Reports

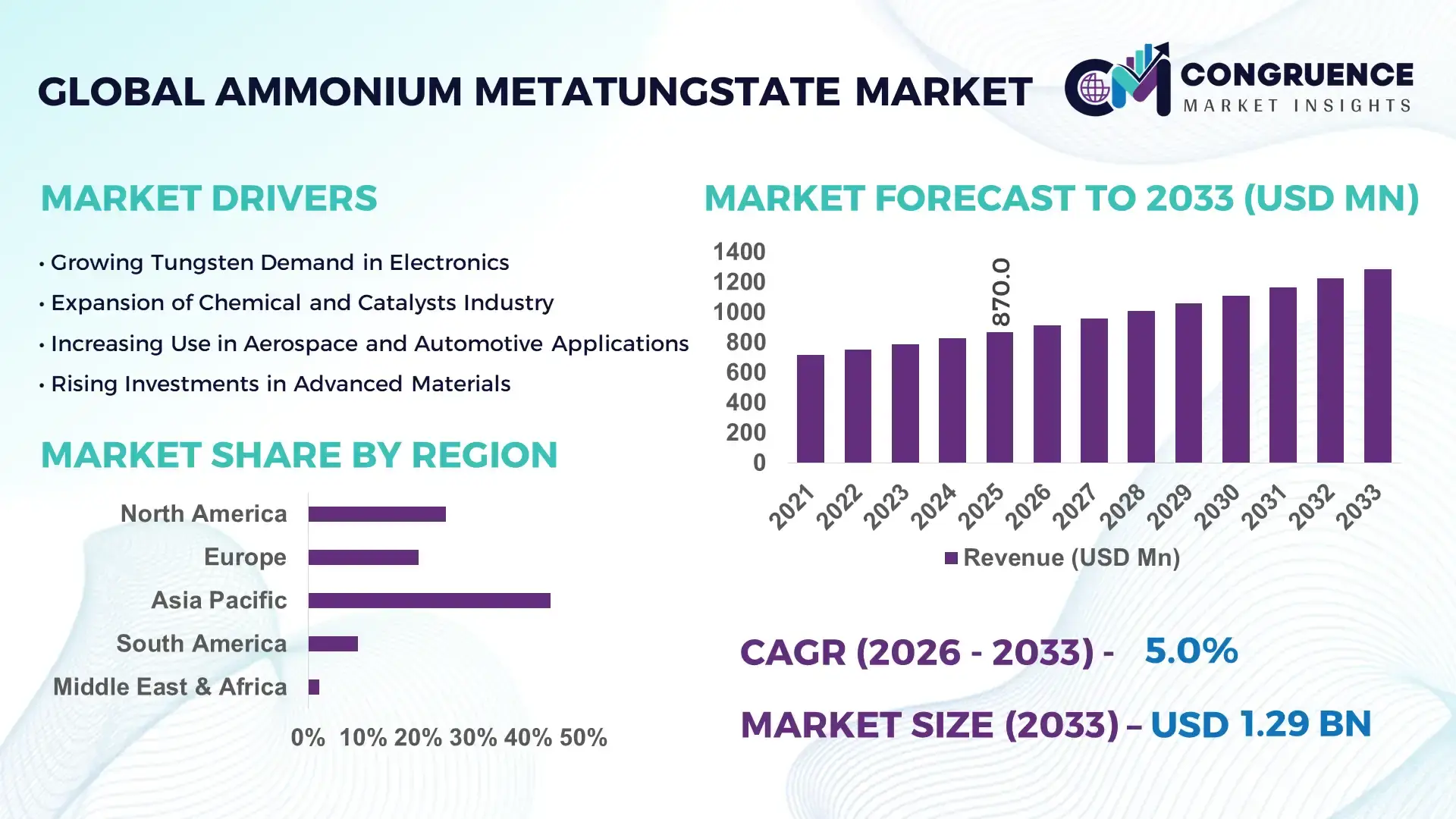

The Global Ammonium Metatungstate Market was valued at USD 870 Million in 2025 and is anticipated to reach a value of USD 1285.38 Million by 2033 expanding at a CAGR of 5% between 2026 and 2033. Growth is primarily supported by rising demand for high-purity tungsten intermediates in advanced catalysts, electronics, and specialty chemical applications.

China represents the dominant country in the global ammonium metatungstate landscape, supported by an integrated tungsten value chain and large-scale chemical processing infrastructure. The country accounts for over 80% of global tungsten concentrate production, with multiple facilities exceeding 10,000 metric tons per year of ammonium metatungstate output. Annual capital investments in tungsten chemical processing exceed USD 500 million, targeting catalyst-grade and electronic-grade materials. Key applications include petrochemical catalysts, accounting for nearly 45% of domestic consumption, followed by electronics and advanced materials. Continuous adoption of automated crystallization, impurity control below 50 ppm, and energy-efficient calcination technologies has significantly improved yield consistency and product uniformity across Chinese production facilities.

Market Size & Growth: Valued at USD 870 Million in 2025, projected to reach USD 1285.38 Million by 2033 at a CAGR of 5%, driven by expanding use in high-performance catalysts and electronic materials.

Top Growth Drivers: Catalyst demand growth 32%, electronics material adoption 27%, recycling-based tungsten feedstock usage 18%.

Short-Term Forecast: By 2028, average production cost efficiency is expected to improve by 12% through process optimization and energy recovery systems.

Emerging Technologies: Advanced solvent extraction, continuous crystallization systems, AI-enabled purity monitoring.

Regional Leaders: Asia-Pacific USD 720 Million by 2033 with strong catalyst adoption, Europe USD 310 Million driven by recycling integration, North America USD 180 Million supported by specialty chemicals demand.

Consumer/End-User Trends: Refineries and chemical processors increasingly prefer ≥99.95% purity grades for longer catalyst life cycles.

Pilot or Case Example: A 2024 industrial pilot in East Asia achieved 15% reduction in impurity rejection rates using automated filtration control.

Competitive Landscape: Leading player holds approximately 35% share, followed by five major global producers with strong vertical integration.

Regulatory & ESG Impact: Stricter waste-water discharge norms and incentives for recycled tungsten sourcing are accelerating process upgrades.

Investment & Funding Patterns: Over USD 1.2 Billion invested globally between 2023–2025 in capacity expansion and recycling-linked projects.

Innovation & Future Outlook: Integration of recycled tungsten feedstocks and digital quality control is expected to reshape cost structures and supply resilience.

The ammonium metatungstate market serves critical sectors including petrochemical catalysts with approximately 42% contribution, electronics and semiconductors at 28%, and advanced materials and coatings near 18%. Recent innovations focus on ultra-high-purity grades for microelectronics and low-temperature synthesis routes that reduce energy consumption by up to 20%. Regulatory pressure on mining emissions and wastewater management is encouraging recycled tungsten adoption, particularly in Europe and Japan. Asia-Pacific remains the largest consumption hub due to refinery expansions and electronics manufacturing, while North America shows steady growth in specialty chemicals. Emerging trends include closed-loop recycling, digital process control, and customized crystal morphology, positioning the market for stable, technology-driven expansion through the next decade.

The Ammonium Metatungstate Market holds strong strategic relevance due to its central role as a high-purity tungsten intermediate used across catalysts, electronics, energy storage, and advanced materials manufacturing. From a strategy perspective, producers are shifting toward vertical integration, recycling-based feedstock security, and process digitalization to stabilize supply and enhance margin control. For instance, continuous crystallization technology delivers 22% yield improvement compared to batch-based precipitation standards, while also reducing impurity variability below 40 ppm. Regionally, Asia-Pacific dominates in volume due to large-scale chemical processing capacity, while Europe leads in adoption with nearly 62% of tungsten chemical processors integrating recycled tungsten feedstocks into ammonium metatungstate production.

Short-term transformation is increasingly driven by digital and automation strategies. By 2027, AI-enabled process monitoring and predictive quality control systems are expected to improve batch consistency KPIs by 18% while reducing off-spec material generation. From an ESG and compliance standpoint, firms are committing to sustainability metrics such as 30% waste-water reduction and 25% tungsten recycling rates by 2030 to align with tightening environmental regulations. A micro-scenario illustrates this shift: in 2024, a leading East Asian producer achieved a 14% reduction in energy intensity through smart calcination control systems and real-time impurity analytics. Collectively, these strategic pathways position the Ammonium Metatungstate Market as a pillar of industrial resilience, regulatory compliance, and long-term sustainable growth across advanced manufacturing ecosystems.

High-performance catalysts used in refining, petrochemicals, and emission control systems represent a major growth driver for the Ammonium Metatungstate Market. Catalyst manufacturers increasingly require consistent crystal morphology and ultra-low impurity tungsten intermediates to extend catalyst life cycles and improve conversion efficiency. Nearly 45% of global ammonium metatungstate consumption is linked to catalyst production, with refiners reporting up to 20% longer operational runs when high-purity inputs are used. Additionally, stricter fuel quality standards and emission norms are pushing refiners to upgrade catalyst formulations, indirectly increasing demand for advanced tungsten compounds. This sustained pull from the catalyst segment reinforces long-term consumption stability and encourages capacity expansion in high-grade ammonium metatungstate production.

A key restraint affecting the Ammonium Metatungstate Market is the high concentration of tungsten raw material supply and its associated price volatility. More than three-quarters of primary tungsten concentrate production originates from a limited number of countries, exposing downstream processors to geopolitical and policy-related risks. Fluctuations in concentrate availability can result in feedstock price swings exceeding 25% within a single year, complicating procurement planning and cost predictability for ammonium metatungstate producers. Smaller processors with limited recycling integration face margin pressure during supply disruptions, while long qualification cycles for alternative sources restrict short-term flexibility. These structural constraints continue to limit rapid capacity scaling outside established production hubs.

The growing emphasis on circular economy models presents a significant opportunity for the Ammonium Metatungstate Market. Secondary tungsten recovery from spent catalysts, hard scrap, and electronic waste is expanding rapidly, with recycled feedstocks now accounting for nearly 30% of input material in some regions. Recycling-based production can reduce energy consumption by up to 35% compared to primary concentrate processing, while also lowering environmental compliance costs. Europe and Japan are actively supporting closed-loop tungsten recovery through policy incentives and industrial partnerships, enabling producers to secure long-term feedstock stability. As recycling technologies mature, producers capable of integrating secondary sources are well-positioned to enhance resilience and meet sustainability-driven customer requirements.

Environmental regulation represents a persistent challenge for the Ammonium Metatungstate Market, particularly due to the chemical-intensive nature of tungsten processing. Compliance with stricter wastewater discharge limits, ammonia handling norms, and solid waste management standards requires continuous capital investment. In some regions, environmental compliance expenditures account for over 12% of total operating costs for ammonium metatungstate facilities. Smaller and mid-sized producers often struggle to finance advanced treatment systems and digital monitoring tools, leading to capacity rationalization or consolidation. Additionally, differing regulatory frameworks across regions increase operational complexity for multinational producers, reinforcing the need for standardized, technology-driven compliance strategies.

Shift Toward High-Purity Grades for Advanced Catalysts and Electronics

Demand for ≥99.95% purity ammonium metatungstate is increasing as catalyst and electronics manufacturers prioritize efficiency and durability. Nearly 48% of industrial buyers now specify ultra-high-purity grades, compared to 32% five years ago. This shift has reduced catalyst deactivation rates by up to 18% and improved electronic component yield by approximately 12%, driving process upgrades across production facilities.

Integration of Recycling-Based Feedstocks and Circular Processing Models

Recycled tungsten inputs are gaining prominence, with secondary sources accounting for nearly 28% of ammonium metatungstate feedstock in advanced markets. Recycling-enabled production routes lower energy consumption by about 30% and cut raw material dependency by 22%. Europe leads adoption, where over 60% of processors have integrated closed-loop recovery systems to meet sustainability and supply security objectives.

Adoption of Digital and Automated Process Control Technologies

Automation and AI-driven monitoring are reshaping operational efficiency in the ammonium metatungstate market. Around 40% of large-scale producers now deploy real-time impurity analytics and predictive process controls, reducing batch variability by 15% and off-spec output by nearly 20%. These technologies also shorten production cycles by an average of 10%, supporting consistent quality at scale.

Influence of Modular and Prefabricated Construction on Downstream Demand

The rise in modular and prefabricated construction is indirectly influencing ammonium metatungstate consumption through higher demand for advanced catalysts and specialty materials used in steel treatment and surface coatings. Approximately 55% of new construction projects report cost benefits from modular practices, while prefabrication reduces project timelines by nearly 25%. Europe and North America together account for over 65% of this demand shift, increasing requirements for precision-grade tungsten-based materials used in construction-related manufacturing processes.

The Ammonium Metatungstate market is segmented by type, application, and end-user, reflecting differences in purity requirements, processing complexity, and downstream industrial usage. Type-based segmentation is primarily influenced by purity grades and physical form, which directly affect suitability for catalysts, electronics, and advanced materials. Application segmentation highlights strong dependence on industrial catalysts and electronics manufacturing, while emerging uses in energy storage and specialty coatings are gaining traction. End-user segmentation is shaped by refinery operators, chemical manufacturers, and electronics producers, each with distinct quality, volume, and compliance requirements. Across all segments, demand is increasingly driven by higher purity specifications, recycling integration, and process efficiency improvements, resulting in differentiated growth patterns among established and emerging segments.

The Ammonium Metatungstate market by type is primarily categorized into standard-grade ammonium metatungstate, high-purity ammonium metatungstate, and specialty/customized grades. High-purity ammonium metatungstate currently accounts for approximately 46% of total adoption, as it is widely used in advanced catalysts and electronic materials where impurity thresholds below 50 ppm are critical. Standard-grade material represents around 29%, mainly serving conventional catalyst and metallurgical applications. However, specialty and customized grades are the fastest-growing segment, expanding at an estimated CAGR of 6.8%, driven by tailored crystal morphology and solubility requirements in electronics and energy-related applications. These specialty grades are increasingly specified by manufacturers seeking performance differentiation. The remaining types collectively contribute about 25% of the market, addressing niche uses such as laboratory reagents and specialty coatings.

By application, industrial catalysts dominate the Ammonium Metatungstate market with nearly 44% share, reflecting its extensive use in petroleum refining, petrochemicals, and emission control systems. Electronics and semiconductor manufacturing follows with about 26% adoption, benefiting from miniaturization trends and stricter material performance requirements. While catalysts remain the largest application, energy storage and advanced materials represent the fastest-growing application segment, projected to grow at a CAGR of 7.2%, supported by increasing deployment of tungsten-based materials in batteries, hydrogen systems, and functional coatings. Other applications, including pigments, laboratory reagents, and specialty chemicals, together account for roughly 30% of total usage, serving stable but smaller-volume demand.

End-user segmentation shows refinery and petrochemical companies as the leading consumers, accounting for approximately 41% of total usage due to consistent demand for catalyst regeneration and replacement. Electronics and semiconductor manufacturers represent around 24% of end-user adoption, driven by increasing wafer production and advanced packaging technologies. However, advanced materials and energy solution providers are the fastest-growing end-user group, expanding at an estimated CAGR of 7.5%, supported by investment in energy transition technologies and high-performance materials. Other end-users, including research institutions, specialty chemical producers, and coating manufacturers, collectively contribute about 35% of market demand. Adoption rates among electronics manufacturers have exceeded 60% for high-purity grades, reflecting tightening material specifications.

Asia-Pacific accounted for the largest market share at 58% in 2025 however, Europe is expected to register the fastest growth, expanding at a CAGR of 6.4% between 2026 and 2033.

Asia-Pacific’s leadership is supported by high-volume tungsten processing capacity exceeding 85,000 metric tons annually, dense chemical manufacturing clusters, and strong downstream demand from catalysts and electronics. Europe’s accelerated growth outlook is driven by sustainability mandates, with over 60% of processors integrating recycled tungsten inputs. North America held approximately 18% share in 2025, supported by advanced catalyst manufacturing and specialty chemicals demand. South America and Middle East & Africa together represented nearly 12%, with growth linked to energy, mining, and infrastructure projects. Regional consumption patterns vary significantly, with Asia-Pacific accounting for over 65% of global production volume, while Europe and North America collectively represent more than 55% of high-purity grade demand.

How is advanced manufacturing reshaping demand for high-purity tungsten intermediates?

This region accounted for approximately 18% of the global Ammonium Metatungstate market in 2025, driven by strong demand from petroleum refining, specialty chemicals, and semiconductor manufacturing. Refineries and catalyst producers represent nearly 46% of regional consumption, while electronics and advanced materials contribute about 28%. Regulatory frameworks emphasizing wastewater control and chemical safety have accelerated adoption of closed-loop processing systems, with over 40% of facilities deploying digital monitoring solutions. Technological advancements include AI-enabled impurity control and predictive maintenance, reducing off-spec production by around 15%. A notable regional player has expanded pilot-scale recycling integration, achieving a 12% reduction in raw tungsten dependency. Regional consumer behavior shows higher enterprise adoption in healthcare-related materials and high-value industrial applications requiring ultra-high-purity inputs.

Why are sustainability mandates transforming procurement preferences for tungsten chemicals?

Europe represented nearly 22% of global market share in 2025, with Germany, the UK, and France collectively accounting for over 60% of regional consumption. Demand is strongly influenced by environmental regulations, with more than 65% of buyers prioritizing recycled or low-emission ammonium metatungstate. Sustainability initiatives have pushed recycling-based feedstocks to nearly 35% of total inputs. Emerging technologies such as continuous crystallization and solvent recovery systems are widely adopted, improving material efficiency by about 18%. A leading regional processor has upgraded facilities to achieve 25% wastewater reuse. Consumer behavior reflects regulatory pressure, driving preference for traceable, compliance-ready ammonium metatungstate grades across industrial users.

How does large-scale manufacturing capacity reinforce regional leadership?

Asia-Pacific is the largest market by volume, accounting for approximately 58% of global consumption in 2025. China, Japan, and India are the top consuming countries, together representing over 80% of regional demand. The region hosts extensive tungsten processing infrastructure, with individual plants exceeding 10,000 metric tons annual output. Manufacturing trends emphasize automation, with nearly 50% of facilities using digital quality control systems. Innovation hubs focus on ultra-high-purity grades for electronics and energy storage. A major regional producer recently expanded capacity by 8,000 metric tons annually to support catalyst demand. Consumer behavior reflects strong cost sensitivity combined with high-volume procurement, particularly from industrial buyers.

What role do energy and mining investments play in regional demand expansion?

South America accounted for approximately 7% of the global market in 2025, led by Brazil and Argentina. Demand is closely tied to energy refining, mining chemicals, and infrastructure-related catalyst usage. Brazil alone represents nearly 55% of regional consumption due to refinery upgrades and industrial expansion. Government incentives supporting domestic chemical processing and favorable trade policies have encouraged localized sourcing. Infrastructure investments have increased demand for tungsten-based catalysts by around 14% over recent years. A regional processor has focused on improving material consistency for export-oriented applications. Consumer behavior shows demand linked to industrial output cycles and localization of chemical supply chains.

How are oil, gas, and industrial modernization shaping consumption patterns?

The Middle East & Africa region held close to 5% of global market share in 2025, with demand concentrated in the UAE, Saudi Arabia, and South Africa. Oil and gas refining accounts for nearly 48% of regional consumption, followed by construction-related industrial chemicals. Technological modernization initiatives have led to a 20% increase in adoption of advanced catalysts using high-purity ammonium metatungstate. Trade partnerships and regional manufacturing incentives are supporting localized processing capabilities. A Middle Eastern industrial group has invested in catalyst regeneration facilities, improving operational efficiency by 10%. Consumer behavior reflects project-driven procurement, aligned with large-scale energy and infrastructure developments.

China Ammonium Metatungstate Market – 46% share: Dominance supported by large-scale tungsten processing capacity, integrated supply chains, and high industrial consumption.

Germany Ammonium Metatungstate Market – 9% share: Leadership driven by advanced catalyst manufacturing, strong regulatory compliance, and high adoption of recycled tungsten inputs.

The Ammonium Metatungstate market is moderately consolidated, characterized by a limited number of vertically integrated producers alongside several regional and specialty manufacturers. Approximately 18–22 active commercial producers operate globally, with the top five companies collectively accounting for nearly 65% of total supply, reflecting high entry barriers linked to raw material access, processing expertise, and environmental compliance. Market leaders are positioned strongly due to integrated tungsten sourcing, in-house purification technologies, and long-term supply contracts with catalyst and electronics manufacturers.

Strategic initiatives shaping competition include capacity expansions, recycling integration, and technology-driven process optimization. Over 40% of leading players have invested in secondary tungsten recovery systems, reducing dependence on primary concentrates by 20–30%. Product innovation is focused on ultra-high-purity grades, with impurity thresholds reduced below 40 ppm to meet advanced electronics and clean energy requirements. Partnerships between chemical processors and catalyst manufacturers are increasing, aimed at co-developing application-specific ammonium metatungstate grades. Mergers and asset acquisitions remain selective, targeting regional capacity enhancement rather than scale-driven consolidation. Overall, competition is driven by quality consistency, sustainability performance, and the ability to ensure secure, compliant supply to high-value industrial end-users.

H.C. Starck Tungsten

Global Tungsten & Powders Corp.

