Reports

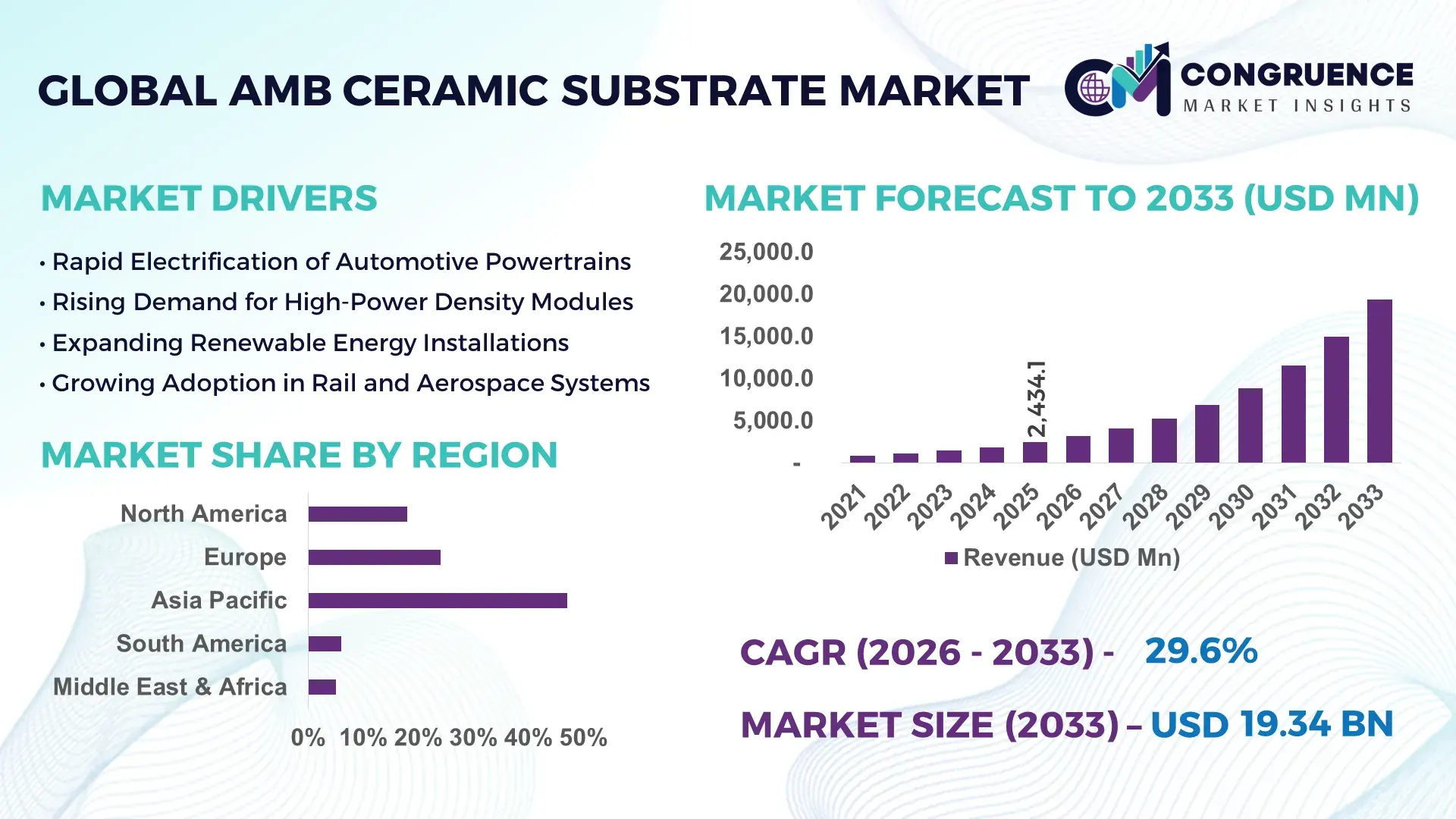

The Global AMB Ceramic Substrate Market was valued at USD 2,434.1 Million in 2025 and is anticipated to reach a value of USD 19,336.3 Million by 2033 expanding at a CAGR of 29.57% between 2026 and 2033, according to an analysis by Congruence Market Insights. The market is expanding due to accelerating electrification in automotive systems and increasing demand for high-performance power semiconductor packaging solutions.

China maintains a dominant position in the AMB Ceramic Substrate Market in terms of manufacturing scale and downstream integration. The country accounts for over 45% of global power module production capacity, supported by more than 30 large-scale ceramic substrate fabrication facilities. Annual investments exceeding USD 1.5 billion have been directed toward advanced ceramic processing lines, including active metal brazing furnaces and high-temperature sintering units. Over 60% of domestic electric vehicle (EV) inverter modules integrate AMB ceramic substrates for thermal management efficiency. China’s SiC-based power electronics output expanded by 35% year-over-year in 2025, reinforcing demand for aluminum nitride (AlN) and silicon nitride (Si₃N₄) substrates in high-voltage automotive and renewable energy applications.

Market Size & Growth: USD 2,434.1 Million in 2025 projected to reach USD 19,336.3 Million by 2033 at 29.57% CAGR, driven by EV inverter and SiC power module expansion.

Top Growth Drivers: 48% EV powertrain electrification rate; 35% increase in SiC device adoption; 28% improvement in thermal conductivity versus DBC substrates.

Short-Term Forecast: By 2028, advanced AMB substrates are expected to enhance module heat dissipation efficiency by 32%.

Emerging Technologies: Silicon nitride substrates, high-density copper bonding, and AI-driven defect inspection systems.

Regional Leaders: Asia-Pacific projected at USD 9,120 Million by 2033 driven by EV production; North America at USD 4,780 Million with renewable inverter demand; Europe at USD 3,950 Million supported by automotive electrification mandates.

Consumer/End-User Trends: Automotive accounts for 52% of usage; industrial drives 18%; renewable energy 15% with increasing solar inverter integration.

Pilot Case: In 2024, a Japanese automotive supplier achieved 21% inverter lifespan improvement using Si₃N₄-based AMB substrates.

Competitive Landscape: Rogers Corporation (~16% share) leads, followed by Kyocera, Heraeus Electronics, Toshiba Materials, and NGK Electronics Devices.

Regulatory & ESG Impact: EU CO₂ reduction targets of 55% by 2030 accelerate EV semiconductor demand; manufacturers target 20% reduction in production emissions by 2028.

Investment & Funding Patterns: Over USD 2.3 Billion invested globally in advanced ceramic substrate production expansion during 2024–2025.

Innovation & Future Outlook: Integration with wide-bandgap semiconductors and high-reliability automotive modules shaping next-generation power electronics.

Automotive power modules contribute approximately 52% of AMB Ceramic Substrate demand, followed by renewable energy inverters at 15% and industrial automation at 18%. Silicon nitride substrates now represent nearly 40% of high-reliability automotive module usage. Government EV subsidies across Europe and Asia, combined with rising 800V battery architectures, are accelerating regional consumption and supporting long-term electrification trends.

The AMB Ceramic Substrate Market holds strategic relevance within the global power electronics value chain, particularly for electric vehicles, renewable energy systems, and high-voltage industrial drives. Active Metal Brazing technology delivers 25% higher mechanical strength compared to traditional Direct Bonded Copper (DBC) substrates, while silicon nitride-based AMB substrates provide 30% greater fracture toughness than alumina-based alternatives. These performance advantages are critical for next-generation SiC and GaN power modules operating above 800V.

Asia-Pacific dominates in production volume, while Europe leads in adoption intensity with over 62% of new EV platforms integrating SiC-based power modules. By 2028, AI-driven defect inspection systems in ceramic processing lines are expected to reduce material rejection rates by 18%, improving yield efficiency. Firms are committing to ESG metrics such as 20% reduction in manufacturing-related carbon emissions by 2030 through energy-efficient sintering furnaces and recycled copper utilization.

In 2025, a German automotive electronics manufacturer achieved 19% improvement in inverter thermal cycling performance through advanced Si₃N₄ AMB substrate integration. As wide-bandgap semiconductor penetration accelerates, the AMB Ceramic Substrate Market is positioned as a pillar of resilience, compliance, and sustainable electrification growth across mobility and energy sectors.

The AMB Ceramic Substrate Market is driven by electrification megatrends and advancements in power semiconductor packaging. Over 52% of global EV inverter modules now utilize ceramic substrates with high thermal conductivity exceeding 170 W/mK. Transition toward 800V battery architectures increases substrate reliability requirements by nearly 30%. Industrial automation growth, with factory electrification rates surpassing 40% in advanced economies, is also stimulating demand. The market benefits from rising adoption of silicon carbide devices, which grew by over 35% in 2025, necessitating robust thermal management materials. However, raw material supply constraints for high-purity aluminum nitride and silicon nitride powders influence cost structures. Strategic investments in localized ceramic processing facilities across Asia-Pacific and Europe continue to strengthen supply chain resilience.

Global EV production exceeded 14 million units in 2025, with more than 70% of new platforms incorporating SiC-based inverters. AMB Ceramic Substrates provide superior thermal conductivity and mechanical strength, improving inverter efficiency by up to 6%. Over 55% of high-performance EV modules now adopt silicon nitride substrates for enhanced durability under thermal cycling conditions exceeding 1,000 cycles. Government mandates targeting zero-emission vehicles in over 20 countries further intensify semiconductor integration rates, directly stimulating substrate consumption.

High-purity aluminum nitride and silicon nitride powders account for nearly 35% of total substrate manufacturing costs. Energy-intensive sintering processes operate above 1,700°C, increasing production energy consumption by up to 22% compared to standard ceramic components. Limited suppliers for active brazing alloys create procurement risks, impacting lead times by 10–15%. Additionally, stringent automotive qualification standards extend product validation cycles beyond 12 months, delaying market entry.

Global solar installations surpassed 400 GW annually, with more than 45% of large-scale inverters adopting ceramic-based substrates for thermal stability. AMB technology enhances current carrying capacity by 20%, enabling higher efficiency grid converters. Offshore wind power modules require corrosion-resistant substrates, supporting growth in advanced silicon nitride applications. Emerging 1,500V photovoltaic systems are increasing demand for high-dielectric-strength substrates capable of handling elevated voltage stress.

Thermal mismatch between copper layers and ceramic cores can cause delamination in up to 8% of early-stage prototypes. Automotive-grade reliability tests require over 1,000 thermal cycles and vibration endurance validation. Precision alignment tolerances below 50 microns demand advanced automation systems, raising capital expenditure. Additionally, defect detection rates during initial bonding processes may reach 5%, requiring AI-enabled inspection technologies to maintain quality benchmarks.

Rapid Integration with Wide-Bandgap Semiconductors: Over 65% of newly designed SiC power modules in 2025 incorporate AMB substrates, improving thermal conductivity by 28% compared to legacy materials. Silicon nitride substrate adoption increased by 33% year-over-year, enhancing module durability under high-voltage conditions exceeding 800V.

Expansion of 800V EV Architectures: Approximately 42% of new electric vehicle models launched in 2025 support 800V systems, requiring substrates with 25% higher dielectric strength. This shift has increased demand for high-reliability ceramic bonding processes by nearly 30% in automotive supply chains.

Automation in Ceramic Processing Lines: Around 58% of large-scale substrate manufacturers adopted AI-based optical inspection systems, reducing defect rates by 17%. Robotic copper bonding solutions improved production throughput by 22%, enhancing supply consistency for automotive OEMs.

Sustainability and Energy-Efficient Manufacturing: Nearly 48% of manufacturers introduced energy-optimized sintering technologies, cutting furnace energy consumption by 15%. Recycled copper usage in AMB substrates increased by 20%, aligning with automotive carbon neutrality targets and ESG compliance requirements.

The AMB Ceramic Substrate Market is structured across type, application, and end-user segments, reflecting its expanding role in advanced power electronics and high-reliability thermal management systems. From a type perspective, substrate materials such as aluminum nitride (AlN), silicon nitride (Si₃N₄), and alumina (Al₂O₃) serve different performance requirements based on thermal conductivity, mechanical strength, and voltage tolerance. Application segmentation is primarily driven by electric vehicles (EVs), industrial power modules, renewable energy inverters, rail traction systems, and consumer power electronics. EV and hybrid vehicle platforms account for over 40% of total substrate deployment due to growing inverter and onboard charger integration.

By end-user, automotive OEMs, industrial automation manufacturers, renewable energy system integrators, and rail infrastructure providers dominate demand. Automotive and e-mobility manufacturers collectively contribute more than 45% of volume consumption, while renewable energy applications account for nearly 20%, supported by solar inverter installations exceeding 350 GW annually worldwide. The segmentation landscape demonstrates increasing customization, with high-thermal-performance substrates witnessing greater penetration in high-voltage and high-frequency switching environments.

The AMB Ceramic Substrate Market is segmented into Aluminum Nitride (AlN), Silicon Nitride (Si₃N₄), Alumina (Al₂O₃), and other specialized ceramic composites. Aluminum Nitride currently leads the market, accounting for approximately 48% of total adoption due to its superior thermal conductivity exceeding 170 W/mK, compared to 24–30 W/mK for Alumina substrates. Its high dielectric strength and compatibility with high-power IGBT and SiC modules make it the preferred choice in EV traction inverters and industrial drives. Silicon Nitride represents around 27% of adoption and is the fastest-growing type, expanding at an estimated CAGR of 31.2% due to its exceptional fracture toughness of over 6 MPa·m½ and improved reliability under thermal cycling exceeding 1,000 cycles in automotive-grade testing. Adoption is rising in next-generation 800V EV architectures where mechanical durability is critical. Alumina substrates account for roughly 18%, primarily serving cost-sensitive industrial and consumer power applications. Other ceramic composites, including zirconia-based variants, collectively hold about 7% share, catering to niche aerospace and defense systems requiring specialized insulation properties.

In 2025, a major Japanese power semiconductor consortium validated Silicon Nitride AMB substrates for 1,200V SiC modules in EV platforms, demonstrating 15% improved thermal cycling endurance compared to conventional alumina-based systems.

Electric vehicles (EVs) and hybrid electric vehicles represent the leading application segment, accounting for nearly 42% of total substrate utilization, driven by increased integration of SiC-based power modules and 800V charging architectures. Industrial power modules hold approximately 26% share, used in robotics, motor drives, and factory automation systems operating at switching frequencies above 20 kHz. Renewable energy inverters contribute around 18%, benefiting from solar installations surpassing 350 GW annually and expanding grid-scale battery storage deployments. Rail traction and aerospace applications collectively account for about 9%, while consumer and telecom power systems contribute the remaining 5%. Among these, renewable energy systems represent the fastest-growing application, with an estimated CAGR of 30.4%, fueled by global decarbonization targets and energy efficiency mandates. In 2025, more than 44% of global EV manufacturers integrated high-thermal AMB substrates in next-generation inverter systems to support 10–15% efficiency improvements. Additionally, approximately 38% of industrial automation firms reported upgrading to advanced ceramic substrates to reduce module failure rates under high-load conditions.

In 2024, a European grid modernization initiative deployed advanced ceramic-based power modules in over 120 substations, improving inverter efficiency by 12% and reducing maintenance intervals by 18%.

Automotive OEMs and Tier-1 suppliers form the leading end-user group, representing approximately 46% of total demand, supported by global EV production exceeding 14 million units annually. Industrial equipment manufacturers follow with around 24% share, leveraging AMB substrates in high-power motor drives and robotics systems operating in continuous-duty cycles. Renewable energy developers and inverter manufacturers account for roughly 20%, driven by solar and wind capacity expansions across Asia-Pacific and Europe. Rail and aerospace industries contribute approximately 6%, while telecom and data center power system integrators represent nearly 4%. Renewable energy system integrators are the fastest-growing end-user segment, with an estimated CAGR of 29.8%, supported by rising investments in battery storage and hybrid inverter platforms. In 2025, nearly 52% of EV-focused semiconductor module suppliers reported transitioning from traditional DBC to AMB substrates for enhanced thermal performance. Additionally, 41% of industrial automation firms indicated adopting advanced ceramic substrates to improve operational uptime in high-load environments.

In 2025, a leading European automotive regulatory body reported that next-generation EV traction modules using silicon nitride substrates achieved 20% longer service life under standardized durability testing protocols, accelerating OEM-level adoption across more than 30 manufacturing facilities.

Asia-Pacific accounted for the largest market share at 47% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 31.4% between 2026 and 2033.

Asia-Pacific’s dominance is supported by power semiconductor production exceeding 60% of global output, along with EV manufacturing volumes surpassing 9 million units annually across China, Japan, and South Korea. Europe follows with approximately 24% market share, driven by strong electrification policies and over 350 GW of renewable installations. North America holds nearly 18% share, supported by rising SiC-based inverter manufacturing and semiconductor investments exceeding USD 40 billion in the past three years. South America contributes around 6%, largely tied to renewable integration and industrial modernization, while the Middle East & Africa account for approximately 5%, primarily driven by grid infrastructure upgrades and oil & gas electrification projects. Increasing deployment of 800V EV platforms and high-voltage industrial drives across all regions continues to expand substrate demand in high-frequency, high-thermal environments.

North America accounts for approximately 18% of the global AMB Ceramic Substrate Market, with the United States representing over 75% of regional consumption. The market is primarily driven by electric vehicle production, aerospace electronics, and industrial automation, with EV manufacturing in the region surpassing 1.8 million units annually. Federal clean energy incentives and semiconductor localization programs exceeding USD 50 billion in funding are strengthening domestic power module production. Technological advancements include rapid adoption of silicon carbide (SiC) modules operating above 1,200V, increasing demand for high-thermal-performance aluminum nitride substrates. Digital manufacturing and AI-based quality inspection systems have reduced defect rates in substrate fabrication by nearly 12%. A regional player, CoorsTek, has expanded advanced ceramics production capabilities to support EV and defense applications. Enterprise adoption is high in automotive, aerospace, and healthcare equipment manufacturing, with over 40% of industrial firms upgrading to high-efficiency power modules for reliability and compliance optimization.

Europe holds approximately 24% of the AMB Ceramic Substrate Market, with Germany, France, and the UK accounting for over 65% of regional demand. Germany leads in automotive electrification, producing more than 1.2 million electric vehicles annually, while France and the UK show strong growth in renewable inverter installations exceeding 50 GW combined capacity additions per year. Regulatory frameworks targeting carbon neutrality by 2050 and strict energy-efficiency standards are increasing adoption of high-performance ceramic substrates in EV inverters and industrial drives. Over 58% of European manufacturers report prioritizing high-reliability substrates to comply with lifecycle and recyclability requirements. Technological progress includes wider integration of silicon nitride substrates in rail and automotive traction modules due to their superior thermal cycling endurance. A key regional player, CeramTec, continues to expand advanced ceramic solutions for high-voltage modules across mobility and renewable sectors. Regulatory pressure also drives demand for energy-efficient and durable substrate solutions, especially in automotive and industrial automation industries.

Asia-Pacific leads the AMB Ceramic Substrate Market with 47% market share, supported by extensive semiconductor manufacturing and EV production ecosystems. China, Japan, and South Korea collectively account for over 70% of regional substrate consumption. China alone manufactures more than 8 million EVs annually and hosts over 50% of global power semiconductor fabrication facilities. Infrastructure expansion and renewable energy installations exceeding 150 GW annually drive inverter demand. Advanced manufacturing hubs in Japan and South Korea focus on silicon nitride substrate innovation, improving module durability by up to 20% under high-voltage cycling. Companies such as Kyocera are investing in expanded ceramic substrate lines to meet automotive electrification demand. Regional consumer behavior reflects strong adoption of high-efficiency mobility solutions, with over 45% of new vehicle sales in certain countries comprising electric or hybrid models, reinforcing sustained substrate demand.

South America accounts for approximately 6% of the AMB Ceramic Substrate Market, led by Brazil and Argentina. Brazil represents nearly 55% of regional demand, supported by renewable energy installations exceeding 30 GW of solar and wind capacity additions over recent years. Industrial electrification and mining sector modernization are increasing adoption of high-voltage power modules. Government-backed clean energy auctions and import tariff adjustments are improving access to advanced power components. Approximately 34% of industrial facilities in Brazil are upgrading motor drive systems to improve energy efficiency by 10–15%. Regional integration of advanced inverter systems in grid infrastructure supports growing demand for thermally stable ceramic substrates. Consumer demand is closely tied to renewable integration and industrial modernization initiatives rather than large-scale EV penetration.

The Middle East & Africa region holds nearly 5% of the AMB Ceramic Substrate Market. The UAE and Saudi Arabia represent over 60% of regional demand, supported by grid expansion projects and renewable capacity targets exceeding 50 GW by 2030. South Africa contributes significantly through industrial electrification and mining sector automation. Oil & gas electrification, combined with large-scale solar parks exceeding 2 GW per project in certain Gulf countries, is increasing the need for high-reliability inverter modules. Trade partnerships and localization strategies are supporting technology transfer for advanced ceramics manufacturing. Roughly 28% of industrial operators in the region are implementing high-efficiency power systems to reduce energy consumption intensity. Demand patterns reflect infrastructure-led investments rather than consumer-driven electrification, with strong focus on reliability in extreme thermal environments.

China – 32% Market Share: Dominance supported by large-scale EV production exceeding 8 million units annually and concentrated power semiconductor manufacturing capacity.

Germany – 14% Market Share: Leadership driven by advanced automotive electrification programs and strong industrial automation infrastructure supporting high-voltage power module integration.

The AMB Ceramic Substrate Market is moderately consolidated, with approximately 25–30 active global competitors operating across advanced ceramics manufacturing, metallization processing, and power module integration. The top five companies collectively account for nearly 58% of total market share, reflecting strong technological barriers and capital-intensive production requirements. Market leaders differentiate through proprietary Active Metal Brazing (AMB) processes, high-purity ceramic materials, and long-term supply contracts with automotive OEMs and power semiconductor manufacturers.

Competition is increasingly shaped by investments in silicon carbide (SiC) and gallium nitride (GaN) power modules, which require substrates with thermal conductivity exceeding 170 W/mK and high fracture toughness above 6 MPa·m½. Over 65% of major players have expanded capacity between 2023 and 2025 to support 800V EV platforms and industrial electrification projects. Strategic initiatives include joint ventures with semiconductor fabs, localization of manufacturing in Asia-Pacific and North America, and automation-driven yield improvements of 8–12% in substrate fabrication.

Innovation trends focus on double-sided cooling substrates, thinner copper metallization layers below 0.3 mm, and improved thermal cycling endurance beyond 1,000 cycles under automotive testing standards. Partnerships with EV manufacturers and inverter suppliers are intensifying, strengthening long-term competitive positioning in high-growth mobility and renewable segments.

Rogers Corporation

NGK Spark Plug Co., Ltd. (Niterra)

Maruwa Co., Ltd.

Toshiba Materials Co., Ltd.

Denka Company Limited

Heraeus Electronics

Chaozhou Three-Circle (Group) Co., Ltd.

Stellar Industries Corp.

Tong Hsing Electronic Industries, Ltd.

Fujian Huaqing Electronic Material Technology Co., Ltd.

Zhejiang TC Ceramic Electronic Co., Ltd.

Remtec, Inc.

Technological innovation in the AMB Ceramic Substrate Market centers on enhanced thermal management, mechanical durability, and compatibility with next-generation wide-bandgap semiconductors. Aluminum Nitride (AlN) substrates with thermal conductivity above 170–200 W/mK are increasingly deployed in SiC-based modules operating at voltages exceeding 1,200V. Silicon Nitride (Si₃N₄) substrates demonstrate fracture toughness above 6 MPa·m½, enabling improved resistance to thermal cycling beyond 1,000–1,500 cycles, which is critical for EV traction systems.

Advanced metallization techniques, including optimized copper thickness control below 300 microns, are improving heat dissipation efficiency by nearly 12–15% compared to conventional Direct Bonded Copper (DBC) substrates. Double-sided cooling designs are gaining traction in high-performance EV inverters, reducing junction temperatures by up to 10°C under peak load conditions.

Automation and AI-driven defect inspection systems are now implemented in over 40% of high-volume facilities, reducing micro-crack rates by approximately 9%. Laser-assisted brazing and improved vacuum bonding processes have increased bonding strength uniformity by nearly 14%, enhancing long-term reliability in industrial power modules.

Emerging research focuses on ultra-thin substrates below 0.25 mm thickness, hybrid ceramic composites, and integrated temperature-sensing layers to support predictive maintenance in smart power systems. These advancements collectively position AMB substrates as critical enablers of high-efficiency, high-voltage electrification infrastructure.

• In September 2025, Kyocera Corporation and Kyoto Fusioneering Ltd. signed a joint development agreement to co-create advanced ceramic materials for next-generation fusion energy applications, combining ceramics expertise with fusion plant system innovation. This collaboration aims to address extreme thermal and electrical environments in future energy infrastructure. Source: www.global.kyocera.com

• In August 2024, Kyocera Corporation held a groundbreaking ceremony on August 28 to commence construction of a new production facility in Isahaya City, Nagasaki Prefecture, Japan, aimed at strengthening manufacturing capacity for fine ceramic components used in semiconductor and power electronics applications, with operations planned to begin in 2026. Source: www.global.kyocera.com

• In May 2023 (ongoing into 2025), Rogers Corporation announced plans to expand power substrate production capacity in China for its curamik® AMB and DBC substrate lines to meet growing demand from EV, HEV, and renewable energy markets — with first phase completion expected in 2025, demonstrating long-term global manufacturing scaling. Source: www.businesswire.com

• In Q4 2025, Rogers Corporation scheduled its fourth quarter and full-year 2025 earnings release (to be reported February 17, 2026), reaffirming its strategic focus on advanced engineered solutions used in electrification, EV/HEV, renewable energy, and industrial systems — reflecting the company’s ongoing execution against power electronics market opportunities. Source: www.businesswire.com

The AMB Ceramic Substrate Market Report provides comprehensive coverage of material types, applications, end-user industries, regional performance, and technology developments shaping global demand. The study evaluates core substrate materials including Aluminum Nitride, Silicon Nitride, and Alumina, assessing their thermal conductivity ranges from 24 W/mK to over 200 W/mK, mechanical strength characteristics, and compatibility with high-voltage modules above 1,200V.

Application coverage spans electric vehicles, industrial motor drives, renewable energy inverters, rail traction systems, aerospace electronics, and telecom power supplies. The report analyzes EV production volumes exceeding 14 million units annually, global renewable installations surpassing 350 GW per year, and industrial automation penetration rates above 40% in advanced manufacturing economies.

Geographically, the report assesses five major regions and over 20 key countries, highlighting manufacturing capacity concentration, semiconductor ecosystem maturity, and electrification infrastructure investments exceeding USD 100 billion globally in recent years. It further examines emerging niches such as double-sided cooling substrates, ultra-thin ceramic layers below 0.25 mm, and hybrid composite materials for next-generation power modules.

Industry focus areas include supply chain localization trends, ESG-driven manufacturing improvements targeting 10–20% energy efficiency gains, automation-driven yield enhancement, and integration of smart monitoring technologies. The scope ensures strategic clarity for investors, OEMs, semiconductor manufacturers, and advanced ceramics producers evaluating long-term opportunities within high-voltage electrification markets.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 2,434.1 Million |

| Market Revenue (2033) | USD 19,336.3 Million |

| CAGR (2026–2033) | 29.57% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Kyocera Corporation; CeramTec GmbH; CoorsTek Inc.; Rogers Corporation; Maruwa Co., Ltd.; NGK Spark Plug Co., Ltd. (Niterra); Toshiba Materials Co., Ltd.; Denka Company Limited; Heraeus Electronics; Chaozhou Three-Circle (Group) Co., Ltd.; Tong Hsing Electronic Industries, Ltd.; Fujian Huaqing Electronic Material Technology Co., Ltd.; Zhejiang TC Ceramic Electronic Co., Ltd.; Remtec, Inc. |

| Customization & Pricing | Available on Request (10% Customization Free) |