Reports

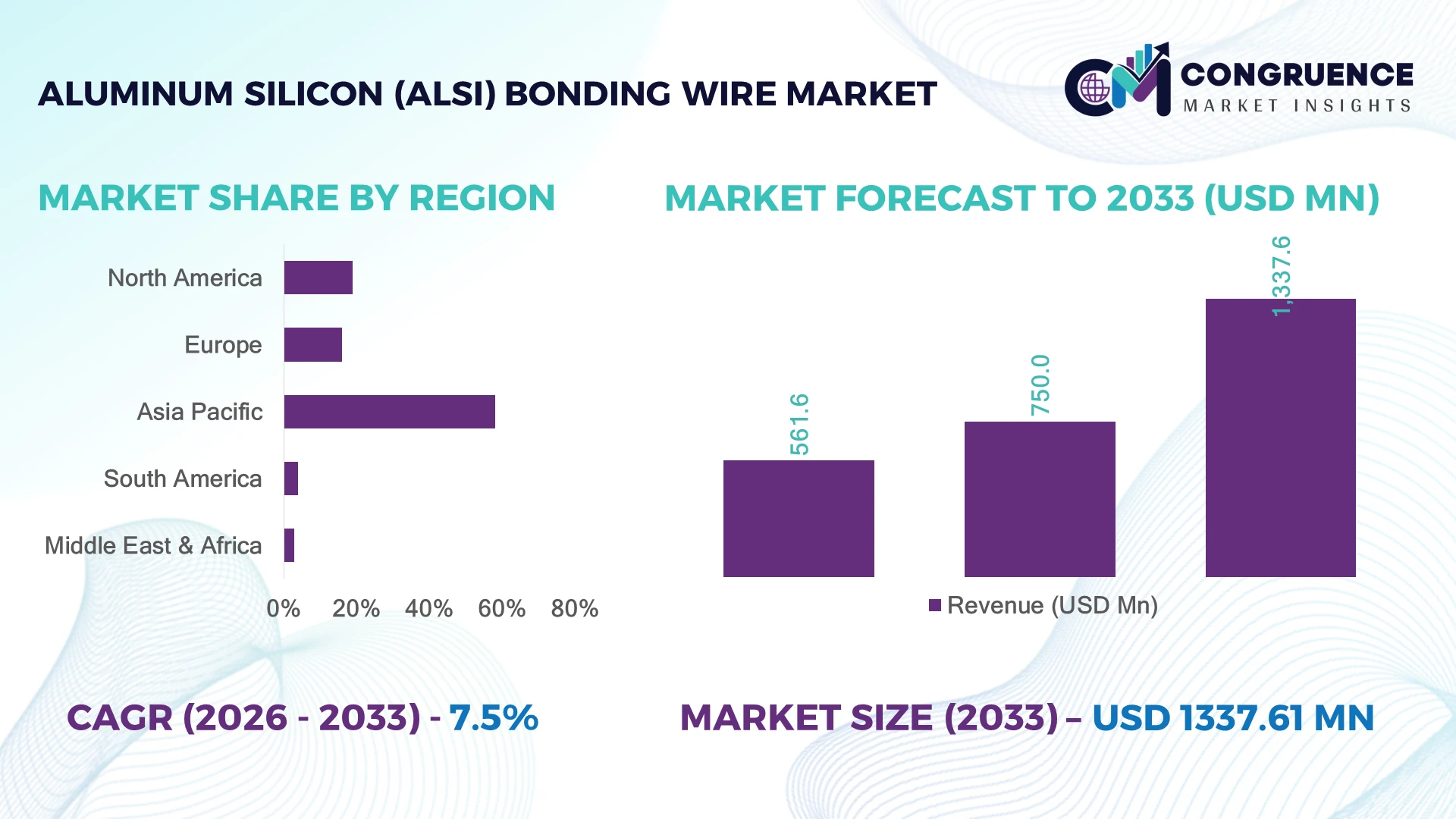

The Global Aluminum Silicon (AlSi) Bonding Wire Market was valued at USD 750 Million in 2025 and is anticipated to reach a value of USD 1,337.6 Million by 2033 expanding at a CAGR of 7.5% between 2026 and 2033. Growth is driven by expanding automotive power electronics production, advanced semiconductor packaging, and the transition toward high-reliability, copper-alternative interconnect solutions for electric vehicles and industrial power modules.

China dominates the market with approximately 38% of global semiconductor packaging capacity, supported by investments exceeding USD 40 billion under national semiconductor initiatives and strong demand from EV, consumer electronics, and industrial automation sectors. Japan remains a technology leader in precision bonding materials, while South Korea accelerates advanced packaging deployment through AI chip manufacturing expansion. Ongoing semiconductor supply-chain realignment following U.S.–China technology restrictions continues reshaping regional manufacturing priorities.

Manufacturers prioritizing localized supply chains, advanced wire metallurgy, and high-performance packaging capabilities are positioned to secure long-term competitive advantages.

Market Size & Growth: USD 750 Million in 2025, projected to reach USD 1,337.6 Million by 2033 at 7.5% CAGR, supported by advanced semiconductor packaging and EV power electronics expansion.

Top Growth Drivers: EV semiconductor demand (+30%), AI chip packaging (+25%), localized semiconductor manufacturing investments (+20%).

Short-Term Forecast: By 2028, bonding efficiency improves by 15% through automation and precision wire-bonding systems.

Emerging Technologies: AI-assisted process control, automated wire bonding, and high-purity AlSi alloy engineering enhance packaging reliability.

Regional Leaders: Asia-Pacific USD 760 Million, North America USD 250 Million, Europe USD 185 Million, each benefiting from semiconductor expansion and supply-chain diversification.

Consumer/End-User Trends: Over 65% of automotive power modules increasingly adopt aluminum-based bonding solutions for higher thermal reliability.

Pilot/Case Example: 2024 advanced packaging upgrades reduced bonding defects by approximately 18% in high-volume semiconductor assembly lines.

Competitive Landscape: Top supplier controls nearly 18% market share; key participants include Heraeus, Tanaka Precious Metals, Sumitomo Metal Mining, MK Electron, and Tatsuta Electric Wire & Cable.

Regulatory & ESG Impact: Energy-efficient manufacturing initiatives lowered production energy intensity by approximately 12% while supporting regional localization strategies.

Investment & Funding: More than USD 8 billion invested globally in advanced semiconductor packaging facilities through strategic partnerships and expansion projects.

Innovation & Future Outlook: Next-generation fine-pitch bonding wires and advanced power-device packaging strengthen global competitiveness amid ongoing semiconductor supply-chain restructuring.

Aluminum Silicon (AlSi) bonding wire demand is accelerating across electric vehicles, industrial power modules, AI processors, and advanced semiconductor packaging where thermal stability and reliability are critical. Fine-diameter wire innovations and precision bonding technologies have improved package consistency by nearly 15%, while regional semiconductor localization programs and resilient supply-chain strategies continue influencing procurement decisions and manufacturing expansion, setting the stage for broader strategic market developments.

The Aluminum Silicon (AlSi) Bonding Wire Market has become strategically important as semiconductor manufacturers prioritize resilient supply chains, localized packaging capabilities, and higher-performance interconnection materials. Expansion of electric mobility, AI computing, industrial automation, and power electronics is reshaping procurement priorities, while government-backed semiconductor manufacturing initiatives across Asia, North America, and Europe are accelerating domestic packaging ecosystems and reducing dependence on concentrated production hubs.

Compared with conventional pure aluminum bonding wire, advanced AlSi variants deliver approximately 20% better resistance to intermetallic degradation and improved high-temperature reliability, lowering package failure rates in demanding automotive and industrial applications. Asia-Pacific continues leading large-scale manufacturing deployment, while North America focuses on advanced packaging innovation and Europe strengthens automotive semiconductor integration. Over the next two to three years, automated bonding systems are expected to increase production throughput by nearly 15% while improving process consistency.

Manufacturers are expanding precision wire production, forming technology partnerships with OSAT providers, and investing in advanced metallurgy to support next-generation semiconductor devices. Sustainability initiatives, including material optimization and energy-efficient manufacturing, further strengthen operational performance. Organizations that combine localized production, advanced packaging expertise, and high-reliability bonding technologies will establish stronger competitive positioning as semiconductor value chains continue to evolve.

The rapid expansion of electric vehicles, AI accelerators, and industrial power electronics is increasing demand for high-reliability Aluminum Silicon (AlSi) bonding wire. More than 65% of automotive power modules continue to rely on aluminum-based interconnects because of superior thermal stability, while advanced packaging adoption has increased by nearly 22% across leading semiconductor assembly facilities. China's semiconductor manufacturing expansion and government-backed localization initiatives are accelerating domestic sourcing following global supply-chain restructuring. This shift is driving manufacturers to invest in finer-diameter AlSi wire, automated production, and higher-purity alloy development. Companies are strengthening partnerships with OSAT providers and expanding specialized production capacity to improve product consistency, reduce defect rates, and secure long-term positions in automotive and industrial semiconductor supply chains.