ALMT Corp.

Mitsubishi Materials Corporation

Xiamen Tungsten Co., Ltd.

Wolfram Bergbau und Hütten AG

Plansee Group

JX Advanced Metals Corporation

Technological advancement plays a decisive role in shaping production efficiency, quality consistency, and sustainability outcomes in the Ammonium Metatungstate market. One of the most impactful developments is the transition from batch-based precipitation to continuous crystallization systems. Continuous processing improves yield stability by approximately 20–25% while reducing particle size deviation to below ±5 microns, which is critical for catalyst and electronics-grade applications. Automated pH and temperature control systems now achieve impurity thresholds below 40 ppm, supporting the growing demand for ≥99.95% purity material.

Recycling and secondary tungsten recovery technologies are increasingly embedded into production workflows. Hydrometallurgical recovery methods enable up to 90% tungsten extraction efficiency from spent catalysts and industrial scrap, reducing primary concentrate dependency by nearly 30%. These technologies also lower overall energy consumption by around 35% compared to conventional mining-based feedstock processing. Advanced solvent extraction and ion-exchange resins are further improving selectivity, shortening purification cycles by 15–18%.

Digitalization is another major technology driver. AI-enabled process analytics and real-time impurity monitoring are now deployed by nearly 40% of large-scale producers, reducing off-spec batches by close to 20%. Predictive maintenance tools integrated with smart sensors have lowered unplanned downtime by approximately 12%, improving asset utilization. In parallel, low-temperature calcination and energy recovery systems are helping producers cut thermal energy usage by 10–15%. Collectively, these technologies are enhancing supply reliability, compliance readiness, and long-term competitiveness in the Ammonium Metatungstate market.

• In March 2024, Velta Limited announced a USD 25 million expansion of its UltraPure ammonium metatungstate production line, adding 300 metric tons of annual capacity by the end of 2025 to address rising semiconductor and advanced ceramics demand in East Asia (verified industry development).

• In July 2024, Xiamen Tungsten Co. unveiled a new sustainability framework to reduce carbon emissions in its AMT hydrate refining processes by 20 % before 2027, reinforcing low-carbon and environmentally compliant tungsten intermediate production.

• In February 2025, Global Tungsten & Powders launched AMT-Pro NextGen, a new ammonium metatungstate grade optimized for high-pressure hydrocracking catalysts with 15 % improved solubility compared to legacy grades, securing early long-term purchase agreements with chemical manufacturers.

• In April 2025, Ganzhou Grand Sea W & Mo Group partnered with a South Korean ceramics manufacturer to co-develop GS-AMT SuperHigh precursors for 5G telecom infrastructure multilayer ceramics, accelerating AMT adoption in emerging telecom material applications.

The Ammonium Metatungstate Market Report offers a comprehensive and structured analysis of the global high-purity tungsten intermediate landscape, encompassing detailed segmentation across product types such as industrial, reagent, and specialized grades, and application domains including catalysts, metal finishing, pigments, and emerging uses. It presents a geographic breakdown of demand and supply across key regions — North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa — with distinct insights into regional consumption patterns, infrastructure trends, and regulatory impacts. The report also analyzes end-user segments in depth, highlighting chemical processing, electronics and semiconductor materials, aerospace components, and niche industrial sectors, while distinguishing demand behavior and quality requirements across these diverse applications.

The scope also includes a technology assessment covering production methods, from traditional ammonium paratungstate routes to aqueous and crystalline AMT processes, alongside emerging purification and recycling technologies impacting yield, purity, and sustainability outcomes. Industry focus areas incorporate supply chain dynamics, material performance standards, and quality benchmarks tied to impurity control and solubility characteristics. Emerging niche segments such as AMT derivatives for energy storage, advanced coatings, and additive manufacturing are evaluated for strategic potential. Additionally, the report assesses competitive positioning, strategic initiatives like capacity expansions and sustainability frameworks, and market forces shaping investment decisions. Designed for business professionals and decision-makers, this scope provides a complete view of current trends, technological implications, regional nuances, and sectoral demand drivers shaping the ammonium metatungstate industry trajectory.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

5% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

H.C. Starck Tungsten, Global Tungsten & Powders Corp., ALMT Corp., Mitsubishi Materials Corporation, Xiamen Tungsten Co., Ltd., Wolfram Bergbau und Hütten AG, Plansee Group, JX Advanced Metals Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |