Reports

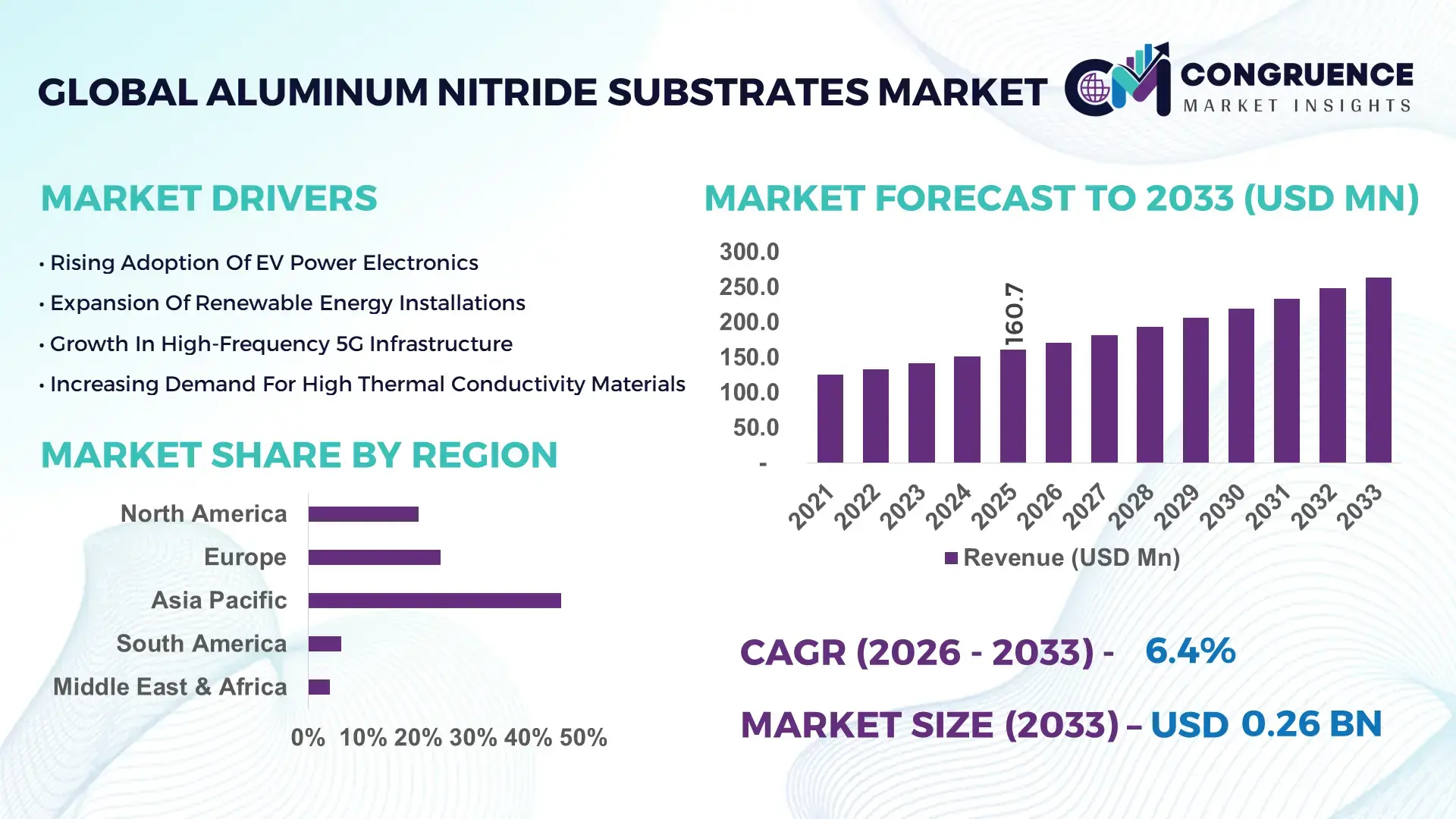

The Global Aluminum Nitride Substrates Market was valued at USD 160.7 Million in 2025 and is anticipated to reach a value of USD 264.0 Million by 2033 expanding at a CAGR of 6.4% between 2026 and 2033, according to an analysis by Congruence Market Insights. This growth is primarily driven by increasing demand for high-thermal-conductivity ceramic substrates in power electronics and advanced semiconductor packaging.