Production of Aluminum Silicon (AlSi) bonding wire depends on tightly controlled alloy composition and precision processing, making manufacturers vulnerable to raw material price fluctuations and quality inconsistencies. Global aluminum price movements have exceeded 18% during recent supply disruptions, while premium semiconductor-grade wire production requires process yields above 98% to remain commercially viable. Trade restrictions affecting semiconductor materials between the United States and China continue to complicate sourcing strategies for packaging manufacturers. These constraints increase qualification costs, delay production schedules, and pressure operating margins. Companies are responding by diversifying supplier networks, securing long-term procurement agreements, expanding localized manufacturing, and investing in advanced quality-control systems to maintain stable production performance.

Rapid commercialization of silicon carbide and gallium nitride power semiconductors is creating new opportunities for advanced Aluminum Silicon (AlSi) bonding wire designed for higher operating temperatures and improved electrical reliability. More than 30% of newly developed EV inverter platforms are incorporating wide-bandgap devices, while automated semiconductor packaging lines have improved bonding precision by approximately 15%. Japan continues investing in advanced packaging innovation, encouraging development of finer-pitch bonding technologies for high-performance electronics. Manufacturers are expanding R&D programs, collaborating with semiconductor equipment suppliers, and developing customized alloy formulations optimized for advanced chip architectures. An emerging opportunity lies in specialized industrial robotics and renewable-energy power modules, where long operational life increasingly outweighs material cost considerations.

Maintaining consistent wire quality across high-volume production remains a significant long-term execution challenge as semiconductor packaging technologies become increasingly complex. Advanced wire bonding equipment now operates with placement accuracy below 10 microns, while acceptable defect rates must remain under 0.1% for automotive-grade semiconductor qualification. Taiwan's advanced packaging ecosystem is raising industry performance expectations, requiring suppliers to meet increasingly stringent reliability standards across multiple device platforms. Expanding production without compromising metallurgical consistency, workforce expertise, or process repeatability requires substantial investment in automation, inspection technologies, and skilled engineering talent. Companies that successfully integrate digital quality monitoring, AI-driven process optimization, and standardized global manufacturing practices will achieve stronger operational resilience and sustained competitive differentiation.

Ultra-Fine Wire Adoption Accelerates: Semiconductor manufacturers are increasingly deploying ultra-fine AlSi bonding wires below 20 microns, with adoption rising by nearly 24% across advanced packaging facilities. AI processors and automotive chips require higher interconnect density, prompting equipment upgrades and automated wire-bonding workflows. Japanese material suppliers are expanding precision production, enabling improved bonding accuracy, shorter cycle times, and lower defect rates through advanced metallurgical control.

Supply Chain Localization Intensifies: More than 35% of semiconductor packaging companies are expanding localized sourcing strategies to reduce geopolitical exposure and logistics risks. Ongoing technology restrictions between the United States and China continue reshaping procurement decisions, encouraging domestic production partnerships and regional manufacturing investments. Companies are restructuring supplier portfolios, qualifying multiple material vendors, and establishing localized inventory hubs to improve delivery reliability and production continuity.

Automation Enhances Production Stability: Automated wire-bonding systems now improve assembly throughput by approximately 15% while reducing bonding variability by nearly 18% in high-volume semiconductor production. Smart process monitoring and AI-assisted inspection enable predictive quality control, minimizing operator intervention and lowering scrap rates. Leading manufacturers are integrating digital manufacturing platforms to improve operational consistency across multiple production sites.

Power Electronics Specification Upgrades: Electric vehicle inverters and industrial power modules increasingly require enhanced thermal endurance, with over 60% of new power-device platforms specifying high-reliability aluminum-based interconnect materials. Silicon carbide device deployment is accelerating material qualification standards, encouraging suppliers to develop optimized alloy compositions and customized bonding solutions through collaborative engineering programs with semiconductor manufacturers.

