional assembly capacity, and redesigning sensor modules around standardized components, improving production continuity while enhancing long-term operational flexibility.

Radar Sensors lead the market with an estimated 38% share due to superior all-weather detection capability, long operating range, and seamless integration with advanced driver assistance systems. Their ability to perform reliably in fog, rain, and low-visibility conditions makes them the preferred technology for automotive safety platforms and commercial transport applications. Camera Sensors continue to strengthen their position through AI-assisted object classification, while Ultrasonic Sensors remain essential for short-range parking and proximity detection because of their low implementation cost. Manufacturers are expanding radar production capacity and improving software integration to support increasingly automated mobility platforms. LiDAR Sensors represent the fastest-growing segment as declining component costs and improved solid-state architectures accelerate deployment in autonomous vehicles and industrial automation. Infrared Sensors are gaining relevance in night-time detection and specialized defense applications, while Other sensing technologies support niche operational environments. More than 55% of newly developed premium vehicle safety platforms now integrate multiple sensing technologies rather than relying on a single detection method, reflecting a clear investment shift toward hybrid perception systems.

Passenger Vehicles account for approximately 52% of market demand as automakers continue expanding advanced safety systems across both premium and mass-market models. Growing regulatory requirements, consumer preference for intelligent safety features, and higher integration of driver assistance technologies are strengthening deployment volumes. Commercial Vehicles remain a significant application because fleet operators increasingly prioritize accident prevention, operating efficiency, and insurance cost optimization. Manufacturers are expanding production partnerships with vehicle OEMs while integrating advanced perception software into standardized safety packages. Warehouse Robotics is the fastest-growing application as automated fulfillment centers continue modernizing logistics operations through autonomous mobile robots and intelligent navigation systems. Industrial Automation and Mining Equipment are also increasing adoption, particularly where worker safety and operational continuity remain critical priorities. Nearly 45% of newly commissioned warehouse automation projects now incorporate intelligent collision avoidance capabilities, highlighting a shift beyond traditional automotive demand into industrial mobility ecosystems.

The Automotive industry represents approximately 58% of total market demand, driven by high-volume vehicle production, expanding electronic safety content, and mandatory driver assistance requirements. Continuous investment in software-defined vehicles and intelligent mobility platforms strengthens purchasing activity among global manufacturers. Manufacturing companies also represent an important customer group as smart factories adopt autonomous transport equipment to reduce workplace incidents and improve production efficiency. Sensor suppliers are responding through customized safety platforms, long-term OEM partnerships, and scalable manufacturing strategies. Logistics & Warehousing is the fastest-growing end-user segment as distribution centers accelerate autonomous equipment deployment and digital warehouse transformation. Aerospace & Defense continues investing in specialized sensing platforms for unmanned systems and mission-critical operations, while Mining increases adoption to improve operator safety in hazardous environments. More than 35% of newly deployed autonomous industrial vehicles now incorporate advanced anti-collision sensing technologies, illustrating expanding demand beyond conventional automotive applications.

Asia-Pacific accounted for the largest market share at 44.0% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 16.1% between 2026 and 2033.

North America represents approximately 26% of the global market, supported by strong adoption of advanced driver assistance systems, autonomous logistics equipment, and industrial automation. The United States and Canada continue expanding intelligent manufacturing and connected mobility programs, increasing deployment of AI-enabled sensing platforms across automotive, warehouse automation, and mining operations. More than 70% of premium vehicles introduced in the region now incorporate multiple anti-collision sensing technologies. Automotive OEMs are strengthening partnerships with semiconductor suppliers and software developers to accelerate sensor integration while reducing validation timelines. Continuous investment in autonomous freight corridors and smart logistics infrastructure is improving operational efficiency, creating sustained demand for advanced collision detection solutions across commercial and industrial environments.

United States Market Outlook: The United States leads regional deployment through its extensive automotive manufacturing ecosystem, autonomous mobility development, and advanced semiconductor innovation. More than 80% of leading autonomous vehicle development programs incorporate multi-sensor perception systems combining radar, cameras, and LiDAR. Continued investment in intelligent transportation infrastructure, robotics, and industrial automation is strengthening domestic production capabilities while encouraging technology partnerships between automotive OEMs, software providers, and electronic component manufacturers.

Europe accounts for approximately 23% of the global market, supported by advanced automotive engineering, strict vehicle safety standards, and continuous investment in intelligent mobility technologies. Germany, France, and Sweden remain major innovation centers for sensor-enabled vehicle platforms and industrial automation systems. Automotive manufacturers are expanding software-defined vehicle programs while integrating advanced radar and camera technologies into broader model portfolios. More than 60% of newly launched premium passenger vehicles in the region include enhanced collision avoidance capabilities. Strategic collaborations between automotive suppliers and semiconductor companies continue improving product validation, manufacturing efficiency, and functional safety compliance across increasingly connected transportation ecosystems.