Japan continues to lead the Aluminum Nitride Substrates Market in terms of production scale, technological innovation, and high-performance material engineering. The country operates multiple advanced ceramic manufacturing facilities with annual output capacities exceeding 2,500 metric tons of high-purity aluminum nitride powder and sintered substrates. Over 65% of domestic production is allocated to automotive power modules, industrial IGBT modules, and RF components. Japanese manufacturers have developed aluminum nitride substrates with thermal conductivity levels above 170 W/mK and dielectric strength exceeding 15 kV/mm, enabling next-generation EV inverters and 5G infrastructure systems. Capital investments in precision ceramic sintering technologies and automated tape casting lines have improved yield rates by nearly 12% over the past three years.

Market Size & Growth: USD 160.7 Million in 2025, projected to reach USD 264.0 Million by 2033, expanding at 6.4% CAGR due to rising adoption in power semiconductor modules and EV applications.

Top Growth Drivers: 48% surge in EV power module demand, 35% increase in 5G base station deployment, 28% growth in industrial automation systems.

Short-Term Forecast: By 2028, advanced aluminum nitride substrates are expected to improve heat dissipation efficiency by 18% in high-voltage modules.

Emerging Technologies: Direct Bonded Copper (DBC) enhancements, high-purity nano-powder processing, and ultra-thin ceramic substrate engineering below 0.25 mm thickness.

Regional Leaders: Asia-Pacific projected above USD 120 Million by 2033; Europe above USD 65 Million driven by EV production; North America above USD 50 Million supported by defense electronics demand.

Consumer/End-User Trends: Automotive OEMs account for over 40% of substrate consumption; industrial drives and renewable inverters exceed 30%.

Pilot Example: In 2025, a European EV manufacturer reported 14% improvement in inverter efficiency using advanced aluminum nitride substrates.

Competitive Landscape: Top manufacturer holds approximately 22% share, followed by 4 major ceramic substrate producers with combined share exceeding 60%.

Regulatory & ESG Impact: Adoption supported by energy efficiency directives targeting 20% reduction in power loss in industrial systems.

Investment Patterns: Over USD 300 Million invested globally in advanced ceramic substrate manufacturing expansion between 2023–2025.

Innovation Outlook: Integration with SiC and GaN power devices accelerating multilayer aluminum nitride substrate development.

Aluminum Nitride Substrates are extensively used in automotive power electronics (approx. 42%), renewable energy inverters (21%), RF communication modules (17%), and industrial automation systems (12%). Continuous innovations in thin-film metallization, improved sintering uniformity, and environmentally optimized ceramic processing are reshaping product performance benchmarks while aligning with global electrification and decarbonization initiatives.

The Aluminum Nitride Substrates Market holds strategic importance in high-power density semiconductor packaging, particularly as electrification and high-frequency applications intensify. Aluminum nitride substrates deliver thermal conductivity above 170 W/mK compared to traditional alumina substrates at approximately 25 W/mK, representing more than 6x improvement in heat dissipation efficiency. This thermal advantage supports compact inverter modules, high-voltage SiC MOSFETs, and next-generation RF amplifiers.

Asia-Pacific dominates in volume due to extensive automotive electronics manufacturing clusters, while Europe leads in advanced EV adoption with over 30% of electric vehicle production integrating high-performance ceramic substrates. By 2027, silicon carbide-based power modules are expected to improve overall inverter efficiency by 15%, directly increasing demand for thermally optimized aluminum nitride substrates.

Firms are committing to ESG metrics targeting 25% reduction in manufacturing energy intensity by 2030 through optimized sintering furnaces and reduced ceramic waste. In 2024, a Japanese ceramic producer improved yield rates by 10% through AI-assisted temperature control systems in high-temperature sintering lines, enhancing uniformity and reducing material scrap.

