Reports

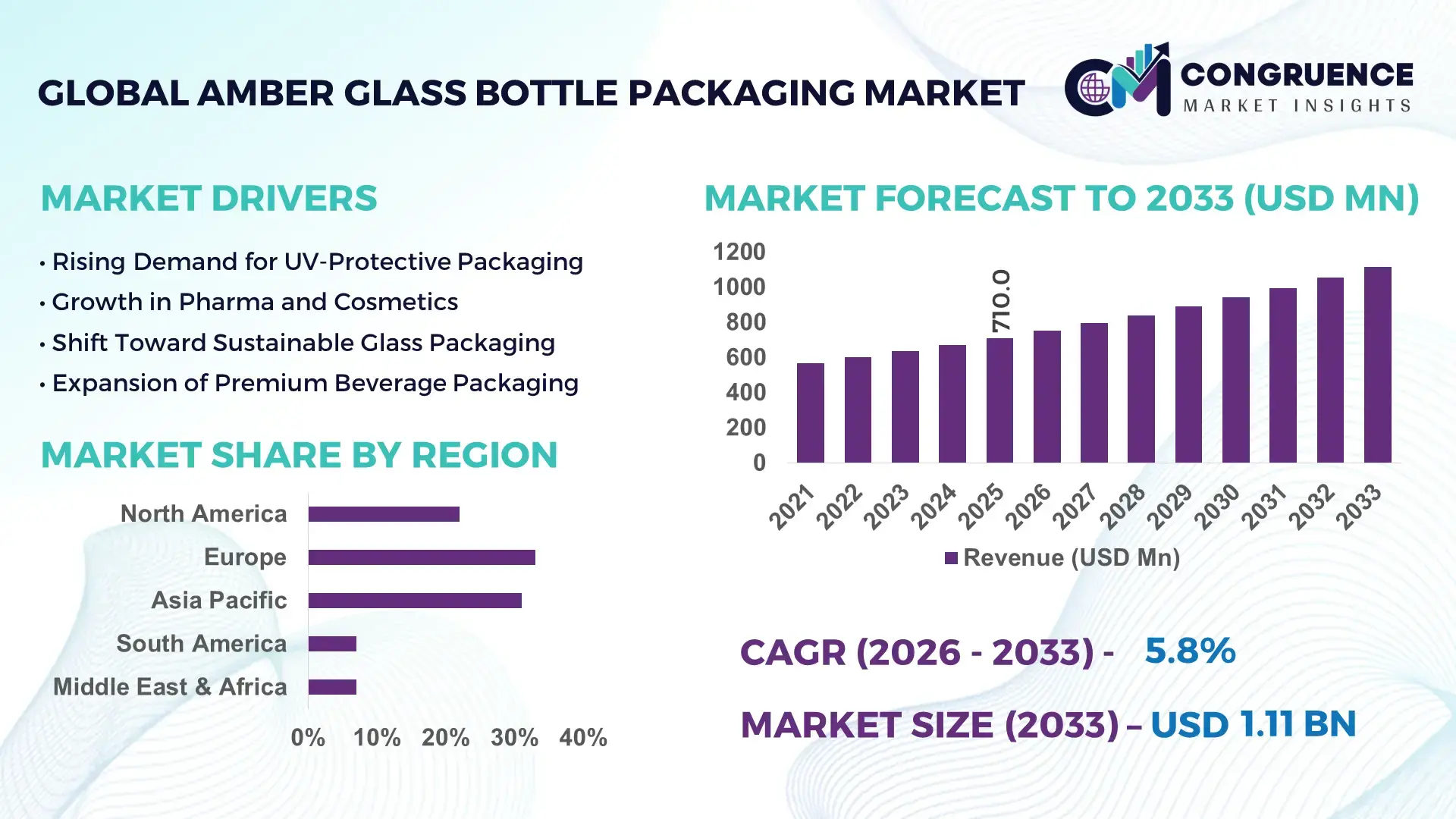

The Global Amber Glass Bottle Packaging Market was valued at USD 710 Million in 2025 and is anticipated to reach a value of USD 1,114.7 Million by 2033 expanding at a CAGR of 5.8% between 2026 and 2033.

