Reports

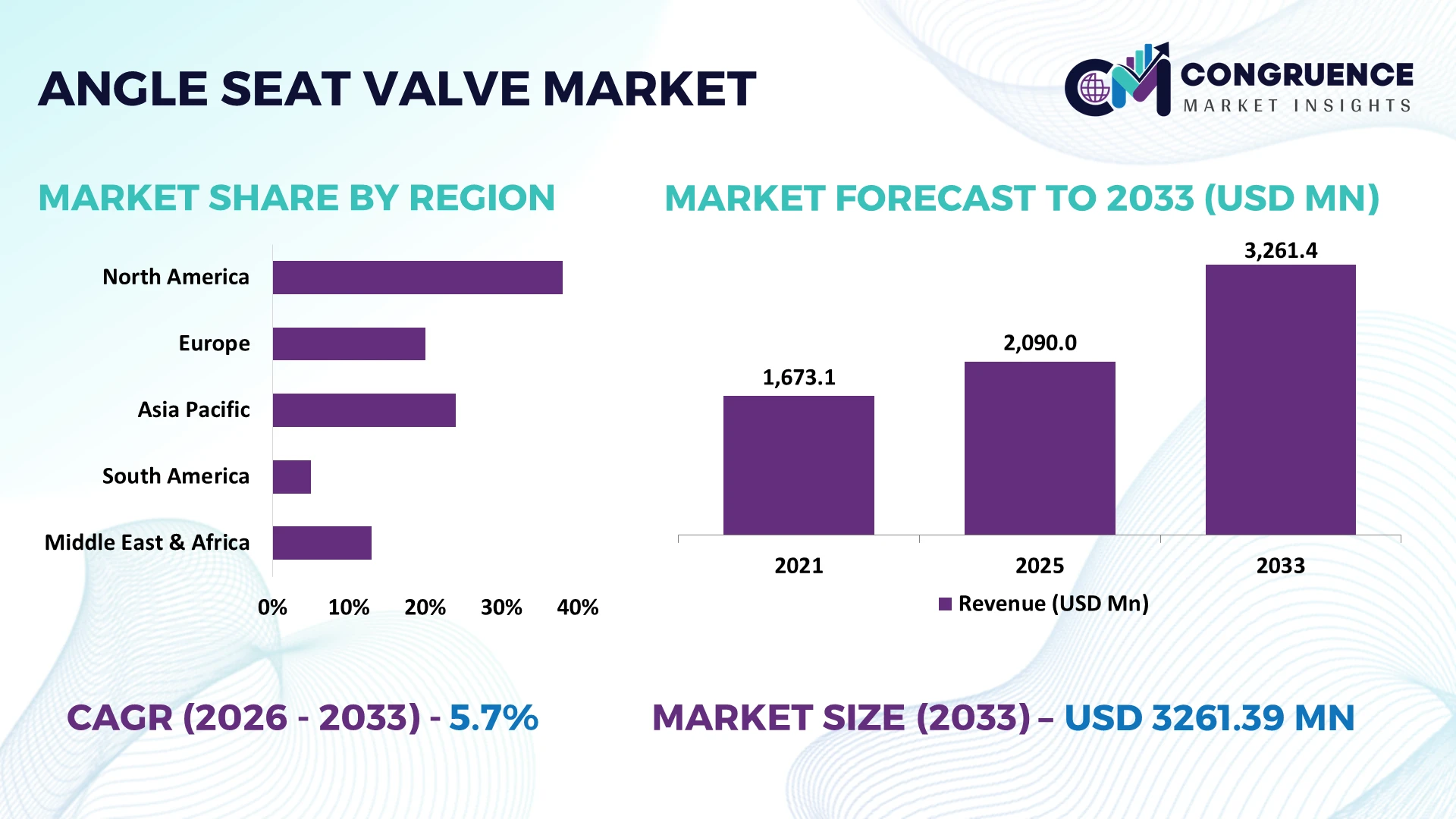

The Global Angle Seat Valve Market was valued at USD 2090 Million in 2025 and is anticipated to reach a value of USD 3261.39 Million by 2033 expanding at a CAGR of 5.72% between 2026 and 2033. Growth is being driven by accelerating automation across food processing, pharmaceuticals, chemicals, and water treatment facilities, where high-cycle, corrosion-resistant flow control systems improve process reliability and reduce maintenance intervals.