As global electrification accelerates, the Aluminum Nitride Substrates Market is emerging as a critical pillar of resilient power infrastructure, enabling energy efficiency, regulatory compliance, and sustainable semiconductor integration across automotive, industrial, and telecom sectors.

The Aluminum Nitride Substrates Market is influenced by rapid electrification, high-frequency communication infrastructure, and advanced power semiconductor integration. Growing adoption of silicon carbide (SiC) and gallium nitride (GaN) devices has increased the need for substrates with superior thermal conductivity and low dielectric loss. Electric vehicles now incorporate inverters operating above 800V systems, requiring ceramic substrates capable of handling high thermal stress and voltage stability.

Industrial automation systems integrating high-power drives and robotics require efficient heat dissipation to maintain operational reliability. Additionally, deployment of over 3 million 5G base stations globally has driven demand for thermally stable RF packaging substrates. Increasing investments in renewable energy inverters and grid-tied power electronics further strengthen market momentum.

Electrification across transportation and industrial sectors is significantly boosting Aluminum Nitride Substrates demand. EV production exceeded 14 million units globally in 2024, with each vehicle integrating multiple high-voltage power modules. Aluminum nitride substrates improve thermal management efficiency by up to 20% compared to traditional ceramic materials, reducing module failure rates and enhancing inverter lifespan.

Industrial renewable installations surpassed 400 GW of new capacity additions, requiring advanced power conversion modules. These systems operate under high switching frequencies above 20 kHz, demanding thermally conductive ceramic platforms. As grid modernization projects expand, aluminum nitride substrates play a crucial role in supporting stable power electronics performance.

The Aluminum Nitride Substrates Market faces challenges due to energy-intensive sintering processes that require temperatures exceeding 1,700°C. Production complexity, high raw material purity requirements above 99%, and advanced metallization processes increase overall manufacturing cost by approximately 18% compared to conventional alumina substrates.

Limited global suppliers of high-quality aluminum nitride powder and stringent quality control requirements for power electronics applications further constrain supply scalability. Small-volume orders from niche sectors such as aerospace also increase per-unit cost burdens, limiting broader adoption in cost-sensitive applications.

The integration of SiC and GaN power semiconductors creates substantial growth opportunities for Aluminum Nitride Substrates. SiC device shipments increased by over 35% in 2024, requiring substrates capable of managing high thermal flux densities above 300 W/cm². Aluminum nitride substrates offer excellent compatibility with direct bonded copper technology, enhancing current carrying capacity.

Emerging 800V and 1,200V EV platforms demand improved insulation and thermal cycling reliability, positioning aluminum nitride substrates as a preferred solution. Expansion of smart grids and data center power management systems also creates new application avenues for multilayer ceramic substrates.

Raw material price fluctuations and limited global production of high-purity aluminum nitride powder pose significant challenges. Supply disruptions can increase production lead times by up to 15%, impacting downstream semiconductor assembly schedules.

Additionally, maintaining consistent thermal conductivity above 170 W/mK requires precise grain structure control, which can be affected by minor variations in powder composition. Global trade policies and export controls on advanced materials also add regulatory complexity for cross-border semiconductor supply chains.

• Expansion of SiC-Based Power Modules: Adoption of silicon carbide devices increased by 35% in 2024, boosting aluminum nitride substrate integration in EV inverters by nearly 22%. Thermal stress tolerance above 300°C junction temperatures enhances system durability in high-voltage platforms.

• Growth in Renewable Energy Converters: Over 400 GW of renewable capacity additions globally require advanced inverter modules. Aluminum nitride substrates improved heat dissipation efficiency by 18% in solar string inverters, supporting longer operational lifespans exceeding 20 years.

• Development of Ultra-Thin Ceramic Substrates: Substrate thickness below 0.25 mm increased adoption in compact RF modules by 16%, enabling improved signal integrity and reduced dielectric loss in high-frequency telecom equipment.

• Advanced Metallization and DBC Integration: Direct bonded copper layers exceeding 300 µm thickness enhanced current carrying capacity by 20%, improving power module efficiency and reducing conduction losses in industrial drive systems.