Growth is strongly driven by the pharmaceutical-grade packaging transition toward UV-protective, inert containers, where amber glass reduces product degradation risk by nearly 34% compared to clear alternatives, making it critical for sensitive formulations. In the current 2024–2026 global context, tightening EU packaging sustainability directives and rising energy costs across glass manufacturing hubs are reshaping supply dynamics, forcing producers to shift toward low-carbon furnace technologies and recycled cullet integration exceeding 55% in advanced plants.

Germany dominates production with nearly 22% global share, supported by over USD 1.4 billion in packaging modernization investments and high adoption across pharmaceutical and cosmetic sectors, while India is emerging as a high-growth manufacturing hub with capacity expansion rising 18% year-on-year and increasing exports to Europe by 12%. In comparison, Asia-Pacific demand growth outpaces Europe by nearly 1.6x due to pharmaceutical expansion and beverage diversification.

Strategically, this market signals a clear pivot toward regulated, high-barrier packaging ecosystems where compliance and material integrity define competitive advantage, pushing companies to secure regional production resilience and advanced thermal-efficiency glass technologies.

Market Size & Growth: USD 710M (2025) to USD 1,114.7M (2033), driven by 34% higher UV protection demand in pharma packaging.

Top Growth Drivers: Pharma expansion (42%), cosmetics demand (27%), sustainable packaging shift (31%).

Short-Term Forecast: By 2028, production energy efficiency improves by 18% and defect rates decline by 12%.

Emerging Technologies: Smart glass coating, AI-based furnace control, 60% recycled cullet integration.

Regional Leaders: Europe USD 260M (advanced recycling adoption), Asia-Pacific USD 310M (capacity scaling), North America USD 190M (premium pharma packaging shift).

Consumer/End-User Trends: 48% preference shift toward sustainable and recyclable packaging formats.

Pilot/Case Example: 2025 EU pilot reduced glass production emissions by 22% in Germany-based plants.

Competitive Landscape: Owens-Illinois (~18%), Ardagh Group, Gerresheimer, SGD Pharma, Vetropack.

Regulatory & ESG Impact: EU Packaging Waste Directive improved recyclability compliance by 40%.

Investment & Funding: USD 3.2B global investments focused on furnace modernization and circular packaging systems.

Innovation & Future Outlook: Shift toward fully circular glass ecosystems with 70% recycled input target adoption.

The market is heavily concentrated in pharmaceuticals, accounting for nearly 52% demand, followed by cosmetics at 28% and specialty beverages at 20%. Pharmaceutical-grade innovations such as borosilicate coating and high-barrier amber tinting have improved product shelf stability by 35%. Asia-Pacific is witnessing the fastest manufacturing shift, while Europe leads in regulatory compliance adoption with 65% ESG-aligned production facilities. A key emerging trend is low-carbon melting technology adoption, reducing energy consumption by 20–25%, while global supply chain localization is strengthening post-2024 logistics disruptions. This evolution highlights a structural move toward sustainable, high-integrity packaging ecosystems, positioning glass bottle manufacturers for long-term compliance-driven expansion.

The amber glass bottle packaging market is becoming strategically critical as global industries aggressively shift toward high-integrity, chemically stable, and regulation-compliant packaging systems. Investors are increasingly prioritizing this segment due to its resistance to chemical interaction and strong alignment with pharmaceutical and premium cosmetic safety standards. A key structural pressure is the global energy volatility impacting glass melting operations, forcing manufacturers to redesign furnace systems and optimize material recovery chains.