Germany Market Outlook: Germany remains Europe's technology leader through its concentration of global automotive OEMs, advanced electronics suppliers, and engineering expertise. Premium vehicle manufacturers continue increasing deployment of AI-enabled perception systems while expanding investments in software validation and autonomous mobility testing. Strong manufacturing capabilities and integrated supplier networks allow rapid commercialization of intelligent sensing technologies, reinforcing Germany's position as a leading innovation hub for advanced vehicle safety solutions.

Asia-Pacific holds approximately 44% of the global market due to unmatched automotive production capacity, electronics manufacturing, and expanding industrial automation. China, Japan, South Korea, and India continue strengthening domestic semiconductor ecosystems while accelerating deployment of intelligent mobility technologies. China alone produces more than 30 million vehicles annually, creating substantial demand for advanced sensing components across passenger and commercial vehicles. Manufacturers are expanding production facilities, localizing supply chains, and increasing AI-enabled sensor development to support both domestic consumption and global exports. Large-scale investment in smart manufacturing and autonomous logistics further reinforces the region's dominant competitive position.

China Market Outlook: China leads the global market through extensive EV manufacturing, advanced electronics production, and rapid deployment of intelligent transportation technologies. Approximately 34% of global anti-collision sensor manufacturing capacity is concentrated within the country, supported by strong government-backed industrial modernization initiatives. Domestic manufacturers continue investing in semiconductor production, AI-enabled perception software, and integrated sensing platforms while expanding export capabilities across automotive and industrial automation sectors.

South America represents approximately 4% of the global market, with demand primarily supported by commercial fleet modernization, mining operations, and expanding logistics infrastructure. Brazil and Chile are increasing adoption of intelligent safety technologies across transportation and industrial sectors to improve operational reliability and worker protection. Fleet operators are integrating advanced collision avoidance systems to reduce accident-related downtime and improve asset utilization. Continued investment in mining automation and warehouse modernization is supporting wider deployment of intelligent sensing platforms despite infrastructure limitations and imported component dependence. Technology providers are strengthening regional distribution partnerships and localized technical support to improve implementation efficiency.

Brazil Market Outlook: Brazil leads regional adoption through its large automotive manufacturing base, expanding commercial vehicle sector, and modernizing logistics network. Increasing deployment of intelligent fleet management systems and warehouse automation is driving greater demand for anti-collision sensing technologies. Automotive manufacturers and industrial equipment suppliers continue expanding technology partnerships while improving local integration capabilities to support safer and more efficient transportation and manufacturing operations.

The Middle East & Africa accounts for approximately 3% of the global market, supported by infrastructure modernization, smart city initiatives, and increasing investment in industrial automation. The United Arab Emirates and Saudi Arabia continue deploying intelligent transportation technologies alongside automated logistics and construction equipment. Major infrastructure developments are encouraging wider adoption of advanced collision avoidance systems across commercial fleets and heavy industrial machinery. Companies are strengthening regional partnerships while expanding technical support capabilities to improve deployment efficiency. Mining operations in Africa are also adopting intelligent sensing technologies to enhance operational safety and equipment productivity under demanding working conditions.

Saudi Arabia Market Outlook: Saudi Arabia is emerging as the region's leading market through significant investment in smart infrastructure, industrial diversification, and intelligent transportation projects. Large-scale development programs are accelerating deployment of automated construction equipment and connected logistics platforms equipped with advanced sensing technologies. Continued investment in industrial digitalization and infrastructure modernization is encouraging international technology providers to establish regional partnerships and expand long-term operational capabilities.

Bosch, Continental, Denso, Aptiv, Valeo, and ZF compete aggressively against regional sensor manufacturers and specialist LiDAR developers, while automotive OEMs increasingly challenge traditional Tier-1 suppliers through in-house software integration. The top five players collectively control approximately 52% of the market, creating a moderately consolidated structure. Competition centers on sensing accuracy, AI-enabled perception, supply-chain resilience, and platform customization rather than price alone. Leading suppliers have reduced sensor calibration time by nearly 20% and improved object detection accuracy by over 30% through integrated radar-camera architectures. Global leaders expand manufacturing footprints, form semiconductor partnerships, and vertically integrate software capabilities, while regional competitors emphasize cost-efficient production and localized engineering support. The competitive landscape is shifting toward software-defined sensing, making algorithm performance as critical as hardware quality. High functional safety certification requirements and semiconductor sourcing remain significant entry barriers. Winning requires scalable AI platforms, resilient supply networks, rapid validation, deep OEM collaboration, and continuous innovation capabilities consistently.