Aluminum Silicon Bonding Wire (0.5–1% Si) remains the leading segment, accounting for approximately 54% of market demand because of its balanced electrical conductivity, reliable bond strength, and compatibility with established semiconductor packaging equipment. Its proven manufacturing scalability and cost efficiency make it the preferred solution for automotive, industrial, and consumer semiconductor applications. High Silicon Aluminum Bonding Wire continues gaining traction in high-temperature power devices where improved mechanical stability is essential, while the Others category serves specialized packaging requirements with limited production volumes. Ultra-Fine AlSi Bonding Wire represents the fastest-growing segment as advanced chip packaging requires smaller bonding pitches and higher interconnect density. Adoption has increased by nearly 23% across AI processors and premium automotive semiconductor platforms. Manufacturers are investing in precision drawing technologies, expanding ultra-fine production capacity, and collaborating with equipment suppliers to improve bonding consistency. These investments reflect shifting priorities toward high-value semiconductor applications where reliability, miniaturization, and process precision increasingly determine supplier competitiveness.

Power Semiconductors remain the largest application segment, contributing approximately 46% of total demand as electric vehicles, renewable energy converters, and industrial motor drives require highly reliable interconnection materials capable of operating under elevated thermal conditions. Their operational importance continues expanding as power-device complexity increases. Integrated Circuits (ICs) maintain substantial demand across computing and consumer electronics, while LEDs, Sensors, and RF Devices support diversified adoption in specialized electronic systems requiring stable bonding performance. Integrated Circuits (ICs) represent the fastest-growing application owing to expanding AI processors, advanced packaging technologies, and higher semiconductor integration levels. Advanced IC packaging deployments have increased by around 20%, encouraging manufacturers to automate bonding operations and qualify finer-diameter AlSi wires. Companies continue expanding product portfolios tailored for miniaturized chip architectures while strengthening partnerships with OSAT providers. These developments reinforce the strategic importance of application-specific material optimization across increasingly complex semiconductor manufacturing environments.

Semiconductor Manufacturing remains the dominant end-user segment, representing nearly 52% of market consumption due to continuous wafer fabrication expansion, advanced packaging investments, and increasing production of AI, automotive, and industrial semiconductor devices. High-volume packaging operations require consistent bonding performance and stringent process control, supporting long-term procurement stability. Consumer Electronics maintains mature purchasing activity, while Industrial Electronics and Telecommunications continue adopting specialized AlSi bonding solutions for demanding operational environments. Automotive Electronics is the fastest-growing end-user segment as electric vehicles, battery management systems, and power control modules require durable wire-bond interconnections capable of withstanding thermal cycling. Automotive semiconductor demand has expanded by approximately 28%, prompting suppliers to develop customized alloy formulations and strengthen technical collaborations with Tier-1 component manufacturers. Companies are refining pricing strategies, expanding localized engineering support, and investing in qualification capabilities to capture emerging opportunities in electrified mobility and intelligent vehicle platforms.

Asia-Pacific accounted for the largest market share at 58% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 8.2% between 2026 and 2033.

North America accounted for approximately 19% of the global Aluminum Silicon (AlSi) Bonding Wire Market in 2025, supported by expanding domestic semiconductor manufacturing, advanced packaging investments, and rising production of automotive and AI processors. Public and private investments under semiconductor manufacturing initiatives are accelerating localization of critical packaging materials and reducing import dependency. More than 15 major semiconductor fabrication and packaging expansion projects are progressing across the United States, increasing demand for premium bonding materials. Companies are strengthening partnerships with equipment suppliers, automating packaging operations, and expanding technical support capabilities to improve manufacturing resilience and supply-chain security for high-performance semiconductor applications.

United States Market Outlook: The United States remains the regional leader due to its concentration of advanced semiconductor manufacturers, packaging technology providers, and government-supported manufacturing expansion. Domestic semiconductor investments continue driving qualification of high-reliability bonding materials for AI, defense, and automotive electronics. More than USD 50 billion has been committed to semiconductor manufacturing expansion through public and private initiatives, encouraging suppliers to establish localized production, collaborative R&D programs, and long-term strategic partnerships with wafer fabrication and OSAT facilities.

Europe represented nearly 16% of the global market in 2025, supported by strong automotive semiconductor demand, industrial automation, and advanced power electronics manufacturing. Regional manufacturers emphasize high-quality bonding materials capable of supporting stringent automotive reliability standards and sustainable production practices. Expansion of electric vehicle manufacturing and industrial digitalization has increased demand for advanced semiconductor packaging materials, while several packaging modernization projects continue improving production capabilities. Companies are prioritizing localized sourcing, material innovation, and strategic collaborations with automotive semiconductor suppliers to strengthen manufacturing resilience and technology competitiveness.

Germany Market Outlook: Germany leads the European market through its world-class automotive manufacturing ecosystem, industrial electronics expertise, and growing semiconductor investment activity. Automotive power modules and industrial automation equipment account for a significant share of bonding wire demand. More than 40% of Europe's automotive production remains concentrated in Germany and neighboring manufacturing hubs, encouraging suppliers to expand engineering support, application-specific product development, and partnerships with automotive semiconductor manufacturers focused on electrified mobility.

Asia-Pacific held the largest market share of approximately 58% in 2025 owing to its unmatched semiconductor manufacturing capacity, integrated supply chains, and concentration of OSAT facilities. China, Taiwan, Japan, and South Korea collectively account for the majority of global semiconductor packaging operations, creating sustained demand for Aluminum Silicon bonding wire across consumer electronics, automotive, and industrial applications. Continuous investment in advanced packaging facilities, export-oriented manufacturing, and precision metallurgy strengthens production competitiveness. Manufacturers are expanding ultra-fine wire capacity, improving automation, and increasing localized raw material processing to support evolving semiconductor technologies.

China Market Outlook: China remains the largest national market because of extensive semiconductor manufacturing infrastructure, rapidly expanding packaging capacity, and significant investment in domestic semiconductor self-sufficiency. The country contributes approximately 38% of global semiconductor packaging capacity while continuously expanding production for electric vehicles, industrial electronics, and consumer devices. Local manufacturers are increasing investments in precision alloy production, automated wire manufacturing, and technology partnerships to strengthen supply-chain independence and improve competitiveness in advanced semiconductor materials.

South America accounted for approximately 4% of the global market in 2025, with demand supported by expanding electronics assembly, industrial automation, and automotive component manufacturing. While large-scale semiconductor fabrication remains limited, increasing localization of electronics production is encouraging greater adoption of advanced packaging materials. Government incentives supporting industrial modernization and manufacturing diversification are gradually strengthening regional demand. Companies are responding by expanding regional distribution networks, developing technical service capabilities, and collaborating with electronics manufacturers to improve supply availability despite infrastructure and logistics constraints.

Brazil Market Outlook: Brazil represents the region's largest market due to its established electronics manufacturing base, automotive production, and industrial modernization initiatives. The country's growing demand for automotive control systems and industrial electronics continues supporting consumption of semiconductor packaging materials. Electronics manufacturing contributes substantially to national industrial output, encouraging suppliers to strengthen local inventories, technical partnerships, and customer support capabilities while improving supply-chain responsiveness for high-value electronic component manufacturers.

The Middle East & Africa represented approximately 3% of the global market in 2025, driven by industrial diversification programs, digital infrastructure investments, and increasing electronics manufacturing activity. Although semiconductor production remains limited, rising demand for telecommunications infrastructure, industrial automation, and smart manufacturing solutions is creating opportunities for advanced electronic materials. Several technology parks and industrial development initiatives continue attracting electronics assembly investments. Suppliers are strengthening regional partnerships, improving technical distribution networks, and supporting localized electronics production through specialized material availability and engineering services.

United Arab Emirates Market Outlook: The United Arab Emirates leads regional market development through advanced industrial infrastructure, logistics connectivity, and technology-focused economic diversification. Strategic investments in smart manufacturing, electronics assembly, and digital infrastructure continue strengthening demand for semiconductor-related materials. More than 20 specialized industrial and technology zones support electronics manufacturing activities, encouraging global suppliers to establish regional partnerships, warehousing operations, and technical support centers serving customers across the Middle East and Africa.

The Aluminum Silicon (AlSi) Bonding Wire Market is led by Heraeus, TANAKA Precious Metals, Sumitomo Metal Mining, MK Electron, and Tatsuta Electric Wire & Cable, with the top five players collectively controlling approximately 63% of global demand. Competition is centered between global technology leaders offering premium reliability and regional manufacturers competing through cost efficiency and localized supply. Performance differentiation depends on ultra-fine wire capability, bond reliability, customized alloy formulations, and delivery resilience, while automated production improves manufacturing efficiency by nearly 15% and localized sourcing reduces lead times by around 20%. Companies are expanding production in Asia, strengthening OSAT partnerships, investing in advanced metallurgy, and integrating quality inspection with digital manufacturing systems. The competitive landscape is shifting toward high-density semiconductor packaging, where material performance increasingly outweighs price advantages. Stringent automotive qualification requirements and precision manufacturing expertise remain significant entry barriers. Winning requires advanced material engineering, resilient multi-site production, rapid customer qualification, and sustained investment in packaging innovation.

TANAKA Precious Metals

Sumitomo Metal Mining Co., Ltd.

MK Electron Co., Ltd.

Tatsuta Electric Wire & Cable Co., Ltd.

Nippon Micrometal Corporation

AMETEK, Inc.

Nippon Steel Chemical & Material Co., Ltd.

Doublink Solders Ltd.

Yantai Zhaojin Kanfort Precious Metals Co., Ltd.

Yantai YesNo Electronic Materials Co., Ltd.

Kangqiang Electronics Co., Ltd.

Advanced Aluminum Silicon (AlSi) bonding wire technology is rapidly evolving toward ultra-fine diameters, precision alloy engineering, and AI-enabled manufacturing. Wire diameters below 20 μm are increasingly deployed in advanced semiconductor packaging, improving interconnect density by nearly 22% while supporting next-generation AI processors and automotive power devices. Approximately 60% of leading semiconductor packaging facilities have expanded automated bonding operations to improve repeatability and reduce manual process variation.

Compared with conventional aluminum bonding wire, optimized AlSi alloys deliver nearly 20% greater resistance to intermetallic degradation and around 15% higher high-temperature reliability under demanding operating conditions. AI-assisted inspection systems reduce bonding defects by approximately 18%, while inline digital process monitoring enables predictive quality control and faster production adjustments. Technology leaders and advanced OSAT providers benefit most through higher yields, shorter qualification cycles, and stronger automotive-grade compliance.

Between 2026 and 2028, hybrid automation, digital twins, machine-vision inspection, and customized alloy formulations will become mainstream across semiconductor packaging facilities. Suppliers investing in advanced metallurgy, precision drawing technology, and integrated manufacturing analytics will strengthen competitive positioning as chip architectures become increasingly complex. Organizations adopting these technologies early will achieve superior production consistency, faster customer qualification, and greater resilience against evolving semiconductor manufacturing requirements.

March 2024 – TANAKA Precious Metals established AuRoFUSE™ bonding technology enabling 4 μm fine-pitch semiconductor mounting with 20 μm bumps, supporting higher-density chip packaging and improved thermal performance for advanced electronics. Source: www.tanaka-preciousmetals.com

September 2025 – TANAKA Electronics showcased advanced bonding wire technologies at SEMICON India 2025, highlighting an ultra-thin 10 μm bonding wire development and its multi-site manufacturing strategy to strengthen supply-chain resilience for semiconductor customers. Source: www.tanaka.com

July 2025 – MK Electron announced progress toward customer qualification of its palladium alloy wire (PAW) for semiconductor pogo pins, targeting market expansion dominated by Japanese suppliers and strengthening its advanced interconnect portfolio.

May 2025 – Heraeus Electronics introduced recycled gold bonding wire solutions and 18 μm vertical wire bonding technology for advanced memory packaging, strengthening sustainability and high-density semiconductor integration strategies.

This report provides comprehensive analysis of the Aluminum Silicon (AlSi) Bonding Wire Market across four product types, six application segments, and six end-user categories, supported by detailed assessments of North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. The study evaluates manufacturing trends, semiconductor packaging developments, advanced bonding technologies, supply-chain evolution, automation adoption, and enterprise investment priorities. More than 50% of market demand remains concentrated within semiconductor manufacturing, while advanced power electronics continue strengthening deployment across multiple industries.

The report delivers strategic intelligence covering competitive positioning, technology innovation, regional manufacturing capabilities, localization strategies, and emerging high-value opportunities between 2026 and 2033. It also examines deployment patterns, evolving customer requirements, advanced packaging adoption, and company expansion initiatives, enabling stakeholders to support investment planning, product development, market entry, capacity expansion, partnership evaluation, and long-term competitive decision-making within the global semiconductor materials ecosystem.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 750 Million |

| Market Revenue (2033) | USD 1,337.6 Million |

| CAGR (2026–2033) | 7.5% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Heraeus; TANAKA Precious Metals; Sumitomo Metal Mining Co., Ltd.; MK Electron Co., Ltd.; Tatsuta Electric Wire & Cable Co., Ltd.; Nippon Micrometal Corporation; AMETEK, Inc.; Nippon Steel Chemical & Material Co., Ltd.; Doublink Solders Ltd.; Yantai Zhaojin Kanfort Precious Metals Co., Ltd.; Yantai YesNo Electronic Materials Co., Ltd.; Kangqiang Electronics Co., Ltd. |

| Customization & Pricing | Available on Request (10% Customization Free) |