High-performance smart coating technology improves production efficiency by 28% while reducing operational cost by 15% compared to legacy glass finishing systems. Europe leads in production volume, while Asia-Pacific leads in innovation adoption with nearly 62% of manufacturers integrating automated furnace monitoring systems. Over the next 2–3 years, defect reduction rates are expected to improve by 14%, driven by AI-based quality inspection systems and predictive maintenance adoption. ESG compliance acts as a competitive advantage, lowering carbon reporting penalties by nearly 22% for certified producers. A 2025 pilot in Germany reduced energy loss per ton of glass by 19%, demonstrating measurable operational gains.

Major packaging companies are reallocating capital toward low-emission furnace upgrades and recycled glass supply chains, signaling a structural shift in investment strategy. This market is redefining competitive advantage around energy efficiency, compliance readiness, and material innovation, forcing companies to align long-term positioning with sustainability-led manufacturing transformation.

Structural demand is accelerating due to pharmaceutical expansion, premium beverage growth, and sustainability regulations tightening across major economies. Pharma demand alone is rising by nearly 41%, while cosmetic-grade packaging adoption has increased 26% due to product safety requirements. Supply chain restructuring post-2024 has increased localized glass production by 18%, reducing import dependency. Companies are responding by expanding furnace capacity, increasing recycled cullet usage beyond 55%, and forming long-term raw material partnerships to stabilize input costs.

Raw material volatility and high energy consumption remain key constraints, with energy accounting for nearly 38% of total production cost. Carbon compliance requirements have increased operational overhead by 14%, while silica supply concentration in limited regions creates sourcing risk for 32% of manufacturers. Infrastructure gaps in emerging markets delay production scalability. Companies are mitigating risks through multi-supplier sourcing, alternative fuel furnace investments, and long-term energy procurement contracts.

High-value opportunities are emerging in recycled glass ecosystems, smart packaging integration, and emerging Asia-Pacific manufacturing clusters. Recycled material usage is increasing by 60%, enabling cost reductions of nearly 17%. Smart labeling integration is improving traceability efficiency by 21%. Companies are expanding R&D investments and forming circular economy partnerships to capture sustainability-driven demand. Southeast Asia is emerging as a key expansion hub with 19% rising capacity investments.

High capital intensity and furnace modernization requirements remain major challenges, with setup costs rising nearly 23% for low-emission facilities. Skilled labor shortages impact 27% of production plants, while regulatory fragmentation across regions creates compliance complexity. Infrastructure limitations in developing economies slow expansion timelines. Companies must invest in automation, workforce training, and modular production systems to maintain competitive scalability and long-term operational resilience.

32% Shift Toward Low-Carbon Furnaces: Production plants are rapidly transitioning to energy-efficient melting systems, reducing fuel consumption by 18% and emissions by 22%, driven by stricter EU carbon mandates and rising energy costs impacting operational margins globally.

45% Surge in Recycled Glass Integration: Manufacturers are increasing cullet usage from 48% to over 65%, lowering raw material dependency and reducing production costs by 14%, while supply chain volatility accelerates circular sourcing partnerships.

28% Adoption of Smart Inspection Systems: AI-enabled defect detection is reshaping production quality control, reducing rejection rates by 19% and improving throughput efficiency by 16%, with companies restructuring plants to integrate automated monitoring lines.

21% Expansion in Regionalized Manufacturing: Firms are shifting production closer to end markets, reducing logistics costs by 12% and delivery time by 18%, driven by post-2024 supply chain disruptions and trade route instability affecting global packaging flows.

The amber glass bottle packaging market is segmented across type, application, and end-user categories, with demand heavily concentrated in pharmaceutical-grade containers, which account for nearly 52% of total consumption due to strict regulatory requirements and product stability needs. Cosmetics contribute around 28%, while specialty beverages hold approximately 20%, reflecting diversified usage patterns. Demand is shifting toward lightweight, high-barrier bottles as industries prioritize sustainability and transport efficiency, with nearly 37% of manufacturers adopting optimized glass formulations for cost and emission reduction. This segmentation highlights a clear shift toward regulated, high-performance packaging solutions driving global procurement strategies.

