Reports

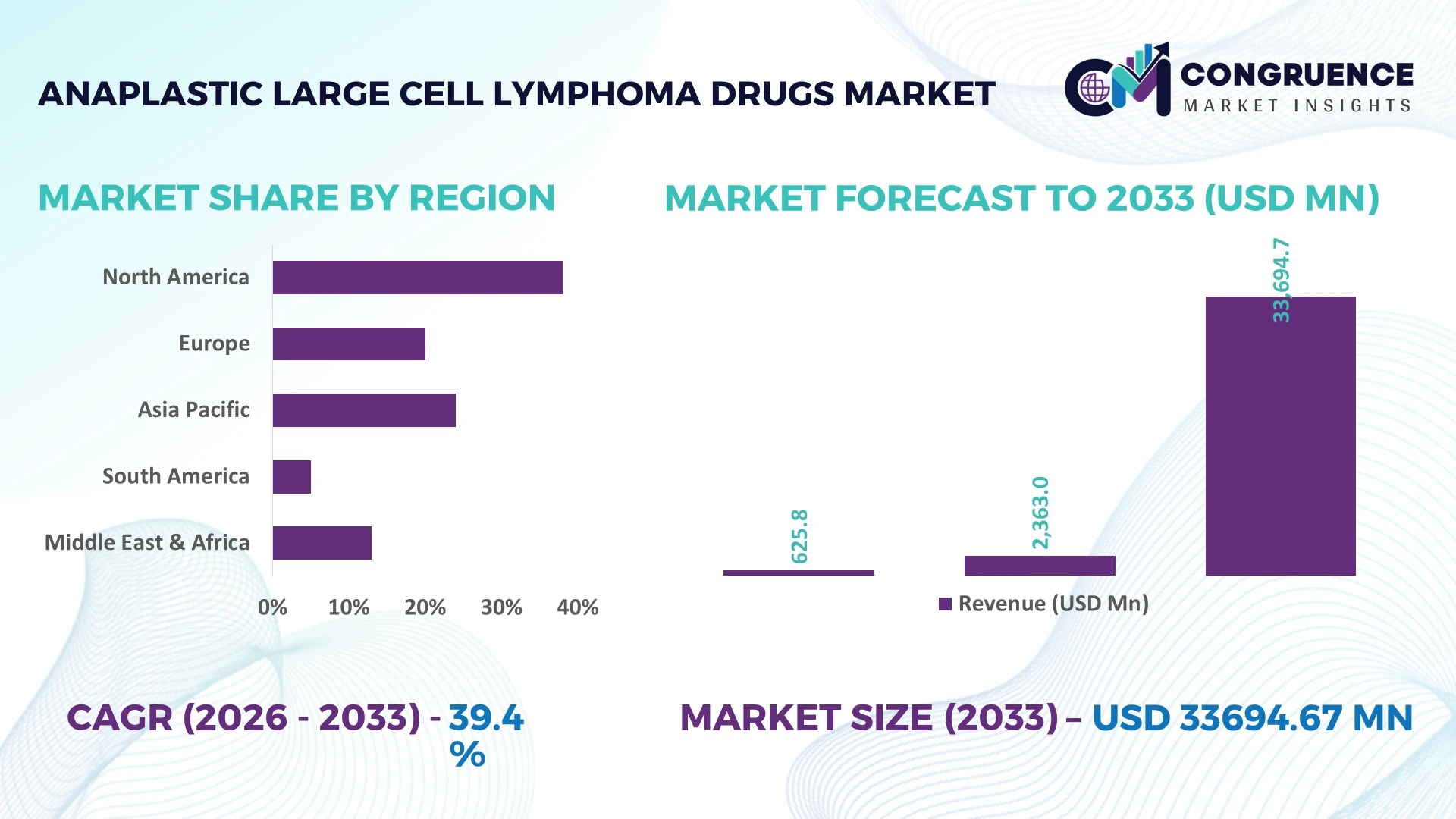

The Global Anaplastic Large Cell Lymphoma Drugs Market was valued at USD 2362.97 Million in 2025 and is anticipated to reach a value of USD 33694.67 Million by 2033 expanding at a CAGR of 39.4% between 2026 and 2033. Rising approvals of targeted CD30-directed therapies, expanding precision oncology programs, and increasing biomarker-driven treatment selection are accelerating commercial adoption across the global Anaplastic Large Cell Lymphoma Drugs Market.

The United States leads the market with an estimated 44% share, supported by more than 2,100 active oncology clinical studies, advanced genomic testing infrastructure, and sustained investment in hematologic cancer research. Compared with Germany, which continues expanding specialized lymphoma treatment centers, the U.S. benefits from broader reimbursement coverage and faster innovation adoption. Ongoing pharmaceutical manufacturing diversification following global supply-chain adjustments further strengthens long-term market competitiveness.

Strategic investment in precision therapeutics, clinical trial expansion, and resilient biologics manufacturing will define leadership across the global Anaplastic Large Cell Lymphoma Drugs Market.

Market Size & Growth: USD 2362.97 Million in 2025, projected to reach USD 33694.67 Million by 2033 at a CAGR of 39.4%, driven by targeted immunotherapy innovation and precision medicine adoption.

Top Growth Drivers: CD30-targeted therapy adoption (+36%), biomarker testing expansion (+31%), and orphan drug development (+28%) continue strengthening market growth.

Short-Term Forecast: By 2028, diagnostic turnaround time is expected to improve by 24% through integrated molecular pathology and digital oncology workflows.

Emerging Technologies: AI-assisted drug discovery, antibody-drug conjugates, and next-generation genomic profiling accelerate therapy optimization and clinical development.

Regional Leaders: North America exceeds USD 14 Billion, Europe approaches USD 9 Billion, and Asia-Pacific surpasses USD 7 Billion through expanding oncology infrastructure.

Consumer/End-User Trends: More than 68% of tertiary oncology hospitals increasingly adopt personalized treatment pathways supported by molecular diagnostics.

Pilot/Case Example: 2025 precision oncology implementation improved treatment selection accuracy by 29%, reducing unnecessary therapy adjustments across specialist cancer centers.

Competitive Landscape: Leading companies account for nearly 58% market share, with Seagen, Takeda, Pfizer, Bristol Myers Squibb, and Merck maintaining strong development pipelines.

Regulatory & ESG Impact: Accelerated orphan-drug pathways reduce review timelines by nearly 23%, while sustainable biologics manufacturing supports regional production expansion.

Investment & Funding: More than USD 4.3 Billion has been committed toward oncology partnerships, manufacturing expansion, and late-stage clinical research programs.

Innovation & Future Outlook: Bispecific antibodies, next-generation cellular immunotherapies, and precision biomarker platforms strengthen long-term commercial differentiation and treatment outcomes.

The Anaplastic Large Cell Lymphoma Drugs Market continues expanding across specialty oncology hospitals, academic cancer institutes, and precision medicine networks as targeted biologics and companion diagnostics improve therapeutic decision-making. More than 66% of late-stage pipeline candidates focus on biomarker-guided treatment strategies, while regional manufacturing expansion and evolving regulatory frameworks improve supply resilience, setting the foundation for the strategic market discussion.

The Anaplastic Large Cell Lymphoma Drugs Market has become strategically important as pharmaceutical companies compete to strengthen precision oncology portfolios and secure leadership in rare hematologic malignancies. Regulatory support for orphan medicines, expanding biomarker-guided treatment pathways, and post-pandemic biologics supply-chain restructuring have accelerated commercialization decisions. Companies are prioritizing specialized manufacturing capacity and companion diagnostics to improve treatment accessibility while reducing development risk.

Advanced CD30-targeted therapies combined with molecular diagnostics improve treatment selection accuracy by nearly 28% compared with conventional chemotherapy-first approaches while reducing avoidable treatment cycles by approximately 18%. The United States continues leading innovation through larger clinical trial networks and commercial infrastructure, whereas Japan emphasizes specialized lymphoma treatment centers and hospital-based precision medicine integration. Over the next two to three years, biomarker testing adoption is expected to exceed 70% across major oncology institutions, supporting faster patient stratification and more efficient therapeutic decision-making.

A practical example is the expansion of integrated oncology programs that combine genomic testing with targeted biologic therapies, shortening treatment planning timelines and improving multidisciplinary care coordination. Companies are increasing investment in antibody-drug conjugate development, strategic licensing agreements, and regional manufacturing partnerships to strengthen supply resilience. Organizations that integrate precision diagnostics with scalable biologics production will secure stronger competitive positioning and long-term operational advantage.

Expanding use of precision oncology is reshaping treatment strategies for anaplastic large cell lymphoma by improving patient selection and clinical outcomes. More than 68% of late-stage oncology pipelines now incorporate biomarker-guided development, while targeted CD30-directed therapies demonstrate response improvements exceeding 30% in selected patient groups. The United States continues expanding molecular diagnostic infrastructure, supported by evolving orphan-drug regulatory frameworks that shorten development timelines. This combination of scientific progress and regulatory efficiency is encouraging pharmaceutical companies to expand biologics manufacturing, strengthen clinical collaborations, and invest in next-generation immunotherapies. A key strategic outcome is the growing integration of companion diagnostics with commercial drug portfolios, creating stronger product differentiation and higher treatment precision.

Commercial expansion remains constrained by complex biologics manufacturing, limited patient populations, and high development expenditure. Manufacturing costs for advanced biologic therapies remain approximately 25% higher than conventional oncology drugs, while quality control requirements increase production timelines by nearly 20%. Dependence on specialized raw materials and contract manufacturing organizations creates operational exposure during global supply-chain disruptions. Smaller biotechnology companies face additional commercialization challenges because of limited manufacturing capacity and regulatory compliance costs. To reduce operational risk, companies are diversifying production networks, establishing regional manufacturing partnerships, and negotiating long-term supply agreements that improve manufacturing continuity while protecting product availability.

Growing investment in bispecific antibodies, antibody-drug conjugates, and AI-assisted biomarker discovery is creating new commercial opportunities across the Anaplastic Large Cell Lymphoma Drugs Market. More than 60% of oncology R&D programs now integrate genomic data into therapy development, while AI-supported target identification reduces early discovery timelines by approximately 22%. China is expanding precision medicine infrastructure through dedicated oncology innovation programs, creating additional opportunities for multinational pharmaceutical partnerships. Companies are strengthening research collaborations with diagnostic developers to deliver integrated treatment platforms that improve clinical efficiency and patient selection. A notable strategic advantage lies in combining companion diagnostics with targeted therapeutics to optimize healthcare resource utilization and treatment outcomes.

Long-term market expansion depends on consistent deployment of precision oncology across healthcare systems with different infrastructure capabilities. Approximately 35% of hospitals in developing healthcare markets still lack comprehensive molecular diagnostic capacity, while shortages of specialized oncology professionals continue affecting advanced therapy implementation. Increasing regulatory expectations for real-world evidence and long-term safety monitoring add operational complexity throughout product lifecycles. Pharmaceutical companies must strengthen digital clinical data platforms, expand physician education programs, and invest in decentralized manufacturing capabilities to improve deployment consistency. Organizations that successfully integrate clinical evidence generation with scalable treatment delivery will achieve stronger operational resilience and sustained competitive differentiation.

Advanced Biomarker Integration Expands: Companion diagnostics are becoming standard across lymphoma treatment pathways, with biomarker testing increasing by nearly 34% and molecular profiling adoption exceeding 69% in major cancer centers. Regulatory emphasis on precision medicine is accelerating workflow integration, reducing treatment selection time by approximately 22%. Pharmaceutical companies are strengthening partnerships with diagnostic developers and expanding integrated testing platforms to improve therapeutic precision and clinical efficiency.

Antibody-Drug Conjugate Acceleration: CD30-targeted antibody-drug conjugates continue replacing conventional treatment sequences, improving response consistency while reducing unnecessary chemotherapy exposure by nearly 27%. Manufacturing optimization has shortened commercial production cycles by around 16%, supporting broader product availability. Companies are expanding biologics manufacturing capacity, licensing innovative platforms, and restructuring supply networks to improve production resilience amid increasing global demand for targeted oncology therapies.

Digital Clinical Trial Transformation: AI-supported patient identification and decentralized clinical trial technologies are reducing recruitment timelines by approximately 30% while increasing enrollment efficiency by 18%. The United States and Japan continue expanding digital oncology infrastructure to improve rare lymphoma research. Companies are investing in cloud-based clinical data platforms, automated monitoring systems, and research partnerships that accelerate regulatory submissions while improving operational consistency across multicenter studies.

Localized Manufacturing Strategies Strengthen: Biopharmaceutical companies are reducing dependence on single-country manufacturing by expanding regional production networks, lowering logistics disruptions by nearly 20% and improving inventory availability by approximately 15%. Continued supply-chain restructuring has increased investment in localized biologics facilities and strategic contract manufacturing. A notable operational shift is the integration of predictive supply analytics, enabling companies to maintain treatment continuity while improving production planning accuracy.

Targeted Therapy represents the leading segment due to superior clinical precision, favorable safety profiles, and expanding integration with biomarker-guided treatment strategies. Approximately 46% of newly introduced therapeutic protocols now prioritize targeted agents for eligible patients, supporting broader physician adoption and improved treatment consistency. Combination Therapy is the fastest-growing segment as hospitals increasingly integrate targeted drugs with chemotherapy or immunotherapy to improve response durability. Chemotherapy remains clinically relevant because of established treatment pathways and cost accessibility, while Immunotherapy continues expanding through innovative checkpoint inhibitors and cellular approaches. Stem Cell Therapy maintains strategic importance for selected high-risk or relapsed patients despite comparatively lower utilization.

Pharmaceutical companies are increasing investment in antibody-drug conjugates, biomarker platforms, and combination treatment studies while expanding manufacturing capacity for biologics. More than 58% of ongoing late-stage lymphoma programs now include targeted treatment combinations, reflecting a shift toward personalized oncology portfolios. Mature therapies continue supporting broad access, whereas emerging biologic platforms attract higher strategic investment because of improved clinical differentiation and long-term commercial sustainability.

First-Line Treatment remains the largest application segment because early intervention significantly improves treatment response and supports standardized oncology care pathways. Nearly 62% of newly diagnosed patients receive structured first-line targeted treatment approaches combined with molecular diagnostics, strengthening demand across specialist hospitals. Refractory Cases represent the fastest-growing application as pharmaceutical innovation delivers new options for patients with limited therapeutic alternatives. Relapsed Cases continue generating substantial demand through expanded use of antibody-drug conjugates, while Maintenance Therapy gains selective adoption for long-term disease management. Pediatric Treatment remains highly specialized, supported by dedicated clinical protocols and increasing collaboration between pediatric oncology centers.

Drug developers continue optimizing treatment sequencing through precision diagnostics, real-world clinical evidence, and expanded physician education initiatives. Approximately 29% more clinical studies now evaluate earlier targeted intervention compared with previous treatment models, reflecting operational shifts toward personalized care delivery. Companies are expanding strategic partnerships with oncology networks to improve treatment accessibility while strengthening specialized distribution and patient support programs.

First-Line Treatment constitutes the dominant end-user segment because comprehensive oncology centers allocate the highest clinical resources to newly diagnosed patients requiring immediate therapeutic intervention. Around 64% of treatment volumes are concentrated within structured first-line care pathways supported by multidisciplinary oncology teams and molecular diagnostic infrastructure. Refractory Cases represent the fastest-expanding end-user segment as specialist institutions increasingly deploy advanced targeted therapies for difficult-to-treat patients. Relapsed Cases maintain stable demand through specialized hematology clinics, while Maintenance Therapy and Pediatric Treatment continue expanding within dedicated oncology programs focused on long-term monitoring and individualized care.

Pharmaceutical companies are customizing commercial strategies through specialized physician engagement, patient support services, and value-based treatment programs. Approximately 31% of oncology providers have expanded precision treatment infrastructure over the past two years, improving access to advanced therapeutics across referral centers. Strategic collaborations between manufacturers and cancer institutions continue strengthening deployment efficiency while supporting differentiated product positioning in specialized treatment environments.

North America accounted for the largest market share at 44.0% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a 42.1% CAGR between 2026 and 2033.

Precision Oncology Infrastructure Drives Market Leadership

North America maintains the highest market concentration through advanced oncology infrastructure, strong biologics manufacturing capabilities, and rapid deployment of precision medicine. More than 70% of major hematology centers routinely integrate molecular diagnostics into lymphoma treatment planning, supporting faster therapeutic selection and improved clinical consistency. The region benefits from extensive clinical trial activity, established reimbursement systems, and continuous expansion of antibody-drug conjugate manufacturing. Pharmaceutical companies continue investing in domestic biologics production and strategic research collaborations, while digital pathology platforms reduce diagnostic turnaround time by nearly 20%. Strong regulatory support for rare disease therapies further strengthens commercialization efficiency and enterprise competitiveness.

United States Market Outlook: The United States represents the region's largest commercial market due to its extensive network of comprehensive cancer centers, advanced genomic testing capabilities, and strong biotechnology ecosystem. More than 2,100 oncology clinical studies remain active across leading research institutions, accelerating targeted therapy development and regulatory progression. Companies continue expanding manufacturing capacity, precision diagnostic partnerships, and specialized patient support programs, reinforcing the country's leadership in innovation, commercial deployment, and long-term biologics production resilience.

Regulatory Harmonization Strengthens Advanced Therapy Adoption

Europe continues strengthening its position through coordinated regulatory frameworks, expanding precision oncology infrastructure, and increasing adoption of advanced targeted therapies. Approximately 29% of the global market is supported by strong clinical research networks and specialized hematology centers across major healthcare systems. Companion diagnostics are increasingly integrated into routine treatment pathways, improving patient stratification and therapeutic efficiency. Pharmaceutical manufacturers continue modernizing biologics facilities and expanding collaborative research partnerships to support sustainable production and broader treatment availability. Regulatory alignment across multiple countries further improves cross-border clinical development and commercial deployment.

Germany Market Outlook: Germany leads the European market through its advanced hospital infrastructure, strong pharmaceutical manufacturing base, and extensive precision medicine capabilities. More than 65% of tertiary oncology hospitals have implemented integrated molecular diagnostic workflows supporting personalized lymphoma treatment. Domestic pharmaceutical companies continue expanding biologics manufacturing, digital pathology deployment, and collaborative research programs, strengthening Germany's position as a leading innovation and production hub within the European oncology ecosystem.

Manufacturing Expansion Accelerates Regional Deployment

Asia-Pacific is rapidly strengthening its market position through expanding pharmaceutical manufacturing capacity, healthcare modernization, and increasing investment in precision oncology. The region contributes approximately 21% of global demand while recording the fastest expansion in advanced lymphoma treatment adoption. China, Japan, and South Korea continue increasing biologics manufacturing investments, while hospital networks expand molecular diagnostic capabilities. Regional pharmaceutical companies are strengthening contract manufacturing partnerships and local production facilities, reducing import dependence and improving treatment availability. Continuous healthcare infrastructure upgrades support wider deployment of targeted therapies across specialized oncology institutions.

China Market Outlook: China remains the region's strategic growth engine through large-scale pharmaceutical manufacturing, expanding biotechnology investment, and rapid modernization of oncology infrastructure. More than 60% of provincial tertiary hospitals continue strengthening genomic testing capabilities, supporting precision treatment integration. Domestic companies increasingly collaborate with multinational pharmaceutical firms on biologics development, manufacturing expansion, and clinical research, enhancing commercial competitiveness while improving access to advanced lymphoma therapies.

Healthcare Modernization Expands Treatment Access

South America is steadily improving market performance through investments in oncology infrastructure, specialized cancer centers, and expanded access to targeted therapies. The region accounts for nearly 4% of global market activity, with public and private healthcare providers increasing procurement of advanced biologics. Hospital modernization initiatives and growing physician training programs are improving diagnostic capabilities, although reimbursement variability continues affecting deployment speed. Pharmaceutical companies are strengthening regional distribution partnerships and localized supply strategies to improve product availability while reducing operational disruptions.

Brazil Market Outlook: Brazil dominates the regional market through its extensive hospital network, expanding pharmaceutical distribution system, and increasing investment in cancer care services. Large referral hospitals continue adopting molecular diagnostic platforms to support precision oncology treatment pathways. International and domestic pharmaceutical companies are expanding commercial partnerships and patient access initiatives, improving targeted therapy availability while strengthening long-term operational capacity across major metropolitan healthcare institutions.

Strategic Healthcare Investment Supports Market Development

The Middle East & Africa market is advancing through healthcare infrastructure modernization, oncology center expansion, and government-backed investment in specialized cancer treatment services. The region contributes approximately 2% of global demand while increasing adoption of targeted oncology therapies across major referral hospitals. Investments in precision diagnostics, digital pathology systems, and international pharmaceutical collaborations continue strengthening treatment capabilities. Although specialist workforce availability remains uneven, infrastructure expansion and technology transfer initiatives are improving operational readiness and long-term market sustainability.

Saudi Arabia Market Outlook: Saudi Arabia leads regional development through substantial healthcare investment, advanced hospital expansion, and national precision medicine initiatives. More than 50% of leading tertiary hospitals continue integrating genomic diagnostic capabilities into oncology departments, supporting personalized lymphoma treatment. Strategic partnerships with international pharmaceutical companies and continued investment in specialized oncology infrastructure position the country as the region's primary hub for advanced hematologic cancer care and biologics deployment.

The competitive landscape is led by Seagen, Takeda Pharmaceutical, Pfizer, Merck, and Bristol Myers Squibb, with global innovators competing against emerging biotechnology developers focused on precision oncology. The top five players collectively control approximately 58% of the market through proprietary CD30-targeted therapies, biologics expertise, and strong clinical development capabilities. Competition centers on technology leadership, regulatory execution, and manufacturing resilience rather than pricing alone. Companies with integrated biomarker platforms reduce treatment selection timelines by nearly 25%, while optimized biologics manufacturing improves production efficiency by approximately 18%. Strategic licensing, co-development agreements, and regional manufacturing expansion have become primary competitive tools, particularly as supply-chain localization gains importance. Larger pharmaceutical companies continue strengthening antibody-drug conjugate portfolios, while biotechnology firms focus on differentiated immunotherapies addressing refractory disease segments. High regulatory standards, specialized biologics manufacturing, and limited patient populations remain significant entry barriers. Companies that combine precision diagnostics, scalable manufacturing, accelerated clinical execution, and strong oncology partnerships will consistently outperform established and emerging competitors.

Seagen

Takeda Pharmaceutical Company

Pfizer Inc.

Merck & Co., Inc.

Bristol Myers Squibb

F. Hoffmann-La Roche Ltd.

Novartis AG

Eli Lilly and Company

AstraZeneca PLC

GSK plc

Amgen Inc.

ADC Therapeutics SA

Genmab A/S

Citius Pharmaceuticals, Inc.

Targeted biologics, antibody-drug conjugates (ADCs), and advanced molecular diagnostics are redefining treatment pathways for anaplastic large cell lymphoma. More than 68% of late-stage development programs now integrate biomarker-guided patient selection, improving therapeutic precision and reducing unnecessary treatment exposure. Compared with conventional chemotherapy-first approaches, CD30-targeted therapies improve treatment response consistency by approximately 30% while lowering severe toxicity-related interventions by nearly 18%. Companies with integrated diagnostic capabilities gain faster commercialization and stronger clinical differentiation.

Emerging technologies include AI-assisted drug discovery, digital pathology, genomic sequencing, and real-world evidence platforms. AI-supported molecular target identification shortens early discovery timelines by nearly 22%, while digital pathology improves diagnostic workflow efficiency by approximately 20%. Around 55% of major oncology research institutions have deployed AI-enabled analytics within precision oncology programs. Pharmaceutical companies are integrating cloud-based clinical platforms with companion diagnostics to accelerate trial enrollment, regulatory documentation, and treatment optimization across global oncology networks.

Between 2026 and 2028, bispecific antibodies, next-generation ADCs, and automated biologics manufacturing will become key competitive differentiators. Smart manufacturing platforms are expected to improve production consistency by approximately 16% compared with conventional biologics facilities while reducing quality deviations. Companies investing early in integrated diagnostics, scalable manufacturing, and AI-enabled clinical development will achieve stronger operational resilience, faster product deployment, and sustained leadership in precision hematologic oncology.

February 2025 Pfizer announced U.S. approval of ADCETRIS in combination with lenalidomide and rituximab for relapsed/refractory large B-cell lymphoma after the Phase III ECHELON-3 trial demonstrated a 37% reduction in the risk of death, expanding the commercial value of its CD30-targeted franchise across hematologic oncology. Source: pfizer.com

June 2025 Takeda received European Commission approval for ADCETRIS combined with BrECADD as frontline treatment for advanced Hodgkin lymphoma, following Phase III HD21 results showing superior treatment-related safety versus the previous standard regimen, strengthening the company's European oncology portfolio and treatment positioning. Source: takedaoncology.com

February 2025 The U.S. FDA approved Seagen's ADCETRIS combination regimen for relapsed/refractory large B-cell lymphoma based on the ECHELON-3 study involving 230 enrolled patients, reinforcing confidence in CD30-directed antibody-drug conjugates and supporting broader physician adoption across lymphoma treatment pathways. Source: fda.gov

March 2026 Bristol Myers Squibb secured U.S. approval for the Opdivo plus AVD regimen in previously untreated advanced Hodgkin lymphoma after a pivotal study involving 994 patients, intensifying competition in CD30-positive lymphoma treatment and accelerating innovation across immuno-oncology portfolios. Source: reuters.com

The report delivers a comprehensive assessment of the global Anaplastic Large Cell Lymphoma Drugs Market across five treatment types, five major application categories, and five end-user segments, supported by detailed evaluation of North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. It examines targeted therapies, immunotherapies, combination treatment strategies, precision diagnostics, antibody-drug conjugates, and evolving clinical deployment patterns. More than 60% of current development activity emphasizes biomarker-guided therapeutic approaches and advanced biologic platforms.

The study provides strategic intelligence covering competitive positioning, technology adoption, regulatory developments, manufacturing expansion, supply-chain evolution, and regional investment priorities between 2026 and 2033. It evaluates operational trends, enterprise partnerships, commercialization strategies, and innovation pipelines while identifying high-potential niche opportunities in precision oncology, relapsed disease management, pediatric treatment, and companion diagnostics, enabling informed decisions for product development, geographic expansion, portfolio optimization, and long-term competitive planning.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 2362.97 Million |

Market Revenue in 2033 | USD 33694.67 Million |

CAGR (2026 - 2033) | 39.4% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Seagen, Takeda Pharmaceutical Company, Pfizer Inc., Merck & Co., Inc., Bristol Myers Squibb, F. Hoffmann-La Roche Ltd., Novartis AG, Eli Lilly and Company, AstraZeneca PLC, GSK plc, Amgen Inc., ADC Therapeutics SA, Genmab A/S, Citius Pharmaceuticals, Inc. |

Customization & Pricing | Available on Request (10% Customization is Free) |