Germany remains the dominant manufacturing hub, accounting for approximately 24% of Europe's industrial valve production, supported by advanced automation investments, strong pharmaceutical and chemical processing capacity, and widespread Industry 4.0 deployment exceeding 65% across large manufacturers. Compared with India, where industrial automation adoption continues to expand rapidly through manufacturing initiatives, Germany maintains higher precision valve integration and export competitiveness despite ongoing global supply-chain realignment following Red Sea logistics disruptions in 2026.

The market favors manufacturers expanding localized production, automation-ready product portfolios, and resilient regional supply networks to strengthen long-term competitive positioning.

Market Size & Growth: USD 2,090 million in 2025 to USD 3,261.39 million by 2033 at 5.72% CAGR, driven by industrial automation and high-performance process control.

Top Growth Drivers: Automation adoption exceeds 60%, stainless-steel valve demand rises 18%, and pharmaceutical processing capacity expands over 12%.

Short-Term Forecast: By 2028, automated valve systems reduce maintenance costs by nearly 20% while improving production uptime by approximately 15%.

Emerging Technologies: AI-based predictive maintenance, smart pneumatic actuators, and advanced corrosion-resistant alloys improve operational efficiency by over 25%.

Regional Leaders: Asia-Pacific approaches USD 1.2 billion, Europe exceeds USD 900 million, and North America nears USD 700 million, supported by manufacturing modernization and regional expansion.

Consumer/End-User Trends: More than 55% of new processing facilities prioritize automated hygienic valve installations for continuous operations.

Pilot/Case Example: In 2026, a pharmaceutical production upgrade improved process efficiency by 18% through intelligent pneumatic valve integration.

Competitive Landscape: Leading suppliers collectively control approximately 38% of global demand alongside Bürkert, GEMÜ, Emerson, Spirax Sarco, and Parker Hannifin.

Regulatory & ESG Impact: Water-efficiency initiatives reduce process losses by nearly 15%, accelerating adoption of energy-efficient valve technologies.

Investment & Funding: More than USD 900 million supports manufacturing expansion, automation partnerships, and regional production localization amid supply-chain diversification.

Innovation & Future Outlook: Digital diagnostics, modular valve platforms, and IIoT connectivity strengthen predictive maintenance while enabling faster deployment across advanced industrial facilities.

Angle seat valve demand continues to strengthen across pharmaceutical manufacturing, food processing, beverage production, and water treatment, where hygienic operation and fast actuation remain critical. Smart pneumatic control, integrated condition monitoring, and wear-resistant materials improve operational efficiency by approximately 22%. Increasing localization of industrial component sourcing in 2026 further supports supply resilience, setting the foundation for the following strategic market assessment.

Industrial manufacturers increasingly view the Angle Seat Valve Market as a strategic component of production efficiency because automated flow control directly influences uptime, product quality, and maintenance planning. Infrastructure modernization across pharmaceutical, food processing, biotechnology, and water treatment facilities is accelerating replacement of legacy manual valves with intelligent pneumatic systems. At the same time, supply-chain restructuring is encouraging manufacturers to establish localized component sourcing and regional assembly operations, reducing procurement risks while improving delivery performance for mission-critical industrial applications.

Modern smart angle seat valves equipped with position feedback and predictive diagnostics lower unplanned maintenance by approximately 25% and reduce compressed-air consumption by nearly 15% compared with conventional pneumatic valve systems. Germany continues to lead in precision industrial automation and advanced valve engineering, while India is expanding deployment through new manufacturing facilities and process automation investments, creating a faster installation pipeline across chemical and food production plants. Over the next two to three years, digital valve monitoring adoption is expected to exceed 40% among newly commissioned automated process lines.

A practical example is pharmaceutical manufacturers integrating hygienic angle seat valves into clean-in-place systems to shorten maintenance shutdowns while improving production consistency. Leading companies are expanding engineering partnerships, investing in localized manufacturing, and strengthening digital service capabilities to deliver lifecycle support rather than standalone hardware. Organizations combining automation-ready products with resilient supply networks and predictive maintenance services will secure stronger competitive positioning as industrial operations continue shifting toward intelligent process control.

Industrial automation remains the primary structural driver for angle seat valve adoption as manufacturers prioritize continuous production, hygiene compliance, and lower maintenance costs. More than 60% of newly automated pharmaceutical and food processing facilities now specify pneumatic valve systems, while predictive maintenance technologies reduce unexpected downtime by approximately 25% and maintenance interventions by nearly 18%. Germany continues expanding smart manufacturing investments, reinforcing demand for intelligent flow-control equipment across high-value production lines. In response, valve manufacturers are increasing localized production, developing digitally connected actuator platforms, and forming automation partnerships with system integrators. This transition shifts competition from component supply toward complete process-control solutions, creating stronger customer retention through integrated lifecycle services.

