Reports

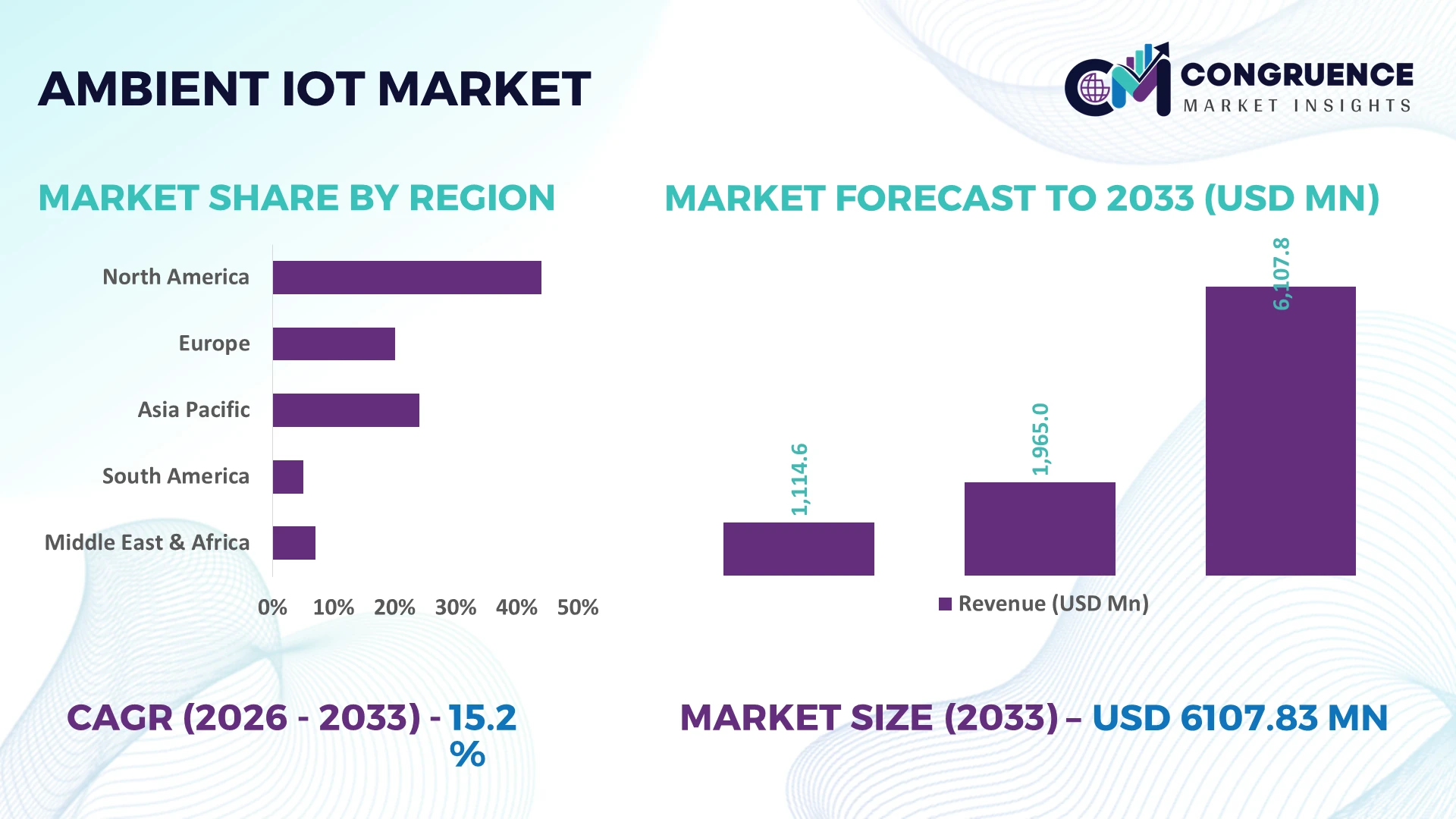

The Global Ambient IoT Market was valued at USD 1965 Million in 2025 and is anticipated to reach a value of USD 6107.83 Million by 2033 expanding at a CAGR of 15.23% between 2026 and 2033. Growth is driven by rapid deployment of battery-free connected devices, standardized low-power wireless protocols, expanding industrial asset visibility, and enterprise investments in intelligent supply-chain automation.

The United States leads the global Ambient IoT market with approximately 34% share, supported by multi-billion-dollar investments in semiconductor innovation, logistics digitalization, and industrial automation across manufacturing, healthcare, and retail sectors. More than 70% of large warehouse operators are expanding smart asset tracking initiatives, while Germany accelerates industrial Ambient IoT integration through advanced factory modernization programs. Ongoing semiconductor supply-chain diversification following global geopolitical trade realignments further strengthens deployment resilience and technology adoption.

Organizations prioritizing scalable Ambient IoT ecosystems, interoperable connectivity, and battery-free sensing capabilities are positioned to achieve stronger operational efficiency and long-term competitive differentiation.

Market Size & Growth: USD 1965 Million (2025) to USD 6107.83 Million (2033) at 15.23% CAGR, driven by battery-free wireless sensing and intelligent asset visibility.

Top Growth Drivers: Battery-free sensors (+38%), logistics digitization (+31%), industrial automation (+29%) accelerate global deployment.

Short-Term Forecast: By 2028, inventory accuracy improves 27% while manual asset-tracking costs decline 24%.

Emerging Technologies: AI-powered analytics, energy harvesting, and Bluetooth LE expansion strengthen scalable Ambient IoT ecosystems.

Regional Leaders: North America exceeds USD 2.1 Billion, Europe USD 1.6 Billion, Asia-Pacific USD 1.8 Billion through manufacturing and logistics modernization.

Consumer/End-User Trends: Over 58% of enterprise deployments prioritize real-time tracking for inventory, healthcare equipment, and reusable assets.

Pilot/Case Example: 2026 smart warehouse deployment improved asset visibility by 35% and reduced misplaced inventory by 28%.

Competitive Landscape: Top suppliers hold approximately 46% market share, led by Qualcomm, Impinj, NXP Semiconductors, Infineon Technologies, and Wiliot.

Regulatory & ESG Impact: Battery-free technologies reduce electronic waste by nearly 20% while supporting sustainability compliance across global operations.

Investment & Funding: More than USD 2.3 Billion supports semiconductor partnerships, industrial expansion, and advanced Ambient IoT platforms amid supply-chain diversification.

Innovation & Future Outlook: Printed electronics, intelligent edge computing, and interoperable connectivity accelerate next-generation enterprise digital transformation.

Ambient IoT market adoption is expanding across logistics, healthcare, retail, and industrial manufacturing as organizations prioritize battery-free sensing, intelligent asset monitoring, and automated inventory visibility. AI-enabled edge intelligence and energy-harvesting devices continue advancing commercial deployments, while over 40% of new enterprise pilots integrate interoperable wireless standards. Evolving sustainability requirements and resilient semiconductor supply chains reinforce long-term deployment strategies, setting the foundation for the strategic discussion.

Ambient IoT is becoming a strategic priority as enterprises transition from periodic asset visibility to continuous, battery-free intelligence across supply chains, industrial facilities, healthcare, and retail. Infrastructure modernization, stricter traceability requirements, and digital warehouse transformation are accelerating deployment decisions. Organizations are integrating low-power sensing into existing operational technology to improve inventory accuracy, automate environmental monitoring, and reduce manual intervention while supporting resilient manufacturing and logistics networks.

Compared with conventional battery-powered tracking systems, Ambient IoT solutions powered by energy harvesting can reduce maintenance costs by nearly 35% while extending operational device availability by more than 50% through battery-free operation. The United States leads commercialization through advanced semiconductor ecosystems and large-scale logistics deployments, whereas Germany emphasizes industrial automation and interoperable factory connectivity under smart manufacturing initiatives. Over the next two to three years, enterprise deployments are expected to expand by more than 40% across warehouse, healthcare, and cold-chain monitoring applications as interoperability standards mature.

Retailers are deploying Ambient IoT-enabled smart labels to improve inventory visibility and reduce stock discrepancies, while manufacturers are expanding partnerships with semiconductor and wireless technology providers to accelerate scalable deployments. Investment priorities increasingly target edge intelligence, standardized wireless ecosystems, and sustainable battery-free devices, positioning early adopters with stronger operational resilience, differentiated service capabilities, and long-term competitive advantage.

The primary market driver is enterprise adoption of battery-free connected devices that deliver continuous visibility across logistics, manufacturing, healthcare, and retail operations. More than 65% of large warehouse modernization projects now include intelligent tracking technologies, while automated inventory accuracy improves by approximately 30% through real-time sensing. The United States continues expanding industrial IoT infrastructure alongside domestic semiconductor investments, strengthening supply resilience and component availability. Companies are responding through strategic alliances between semiconductor manufacturers, cloud platform providers, and wireless technology developers to accelerate commercialization. A significant operational advantage lies in eliminating battery replacement cycles, lowering maintenance costs while enabling large-scale deployment across millions of connected assets with minimal operational disruption.

Limited interoperability between communication standards and legacy enterprise infrastructure remains a structural barrier to broader Ambient IoT deployment. Approximately 42% of industrial facilities continue operating mixed automation environments that require expensive integration, while deployment costs can increase by nearly 20% when proprietary protocols restrict compatibility. Japan and several European manufacturing hubs face integration complexity due to long-established industrial equipment lifecycles. These constraints delay enterprise-scale implementation, reduce operational flexibility, and complicate lifecycle management. Companies are mitigating risks by adopting open communication architectures, diversifying component sourcing, localizing manufacturing partnerships, and investing in standardized development platforms that improve compatibility across heterogeneous industrial ecosystems.

Energy-harvesting technologies create substantial opportunities by enabling maintenance-free sensing across large-scale enterprise environments. More than 55% of emerging smart logistics projects are evaluating battery-free asset monitoring, while intelligent warehouse operations demonstrate productivity improvements exceeding 25% through continuous environmental awareness. South Korea is strengthening next-generation semiconductor innovation, supporting advanced low-power sensing and wireless integration. Companies are expanding research collaborations, ecosystem partnerships, and edge AI development to commercialize intelligent labels, reusable packaging, and connected healthcare devices. A strategic opportunity extends beyond tracking assets toward autonomous operational decision-making, allowing enterprises to optimize workflows without significantly increasing maintenance or infrastructure complexity.

Scaling Ambient IoT deployments across millions of connected endpoints introduces execution challenges involving cybersecurity, network management, and device authentication. Nearly 48% of enterprises identify secure lifecycle management as a critical implementation priority, while connected endpoint volumes are projected to increase by over 35% within operational environments over the next several years. Germany's industrial sector continues strengthening cybersecurity requirements for connected production systems, increasing deployment complexity. Companies must invest in zero-trust security architectures, edge-based intelligence, interoperable device management platforms, and workforce training to maintain consistent performance. Organizations that successfully combine scalable connectivity with robust security governance will establish durable operational advantages and stronger enterprise customer confidence.

Battery-Free Deployment Accelerates: Battery-free connected devices are moving from pilot projects to enterprise-scale operations, with deployment volumes increasing by nearly 42% and maintenance interventions declining by approximately 35%. Large retailers in the United States are replacing conventional inventory tags with energy-harvesting alternatives to improve stock visibility. Ongoing labor shortages and warehouse automation initiatives are encouraging companies to standardize battery-free infrastructure through semiconductor partnerships and integrated wireless ecosystems that reduce operating complexity.

Supply Chains Become Continuously Visible: Ambient IoT is transforming logistics through persistent asset monitoring, with real-time shipment visibility improving by around 38% and inventory discrepancies declining by nearly 27%. Germany's advanced manufacturing sector is integrating connected labels into reusable transport assets to improve traceability. Companies are restructuring logistics workflows by combining cloud analytics, intelligent sensors, and automated replenishment systems, shortening response times while improving supply-chain resilience under evolving trade conditions.

Edge Intelligence Expands Operations: AI-enabled edge processing is reducing network traffic by approximately 30% while shortening device response times by more than 25% for industrial monitoring applications. Japanese manufacturers are embedding lightweight intelligence directly into Ambient IoT endpoints instead of relying solely on centralized processing. This operational transition improves production continuity, minimizes communication overhead, and enables enterprises to scale connected infrastructure without proportionally expanding cloud resources or energy consumption.

Interoperability Becomes Strategic Priority: Standardized wireless connectivity is emerging as a competitive differentiator, with more than 60% of enterprise deployments prioritizing interoperable platforms and integration times decreasing by roughly 22%. New digital product compliance requirements and expanding cross-vendor ecosystems are encouraging companies to redesign product portfolios around open communication standards. A notable shift is the growing preference for ecosystem compatibility over proprietary performance, strengthening long-term deployment flexibility and procurement efficiency.

Battery-Free Sensors represent the dominant segment because they deliver scalable, maintenance-free monitoring across logistics, manufacturing, healthcare, and retail environments. Their ability to eliminate battery replacement reduces lifecycle costs while supporting high-density deployments. Approximately 46% of new Ambient IoT implementations prioritize battery-free sensing technologies, reflecting strong enterprise demand for continuous monitoring and operational efficiency. Smart Tags remain widely deployed for inventory identification, while Connected Labels strengthen intelligent packaging and traceability initiatives. IoT Modules continue supporting integration with existing industrial systems where configurable connectivity remains essential.

Energy Harvesting Devices are the fastest-growing segment as semiconductor innovation improves power conversion efficiency and enables autonomous sensing in previously impractical environments. More than 35% of product development investments now target energy-harvesting architectures, while connected device operating life improves substantially without battery dependence. Companies are expanding product portfolios, forming semiconductor partnerships, and investing in ultra-low-power chipsets to accelerate commercialization. These shifts are redirecting investment toward scalable autonomous sensing rather than conventional powered hardware.

Asset Tracking remains the leading application as enterprises require continuous visibility across warehouses, manufacturing plants, healthcare facilities, and distribution centers. More than 48% of enterprise Ambient IoT deployments prioritize asset identification and condition monitoring to reduce inventory losses and improve operational planning. Smart Logistics is the fastest-growing application, driven by automated fulfillment, reusable transport assets, and intelligent shipment monitoring. Companies are integrating Ambient IoT with warehouse management platforms, enabling faster inventory reconciliation and reducing manual scanning requirements by approximately 30%.

Smart Retail continues expanding through intelligent shelf monitoring and connected pricing solutions, while Industrial Monitoring strengthens predictive maintenance and equipment utilization. Smart Healthcare is gaining momentum through medical asset visibility and environmental monitoring for temperature-sensitive products. Organizations increasingly deploy integrated sensing ecosystems instead of isolated applications, improving operational efficiency across multiple workflows. Vendors are scaling cloud integration, expanding deployment partnerships, and tailoring solutions to sector-specific operational requirements as enterprise demand becomes more process-oriented.

Manufacturing represents the largest end-user segment because production facilities require continuous equipment visibility, material traceability, and automated workflow monitoring. Approximately 44% of enterprise Ambient IoT deployments support manufacturing operations, where intelligent sensing reduces production interruptions and improves resource utilization. Logistics is the fastest-growing end-user segment as warehouse automation, reusable packaging, and shipment transparency become strategic priorities. Companies are expanding industrial partnerships, developing application-specific platforms, and integrating Ambient IoT into digital factory initiatives to strengthen operational performance.

Retail continues accelerating investment through intelligent inventory management and connected merchandising, while Healthcare expands deployment for medical equipment monitoring and pharmaceutical logistics. Agriculture is emerging as a specialized adopter using battery-free sensing for environmental monitoring and precision resource management. More than 33% of enterprise solution providers now offer industry-specific Ambient IoT platforms to improve deployment efficiency and reduce implementation complexity. Competitive positioning increasingly depends on vertical specialization rather than standardized hardware offerings.

North America accounted for the largest market share at 38.4% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a 16.8% CAGR between 2026 and 2033.

Enterprise Digital Infrastructure Accelerates Ambient Intelligence

North America maintains the leading position through advanced semiconductor capabilities, mature cloud ecosystems, and large-scale enterprise digitalization. The region contributes approximately 38.4% of global deployment activity, supported by extensive adoption across logistics, healthcare, manufacturing, and retail. More than 68% of large distribution centers are integrating battery-free sensing into inventory workflows, improving operational visibility while reducing maintenance requirements. Continuous investments in edge computing, wireless connectivity, and semiconductor manufacturing strengthen deployment capacity. Technology providers are expanding ecosystem partnerships to improve interoperability, enabling enterprises to connect intelligent devices across complex operational environments with lower implementation complexity.

United States Market Outlook: The United States remains the regional growth engine due to its leadership in semiconductor innovation, enterprise software integration, and warehouse automation. Over 70% of large logistics operators continue expanding intelligent asset visibility programs using Ambient IoT technologies. Strong investment in domestic semiconductor production, cloud infrastructure, and industrial automation supports rapid commercialization. Companies increasingly collaborate with wireless technology developers and industrial solution providers to accelerate deployment across healthcare, manufacturing, and retail, strengthening long-term operational competitiveness.

Industrial Modernization Strengthens Connected Operations

Europe continues expanding Ambient IoT deployment through advanced manufacturing modernization, sustainability initiatives, and industrial automation. The region accounts for nearly 27% of global adoption, supported by smart factory investments and digital supply-chain transformation. More than 60% of large industrial modernization projects now incorporate connected sensing technologies to improve equipment visibility and operational efficiency. Battery-free devices align with enterprise sustainability priorities by reducing maintenance requirements and electronic waste. Companies are strengthening collaborative innovation programs focused on standardized connectivity and interoperable industrial ecosystems to improve long-term deployment flexibility.

Germany Market Outlook: Germany leads the European market through its advanced manufacturing ecosystem and Industry 4.0 implementation. Industrial enterprises continue integrating Ambient IoT into production monitoring, predictive maintenance, and intelligent logistics operations. Approximately 45% of newly modernized manufacturing facilities incorporate advanced connected sensing platforms. Strong engineering expertise, automation infrastructure, and collaboration between industrial technology providers position Germany as a key commercialization hub for enterprise-scale Ambient IoT deployment.

Manufacturing Scale Drives Rapid Deployment

Asia-Pacific is emerging as the fastest-expanding market through semiconductor manufacturing strength, electronics production, and accelerating industrial digitalization. The region contributes approximately 31% of global manufacturing capacity for key Ambient IoT components while increasing enterprise adoption across logistics and smart factories. Investments in low-power chip development and wireless infrastructure continue expanding deployment readiness. Manufacturers are scaling production of intelligent labels, battery-free sensors, and connected modules to support both domestic implementation and export demand. Enterprise adoption is accelerating alongside digital manufacturing initiatives and warehouse modernization programs.

China Market Outlook: China dominates regional deployment through extensive electronics manufacturing capacity, large-scale logistics infrastructure, and rapid industrial automation. More than 50% of advanced connected device manufacturing is concentrated within the country's electronics ecosystem. Domestic technology companies continue expanding semiconductor capabilities while integrating Ambient IoT into manufacturing, retail, and transportation operations. Strong government support for intelligent manufacturing and digital infrastructure further accelerates commercialization and strengthens international competitiveness.

Logistics Modernization Expands Enterprise Adoption

South America is gradually strengthening Ambient IoT implementation through logistics modernization, retail digitalization, and industrial process optimization. The region contributes approximately 5% of global market activity, with deployment concentrated around major distribution networks and manufacturing corridors. Warehouse modernization programs have improved automated inventory visibility by nearly 22% across selected enterprise operations. Infrastructure limitations and connectivity variation continue influencing deployment speed, prompting companies to prioritize scalable pilot programs and localized technology partnerships before expanding enterprise-wide implementations.

Brazil Market Outlook: Brazil represents the largest national opportunity due to expanding retail infrastructure, manufacturing activity, and logistics investments. Large enterprises are deploying connected tracking technologies across distribution centers to improve inventory management and transportation efficiency. Growing cloud adoption and digital supply-chain initiatives encourage solution providers to establish regional partnerships while adapting products to local operational requirements. Continued investment in warehouse automation supports broader enterprise acceptance of Ambient IoT technologies.

Infrastructure Investment Supports Intelligent Connectivity

The Middle East & Africa market is expanding through smart infrastructure development, industrial diversification, and logistics modernization initiatives. The region accounts for approximately 4% of global deployment activity while increasing investments in digital industrial ecosystems. More than 30% of newly developed logistics facilities within major economic zones incorporate intelligent connectivity planning for future Ambient IoT integration. Companies are aligning technology deployments with smart city initiatives, energy optimization programs, and advanced warehouse operations, creating stronger foundations for long-term enterprise adoption.

United Arab Emirates Market Outlook: The United Arab Emirates leads regional implementation through advanced logistics infrastructure, smart city investments, and technology-friendly regulatory frameworks. Major logistics operators continue integrating connected monitoring technologies into warehousing and transportation networks to improve operational visibility. Expansion of digital free zones, enterprise cloud infrastructure, and intelligent port operations strengthens demand for scalable Ambient IoT solutions. Strategic collaboration between technology providers and logistics enterprises positions the country as the primary regional innovation hub.

The Ambient IoT market is shaped by competition between global semiconductor leaders including Qualcomm, NXP Semiconductors, Impinj, Infineon Technologies, and Wiliot, against specialized wireless innovators and regional connectivity solution providers. The top five participants collectively control approximately 46% of market activity through integrated hardware, connectivity, and software ecosystems. Competition centers on ultra-low-power performance, interoperability, deployment speed, and ecosystem integration rather than component pricing alone. Battery-free architectures reduce maintenance requirements by nearly 35%, while standardized wireless platforms shorten enterprise deployment cycles by approximately 25%, creating measurable differentiation. Companies are expanding through semiconductor partnerships, cloud integration, reference platform development, and vertical collaboration with logistics and industrial automation providers. Competitive momentum is shifting toward ecosystem ownership as interoperable platforms outperform proprietary solutions and supply-chain localization strengthens component availability. Certification complexity, semiconductor design capability, and enterprise-scale deployment expertise remain significant entry barriers. Sustainable leadership depends on delivering scalable battery-free innovation, trusted interoperability, rapid commercialization, and strong enterprise integration capabilities.

Qualcomm Incorporated

NXP Semiconductors N.V.

Impinj, Inc.

Infineon Technologies AG

Wiliot Ltd.

STMicroelectronics N.V.

Texas Instruments Incorporated

Silicon Laboratories Inc.

EM Microelectronic

Nordic Semiconductor ASA

Atmosic Technologies, Inc.

Alien Technology, LLC

Ambient IoT technology is rapidly transitioning from conventional battery-powered sensing to autonomous, energy-harvesting architectures capable of continuous operation with minimal maintenance. Battery-free sensors, RF energy harvesting, Bluetooth Low Energy, and ultra-low-power integrated circuits are becoming the foundation of intelligent asset monitoring across logistics, manufacturing, healthcare, and retail. Compared with legacy battery-dependent tracking systems, energy-harvesting devices reduce maintenance costs by approximately 35% while improving operational availability by more than 50%. Nearly 45% of new enterprise pilots now evaluate battery-free connectivity as the preferred deployment model for large-scale monitoring.

Emerging innovation focuses on edge AI, printed electronics, ambient backscatter communication, and interoperable wireless standards. Intelligent edge processing lowers network traffic by nearly 30%, while lightweight AI improves event detection accuracy by approximately 25% without increasing cloud workloads. Semiconductor manufacturers and wireless platform providers gain the strongest competitive advantage by integrating sensing, connectivity, and analytics into unified ecosystems. Enterprises increasingly prioritize interoperable platforms capable of supporting millions of connected assets through standardized deployment frameworks.

Between 2026 and 2028, printed battery-free electronics, intelligent digital labels, and advanced energy-harvesting chipsets will accelerate enterprise-scale deployment. Organizations investing early in integrated Ambient IoT platforms will strengthen supply-chain visibility, reduce operational complexity, improve sustainability performance, and establish differentiated competitive positions as autonomous connected infrastructure becomes a core enterprise capability.

June 2024 – Wiliot launched its inaugural Ambient IoT Unplug Fest and introduced the Ambient IoT Certified Product program to accelerate interoperability across battery-free devices. The initiative targeted 100% interoperability validation for certified solutions, strengthening ecosystem scalability and enterprise deployment readiness. Source: wiliot.com

February 2025 – Qualcomm joined Intel, Infineon Technologies, Atmosic, PepsiCo, VusionGroup, and Wiliot as a founding member of the Ambient IoT Alliance to develop global battery-free connectivity standards spanning b—Bluetooth, Wi-Fi, and 5G. The alliance accelerated ecosystem standardization and cross-industry commercialization.

September 2025 – Avery Dennison expanded its strategic partnership with Wiliot to manufacture next-generation Bluetooth-enabled Ambient IoT sensors featuring a smaller chip footprint and simplified inlay architecture. The collaboration strengthened large-scale production capability while improving sensor performance and lowering manufacturing complexity.

January 2026 – Wiliot partnered with Tageos to launch the EOS-654 BLE G3 passive Bluetooth Low Energy inlay supporting the Gen3 IoT Pixel platform through a dual-band 2.4 GHz and sub-1 GHz architecture. The innovation enabled broader enterprise-scale deployment across retail and logistics supply chains. Source: tageos.com

This report provides a comprehensive assessment of the global Ambient IoT market, examining deployment trends, competitive positioning, technology evolution, and strategic industry developments between 2026 and 2033. The analysis covers five core product types, five major application areas, and five primary end-user industries while evaluating adoption patterns across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. More than 45% of enterprise deployments are assessed through operational use cases including asset visibility, industrial monitoring, and intelligent logistics.

The study evaluates battery-free sensing, energy harvesting, connected labels, smart tags, low-power wireless connectivity, and edge intelligence alongside emerging Ambient IoT ecosystems. It benchmarks leading technology providers, enterprise deployment strategies, and innovation priorities while highlighting regional investment patterns, interoperability progress, and supply-chain transformation. Strategic insights support market entry, product development, partnership evaluation, expansion planning, competitive benchmarking, and long-term business decision-making across established and emerging Ambient IoT deployment environments.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 1965 Million |

Market Revenue in 2033 | USD 6107.83 Million |

CAGR (2026 - 2033) | 15.23% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Qualcomm Incorporated, NXP Semiconductors N.V., Impinj, Inc., Infineon Technologies AG, Wiliot Ltd., STMicroelectronics N.V., Texas Instruments Incorporated, Silicon Laboratories Inc., EM Microelectronic, Nordic Semiconductor ASA, Atmosic Technologies, Inc., Alien Technology, LLC |

Customization & Pricing | Available on Request (10% Customization is Free) |