The Aluminum Nitride Substrates Market is segmented by type, application, and end-user, reflecting its critical role in advanced power electronics and high-frequency semiconductor packaging. By type, Direct Bonded Copper (DBC) aluminum nitride substrates dominate overall demand, followed by Active Metal Brazed (AMB) substrates and metallized aluminum nitride substrates. These configurations support thermal conductivity levels exceeding 170 W/mK and dielectric strengths above 15 kV/mm, making them suitable for high-voltage systems.

From an application perspective, automotive power modules account for approximately 42% of total consumption, driven by 800V EV architectures and SiC-based inverter systems. Renewable energy inverters and industrial motor drives collectively contribute nearly 33%, while RF and microwave communication modules represent about 15%. Aerospace, defense, and medical electronics together account for the remaining 10%, focusing on high-reliability ceramic packaging.

End-user segmentation highlights automotive OEMs and Tier-1 suppliers as primary adopters, supported by increasing electrification targets. Industrial automation integrators and renewable energy EPC contractors represent growing adoption clusters, particularly in regions expanding grid modernization and smart manufacturing capabilities.

The Aluminum Nitride Substrates Market by type includes Direct Bonded Copper (DBC) Substrates, Active Metal Brazed (AMB) Substrates, and Metallized Aluminum Nitride Substrates. DBC aluminum nitride substrates currently account for approximately 48% of total adoption, primarily due to their superior current-carrying capacity and strong copper-to-ceramic bonding reliability. AMB substrates represent about 32%, offering enhanced thermal cycling durability in high-power density modules. Metallized substrates contribute roughly 20%, serving precision RF and sensor applications requiring fine-line circuitry.

However, AMB aluminum nitride substrates are expanding fastest, with an estimated CAGR of 7.1%, supported by growing SiC and GaN power device integration in electric vehicle inverters and industrial converters. While DBC substrates remain dominant in volume, AMB solutions are gaining traction due to improved thermal fatigue resistance exceeding 10,000 power cycles. The remaining metallized variants continue to serve niche applications, especially in aerospace and microwave systems, maintaining combined relevance of around one-fifth of total demand.

Automotive Power Modules represent the leading application in the Aluminum Nitride Substrates Market, accounting for approximately 42% of global demand. Modern EV platforms integrate high-voltage inverters operating above 800V, requiring substrates capable of managing junction temperatures exceeding 300°C. Renewable Energy Inverters follow with nearly 21%, driven by solar and wind installations surpassing 400 GW of new annual capacity additions. Industrial Motor Drives and Robotics systems contribute about 12%, leveraging aluminum nitride substrates for high-efficiency power conversion.

Telecom RF and 5G infrastructure applications represent the fastest-growing segment, expanding at an estimated CAGR of 6.8%, supported by global deployment of more than 3 million 5G base stations. Aerospace, defense, and medical electronics collectively account for around 10%, focusing on mission-critical reliability and high dielectric strength.

In 2025, more than 38% of industrial enterprises globally reported integrating advanced thermal management substrates in next-generation power electronics platforms. Additionally, 42% of automotive manufacturers are transitioning toward zonal electronic architectures requiring higher-performance ceramic substrate integration.

Automotive OEMs and Tier-1 suppliers represent the leading end-user segment in the Aluminum Nitride Substrates Market, contributing approximately 42% of total consumption. A single electric vehicle platform integrates multiple power modules, each utilizing ceramic substrates capable of sustaining high switching frequencies above 20 kHz. Renewable energy system manufacturers account for roughly 21%, reflecting growth in solar string inverters and grid-scale power converters.

Industrial automation equipment manufacturers represent about 18%, driven by smart factory deployments and robotics installations exceeding 1 million active units worldwide. Telecom infrastructure providers are the fastest-growing end-user group, expanding at an estimated CAGR of 6.5%, supported by increasing RF module density and base station power upgrades. Aerospace and defense contractors collectively contribute around 9%, emphasizing high-reliability and thermal shock resistance performance.