Continental AG

Denso Corporation

Aptiv PLC

Valeo SA

ZF Friedrichshafen AG

HELLA GmbH & Co. KGaA

Innoviz Technologies Ltd.

Luminar Technologies, Inc.

Ouster, Inc.

Arbe Robotics Ltd.

Aeva Technologies, Inc.

Multi-sensor perception platforms combining radar, cameras, ultrasonic sensors, and LiDAR are becoming the industry benchmark for intelligent collision avoidance. AI-powered sensor fusion improves object recognition accuracy by approximately 35% while reducing false detection events by nearly 20% compared with conventional single-sensor systems. More than 55% of newly developed premium vehicle safety platforms now incorporate hybrid sensing architectures, enabling faster environmental interpretation and greater operational reliability.

Emerging technologies include solid-state LiDAR, edge AI processors, high-resolution imaging radar, and software-defined sensing platforms that separate hardware from software upgrades. Compared with legacy mechanical LiDAR, solid-state designs reduce component complexity by nearly 40% while improving durability and lowering maintenance requirements. Automotive OEMs, robotics manufacturers, and industrial automation providers benefit from shorter product validation cycles and easier integration across multiple vehicle and equipment platforms.

Between 2026 and 2028, AI-driven predictive perception, vehicle-to-everything connectivity, and cloud-assisted safety analytics are expected to accelerate deployment across intelligent mobility and automated industrial environments. More than 60% of advanced autonomous systems are projected to integrate centralized perception software, strengthening real-time decision-making and operational scalability. Companies investing early in software-defined sensing, semiconductor optimization, and unified sensor architectures will secure stronger competitive differentiation and faster commercialization.

September 2024 – Luminar Technologies announced that the Volvo EX90 officially began customer deliveries, making it one of the first global production vehicles to feature long-range LiDAR as standard equipment. The company highlighted a technology platform supporting approximately 24 commercial vehicle programs, reinforcing large-scale automotive deployment and production maturity.

April 2024 – Valeo received the Automotive News PACE Award for its SCALA™ 3 LiDAR. The automotive-grade system delivers more than 12 million pixels per second and supports Level 3 autonomous driving up to 130 km/h (80 mph). The recognition strengthens Valeo's leadership in production-ready LiDAR and software-defined vehicle technologies. Source: www.valeo.com

October 2024 – Luminar Technologies announced an additional Volvo vehicle program alongside a new advanced development contract with a major Japanese automaker. The company also reported shipping more LiDAR units in Q3 2024 than in the previous three quarters combined, demonstrating accelerating production and stronger OEM adoption.

October 2024 – Bosch showcased its latest AI-enabled radar, ultrasonic sensors, and hardware-agnostic video perception software during its U.S. Experience Days. The company introduced a new generation of radar and ultrasonic sensors with artificial intelligence, supporting next-generation ADAS deployment and expanding software-defined vehicle capabilities. Source: www.us.bosch-press.com

The report provides comprehensive analysis across Radar Sensors, Ultrasonic Sensors, LiDAR Sensors, Camera Sensors, Infrared Sensors, and Other sensing technologies, together with applications spanning Passenger Vehicles, Commercial Vehicles, Industrial Automation, Warehouse Robotics, Mining Equipment, and additional emerging use cases. It further evaluates demand across Automotive, Manufacturing, Logistics & Warehousing, Aerospace & Defense, Mining, and other end-user industries. Regional assessment covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa while examining deployment trends, technology adoption, and competitive positioning.

The study assesses AI-enabled sensor fusion, software-defined sensing, edge computing, and advanced perception technologies alongside evolving supply-chain strategies and manufacturing capabilities. With analysis of leading industry participants, segment performance, adoption patterns exceeding 55% in advanced vehicle platforms, and enterprise deployment trends, the report supports investment planning, product expansion, partnership strategies, competitive benchmarking, and long-term business decision-making across the global anti-collision sensor ecosystem between 2026 and 2033.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 2,061.0 Million |

| Market Revenue (2033) | USD 6,500.2 Million |

| CAGR (2026–2033) | 15.44% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Companies Profiled | Robert Bosch GmbH; Continental AG; Denso Corporation; Aptiv PLC; Valeo SA; ZF Friedrichshafen AG; HELLA GmbH & Co. KGaA; Innoviz Technologies Ltd.; Luminar Technologies, Inc.; Ouster, Inc.; Arbe Robotics Ltd.; Aeva Technologies, Inc. |

| Customization & Pricing | Available on Request (10% Customization Free) |