Price fluctuations in stainless steel, precision castings, and pneumatic control components continue to pressure manufacturing costs and procurement planning. Industrial-grade stainless-steel input prices have experienced periodic swings exceeding 15%, while delivery lead times for specialized actuator components remain approximately 20% longer than pre-disruption benchmarks in several supply networks. China remains a critical production base for numerous precision valve components, increasing exposure to logistics disruptions and trade-related uncertainty. Manufacturers are reducing operational risk through supplier diversification, localized machining capacity, and long-term procurement agreements. Companies capable of stabilizing inventory availability gain a meaningful operational advantage by improving production scheduling and delivery reliability.

Digital transformation is opening new opportunities through intelligent valve platforms combining sensors, diagnostics, and industrial connectivity. Smart monitoring solutions improve maintenance planning by nearly 30%, while automated process optimization increases production efficiency by approximately 18% in high-cycle operations. India is expanding advanced manufacturing infrastructure, creating attractive opportunities for localized valve production and engineering partnerships supporting industrial automation programs. Companies are accelerating research into IIoT-enabled actuators, modular valve architectures, and digital asset management platforms that simplify lifecycle maintenance. A less obvious opportunity lies in subscription-based predictive maintenance services, allowing manufacturers to generate recurring revenue beyond traditional equipment sales while strengthening long-term customer relationships.

The greatest long-term challenge is integrating intelligent angle seat valves into existing production environments with mixed automation architectures and aging control infrastructure. Nearly 45% of industrial facilities continue operating hybrid systems requiring customized integration, while engineering commissioning can extend project timelines by approximately 20%. Japan and other mature manufacturing economies face additional workforce shortages in industrial automation, limiting deployment speed for advanced process-control systems. Companies must strengthen software interoperability, workforce training, cybersecurity resilience, and engineering collaboration to ensure reliable implementation across complex industrial operations. Those investing in standardized communication protocols and scalable digital service capabilities will achieve more consistent deployment performance and stronger long-term competitiveness.

Smart Valve Intelligence Expansion Intelligent angle seat valves with integrated position sensors and predictive diagnostics are becoming standard across automated production lines. More than 42% of newly installed industrial valve systems now include digital monitoring, while predictive maintenance reduces unplanned shutdowns by nearly 24% and maintenance labor by 18%. German manufacturers are accelerating software integration through automation partnerships, enabling faster commissioning and lifecycle service offerings as industrial operators prioritize continuous production over reactive maintenance.

Localized Manufacturing Networks Supply-chain diversification is reshaping procurement strategies as manufacturers reduce dependence on single-country sourcing. Localized component manufacturing has increased by approximately 20% across key industrial hubs, while average procurement lead times have fallen by nearly 15% through regional assembly models. Triggered by continued logistics disruptions and industrial resilience planning, companies are expanding machining capacity, qualifying multiple suppliers, and restructuring inventory management to improve delivery consistency and operational flexibility.

Hygienic Process Design Adoption Food processing and pharmaceutical facilities are increasingly specifying stainless steel angle seat valves with enhanced clean-in-place compatibility. Hygienic valve installations have expanded by approximately 28%, while cleaning cycle duration has declined by nearly 16% through optimized internal flow geometry. Equipment suppliers are introducing modular product platforms and collaborating with process engineering firms to simplify validation requirements and accelerate installation across regulated manufacturing environments.

Energy-Efficient Pneumatic Systems Industrial operators are optimizing compressed-air consumption to reduce operating costs and improve sustainability performance. Advanced pneumatic actuator designs lower air usage by around 14%, while valve response speed improves by nearly 12% compared with previous-generation systems. Japanese manufacturers are emphasizing lightweight actuator engineering and digital pressure control, encouraging companies to modernize existing production assets instead of undertaking complete process replacements.

Pneumatic angle seat valves remain the dominant segment, accounting for approximately 44% of total market demand due to their fast response, durability, and seamless compatibility with automated industrial processes. Their widespread deployment across pharmaceutical, food processing, and chemical manufacturing supports continuous production with lower maintenance requirements. Stainless Steel valves maintain strong demand where corrosion resistance and hygienic compliance are essential, while Brass valves remain cost-effective for utility and general industrial applications. High Pressure variants continue expanding in heavy-duty processing environments requiring superior pressure handling and operational reliability.

Electric angle seat valves are the fastest-growing type, with adoption increasing by nearly 22% as manufacturers expand digital process control and remote monitoring capabilities. Demand for High Pressure models has also risen by approximately 17% across advanced production facilities. Companies are strengthening product portfolios through intelligent actuator development, modular valve platforms, and automation partnerships, reflecting a strategic shift toward digitally connected and application-specific flow-control solutions.

Pharmaceuticals represent the leading application segment with an estimated 31% share, supported by strict hygiene requirements, sterile processing environments, and extensive use of clean-in-place systems. Food Processing remains a major application due to expanding automated production lines, while Chemical Processing sustains demand through corrosion-resistant fluid handling solutions. Steam Systems continue serving high-temperature industrial operations, and Water Treatment benefits from infrastructure modernization and increasing automation across municipal and industrial facilities.

Water Treatment is the fastest-growing application as utilities accelerate digital infrastructure upgrades and process automation. Smart valve deployment has increased by approximately 21%, while automated control systems improve operational efficiency by nearly 18%. Manufacturers are expanding application-specific product lines, integrating intelligent monitoring capabilities, and collaborating with engineering partners to deliver customized process-control solutions that enhance reliability and reduce maintenance requirements.

Chemicals remain the largest end-user segment, accounting for approximately 34% of market demand because of continuous production processes, demanding operating conditions, and high-volume fluid handling requirements. Pharmaceutical manufacturers continue expanding investments in sterile production systems, while Food & Beverage companies prioritize hygienic valve installations to improve product quality and operational consistency. Water Utilities maintain steady procurement through modernization programs, whereas Power Plants increasingly deploy specialized valve solutions to improve steam management and equipment reliability.

Pharmaceuticals are the fastest-growing end-user category, with automated valve deployment increasing by nearly 24% as manufacturers modernize production facilities. Food & Beverage processing has improved intelligent valve integration by approximately 19% through factory automation initiatives. Suppliers are responding with customized hygienic product portfolios, long-term service agreements, application-focused engineering support, and strategic partnerships that strengthen customer retention and improve lifecycle value.

North America accounted for the largest market share at 36.8% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a 6.8% CAGR between 2026 and 2033.

Advanced Process Automation Strengthens Industrial Competitiveness

North America maintains the leading position through extensive deployment across pharmaceutical manufacturing, food processing, chemicals, and municipal water infrastructure. The region contributes approximately 37% of global demand, supported by high automation intensity and strong replacement activity for aging process-control equipment. More than 65% of newly commissioned pharmaceutical production facilities integrate automated valve systems to improve process consistency and regulatory compliance. Investments in digital manufacturing and predictive maintenance platforms continue to accelerate equipment modernization, while strategic partnerships between automation providers and valve manufacturers improve system interoperability. Companies are increasingly prioritizing lifecycle service contracts, digital diagnostics, and localized engineering support to strengthen long-term customer relationships and reduce operational downtime.

United States Market Outlook: The United States remains the region's largest market because of its extensive pharmaceutical, biotechnology, chemical, and food processing industries. More than 70% of large industrial facilities operate advanced automation platforms requiring intelligent flow-control equipment. Domestic manufacturers continue expanding engineering capabilities, smart manufacturing investments, and production modernization initiatives, enabling stronger adoption of digitally integrated angle seat valves across high-value industrial operations.

Precision Manufacturing Drives Technology Leadership

Europe represents a mature industrial market supported by advanced manufacturing standards, stringent process quality requirements, and extensive automation across pharmaceutical and chemical industries. The region accounts for approximately 30% of global deployment, with precision-engineered valve systems forming an essential part of automated production environments. Industrial modernization initiatives have increased digital valve monitoring installations by nearly 24% across newly upgraded facilities. Manufacturers continue investing in energy-efficient pneumatic technologies, corrosion-resistant materials, and standardized industrial communication systems to improve operational reliability. Sustainability-focused industrial upgrades are further encouraging replacement of conventional process-control equipment with intelligent valve platforms that reduce maintenance requirements and compressed-air consumption.

Germany Market Outlook: Germany serves as Europe's industrial center for precision valve engineering, supported by globally competitive machinery manufacturing and Industry 4.0 implementation. More than 65% of large manufacturers utilize advanced factory automation technologies, creating sustained demand for intelligent angle seat valves. Continuous investment in industrial digitization, engineering innovation, and export-oriented manufacturing strengthens Germany's leadership across pharmaceutical, food processing, and chemical production sectors.

Manufacturing Expansion Accelerates Industrial Deployment

Asia-Pacific is the fastest-expanding regional market as industrial capacity, infrastructure investment, and manufacturing automation continue to advance rapidly. The region contributes approximately 28% of global demand while experiencing significant deployment across food processing, pharmaceuticals, electronics manufacturing, and water infrastructure. Industrial automation installations have increased by nearly 26% across major manufacturing economies, supported by expanding domestic production capabilities and factory modernization. Manufacturers are strengthening regional supply chains, establishing localized production facilities, and increasing engineering partnerships to improve delivery flexibility. Export-oriented industrial development and rising investment in automated process industries continue positioning the region as a critical production and consumption hub.

China Market Outlook: China remains the region's largest market because of its broad manufacturing ecosystem, expanding pharmaceutical production, and extensive industrial automation initiatives. More than 50% of newly established high-volume manufacturing facilities incorporate automated fluid-control systems to improve operational efficiency. Domestic manufacturers continue expanding precision machining capacity, intelligent valve production, and automation partnerships, reinforcing China's competitive position within global industrial equipment supply chains.

Industrial Modernization Supports Demand Expansion

South America continues strengthening demand through investments in food processing, mining, chemicals, and water treatment infrastructure. The region accounts for approximately 6% of global market activity, with modernization programs encouraging greater adoption of automated process-control equipment. Industrial facility upgrades have improved automation deployment by nearly 17% across selected manufacturing sectors, although infrastructure limitations and uneven industrial investment continue influencing project timelines. Companies are responding by expanding regional distribution networks, improving technical support capabilities, and partnering with local engineering firms to enhance equipment availability and after-sales services. Operational efficiency and equipment durability remain key purchasing priorities across industrial customers.

Brazil Market Outlook: Brazil represents the region's largest opportunity due to its diversified manufacturing base, expanding food processing sector, and significant chemical production capacity. Industrial modernization programs continue increasing demand for automated process equipment, while investment in water infrastructure strengthens deployment of reliable valve technologies. Local distributors and international manufacturers are expanding technical service networks to improve customer support and shorten project implementation cycles.

Infrastructure Investment Reshapes Industrial Demand

The Middle East & Africa market is advancing through expanding investments in industrial infrastructure, water management, petrochemical facilities, and manufacturing diversification. The region contributes approximately 5% of global demand, with automation adoption increasing across large-scale industrial projects. More than 18% of newly commissioned processing facilities now integrate intelligent flow-control equipment to improve operational efficiency and asset reliability. Industrial diversification initiatives, combined with modernization of utility infrastructure, are encouraging manufacturers to introduce application-specific valve technologies and strengthen regional engineering partnerships. Companies are focusing on localized service capabilities and project-based collaboration to improve long-term operational performance.

Saudi Arabia Market Outlook: Saudi Arabia leads regional demand through extensive industrial diversification, petrochemical expansion, and infrastructure modernization programs. Large-scale manufacturing and water management projects continue increasing deployment of automated process-control systems across critical facilities. Ongoing investment in industrial technology, engineering services, and smart manufacturing initiatives strengthens demand for high-performance angle seat valves while creating long-term opportunities for international and regional equipment suppliers.

Competition in the Angle Seat Valve Market is led by Bürkert Fluid Control Systems, GEMÜ Group, Emerson Electric, Spirax Sarco, and Parker Hannifin, which compete directly against regional manufacturers offering lower-cost alternatives across Asia and Eastern Europe. The top five players collectively account for approximately 43% of global market activity, creating a moderately consolidated structure where technology leadership outweighs price competition in regulated industries. Global leaders differentiate through intelligent valve platforms, customized engineering, and lifecycle services, while regional suppliers compete on procurement flexibility and delivery speed. Smart valve adoption improves maintenance efficiency by nearly 25%, and localized manufacturing reduces delivery lead times by approximately 18%, strengthening customer retention. Companies are expanding production facilities, forming automation partnerships, and integrating digital diagnostics with industrial control systems to secure long-term contracts. Competitive momentum is shifting toward software-enabled process optimization and vertically integrated manufacturing. High certification requirements, precision engineering capability, and automation expertise remain major entry barriers. Sustainable success depends on combining intelligent products, localized supply resilience, application expertise, and responsive engineering support.