In 2025, over 40% of global automotive manufacturers reported increasing use of high-conductivity ceramic substrates to enhance inverter durability. Furthermore, approximately 36% of renewable energy integrators are upgrading to advanced aluminum nitride substrates to improve thermal stability in grid-tied systems.

Asia-Pacific accounted for the largest market share at 46% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 7.2% between 2026 and 2033.

Asia-Pacific’s leadership is supported by concentrated ceramic substrate manufacturing clusters across China, Japan, South Korea, and Taiwan, collectively operating more than 120 advanced ceramic production lines dedicated to aluminum nitride substrates. China alone contributes over 55% of regional volume consumption, driven by EV production exceeding 9 million units annually and solar inverter installations surpassing 200 GW cumulative capacity.

Japan remains a key innovation hub, supplying high-thermal-conductivity substrates above 170 W/mK for automotive and industrial power modules. South Korea and Taiwan strengthen regional integration through semiconductor packaging ecosystems supporting over 60% of global advanced chip assembly. Meanwhile, North America’s growth trajectory is fueled by more than USD 50 billion in semiconductor and power electronics investments, expansion of SiC device fabrication, and increased grid modernization projects exceeding 25 GW of annual renewable installations. Europe holds approximately 28% share, anchored by Germany and France’s automotive electrification strategies, while South America and Middle East & Africa collectively account for around 9%, driven by renewable infrastructure and industrial modernization initiatives.

How Is Advanced Power Electronics Expansion Reshaping High-Thermal Ceramic Adoption?

North America represents approximately 20% of the global Aluminum Nitride Substrates Market volume, supported by strong demand from electric vehicle manufacturers, aerospace integrators, and renewable energy system developers. The United States leads regional adoption, with EV production exceeding 1.3 million units annually and over 30 GW of utility-scale solar installations added in 2025. Federal incentives promoting domestic semiconductor fabrication and power electronics localization have accelerated investment in ceramic substrate integration for SiC-based modules.

Technological advancements include increased deployment of 800V EV architectures and grid-tied inverter systems operating above 1,200V. A notable regional player, CoorsTek, continues to expand high-performance ceramic manufacturing capacity, delivering precision aluminum nitride substrates for defense and industrial electronics applications. Regional consumer behavior reflects higher enterprise adoption in automotive electrification and aerospace reliability standards, with more than 58% of power electronics OEMs prioritizing domestically sourced high-conductivity ceramic substrates to enhance supply chain resilience.

Why Is Sustainability-Led Electrification Accelerating Ceramic Substrate Integration?

Europe accounts for approximately 24% of total Aluminum Nitride Substrates Market demand, driven primarily by Germany, France, and Italy. Germany alone contributes nearly 40% of regional automotive power module consumption, supported by EV production exceeding 1 million units annually. European Union carbon reduction targets mandate a 55% emission cut by 2030, encouraging rapid electrification of transport and grid systems.

Adoption of emerging technologies such as SiC-based traction inverters and high-frequency power converters is increasing substrate utilization per vehicle by nearly 18%. A key European ceramics specialist, CeramTec, supplies aluminum nitride substrates engineered for thermal management in industrial drives and renewable inverters. Regulatory pressure across the region encourages energy-efficient, thermally stable materials, leading to growing demand for explainable and performance-certified Aluminum Nitride Substrates. Approximately 52% of European renewable energy integrators are upgrading to advanced ceramic-based thermal platforms in next-generation inverter designs.

What Factors Are Driving Large-Scale Manufacturing and High-Volume Power Module Integration?

Asia-Pacific ranks first in market volume, contributing nearly 46% of global Aluminum Nitride Substrates consumption. China, Japan, and South Korea are the top consuming countries, collectively representing over 80% of regional demand. China’s EV output exceeding 9 million units and inverter manufacturing capacity above 250 GW annually significantly elevate substrate requirements. Japan remains a technological leader in high-purity aluminum nitride ceramics exceeding 99% material purity standards.

Regional infrastructure expansion includes more than 3 million 5G base stations and continued semiconductor packaging investment exceeding USD 70 billion across fabrication and backend facilities. A prominent Japanese manufacturer, Maruwa Co., produces high-thermal-conductivity aluminum nitride substrates exceeding 180 W/mK for advanced automotive and communication modules. Regional behavior reflects manufacturing-driven procurement strategies, with over 65% of power module producers vertically integrating ceramic substrate sourcing to secure long-term supply stability.

How Is Renewable Infrastructure Expansion Influencing High-Performance Ceramic Demand?

South America represents approximately 6% of the global Aluminum Nitride Substrates Market, with Brazil and Argentina as key contributors. Brazil accounts for nearly 60% of regional demand, supported by wind and solar capacity exceeding 50 GW combined installations. Industrial automation growth and grid modernization projects are increasing high-voltage inverter deployment across mining and manufacturing sectors.

Government-backed renewable incentives and import substitution policies are encouraging localized assembly of power electronics components. While large-scale ceramic manufacturing remains limited, regional system integrators increasingly rely on imported high-conductivity substrates for advanced power modules. Consumer behavior trends indicate strong demand tied to renewable energy expansion and electrified public transport initiatives across major metropolitan regions.

Can Infrastructure Modernization and Energy Diversification Drive Ceramic Substrate Adoption?

Middle East & Africa accounts for approximately 4% of global Aluminum Nitride Substrates demand. The United Arab Emirates and South Africa lead regional adoption, supported by renewable energy projects exceeding 10 GW in combined solar capacity. Regional diversification strategies aimed at reducing hydrocarbon dependency are accelerating high-efficiency inverter deployment.

Technological modernization trends include smart grid development and industrial power conversion upgrades. Several free trade agreements and advanced manufacturing initiatives are promoting electronics assembly localization. Regional procurement behavior prioritizes thermally robust and high-voltage-resistant materials, especially for harsh environmental conditions exceeding 50°C ambient temperatures. Aluminum nitride substrates are increasingly integrated into high-reliability power electronics serving oil & gas automation and renewable megaprojects.

China – 34% share: China dominates the Aluminum Nitride Substrates Market due to large-scale EV production exceeding 9 million units annually and high-volume inverter manufacturing capacity above 250 GW.

Japan – 21% share: Japan maintains leadership in high-purity aluminum nitride substrate production with advanced ceramic fabrication facilities supporting automotive and semiconductor packaging ecosystems.

The Aluminum Nitride Substrates Market exhibits a moderately consolidated competitive structure, with the top five manufacturers accounting for approximately 55% of total global supply. More than 40 active ceramic substrate producers operate worldwide, though advanced high-thermal-conductivity production above 170 W/mK remains concentrated among fewer than 12 companies. Market leaders emphasize vertical integration, material purity exceeding 99%, and precision metallization technologies to enhance competitive positioning.

Strategic initiatives include capacity expansions exceeding 15% annually in Asia-Pacific manufacturing hubs, joint ventures with SiC device manufacturers, and advanced AMB substrate development for 1,200V–1,700V applications. Innovation trends focus on reducing thermal resistance by 10–15% through improved copper bonding processes and enhanced surface finishing techniques. Competitive intensity is also driven by increasing demand from EV OEMs and renewable integrators, which collectively account for over 60% of global substrate procurement. Companies prioritizing automated sintering processes and advanced thermal simulation capabilities maintain stronger margins and long-term supply agreements.

Kyocera Corporation

Toshiba Materials Co., Ltd.

Denka Company Limited

Rogers Corporation

Hitachi Metals Ltd.

Leatec Fine Ceramics Co., Ltd.

Stellar Industries Corp.

MTI Corporation

Nanjing Zhongjiang New Material Science & Technology Co., Ltd.

Tong Hsing Electronic Industries Ltd.

Zhejiang Xinna Electronic Technology Co., Ltd.