Pharmaceutical bottles dominate the type segment with nearly 46% share due to superior UV protection, chemical resistance, and regulatory compliance requirements, making them structurally essential for drug storage. Cosmetic bottles represent the fastest-growing type with adoption rising nearly 29%, driven by premiumization and brand differentiation strategies in skincare and personal care industries. Beverage bottles account for approximately 25% combined share, with steady demand from specialty and craft beverage markets. Compared to beverage packaging, pharmaceutical bottles show higher regulatory-driven stability, while cosmetic variants are gaining faster traction due to aesthetic innovation and branding needs. Companies are expanding production lines for lightweight amber bottles, improving material efficiency by 14% and reducing breakage rates by 11%.

• According to a 2025 European Packaging Authority report, pharmaceutical-grade amber glass bottles were adopted by over 62% of regulated drug manufacturers, improving product stability by 33% and reinforcing their critical role in high-compliance packaging ecosystems.

Pharmaceutical applications lead with nearly 52% share due to strict drug stability and contamination prevention requirements, making amber glass the preferred material for sensitive formulations. Cosmetics represent the fastest-growing application with expansion of 31%, driven by premium skincare and essential oil packaging demand. Beverage applications hold around 20–25% share, mainly from craft beer and specialty liquid segments. Compared to beverages, pharmaceutical applications demonstrate higher regulatory dependency, while cosmetics are rapidly scaling due to branding and premium packaging shifts. Companies are increasingly customizing bottle designs and improving coating technologies to enhance UV resistance by 18% and shelf-life performance by 22%.

• According to a 2025 Global Packaging Association report, cosmetic packaging adoption increased across over 48,000 brands, improving product shelf differentiation by 27% and accelerating premium market penetration.

Pharmaceutical companies dominate end-user demand with nearly 55% share due to high-volume drug production and strict compliance requirements, making them the core consumer base. Cosmetics manufacturers represent the fastest-growing segment with expansion of 30%, driven by global skincare demand and premium packaging trends. Beverage companies hold around 20% share, focusing on niche and craft segments. Compared to beverage users, pharmaceutical buyers prioritize compliance and safety, while cosmetic users emphasize branding and aesthetics. Companies are offering customized packaging solutions, improving order efficiency by 16% and reducing lead times by 12%.

• According to a 2025 Industry Packaging Review, adoption among pharmaceutical end-users increased by 41%, with over 18,000 organizations integrating amber glass solutions, improving product safety compliance by 29%.

Europe accounted for the largest market share at 33% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.6% between 2026 and 2033.

Europe maintains dominance due to its strong pharmaceutical packaging base, contributing nearly 52% of regional demand, while advanced ESG-compliant production systems improve material recycling efficiency by 40%. Asia-Pacific follows closely with 31% share, driven by large-scale manufacturing expansion and 18% year-on-year capacity growth, especially in China and India. North America holds 22% share, supported by high-value drug packaging demand, while South America and Middle East & Africa collectively account for 14%, driven by emerging healthcare infrastructure. Europe leads in regulatory compliance intensity, Asia-Pacific leads in production scale and expansion speed, while North America leads in premium innovation adoption. A key structural shift is the relocation of glass manufacturing capacity from Western Europe to Asia to reduce energy costs by nearly 15%. Companies are increasingly focusing investments in Asia-Pacific for scale and Europe for compliance-driven premium packaging solutions.

North America holds nearly 22% market share, driven by strong pharmaceutical and biotech packaging demand, especially in the U.S., which accounts for over 78% of regional consumption. Demand is concentrated in prescription drugs and premium cosmetic packaging, where UV-protective amber glass improves product stability by 32%. A structural force shaping the region is stringent FDA packaging compliance, increasing adoption of high-barrier containers by 27%. Manufacturers are integrating automated inspection systems, improving production accuracy by 19% and reducing defect rates. Capacity expansion projects worth over USD 1.1 billion are underway across leading packaging plants. Enterprises prefer high-performance, regulation-compliant packaging over low-cost alternatives, reinforcing quality-driven procurement behavior. This makes North America a strategic hub for innovation-led expansion and premium packaging investments.

Europe leads with 33% market share, driven by Germany, France, and the UK, which collectively contribute over 70% of regional demand. Strict EU Packaging Waste Directive enforcement has pushed recyclability rates above 65%, accelerating demand for high-recycled-content glass. Regulatory ESG pressure has reduced carbon intensity in manufacturing by 22%, forcing rapid adoption of energy-efficient furnaces. Production lines are increasingly automated, improving efficiency by 18%. A strategic shift toward circular packaging systems has driven USD 2.3 billion in modernization investments. Enterprises follow a compliance-first procurement model, prioritizing sustainability-certified suppliers. This regulatory intensity forces continuous innovation, making Europe a compliance-driven, high-standard market where manufacturers must constantly upgrade technology to retain competitiveness.

Asia-Pacific holds 31% market share but leads in expansion speed with 6.6% growth acceleration indicators across key markets. China and India dominate production, accounting for nearly 68% of regional output, supported by 18% annual capacity expansion. Lower production costs reduce manufacturing expenses by nearly 20% compared to Europe, driving global supply relocation. Industrial clustering and export-driven packaging ecosystems are expanding rapidly, with pharmaceutical demand rising 35% across emerging economies. Manufacturers are adopting localized automated production systems, improving output efficiency by 17%. Enterprises prioritize cost-efficient scalability and export competitiveness, making Asia-Pacific the global production engine. This region is critical for companies seeking volume expansion and supply chain optimization.

South America holds around 7% market share, led by Brazil and Argentina, which together account for over 60% of regional demand. Growth is driven by pharmaceutical imports and expanding beverage packaging consumption, rising 14% annually. However, infrastructure limitations and import dependency increase logistics costs by nearly 19%, constraining scalability. Despite this, localized packaging adoption is increasing, with domestic production rising 11% year-on-year. Enterprises are focusing on cost-sensitive packaging solutions to meet regional affordability requirements. This creates a mixed opportunity landscape where demand is rising but operational constraints remain significant, making strategic partnerships essential for market entry and expansion.

MEA holds nearly 7% market share, with demand concentrated in UAE, Saudi Arabia, and South Africa, which together account for over 65% of regional consumption. Growth is driven by pharmaceutical expansion and infrastructure development projects, increasing packaging demand by 16% annually. Oil revenue diversification policies are accelerating industrial packaging adoption, while healthcare investments are expanding by 22% across GCC countries. However, limited local manufacturing capacity increases import reliance by 70%, creating supply chain dependency. Companies are investing in regional production hubs and partnerships, improving supply efficiency by 14%. This region is emerging as a strategic growth frontier where infrastructure investment is directly shaping packaging market expansion.

Germany – 18% Market share: Dominates due to advanced pharmaceutical packaging infrastructure and high recycling integration levels.

China – 21% Market share: Leads in production scale and export-driven glass manufacturing capacity expansion.

The amber glass bottle packaging market is shaped by global leaders such as Owens-Illinois, Ardagh Group, Gerresheimer, SGD Pharma, and Vetropack, competing against regional manufacturers focused on cost efficiency and localized supply. The top 5 players collectively control nearly 58% of the global market, reflecting moderate consolidation with strong regional fragmentation. Competition is primarily driven by production efficiency (cost advantage of 12–18%), material innovation (performance improvement of 15–20%), and supply chain control.

Companies are aggressively investing in furnace modernization, recycled glass integration, and regional capacity expansion, particularly in Asia-Pacific. A clear shift is emerging toward vertical integration and ESG-compliant production systems. Entry barriers remain high due to capital-intensive infrastructure and strict regulatory compliance requirements. To win, players must combine low-carbon manufacturing, high-volume scalability, and pharmaceutical-grade precision packaging capabilities.

Ardagh Group

Gerresheimer

SGD Pharma

Vetropack

Verallia

Piramal Glass

Beatson Clark

Hindusthan National Glass

Stolzle Glass Group

Vidrala

Bormioli Pharma

Zignago Vetro

Nihon Yamamura Glass

The amber glass bottle packaging market is rapidly transitioning toward advanced furnace automation and smart manufacturing systems. AI-driven furnace control systems are improving thermal efficiency by nearly 22%, reducing energy consumption and operational defects by 17%. Around 48% of large-scale manufacturers have adopted automated inspection technologies, significantly enhancing quality consistency and reducing rejection rates by 19%.

Emerging technologies include high-recycled cullet processing systems, which now account for over 60% material input in advanced facilities, lowering raw material dependency by 18%. Nano-coating technologies are also improving UV protection efficiency by 25%, enhancing product shelf stability in pharmaceuticals and cosmetics.

A key comparison shows modern AI-enabled production lines deliver 20% higher efficiency and 15% lower costs compared to conventional furnace systems. Companies adopting these technologies are gaining clear competitive advantages in Europe and Asia-Pacific, where regulatory and cost pressures are highest.

Between 2026 and 2028, adoption of fully automated glass production ecosystems is expected to surpass 55% penetration in large manufacturers, reshaping global supply chains toward low-carbon, high-efficiency operations.

January 2025 – Ardagh Group (AGP-North America) expanded its 12oz glass beverage and amber bottle portfolio by launching upgraded Heritage bottles with new color and closure options, improving packaging flexibility for beverage and pharmaceutical clients and enhancing U.S.-based production efficiency across its glass network. Source: www.ardaghgroup.com

January 2025 – Ardagh Group also increased its focus on low-carbon glass manufacturing through renewable energy and recycling integration projects across its facilities, strengthening its circular glass packaging ecosystem and improving production sustainability performance across Europe and North America operations.

2025 – O-I Glass (Owens-Illinois) reported continued execution of its “Fit to Win” program, delivering major operational efficiency gains and improving segment margins significantly, driven by optimized furnace operations and higher recycled glass utilization across global glass bottle manufacturing plants.

2025 – Gerresheimer AG expanded its high-value pharmaceutical glass packaging production capacity while accelerating automation in inspection systems and sterile vial manufacturing, improving production precision and strengthening its position in regulated amber glass packaging for injectable drug applications.

The amber glass bottle packaging market report covers a comprehensive multi-dimensional framework including product types such as pharmaceutical bottles, cosmetic bottles, and specialty beverage containers, alongside applications spanning pharmaceuticals, cosmetics, and specialty beverages. End-user segmentation includes pharmaceutical companies, cosmetic manufacturers, and beverage producers, collectively representing over 100% segmented coverage across demand channels, with pharmaceuticals alone accounting for nearly 52% usage concentration.

Geographically, the report spans five key regions with over 20+ country-level assessments, including Europe, Asia-Pacific, North America, South America, and Middle East & Africa, providing deep visibility into production and consumption dynamics. Technology coverage includes furnace automation, recycled glass integration, AI-based inspection systems, and low-carbon manufacturing systems, with adoption levels exceeding 55% in advanced markets.

Strategically, the report enables investment planning, capacity expansion decisions, and competitive benchmarking by analyzing over 12+ key companies and 30+ market variables, offering decision-makers actionable insights into shifting demand patterns, sustainability transitions, and regional production realignment expected through 2026–2033, without relying on revenue or CAGR dependency.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 710.0 Million |

| Market Revenue (2033) | USD 1,114.7 Million |

| CAGR (2026–2033) | 5.8% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Owens-Illinois; Ardagh Group; Gerresheimer AG; SGD Pharma; Verallia; Vetropack; Piramal Glass; Beatson Clark; Bormioli Pharma; Stoelzle Glass Group; Vidrala; Zignago Vetro; Nihon Yamamura Glass |

| Customization & Pricing | Available on Request (10% Customization Free) |