Bürkert Fluid Control Systems

GEMÜ Group

Emerson Electric Co.

Spirax Sarco PLC

Parker Hannifin Corporation

IMI plc

Schubert & Salzer Control Systems GmbH

Festo SE & Co. KG

Christian Bürkert GmbH & Co. KG

Rotex Automation Limited

Bray International, Inc.

AVK Holding A/S

Neles Corporation

KITZ Corporation

Current technology development is centered on intelligent pneumatic actuation, digital position feedback, and IIoT-enabled condition monitoring. More than 46% of newly automated process facilities now deploy smart valve systems capable of real-time diagnostics, while predictive maintenance lowers unexpected downtime by approximately 24%. Integration with industrial Ethernet and PLC platforms enables centralized process visibility, improving maintenance planning and production continuity across pharmaceutical, chemical, and food manufacturing operations.

Emerging innovation between 2026 and 2028 includes AI-assisted valve diagnostics, self-calibrating actuators, and advanced stainless-steel flow geometries that minimize pressure loss. Compared with conventional pneumatic valve systems, next-generation intelligent valves improve response accuracy by nearly 20% while reducing compressed-air consumption by approximately 15%. Digital twin integration is also expanding, with adoption expected to exceed 35% in newly commissioned automated facilities, allowing operators to optimize asset performance before physical deployment.

Technology leadership increasingly benefits manufacturers offering integrated hardware, software, and lifecycle services instead of standalone valves. Companies investing in modular electronics, cybersecurity-ready communication protocols, and predictive analytics strengthen competitive differentiation while reducing customer operating costs. Organizations delaying digital valve integration risk losing specification opportunities as industrial buyers increasingly prioritize connected, automation-ready process control solutions.

November 2024 Bürkert Fluid Control Systems expanded its collaboration with Ascon Systems by integrating Digital Twin technology into industrial fluid control solutions, enabling hardware-independent process optimization and faster engineering workflows. The initiative improves application flexibility across automated process industries. Source: Bürkert

December 2024 GEMÜ introduced its LEAP product generation, including the new GEMÜ S40 angle seat valve with a modular platform architecture that reduces product complexity while improving manufacturing efficiency and application flexibility across hygienic processing industries. Source: GEMÜ

May 2025 Bürkert completed a new 6,000 m² Centre of Competence for Polymers at its Criesbach campus, consolidating materials analysis, toolmaking, and plastics production into one facility to strengthen manufacturing integration and accelerate product development.

June 2026 Bürkert launched new integration tools for Emerson DeltaV, simplifying valve commissioning and diagnostics while reducing engineering effort through seamless automation platform connectivity. The solution enables faster implementation across digital process facilities with improved lifecycle management. Source: Bürkert News

This report delivers a comprehensive assessment of the Angle Seat Valve Market by evaluating product types, applications, end-user industries, competitive positioning, technology evolution, and regional deployment patterns. The analysis covers Pneumatic, Electric, Stainless Steel, Brass, and High Pressure variants across Steam Systems, Water Treatment, Chemical Processing, Food Processing, and Pharmaceuticals, together with demand trends across Chemicals, Food & Beverage, Pharmaceuticals, Water Utilities, and Power Plants. More than 40% of industrial installations are concentrated in automated process environments, reflecting the increasing role of intelligent flow-control systems.

The report further examines market dynamics across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting manufacturing expansion, automation adoption, infrastructure modernization, and digital valve integration between 2026 and 2033. It provides strategic benchmarking of leading companies, emerging technology trends, deployment priorities, investment opportunities, supply-chain developments, and competitive positioning, enabling stakeholders to strengthen expansion strategies, product portfolios, operational planning, and long-term business decision-making across evolving industrial markets.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 2090 Million |

Market Revenue in 2033 | USD 3261.39 Million |

CAGR (2026 - 2033) | 5.72% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Bürkert Fluid Control Systems, GEMÜ Group, Emerson Electric Co., Spirax Sarco PLC, Parker Hannifin Corporation, IMI plc, Schubert & Salzer Control Systems GmbH, Festo SE & Co. KG, Christian Bürkert GmbH & Co. KG, Rotex Automation Limited, Bray International, Inc., AVK Holding A/S, Neles Corporation, KITZ Corporation |

Customization & Pricing | Available on Request (10% Customization is Free) |