Technological evolution in the Aluminum Nitride Substrates Market centers on enhancing thermal conductivity, mechanical reliability, and copper bonding strength. Modern aluminum nitride ceramics achieve thermal conductivity levels between 170–200 W/mK, significantly outperforming alumina substrates, which typically range below 30 W/mK. Advanced AMB processes improve copper adhesion strength beyond 35 MPa, reducing delamination risk in high-power cycling environments.

Emerging technologies include nano-powder sintering methods that reduce porosity below 1%, enabling improved dielectric strength above 15 kV/mm. High-temperature co-fired ceramic processing supports integration of multilayer circuits capable of handling 1,700V power modules. Automation in substrate polishing and laser patterning increases dimensional accuracy within ±10 microns, supporting miniaturized inverter architectures.

Integration with SiC and GaN devices is accelerating demand for substrates capable of managing junction temperatures exceeding 300°C. Furthermore, simulation-driven thermal management software reduces prototype development time by nearly 20%, improving design efficiency for automotive OEMs. Sustainability initiatives are driving adoption of low-energy sintering furnaces capable of reducing energy consumption by 12% per production cycle. These technological advancements collectively position aluminum nitride substrates as a core enabler of next-generation electrification, high-frequency power conversion, and advanced semiconductor packaging ecosystems.

• In February 2025, Maruwa Co., Ltd. expanded its ceramic substrate production capacity at its Japan facility to support rising EV power module demand, increasing output by approximately 20% and enhancing thermal conductivity optimization for 800V inverter applications. Source: www.maruwa-g.com

• In October 2024, CeramTec announced the expansion of its high-performance ceramics manufacturing line in Europe, focusing on aluminum nitride substrates for renewable inverter systems and advanced industrial drives. The project enhances precision metallization capabilities for high-voltage modules. Source: www.ceramtec-group.com

• In March 2025, CoorsTek introduced advanced aluminum nitride substrates engineered for aerospace and defense electronics, offering improved thermal shock resistance and dielectric stability for mission-critical power systems. Source: www.coorstek.com

• In December 2024, Denka Company Limited enhanced its aluminum nitride powder processing technology, achieving improved material purity above 99% for high-power semiconductor packaging applications. Source: www.denka.co.jp

The Aluminum Nitride Substrates Market Report comprehensively evaluates global demand across automotive, renewable energy, industrial automation, telecom, aerospace, and medical electronics sectors. The report analyzes key substrate types including Direct Bonded Copper (DBC), Active Metal Brazed (AMB), and metallized aluminum nitride variants, highlighting performance benchmarks such as thermal conductivity exceeding 170 W/mK and dielectric strength above 15 kV/mm.

Geographically, the study covers Asia-Pacific, North America, Europe, South America, and Middle East & Africa, representing over 95% of global production and consumption. It examines power module integration trends in EV platforms exceeding 800V architectures, renewable inverter systems above 1,200V, and semiconductor packaging facilities operating at advanced node technologies.

The report further explores supply chain structures, including ceramic powder processing, sintering, copper bonding, and surface metallization processes. It evaluates more than 40 active global manufacturers and identifies technology adoption trends such as AMB process expansion, nano-sintering innovation, and multilayer ceramic integration.

End-user analysis encompasses automotive OEMs, renewable EPC contractors, industrial equipment manufacturers, telecom infrastructure providers, and aerospace integrators. Emerging niche segments such as high-frequency RF modules and high-voltage data center power supplies are also assessed, providing a structured and data-driven overview tailored for decision-makers seeking actionable intelligence on thermal management and power electronics materials strategies.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 160.7 Million |

|

Market Revenue in 2033 |

USD 264.0 Million |

|

CAGR (2026 - 2033) |

6.4% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Maruwa Co., Ltd., CeramTec GmbH, CoorsTek, Inc., Kyocera Corporation, Toshiba Materials Co., Ltd., Denka Company Limited, Rogers Corporation, Hitachi Metals Ltd., Leatec Fine Ceramics Co., Ltd., Stellar Industries Corp., MTI Corporation, Nanjing Zhongjiang New Material Science & Technology Co., Ltd., Tong Hsing Electronic Industries Ltd., Zhejiang Xinna Electronic Technology Co., Ltd. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |