Reports

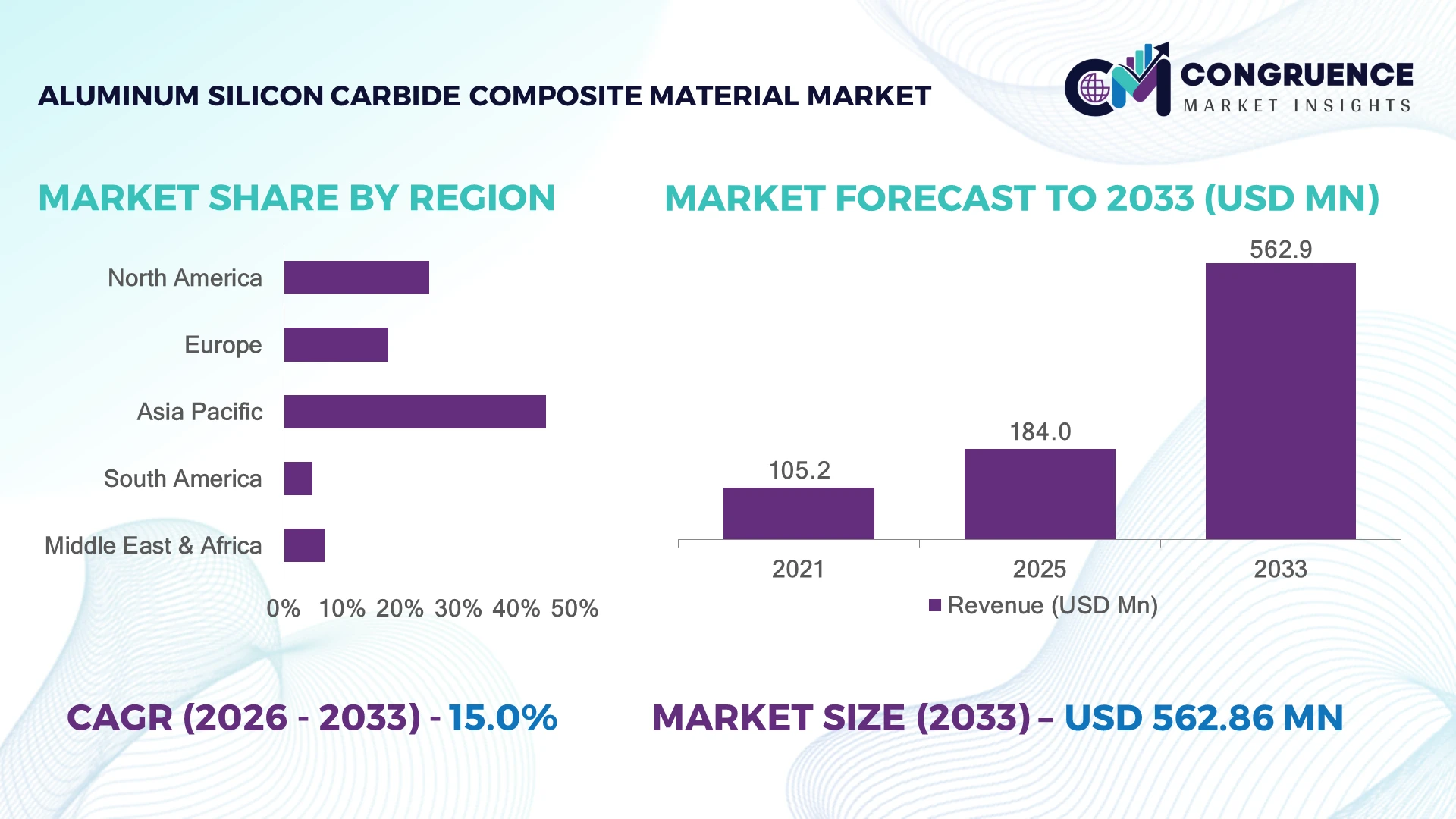

The Global Aluminum Silicon Carbide Composite Material Market was valued at USD 184 Million in 2025 and is anticipated to reach a value of USD 562.9 Million by 2033 expanding at a CAGR of 15% between 2026 and 2033. Growth is driven by rising adoption of lightweight thermal management materials in electric vehicles, aerospace electronics, power modules, and high-performance semiconductor packaging requiring superior heat dissipation and dimensional stability.

China dominates the market with nearly 38% share, supported by large-scale SiC material production capacity, EV manufacturing expansion, and semiconductor investments exceeding USD 100 billion under national technology initiatives. The United States follows with strong aerospace and defense applications, while Japan maintains advanced electronics adoption with over 25% of global precision component manufacturing influence. Compared with India’s emerging manufacturing base, China’s established supply chain delivers faster industrial scaling.

Strategic material localization and advanced manufacturing investments will determine future competitive advantage.

Market Size & Growth: USD 184 Million (2025) to USD 562.9 Million (2033), expanding at 15% CAGR, driven by advanced semiconductor packaging and lightweight thermal solutions.

Top Growth Drivers: Electric vehicle electronics +35%, aerospace component demand +28%, semiconductor thermal management adoption +30%.

Short-Term Forecast: By 2028, material processing efficiency improves 20% and manufacturing waste reduces 15% through automation.

Emerging Technologies: AI-based material optimization, automated composite fabrication, and next-generation SiC power electronics accelerate global adoption.

Regional Leaders: Asia-Pacific reaches USD 300 Million+ by 2033 with EV expansion; North America exceeds USD 150 Million with aerospace adoption; Europe approaches USD 100 Million through energy transition programs.

Consumer/End-User Trends: Over 60% of advanced electronics manufacturers prioritize high thermal conductivity composites for compact designs.

Pilot/Case Example: 2024 automotive thermal management projects using aluminum silicon carbide composites achieved around 25% weight reduction in power module applications.

Competitive Landscape: Leading suppliers include around 20% market concentration among major players such as Denka, CeramTec, Materion, CPS Technologies, and Thermal Management Technologies.

Regulatory & ESG Impact: Lightweight composite adoption supports up to 15% efficiency improvement in selected transportation systems through reduced component weight.

Investment & Funding: More than USD 500 Million in material science investments target semiconductor supply chain expansion and regional manufacturing capacity.

Innovation & Future Outlook: Next-generation SiC-aluminum composites, localized production hubs, and AI-driven design platforms will reshape high-growth industrial applications.

Aluminum Silicon Carbide Composite Material is gaining importance across semiconductor, aerospace, defense, and electric mobility sectors due to its exceptional thermal conductivity and lightweight structure. Recent innovations focus on improved particle distribution, automated manufacturing, and precision electronic packaging, with advanced composite adoption rising by approximately 30% in high-performance applications. Supply-chain diversification after global semiconductor disruptions is accelerating regional production investments. These developments position aluminum silicon carbide composites as a strategic material for next-generation industrial systems.

Aluminum silicon carbide composite material is becoming strategically important as industries seek lightweight, high-strength, and thermally efficient alternatives for advanced electronics, electric vehicles, and aerospace systems. Supply-chain restructuring following semiconductor shortages and increasing regional manufacturing initiatives are encouraging companies to secure domestic sources of critical composite materials.

Compared with traditional aluminum components, aluminum silicon carbide composites deliver significantly higher thermal stability and improved dimensional control, reducing thermal management challenges by nearly 30% in demanding electronic applications. Asia-Pacific leads in manufacturing scale through China, Japan, and South Korea, while North America emphasizes defense, aerospace, and semiconductor innovation with higher-value applications.

Over the next 2–3 years, manufacturers are increasing automation, improving powder processing techniques, and forming partnerships across semiconductor and automotive ecosystems. For example, EV power module suppliers are integrating aluminum silicon carbide heat spreaders to improve reliability and reduce system weight. Companies prioritizing localized production, advanced fabrication capabilities, and strategic collaborations will gain stronger positioning as industries transition toward efficient and resilient material solutions.

The increasing deployment of aluminum silicon carbide composites in semiconductor packaging, EV power modules, and aerospace electronics is accelerating market expansion. Demand is supported by over 35% growth in electric vehicle power electronics integration and nearly 30% improvement in thermal efficiency requirements for compact systems. China’s semiconductor localization programs and the United States’ advanced manufacturing investments are strengthening domestic supply chains. Companies are responding through automated composite fabrication, strategic partnerships, and capacity expansion to meet precision material requirements. The key advantage is enabling smaller, lighter, and more reliable thermal components while reducing system-level engineering constraints.

High manufacturing complexity and specialized processing requirements remain major barriers for aluminum silicon carbide composite adoption. Production costs are approximately 20–30% higher than conventional aluminum solutions due to advanced powder metallurgy and precision fabrication processes. Dependence on limited high-quality silicon carbide suppliers, particularly for aerospace-grade applications, creates supply volatility. Japan and China maintain stronger material processing ecosystems, while emerging manufacturing hubs face infrastructure gaps. Companies are reducing exposure through supplier diversification, long-term procurement agreements, and localized production investments. The primary operational challenge is balancing premium material performance with cost competitiveness in price-sensitive industrial applications.

Expanding applications in electric mobility, renewable power systems, and advanced electronics create significant opportunities for aluminum silicon carbide composites. More than 40% of new EV platforms emphasize improved thermal management solutions, while semiconductor manufacturers increasingly adopt advanced heat dissipation materials for high-power devices. India’s growing electronics manufacturing ecosystem and China’s EV production scale are creating new demand channels. Companies are investing in R&D partnerships, AI-assisted material design, and automated manufacturing technologies to improve consistency and reduce production costs. A key opportunity lies in integrating these composites into compact power modules where traditional materials cannot meet increasing thermal performance requirements.

Maintaining consistent quality during large-scale aluminum silicon carbide composite production remains a critical challenge for manufacturers. Variations in particle distribution, bonding quality, and manufacturing parameters can affect component reliability by 10–15% across high-precision applications. Aerospace and semiconductor industries require strict validation standards, increasing qualification timelines and operational complexity. The United States and European manufacturers face pressure to strengthen domestic composite manufacturing capabilities amid global supply-chain restructuring. Companies must invest in process automation, advanced quality monitoring, and workforce expertise to achieve reliable scaling. Long-term competitiveness depends on creating standardized production systems that support high-volume deployment without compromising performance.

Automated Composite Manufacturing Shift Manufacturers are accelerating automated processing and precision fabrication as quality requirements increase across semiconductor and aerospace applications. Automated production lines are improving material consistency by nearly 20% and reducing processing defects by approximately 15%. Companies in Japan and China are adopting intelligent manufacturing systems to strengthen output reliability, while supply-chain disruptions have encouraged localized production. The non-obvious shift is that automation is becoming a cost-control strategy rather than only a productivity tool.

EV Thermal Systems Integration Electric vehicle manufacturers are increasing aluminum silicon carbide adoption in power modules, with advanced thermal components appearing in more than 35% of new high-performance EV designs. Companies are redesigning battery and inverter systems to reduce weight and improve heat dissipation efficiency by 20–30%. Rising localization policies in China and the United States are accelerating supplier partnerships and technology collaborations for next-generation mobility platforms.

Semiconductor Packaging Optimization Advanced electronics companies are using aluminum silicon carbide composites to manage higher power densities in semiconductor systems. Adoption in specialized thermal packaging applications has increased by around 25%, driven by AI hardware expansion and high-performance computing requirements. Enterprises are investing in customized composite solutions and supplier alliances to improve reliability, shorten design cycles, and support compact electronic architectures.

Regional Supply Chain Restructuring Global material producers are restructuring sourcing strategies as governments prioritize critical material security. China currently supports over 40% of processing capacity, while the United States and Europe are expanding domestic advanced material programs. Companies are increasing inventory planning, dual sourcing, and regional manufacturing partnerships to reduce supply risks and maintain stable production schedules.

Silicon carbide reinforced aluminum composites represent the leading type segment due to superior thermal conductivity, lightweight performance, and compatibility with semiconductor and aerospace components. This segment accounts for approximately 55% of current applications, supported by strong adoption in power electronics and thermal management systems. Aluminum-based composites with optimized SiC distribution provide 25–35% better heat dissipation than conventional aluminum alloys, strengthening their position in high-performance industries. Companies are expanding production capabilities and improving reinforcement techniques to enhance reliability and reduce manufacturing complexity. Other composite formulations, including aluminum matrix variants and customized hybrid materials, continue gaining attention for specialized applications. The fastest-growing shift is toward advanced SiC particle optimization, driven by increasing demand for compact electronic systems. Emerging material designs are achieving around 20% improvement in dimensional stability, encouraging partnerships between material suppliers and electronics manufacturers. Companies are prioritizing R&D investments to develop application-specific grades for EV, aerospace, and semiconductor markets.

Semiconductor thermal management is the leading application segment, accounting for nearly 45% of aluminum silicon carbide composite usage due to rising power density in electronic devices. AI processors, power modules, and high-performance computing systems require materials capable of maintaining thermal stability under demanding conditions. Companies are integrating these composites into heat spreaders and electronic packaging solutions, improving operational efficiency and reducing overheating risks by approximately 30%. Electric vehicle power systems represent the fastest-growing application area, supported by increasing inverter and battery management requirements. EV manufacturers are adopting lightweight thermal components to improve system efficiency, with adoption increasing by nearly 35% across advanced vehicle platforms. Aerospace electronics and defense applications remain strategically important due to reliability requirements, while industrial systems are gradually shifting toward advanced thermal materials. Companies are forming technology partnerships and expanding production capacity to address rising demand from electrification and digital infrastructure.

The electronics industry represents the dominant end-user segment due to extensive requirements for thermal control in semiconductor devices, power modules, and communication infrastructure. This segment contributes approximately 50% of overall application demand, supported by increasing miniaturization and higher processing power requirements. Companies are developing customized composite solutions for electronic manufacturers to improve reliability and support compact designs. Automotive manufacturers represent the fastest-growing end-user group as EV production expands and thermal efficiency becomes a critical engineering priority. Automotive adoption is increasing by nearly 30–35% as manufacturers integrate advanced materials into inverter systems, battery platforms, and charging infrastructure. Aerospace, defense, and industrial users continue adopting aluminum silicon carbide composites where durability and thermal stability are essential. Companies are targeting these segments through strategic collaborations, application-specific product development, and localized manufacturing initiatives. Future demand is shifting toward industries requiring lightweight, high-performance materials with improved lifecycle efficiency.

Asia-Pacific accounted for the largest market share at 45% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 16.2% between 2026 and 2033.

North America holds approximately 25% of the aluminum silicon carbide composite material market, supported by semiconductor manufacturing, aerospace electronics, defense systems, and electric vehicle component development. The United States is increasing domestic advanced material capabilities through semiconductor supply-chain programs and industrial modernization initiatives. More than 30% of regional demand originates from high-performance thermal management applications requiring lightweight and durable materials. Companies are expanding fabrication capacity, forming technology partnerships, and investing in specialized composite processing facilities. The region’s strategic advantage comes from strong aerospace engineering expertise and growing demand for reliable thermal solutions in advanced computing and electrification systems.

United States Market Outlook: The United States represents the leading country market in North America due to its semiconductor, aerospace, and defense manufacturing ecosystem. Over 40% of regional advanced electronics investments are concentrated in domestic semiconductor expansion projects, creating demand for high-performance thermal materials. Companies are strengthening local supply networks and developing customized aluminum silicon carbide solutions for next-generation power systems.

Europe contributes nearly 18% of global aluminum silicon carbide composite demand, driven by automotive electrification, industrial automation, aerospace engineering, and energy-efficient technology adoption. Germany, France, and Italy are key manufacturing centers where advanced materials support lightweight component development and thermal management requirements. Approximately 25% of European industrial manufacturers are increasing investment in material efficiency and process optimization initiatives. Regulatory focus on carbon reduction and energy efficiency is encouraging adoption of lightweight composite solutions. Companies are strengthening partnerships with automotive suppliers and research institutions to improve production scalability and application-specific performance.

Germany Market Outlook: Germany leads Europe’s adoption due to its automotive engineering strength and precision manufacturing capabilities. The country’s electric vehicle production ecosystem supports increasing demand for advanced thermal materials, with more than 20 major automotive technology projects integrating lightweight component innovations. Manufacturers are prioritizing composite material partnerships to improve vehicle efficiency and electronic system reliability.

Asia-Pacific dominates the aluminum silicon carbide composite material market with approximately 45% share, supported by China, Japan, South Korea, and Taiwan’s advanced electronics manufacturing infrastructure. China contributes nearly 35% of regional demand due to semiconductor production, electric vehicle manufacturing, and large-scale material processing capabilities. Japan and South Korea strengthen the market through precision engineering and high-performance electronic applications. More than 50% of regional deployments are linked to electronics and power management systems. Companies are expanding local production facilities, improving automation, and developing supplier networks to support rising demand from EV and semiconductor industries.

China Market Outlook: China remains the largest country market due to its extensive semiconductor, EV, and advanced manufacturing ecosystem. The country supports over one-third of global electric vehicle production, increasing demand for efficient thermal management materials. Domestic manufacturers are investing in composite processing technologies and strengthening supply-chain independence through localized material development.

South America represents an emerging market with approximately 5% global share, supported by industrial modernization, mining technology upgrades, renewable energy projects, and growing electronics requirements. Brazil is the primary contributor due to its manufacturing base and infrastructure scale. Around 15% of regional industrial companies are increasing investments in automation and advanced component technologies. However, limited local composite manufacturing capacity and dependence on imported specialized materials continue affecting deployment speed. Companies are addressing these limitations through international partnerships, technology transfers, and targeted investments in high-value industrial applications.

Brazil Market Outlook: Brazil holds the strongest market position in South America due to its industrial base, automotive manufacturing presence, and infrastructure development activity. The country’s automotive sector accounts for a significant portion of advanced material demand, while manufacturers are exploring lightweight composite solutions to improve efficiency and durability in industrial systems.

Middle East & Africa accounts for nearly 7% of global aluminum silicon carbide composite material demand, supported by industrial diversification programs, aerospace investments, energy infrastructure modernization, and advanced manufacturing initiatives. The United Arab Emirates and Saudi Arabia are increasing adoption of high-performance materials through technology-driven industrial projects. More than 20% of new advanced manufacturing investments in selected Gulf economies focus on improving production capabilities and supply-chain resilience. Companies are targeting aerospace, energy, and electronics applications through partnerships and localized manufacturing strategies. The region’s opportunity is strengthened by infrastructure expansion, although specialized material expertise remains concentrated among global suppliers.

United Arab Emirates Market Outlook: The United Arab Emirates is emerging as the leading country market in the region due to investments in aerospace, advanced manufacturing, and technology infrastructure. The country’s industrial diversification programs are supporting adoption of engineered materials, with multiple aerospace and electronics initiatives requiring lightweight, thermally efficient components. Companies are expanding partnerships to establish regional material capabilities.

The Aluminum Silicon Carbide Composite Material market is shaped by competition between global advanced material suppliers such as Materion and CeramTec, specialized AlSiC manufacturers including CPS Technologies, and regional producers targeting cost-efficient thermal management applications. The top five players account for approximately 45% of market activity, reflecting moderate concentration. Competition is based on material performance, customization, production reliability, and supply-chain control, with thermal conductivity improvements of 20–30% and weight reductions of 15–25% influencing customer decisions. Players are expanding through aerospace qualification, semiconductor partnerships, automated manufacturing, and vertical integration of composite processing. The market is shifting toward localized supply networks as EV and semiconductor companies prioritize secure material access. High technical expertise, certification requirements, and processing capabilities create strong entry barriers. Companies that combine proprietary manufacturing, application-specific engineering, and dependable global supply networks will gain the strongest competitive position.

CPS Technologies Corporation

CeramTec GmbH

Denka Company Limited

Toshiba Materials Co., Ltd.

Kyocera Corporation

CoorsTek, Inc.

Ferrotec Holdings Corporation

Ametek, Inc.

3M

Toyo Aluminium K.K.

Hitachi Metals, Ltd.

Advanced powder metallurgy, pressure infiltration, and precision composite fabrication are driving current aluminum silicon carbide technology adoption. These processes improve reinforcement distribution, thermal stability, and manufacturing consistency by approximately 20%. Automated inspection and digital process monitoring are increasingly integrated into production workflows, with adoption concentrated in semiconductor packaging, aerospace components, and high-power electronics. Companies benefit through reduced defects, improved reliability, and faster qualification cycles.

Emerging technologies include AI-assisted material optimization, advanced particle engineering, and near-net-shape manufacturing. Compared with conventional aluminum alloys, aluminum silicon carbide composites deliver around 25–30% improvement in dimensional stability and thermal performance, creating advantages for EV power modules and electronic heat spreaders. Technology-focused suppliers such as Materion and CPS Technologies benefit as OEMs prioritize customized performance materials over standard metals.

Between 2026 and 2028, disruptive advancements will center on intelligent manufacturing, localized production, and application-specific composite grades. Companies investing in automation and digital quality systems will achieve stronger operational control, shorter development timelines, and improved scalability. The competitive advantage will shift toward manufacturers capable of combining material innovation with reliable supply-chain execution.

January 2024 Materion Corporation received SAE aerospace material specification approval for SupremEX 225XE aluminum silicon carbide composite containing 25 volume percent silicon carbide reinforcement. The certification expanded aerospace adoption opportunities and strengthened qualified supply availability for lightweight structural applications. Source: www.materion.com

September 2025 CPS Technologies expanded its AlSiC product development portfolio with advanced composite manufacturing processes using proprietary infiltration methods. The technology supports high-throughput production of thousands of components weekly and improves thermal management performance for electronic applications. Source: www.cpstechnologysolutions.com

March 2025 Materion continued expanding SupremEX metal matrix composite applications across aerospace, automotive, defense, and electronics sectors. The company highlighted lightweight structures, thermal conductivity benefits, and adjustable thermal expansion characteristics supporting next-generation system designs. Source: www.materion.com

February 2024 Researchers demonstrated silicon carbide integration technologies for advanced electronics platforms, showing improved thermal and photonic performance through engineered SiC structures. The development highlights growing demand for silicon carbide-based materials in future high-performance computing and semiconductor applications.

The Aluminum Silicon Carbide Composite Material Market Report provides comprehensive coverage across material types, applications, end-users, and global regions including North America, Europe, Asia-Pacific, South America, and Middle East & Africa. The study evaluates reinforced composite technologies, semiconductor thermal management, aerospace structures, automotive systems, electronics packaging, and industrial applications.

The report analyzes competitive positioning, manufacturing capabilities, technology adoption patterns, supply-chain developments, and investment opportunities involving key industry participants. Coverage includes mature applications and emerging niches such as EV power electronics, advanced cooling systems, and lightweight aerospace components. The analysis supports strategic decisions related to expansion planning, partnership development, product innovation, and competitive positioning between 2026 and 2033.

CPS Technologies Corporation

CeramTec GmbH

Denka Company Limited

Toshiba Materials Co., Ltd.

Kyocera Corporation

CoorsTek, Inc.

Ferrotec Holdings Corporation

Ametek, Inc.

3M

Toyo Aluminium K.K.

Hitachi Metals, Ltd.

Advanced powder metallurgy, pressure infiltration, and precision composite fabrication are driving current aluminum silicon carbide technology adoption. These processes improve reinforcement distribution, thermal stability, and manufacturing consistency by approximately 20%. Automated inspection and digital process monitoring are increasingly integrated into production workflows, with adoption concentrated in semiconductor packaging, aerospace components, and high-power electronics. Companies benefit through reduced defects, improved reliability, and faster qualification cycles.

Emerging technologies include AI-assisted material optimization, advanced particle engineering, and near-net-shape manufacturing. Compared with conventional aluminum alloys, aluminum silicon carbide composites deliver around 25–30% improvement in dimensional stability and thermal performance, creating advantages for EV power modules and electronic heat spreaders. Technology-focused suppliers such as Materion and CPS Technologies benefit as OEMs prioritize customized performance materials over standard metals.

Between 2026 and 2028, disruptive advancements will center on intelligent manufacturing, localized production, and application-specific composite grades. Companies investing in automation and digital quality systems will achieve stronger operational control, shorter development timelines, and improved scalability. The competitive advantage will shift toward manufacturers capable of combining material innovation with reliable supply-chain execution.

January 2024 Materion Corporation received SAE aerospace material specification approval for SupremEX 225XE aluminum silicon carbide composite containing 25 volume percent silicon carbide reinforcement. The certification expanded aerospace adoption opportunities and strengthened qualified supply availability for lightweight structural applications. Source: www.materion.com

September 2025 CPS Technologies expanded its AlSiC product development portfolio with advanced composite manufacturing processes using proprietary infiltration methods. The technology supports high-throughput production of thousands of components weekly and improves thermal management performance for electronic applications. Source: www.cpstechnologysolutions.com

March 2025 Materion continued expanding SupremEX metal matrix composite applications across aerospace, automotive, defense, and electronics sectors. The company highlighted lightweight structures, thermal conductivity benefits, and adjustable thermal expansion characteristics supporting next-generation system designs. Source: www.materion.com

February 2024 Researchers demonstrated silicon carbide integration technologies for advanced electronics platforms, showing improved thermal and photonic performance through engineered SiC structures. The development highlights growing demand for silicon carbide-based materials in future high-performance computing and semiconductor applications.

The Aluminum Silicon Carbide Composite Material Market Report provides comprehensive coverage across material types, applications, end-users, and global regions including North America, Europe, Asia-Pacific, South America, and Middle East & Africa. The study evaluates reinforced composite technologies, semiconductor thermal management, aerospace structures, automotive systems, electronics packaging, and industrial applications.

The report analyzes competitive positioning, manufacturing capabilities, technology adoption patterns, supply-chain developments, and investment opportunities involving key industry participants. Coverage includes mature applications and emerging niches such as EV power electronics, advanced cooling systems, and lightweight aerospace components. The analysis supports strategic decisions related to expansion planning, partnership development, product innovation, and competitive positioning between 2026 and 2033.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 184 Million |

| Market Revenue (2033) | USD 562.9 Million |

| CAGR (2026–2033) | 15% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Companies Profiled | Materion Corporation; CPS Technologies Corporation; CeramTec GmbH; Denka Company Limited; Toshiba Materials Co., Ltd.; Kyocera Corporation; CoorsTek, Inc.; Ferrotec Holdings Corporation; Ametek, Inc.; 3M; Toyo Aluminium K.K.; Hitachi Metals, Ltd. |

| Customization & Pricing | Available on Request (10% Customization Free) |